|

시장보고서

상품코드

2073014

독일의 농업용 분무기 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Germany Agricultural Sprayers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

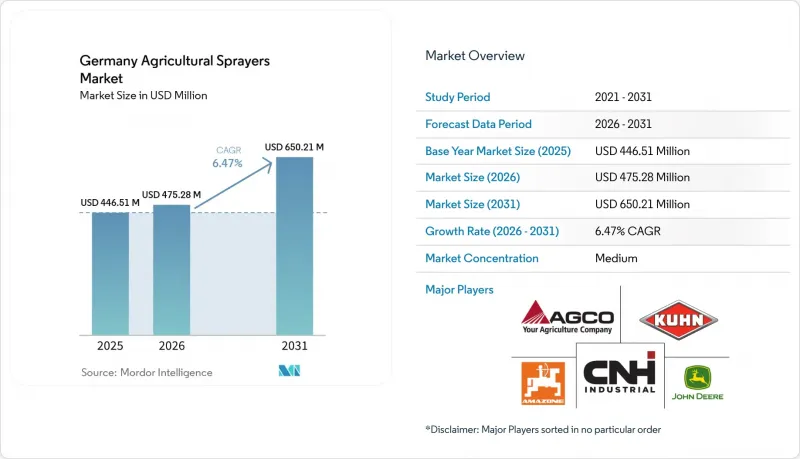

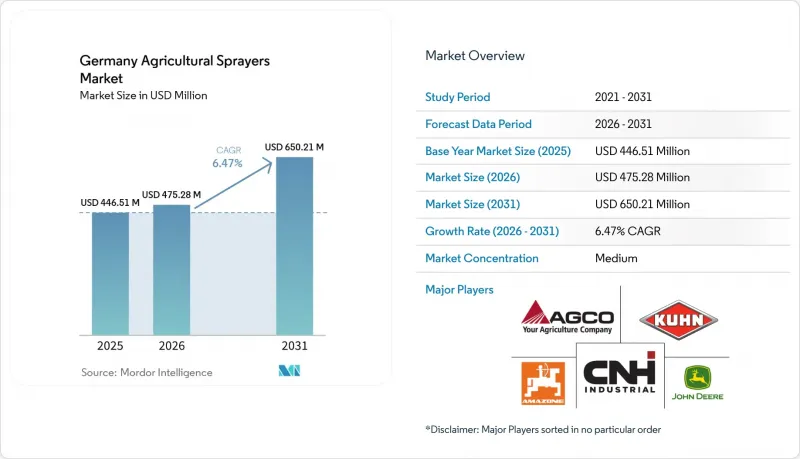

Mordor Intelligence에 의하면, 독일 농업용 분무기 시장 규모는 2025년 4억 4,651만 달러, 2026년 4억 7,528만 달러에서 2031년까지 6억 5,021만 달러로 확대한다고 추정되고 있어 2026년부터 2031년까지 CAGR 6.47%로 성장할 전망입니다.

본 보고서는 제품 유형(휴대용 분무기, 트랙터 탑재형 분무기, 견인식 분무기 등), 동력원(수동식, 태양광 발전식, 연료 구동식 등), 용도(밭작물, 과수원·포도원 등), 기술 수준(기존, 정밀 살포·GPS 유도형 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

독일 농업용 분무기 시장 동향 및 분석

드리프트 저감 및 완충 구역 규정 준수를 통한 정밀 살포 의무화

독일의 작물 보호 제도는 시장에 순전히 자발적인 갱신 주기가 아닌, 규제 준수에 기반한 수요 기반을 마련해 주고 있습니다. 니더작센주 식물보호국(Niedersachsen Pflanzenschutzdienst)은 드리프트 저감 노즐 등급, 붐 높이 설정 및 경계 노즐 사용에 대해 명확한 요건을 규정하고 있으며, 이러한 규정은 현장에서 어떤 기계나 사후 장착 키트가 계속해서 규정을 준수할 수 있는지에 직접적인 영향을 미치고 있습니다. 농가가 드리프트 저감 효과가 인정되지 않은 노즐을 사용할 경우, 실질적으로 완충지대 요건이 확대되어 밭 가장자리에서 살포할 수 있는 면적이 좁아지게 됩니다. 이로 인해 규정 준수는 단순한 기술적 문제가 아니라 명백한 경제적 문제로 변모합니다. 그 결과, 시장의 많은 지역에서 인증된 정밀 살포 장비에 대한 투자가 일반 장비의 교체 주기보다 빠른 속도로 진행되고 있습니다. 또한, 3년마다 실시되는 장비 검사 요건 역시 반복적으로 판단을 내려야 하는 요인이 되고 있습니다. 왜냐하면, 검사 기준을 통과하지 못한 구형 기존 기계는 계속 사용하기 위해 고액의 수리비나 전면적인 교체가 필요한 경우가 많기 때문입니다. 따라서 독일의 농업용 분무기 시장 수요는 다른 몇몇 농업 기계 부문에 비해 안정적인 임베디드니다. 정책 방향도 더욱 엄격해지고 있으며, 독일은 2030년까지 농약 사용량을 2004년부터 2023년까지의 평균치 대비 50% 감축하는 것을 목표로 하고 있어, 이에 따라 정밀 살포 시스템은 규제 준수 및 비용 관리 양면에서 계속해서 중요한 역할을 수행하고 있습니다.

인력 부족과 위탁 살포 비용의 상승

인력 부족으로 인해 시장 전반에서 처리 능력, 작업 속도, 자동화의 가치가 높아지고 있습니다. 북유럽 및 서유럽의 농장과 도급업체들은 살포 가능 기간이 단축되는 가운데 작업을 진행하고 있으며, 살포 성수기에는 작업자 1인당 작업 시간의 가치가 더욱 높아지고 있습니다. 이에 따라 구매자들은 더 큰 붐과 탱크, 경로 효율성 향상, 그리고 한 명의 운전자가 하루에 더 많은 헥타르를 작업할 수 있게 해주는 자동화 기능을 갖춘 기종을 선호하는 추세입니다. 이러한 변화는 특히 도급업자 부문에서 두드러지는데, 이 부문에서는 단일 농장의 소유 경제성보다 여러 농장에 걸친 기계 가동률이 더 중요하게 여겨지고 있습니다. HORSCH Maschinen GmbH는 2025년 6월부터 더 폭넓은 계약업체층을 대상으로 한 5,000리터 용량의 엔트리 모델을 "Leeb PT" 자주식 시리즈에 추가했습니다. 이는 같은 카테고리의 프리미엄 모델보다 다소 저렴한 가격대로, 대용량 기기에 대한 제조업체 측 수요가 증가하고 있음을 뒷받침하고 있습니다. 인력 부족은 특수 작물 분야의 자율형 기술 개발에도 박차를 가하고 있습니다. 이 분야에서는 내비게이션의 정확도와 재현성을 통해 훈련을 받은 계절 근로자의 부족을 보완할 수 있습니다. 쿠보타의 2세대 "KFAST" 자율 주행형 과수원용 분무기는 스페인과 포르투갈에서 현장 시험을 거친 후, 2026년 중반에 제한적인 상업화 단계로 전환될 예정이며, 2027년에는 유럽 전역에서 판매를 시작하는 것을 목표로 하고 있습니다.

정밀·자율형 분무기의 높은 초기 비용

여전히 높은 구매 가격이 독일 농업용 분무기 시장이 정밀 농업을 중시하는 기종군으로 전환되는 속도를 제한하고 있습니다. 독일 농업기술·구조협회가 농업 기계의 경제성에 대해 실시한 조사에 따르면, 직접 분사식 자가주행 분무기나 정밀 농업용 후부착 시스템에는 막대한 초기 투자가 필요하기 때문에 비용에 민감한 농업 경영자들의 도입을 지연시키고 있습니다. 독일에서는 대규모 농장이나 농업 서비스 제공업체가 이러한 비용을 더 많은 헥타르에 분산시킬 수 있지만, 소규모 농장의 경우 도입 비용을 충당하기 위해 보조금, 대출 프로그램 또는 장비 공유 계약에 의존하는 경우가 많은 것이 현실입니다. 무인항공기(UAV) 플랫폼이나 정밀 살포용 후장착 시스템 등의 기술에 대해서는 경쟁으로 인해 보급형 가격대가 하락할 것으로 예상되지만, 막대한 초기 투자가 필요하다는 점은 첨단 농업용 분무기의 보급에 여전히 큰 걸림돌이 되고 있습니다.

부문별 분석

2025년에는 트랙터 탑재형 분무기가 제품 매출의 40.7%를 차지하며, 독일 농업용 분무기 시장에서 가장 큰 점유율을 기록했습니다. 이에 이어 견인식 분무기와 자주식 유닛이 뒤를 잇고 있는 반면, 무인항공기(UAV) 분무기나 휴대용 모델은 이용 사례가 제한적이고 도입 기반도 작기 때문에 여전히 소규모 범주에 머물러 있습니다. 이러한 기종들이 시장을 독점하고 있는 배경으로는 기존 트랙터와의 폭넓은 호환성, 낮은 소유 비용, 그리고 독일 전역에서 널리 구할 수 있다는 점 등을 들 수 있습니다.

무인항공기(UAV) 방식 분무기는 2031년까지 연평균 성장률(CAGR) 9.4%로 확대될 것으로 예측되며, 이 부문에서 가장 빠른 성장세를 보일 것으로 예상되어 제품 카테고리 중 시장 규모 확대가 가장 두드러질 것으로 전망됩니다. 도급업체들이 일일 작업 범위의 확대를 요구하는 가운데, 자행식 및 견인식 플랫폼도 발전하고 있지만, 트랙터 탑재형 시스템은 기존의 농기계군 및 농지 규모의 경제성에 부합하기 때문에 여전히 중심적인 위치를 차지하고 있습니다. 휴대용 분무기는 광활한 농경지에서의 작업보다는 소규모 원예나 온실에서의 작업에 계속해서 활용되고 있습니다. 이러한 성장은 노동력 부족, 정밀 살포의 장점, 그리고 디지털 농업 기술의 보급 확대에 힘입어 더욱 가속화되고 있습니다.

2025년 매출에서 차지하는 비중은 연료 구동식 시스템이 41.2%를 차지하여, 독일 농업용 분무기 시장에서 가장 큰 동력원 부문으로 자리매김하고 있습니다. 수동식 시스템은 소규모 용도에서 여전히 중요한 역할을 하고 있으며, 태양광 발전식 유닛은 틈새 시장 수준에 머물러 있습니다. 또한, 배터리 구동식 기계는 기술적인 성장세가 강해지고 있지만, 매출액 측면에서는 여전히 소규모 수준에 머물러 있습니다. 확립된 인프라, 실증된 포장에서의 성능, 그리고 집중적인 살포 작업에 대응할 수 있는 능력 덕분에 독일 전역에서 도입이 지속적으로 확대되고 있습니다.

배터리 구동식 분무기는 2026년부터 2031년까지의 예측 기간 동안 연평균 성장률(CAGR) 7.1%를 나타낼 것으로 예측되며, 이는 시장 내 동력원 부문에서 가장 높은 성장률입니다. 이러한 성장은 과수원용 로봇, 온실 시스템, 그리고 전기식 특수 작물용 플랫폼에 의해 뒷받침되고 있는데, 이는 이러한 용도의 경우 광활한 농지에서 살포하는 것에 비해 탱크 용량이나 가동 시간에 대한 요구 사항이 상대적으로 낮기 때문입니다. 연료 구동형 플랫폼은 예측 기간 내내 핵심적인 위치를 차지할 것으로 보입니다. 이는 대형 붐, 고출력, 장시간 가동과 같은 요건에서 여전히 디젤 엔진을 탑재한 기계가 유리하기 때문입니다. 수동식 및 태양광 발전식 시스템은 주류 기체 수요를 주도하기보다는 특정 작물에 한정된 역할을 계속 수행할 것으로 보입니다. 또한, 지속가능성에 대한 관심 증가와 배터리 효율 향상 역시 전문적인 농업 분야에서의 보급 확대를 뒷받침하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.03According to Mordor Intelligence, the germany agricultural sprayers market size is estimated to increase from USD 446.51 million in 2025 and USD 475.28 million in 2026 to USD 650.21 million by 2031, growing at a CAGR of 6.47% during 2026 to 2031.

This report is Segmented by Product Type (Handheld Sprayers, Tractor-Mounted Sprayers, Trailed Sprayers, and More), by Source of Power (Manual, Solar-Powered, Fuel-Operated, and More), by Application (Field Crops, Orchards and Vineyards, and More), and by Technology Level (Conventional, Precision and GPS-Guided, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Agricultural Sprayers Market Trends and Insights

Precision Spraying Mandates from Drift Reduction and Buffer-Zone Compliance

Germany's crop protection regime is giving the market a compliance-based demand base rather than a purely discretionary replacement cycle. The Niedersachsen Pflanzenschutzdienst has laid out clear requirements on drift-reduction nozzle classes, boom-height settings, and border-nozzle use, and those rules directly influence which machines and retrofit packages can remain compliant in the field. When a grower uses a nozzle that is not recognized for drift reduction, the practical effect is a wider buffer requirement and a smaller sprayable area at field edges, turning compliance into a clear financial issue rather than a simple technical one. That is why investment in certified precision hardware is moving faster than the typical equipment replacement cycle in many parts of the market. The three-year equipment inspection requirement also creates a recurring decision point, because older conventional machines that fail inspection often require costly repairs or a full replacement to remain in service. This makes demand in the Germany agricultural sprayers market steadier than in several other farm machinery categories. The policy direction is also becoming tighter, with Germany targeting a 50% reduction in plant protection product use by 2030 from the 2004 to 2023 average, which keeps precision application systems relevant to both compliance and cost control.

Labor Scarcity and Rising Custom-Application Costs

Labor shortages are increasing the value of capacity, speed, and automation across the market. Farms and contractors in Northern and Western Europe are working within shorter spray windows, and each operator hour now carries more value during peak treatment periods. This is pushing buyers toward larger booms, bigger tanks, better route efficiency, and more automated functions that let one operator cover more hectares in a day. The change is especially visible in the contractor segment, where machine utilization across multiple farms matters more than single-farm ownership economics. HORSCH Maschinen GmbH expanded its Leeb PT self-propelled line in June 2025 with a 5,000-liter entry-level model aimed at a broader contractor base, underscoring manufacturers' stronger demand for high-capacity machines at a slightly lower entry point than the premium end of the category. Labor scarcity is also supporting autonomous development in specialty crops, where navigation accuracy and repeatability can offset the shortage of trained seasonal operators. Kubota's second-generation KFAST autonomous orchard sprayer moved from field trials in Spain and Portugal toward a limited commercial launch in mid-2026, with full European availability targeted for 2027.

High Upfront Cost of Precision and Autonomous Sprayers

High purchase prices still limit how quickly the Germany agricultural sprayers market can move toward precision-heavy fleets. Studies conducted by the German Association for Technology and Structures in Agriculture on farm machinery economics indicate that direct-injection self-propelled sprayers and precision retrofit systems require significant upfront capital expenditure, slowing adoption among cost-sensitive farming operations. In Germany, large arable farms and agricultural service providers can spread these costs across more hectares, whereas smaller operations often rely on subsidies, financing programs, or equipment-sharing arrangements to justify adoption. Although increased competition is estimated to reduce entry-level pricing for technologies such as unmanned aerial vehicle platforms and precision retrofit systems, the substantial upfront capital requirements remain a significant barrier to the widespread adoption of advanced agricultural sprayers.

Other drivers and restraints analyzed in the detailed report include:

- Subsidies for Targeted Plant Protection and Drift Avoidance

- Precision Retrofits on Large Arable Farms

- Operator Know-How Gap for Advanced Precision Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tractor-mounted sprayers led product revenue with 40.7% in 2025, giving them the largest share of the Germany agricultural sprayers market. Trailed sprayers followed, then self-propelled units, while unmanned aerial vehicle sprayers and handheld models remained smaller categories shaped by narrower use cases and smaller starting bases. Their dominance is further supported by broad compatibility with existing tractors, lower ownership costs, and widespread availability across Germany.

Unmanned aerial vehicle sprayers are projected to expand at a 9.4% CAGR through 2031, giving them the fastest growth path in this segmentation and the strongest expansion in market size among product categories. Self-propelled and trailed platforms are also advancing as contractors seek higher daily coverage, while tractor-mounted systems remain central because they fit established farm fleets and field-scale economics. Handheld sprayers continue to serve smaller horticultural and greenhouse tasks rather than broad-acre field work. Growth is additionally supported by labor shortages, precision application benefits, and increasing acceptance of digital farming technologies.

Fuel-operated systems accounted for 41.2% of 2025 revenue, making them the largest power-source segment for the Germany agricultural sprayers market. Manual systems remained relevant for small-scale use, while solar-powered units remained niche, and battery-operated machines were still smaller in terms of revenue despite stronger technology momentum. Their established infrastructure, proven field performance, and ability to support intensive spraying operations continue to strengthen adoption across Germany.

Battery-operated sprayers are projected to grow at a 7.1% CAGR during the forecast period 2026-2031, the fastest rate across power-source categories in the market. This rise is supported by orchard robots, greenhouse systems, and electric specialty-crop platforms, where tank size and endurance requirements are lower than in broad-acre spraying. Fuel-operated platforms will remain central throughout the forecast period, as large booms, higher horsepower, and long working hours still favor diesel-based machines. Manual and solar-powered systems should continue to play limited, crop-specific roles rather than drive mainstream fleet demand. Increasing sustainability targets and advances in battery efficiency are also encouraging wider adoption across specialized agricultural applications.

Complete Report Scope:

- By Product Type

- Handheld Sprayers

- Tractor-Mounted Sprayers

- Trailed Sprayers

- Self-Propelled Sprayers

- Unmanned Aerial Vehicle Sprayers

- By Source of Power

- Manual

- Solar-Powered

- Fuel-Operated

- Battery-Operated

- By Application

- Field Crops

- Orchards and Vineyards

- Greenhouse Crops

- Turf and Gardening

- By Technology Level

- Conventional

- Precision and GPS-Guided

- AI-Enabled and Autonomous

List of Companies Covered in this Report:

- Amazonen-Werke H. Dreyer GmbH & Co. KG

- CNH Industrial N.V.

- Deere and Company

- AGCO Corporation

- Kuhn Group

- HORSCH Maschinen GmbH

- Lemken GmbH & Co. KG

- Kverneland AS

- Chafer Machinery Ltd

- Knight Farm Machinery Ltd

- Grim S.r.l.

- Bargam S.p.A.

- Pulverizadores Fede S.L.

- DJI Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Precision spraying mandates from drift reduction and buffer-zone compliance

- 4.2.2 Labor scarcity and rising custom-application costs

- 4.2.3 Subsidies for targeted plant protection and drift avoidance

- 4.2.4 Precision retrofits on large arable farms

- 4.2.5 Site-specific pesticide savings from direct injection and application assistants

- 4.2.6 Connected sprayers supported by digital documentation workflows

- 4.3 Market Restraints

- 4.3.1 High upfront cost of precision and autonomous sprayers

- 4.3.2 Operator know-how gap for advanced precision systems

- 4.3.3 Drone-use approvals remain narrow and multi-step

- 4.3.4 Documentation, inspection, and nozzle-compliance burden

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Handheld Sprayers

- 5.1.2 Tractor-Mounted Sprayers

- 5.1.3 Trailed Sprayers

- 5.1.4 Self-Propelled Sprayers

- 5.1.5 Unmanned Aerial Vehicle Sprayers

- 5.2 By Source of Power

- 5.2.1 Manual

- 5.2.2 Solar-Powered

- 5.2.3 Fuel-Operated

- 5.2.4 Battery-Operated

- 5.3 By Application

- 5.3.1 Field Crops

- 5.3.2 Orchards and Vineyards

- 5.3.3 Greenhouse Crops

- 5.3.4 Turf and Gardening

- 5.4 By Technology Level

- 5.4.1 Conventional

- 5.4.2 Precision and GPS-Guided

- 5.4.3 AI-Enabled and Autonomous

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-Level Overview, Market-Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Amazonen-Werke H. Dreyer GmbH & Co. KG

- 6.4.2 CNH Industrial N.V.

- 6.4.3 Deere and Company

- 6.4.4 AGCO Corporation

- 6.4.5 Kuhn Group

- 6.4.6 HORSCH Maschinen GmbH

- 6.4.7 Lemken GmbH & Co. KG

- 6.4.8 Kverneland AS

- 6.4.9 Chafer Machinery Ltd

- 6.4.10 Knight Farm Machinery Ltd

- 6.4.11 Grim S.r.l.

- 6.4.12 Bargam S.p.A.

- 6.4.13 Pulverizadores Fede S.L.

- 6.4.14 DJI Technology Co., Ltd.