|

시장보고서

상품코드

2072829

영국의 헬스케어 컨설팅 서비스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United Kingdom Healthcare Consulting Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

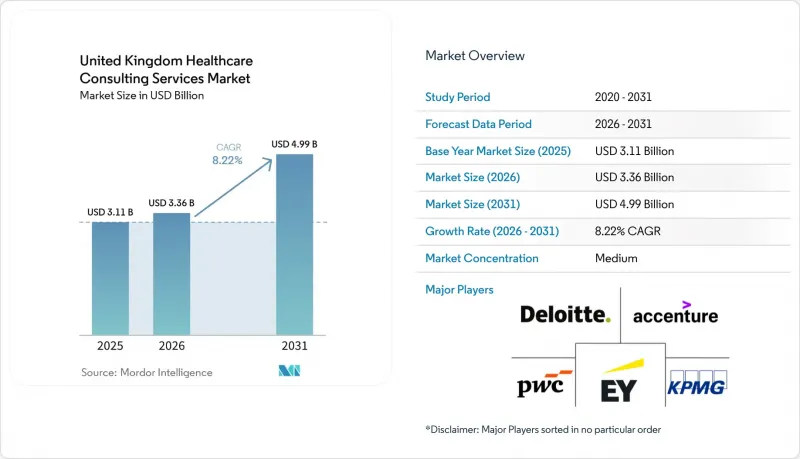

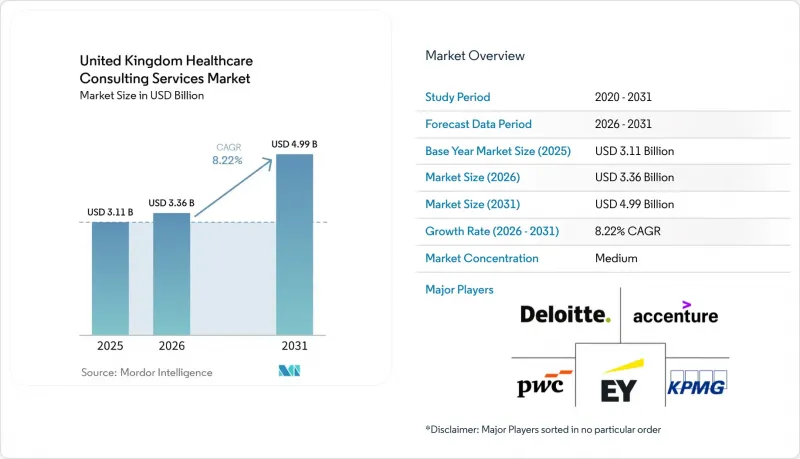

Mordor Intelligence에 의하면, 영국의 헬스케어 컨설팅 서비스 시장 규모는 2025년 31억 1,000만 달러로 평가되었고, 2026년에는 33억 6,000만 달러로 추정되고, 2026-2031년 CAGR 8.22%로 성장을 지속할 전망이며, 2031년에는 49억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 서비스 유형별(IT 컨설팅, 전략 컨설팅, 업무 컨설팅 등), 최종 사용자별(의료 서비스 제공업체, 의료 보험사, 생명과학 기업, 정부 기관 등), 제공 모델별(온사이트 컨설팅, 원격 및 가상 컨설팅, 하이브리드 모델)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

영국의 헬스케어 컨설팅 서비스 시장 동향 및 인사이트

가치 기반 돌봄 모델로의 전환이 가속화되고 있습니다.

영국의 헬스케어 컨설팅 서비스 시장은 NHS(국민보건서비스)가 인구 기반 의료 서비스 제공 및 가치 연계형 계약으로 전환함에 따라 지속적인 성장 동력을 얻고 있습니다. NHS 컨페더레이션은 2026년 3월, 'Population Health Delivery Models(인구 건강 서비스 제공 모델)'의 청사진이 IHO, SNP, MNP 각 계약을 장기적인 정책 논의의 틀에서 운영 프레임워크로 전환시켰음을 지적했습니다. 이러한 변화가 중요한 이유는 현재 시스템이 활동량이 아닌 인구 관련 성과를 중심으로 지급 규칙, 치료 경로, 책임 구조를 재설계하기 위해 외부 지원이 필요하기 때문입니다. 또한, NHS 잉글랜드는 '절약하지 않으면 지불할 필요도 없습니다(no saving, no payment)' 모델을 바탕으로, 모든 연령대를 대상으로 한 지속적 의료비 지출 75억 파운드(95억 달러)를 관리하기 위해 외부 전문 지식을 요청했습니다. 이로 인해 컨설팅 업무는 직접적인 실적 평가 및 위험 분담의 영역으로 진출하게 될 것입니다. 2025/26 회계연도 운영 계획에서 각 시스템 전반에 걸쳐 44억 파운드(56억 달러)의 계획 격차가 확인됨에 따라, 재설계 작업 중에 내부 자금을 활용한 시행착오를 거칠 여지가 제한적이며, 이에 따른 압박은 더욱 커지고 있습니다. 템즈 밸리 ICB가 옥스퍼드 대학교 연구진들과 공동으로 진행하고 있는 프로그램은 컨설팅 팀이 이미 거버넌스 설계 및 가치 측정에 통합되어 있음을 보여주고 있으며, 이로 인해 영국 헬스케어 컨설팅 서비스 시장에 대한 수요 기반은 단기적인 정책 지원의 범위를 훨씬 뛰어넘어 확대되고 있습니다.

'디지털 우선'형 환자 참여 플랫폼에 대한 수요 급증

영국의 헬스케어 컨설팅 서비스 시장은 '디지털 우선' 환자 접근성, 상호운용성, 그리고 도입 후 최적화를 향한 광범위한 움직임으로부터도 혜택을 받고 있습니다. NHS 트러스트의 IT 지출은 2024/25 회계연도에 41억 파운드(52억 달러)에 달했으며, 이러한 지출 확대에 따라 통합, 워크플로우 재설계 및 환자 서비스 업그레이드와 관련된 자문 지원이 필요한 도입 기반이 더욱 확대되었습니다. 지출 추세가 변화하고 있는 이유는 EPR 도입이 포화 상태에 가까워짐에 따라 컨설팅 업무가 소프트웨어 도입에서 최적화, 상호 운용성 및 디지털 프론트도어 설계로 전환되고 있기 때문입니다. 2026년 1월에 발표된 왕립내과의학회(Royal College of Physicians)의 조사에 따르면, 조사 대상인 548명의 회원 중 68%가 'NHS는 AI의 광범위한 도입에 적합한 디지털 인프라를 갖추고 있다'라는 견해에 동의하지 않았습니다. 이는 변화가 이미 완료된 것이 아니라, 여전히 준비 태세에 미흡한 점이 있음을 시사합니다. 정부가 2025/26 회계연도에 '최전선의 디지털화' 및 '진료 기록 연계'에 6억 파운드(8억 200만 달러)를 투자함으로써, 이러한 수요는 단순한 이상론에 그치지 않고 자금 면에서의 뒷받침을 얻은 길이 열렸습니다. 이러한 자금 환경은 기술 자문과 도입 보장, NHS 기준에 대한 지식, 그리고 환자 참여 설계 등을 결합할 수 있는 영국 헬스케어 컨설팅 서비스 시장의 기업들에게 유리하게 작용할 것입니다.

인력 부족과 일당 급등

영국의 헬스케어 컨설팅 서비스 시장은 심각한 인력 부족에 직면해 있습니다. 이는 프로젝트에서 임상 경로, 디지털 시스템, 데이터 거버넌스, NHS 조달 프로세스를 동시에 이해할 수 있는 인력에 대한 수요가 증가하고 있기 때문입니다. 컨설턴트의 일당 상승으로 인해, 구매 측에서는 일반적인 조건으로 자문 수수료를 승인받기가 어려워지고 있으며, 특히 프로젝트가 일반적인 비즈니스 팀이 아닌 고위급 헬스케어 전문가를 필요로 하는 경우에는 이러한 경향이 두드러집니다. NHS의 인력 부족은 컨설팅 기업이 임상 분야 전문가를 채용하는 인재 풀에도 영향을 미치고 있으며, 개혁 업무를 수행할 예비 인력의 두께가 얇아지고 있어 이러한 압박은 더욱 심해지고 있습니다. 중소기업은 다양한 분야에 걸쳐 사업을 영위하는 대형 경쟁사들만큼 임금 인상, 인재 유지 보너스, IR35와 관련된 가격 압박에 쉽게 대응할 수 없기 때문에 특히 큰 영향을 받기 쉬운 상황에 놓여 있습니다. 이 때문에 영국의 헬스케어 컨설팅 서비스 시장은 수요 증가를 수용할 여지가 있는 반면, 복잡한 프로젝트의 경우 실행 비용 상승과 인력 확보 기간의 장기화를 초래하고 있습니다.

부문별 분석

2025년, IT 컨설팅은 영국 헬스케어 컨설팅 서비스 시장 점유율의 31.31%를 차지했으며, NHS 기관들이 핵심 시스템, 데이터 흐름 및 인프라의 현대화를 지속함에 따라 가장 큰 서비스 부문이 되었습니다. 이러한 선도적인 위상은 의료 제공 기관 전반에 걸쳐 디지털 자산, EPR(전자건강기록) 프로그램, 상호운용성 및 시스템 통합 업무에 대한 지속적인 투자를 반영한 것입니다. 디지털 전환 컨설팅 시장은 초기 도입에서 최적화, 워크플로우 재설계, 커넥티드 케어 도입으로 이어지는 추세를 바탕으로 2031년까지 연평균 성장률(CAGR) 11.38%를 기록하며 성장할 것으로 전망됩니다. 2025/26 회계연도에 6억 파운드(8억 200만 달러) 규모의 '최전선 디지털화 및 진료 기록 연계' 자금 계획에 따라, 이러한 노력들은 개별 트러스트 수준의 예산에 의존하는 것이 아니라, 영국 의료 컨설팅 서비스 업계 내에서 공식적인 지출 경로가 확보되게 됩니다.

전략 컨설팅의 중요성이 다시금 부각되고 있습니다. 이는 IHO(통합보건기구)의 계약 설계, 인구 건강 계획, 그리고 NHS 잉글랜드에서 DHSC(보건·사회돌봄부)로의 전환이 모두 소프트웨어 도입만으로는 해결할 수 없는 조직 전체에 걸친 설계 작업을 필요로 하기 때문입니다. 운영 컨설팅은 의료 제공업체 및 DHSC 산하 기관들이 업무 흐름 재설계, 비효율 제거, 서비스 처리 능력 향상을 요구받고 있는 상황에서 지속적인 생산성 향상에 대한 압박을 받고 있는 덕분에 혜택을 보고 있습니다. 재무 컨설팅 분야에서도 요금 개정, 가치 기반 조달, 그리고 계획의 불확실성으로 인해 더욱 강력한 모델링과 상업적 지원이 요구되고 있어 꾸준한 수요가 나타나고 있습니다. 인사·인재 컨설팅은 ICS 및 ICB의 구조가 지속적으로 노동력 모델과 리더십 설계를 재구축하고 있기 때문에 그 중요성이 커지고 있습니다. 영국의 헬스케어 컨설팅 서비스 업계 전반에서 DTAC, DCB 및 조달 프레임워크의 요건으로 인해 진입 장벽이 높아지고 있으며, 단일 규정 준수 모델 하에서 여러 서비스 분야를 아우를 수 있는 기업이 우대받고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the united kingdom healthcare consulting services market size is expected to grow from USD 3.11 billion in 2025 to USD 3.36 billion in 2026 and is forecast to reach USD 4.99 billion by 2031 at 8.22% CAGR over 2026-2031.

This report is Segmented by Service Type (IT Consulting, Strategy Consulting, Operations Consulting, and More), End User (Healthcare Providers, Healthcare Payers, Life Sciences Companies, Government Agencies, and More), Delivery Model (On-Site Consulting, Remote/Virtual Consulting, Hybrid Model). The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom Healthcare Consulting Services Market Trends and Insights

Accelerated Shift to Value-Based Care Models

The UK healthcare consulting services market is gaining sustained support from the NHS move toward population-based delivery and value-linked contracting. NHS Confederation noted in March 2026 that the Population Health Delivery Models blueprint moved IHO, SNP, and MNP contracts into an operating framework rather than a long-range policy discussion. This change matters because systems now need outside support to redesign payment rules, care pathways, and accountability structures around population outcomes instead of activity volumes. NHS England also sought external expertise to help manage GBP 7.5 billion (USD 9.5 billion) in all-age continuing care spend under a no saving, no payment model, which pushes consulting work into direct performance and risk-sharing territory. The pressure is stronger because the 2025/26 operating plan identified a GBP 4.4 billion (USD 5.6 billion) planning gap across systems, leaving limited room for internally funded trial and error during redesign work. Thames Valley ICB's program with University of Oxford researchers shows that consulting teams are already being embedded into governance design and value measurement, which extends the demand base for the UK healthcare consulting services market well beyond short-term policy support.

Surging Demand for Digital-First Patient Engagement Platforms

The UK healthcare consulting services market is also benefiting from a wider move toward digital-first patient access, interoperability, and post-implementation optimization. NHS trust IT spend reached GBP 4.1 billion (USD 5.2 billion) in 2024/25, and that expansion created a larger installed base that now needs advisory support for integration, workflow redesign, and patient-facing service upgrades. The spending pattern is shifting because once EPR adoption nears saturation, consulting work moves from software deployment toward optimization, interoperability, and digital front-door design. A Royal College of Physicians review published in January 2026 found that 68% of 548 surveyed members disagreed that the NHS had the right digital infrastructure for widespread AI adoption, which points to an ongoing readiness gap rather than a completed transformation story. The government's GBP 600 million (USD 802 million) investment in Frontline Digitisation and Connecting Care Records for 2025/26 gives this demand a funded pathway rather than a purely aspirational one. That funding environment favors firms in the UK healthcare consulting services market that can combine technology advisory with delivery assurance, NHS standards knowledge, and patient engagement design.

Talent Shortage and Soaring Bill Rates

The UK healthcare consulting services market faces a clear staffing constraint because projects increasingly require people who understand clinical pathways, digital systems, data governance, and NHS procurement at the same time. Rising consultant day rates are making it harder for buyers to approve advisory spend on routine terms, especially when projects need senior healthcare specialists rather than general business teams. The pressure is stronger because NHS staffing shortages also affect the pool from which consulting firms recruit clinical subject matter experts, which reduces bench depth for transformation work. Smaller firms are especially exposed because they cannot always absorb wage inflation, retention bonuses, and IR35-related pricing pressure as easily as large multidisciplinary competitors. This keeps the UK healthcare consulting services market open to demand growth, but it also raises delivery costs and lengthens staffing cycles on complex engagements.

Other drivers and restraints analyzed in the detailed report include:

- Heightened Cyber-Threat Environment Driving Security Consulting

- Regulatory Push for Healthcare Price-Transparency Compliance

- Prolonged Provider Margin Squeeze Curbing Discretionary Spend

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

IT Consulting held 31.31% of the UK healthcare consulting services market share in 2025, making it the largest service category as NHS organizations continued to modernize core systems, data flows, and infrastructure. This leadership position reflected continued trust spending on digital estate, EPR programs, interoperability, and system integration work across provider settings. Digital Transformation Consulting is projected to expand at an 11.38% CAGR through 2031, supported by the move from initial deployment into optimization, workflow redesign, and connected care implementation. The GBP 600 million (USD 802 million) Frontline Digitisation and Connecting Care Records funding path for 2025/26 gives these mandates a formal spending route inside the UK healthcare consulting services industry rather than leaving them dependent on isolated trust-level budgets.

Strategy Consulting is regaining weight because IHO contract design, population health planning, and the NHS England to DHSC transition all require organization-wide design work that cannot be solved by software implementation alone. Operations Consulting is benefiting from recurring productivity pressure as provider and DHSC bodies are pushed to redesign workflows, reduce waste, and improve service throughput. Financial Consulting is also seeing steady demand because tariff reform, value-based procurement, and planning uncertainty require stronger modeling and commercial support. HR and Talent Consulting is gaining relevance as ICS and ICB structures continue to reshape workforce models and leadership design. Across the UK healthcare consulting services industry, DTAC, DCB, and procurement framework requirements are raising entry barriers and rewarding firms that can cover multiple service lines under a single compliant delivery model.

Complete Report Scope:

- By Service Type

- IT Consulting

- Strategy Consulting

- Operations Consulting

- Digital Transformation Consulting

- Financial Consulting

- HR and Talent Consulting

- By End User

- Healthcare Providers

- Healthcare Payers

- Life Sciences Companies

- Government Agencies

- Healthcare IT Vendors

- MedTech Start-Ups

- By Delivery Model

- On-Site Consulting

- Remote / Virtual Consulting

- Hybrid Model

List of Companies Covered in this Report:

- Accenture

- Atos

- Bain and Company

- Boston Consulting Group

- Cognizant

- Deloitte

- EY

- GE Healthcare Partners

- IQVIA

- KPMG

- L.E.K. Consulting

- McKinsey & Company

- NTT DATA Services

- Oliver Wyman

- Optum Advisory

- PA Consulting Group

- PwC

- Slalom

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Shift to Value-Based Care Models

- 4.2.2 Surging Demand for Digital-First Patient Engagement Platforms

- 4.2.3 Heightened Cyber-Threat Environment Driving Security Consulting

- 4.2.4 Regulatory Push for Healthcare Price-Transparency Compliance

- 4.2.5 Generative AI Advisory for Clinical Decision Support

- 4.2.6 Climate-Resilience Planning for Hospital Infrastructure

- 4.3 Market Restraints

- 4.3.1 Talent Shortage and Soaring Bill Rates

- 4.3.2 Prolonged Provider Margin Squeeze Curbing Discretionary Spend

- 4.3.3 Data-Ownership Disputes in Multi-Party Analytics Ecosystems

- 4.3.4 Rising Carbon-Footprint Scrutiny of Consultants Travel

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service Type

- 5.1.1 IT Consulting

- 5.1.2 Strategy Consulting

- 5.1.3 Operations Consulting

- 5.1.4 Digital Transformation Consulting

- 5.1.5 Financial Consulting

- 5.1.6 HR and Talent Consulting

- 5.2 By End User

- 5.2.1 Healthcare Providers

- 5.2.2 Healthcare Payers

- 5.2.3 Life Sciences Companies

- 5.2.4 Government Agencies

- 5.2.5 Healthcare IT Vendors

- 5.2.6 MedTech Start-Ups

- 5.3 By Delivery Model

- 5.3.1 On-Site Consulting

- 5.3.2 Remote / Virtual Consulting

- 5.3.3 Hybrid Model

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Accenture

- 6.3.2 Atos

- 6.3.3 Bain and Company

- 6.3.4 Boston Consulting Group

- 6.3.5 Cognizant

- 6.3.6 Deloitte

- 6.3.7 EY

- 6.3.8 GE Healthcare Partners

- 6.3.9 IQVIA

- 6.3.10 KPMG

- 6.3.11 L.E.K. Consulting

- 6.3.12 McKinsey & Company

- 6.3.13 NTT DATA Services

- 6.3.14 Oliver Wyman

- 6.3.15 Optum Advisory

- 6.3.16 PA Consulting Group

- 6.3.17 PwC

- 6.3.18 Slalom

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment