|

시장보고서

상품코드

2072872

LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)LLM and Generative AI Energy Optimization Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

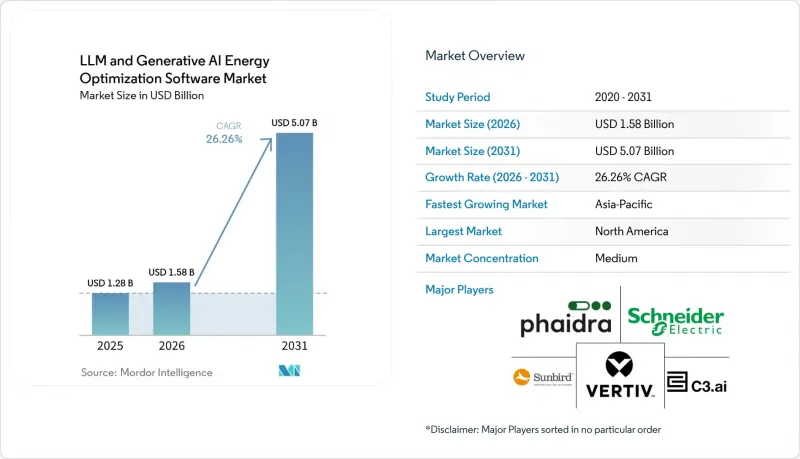

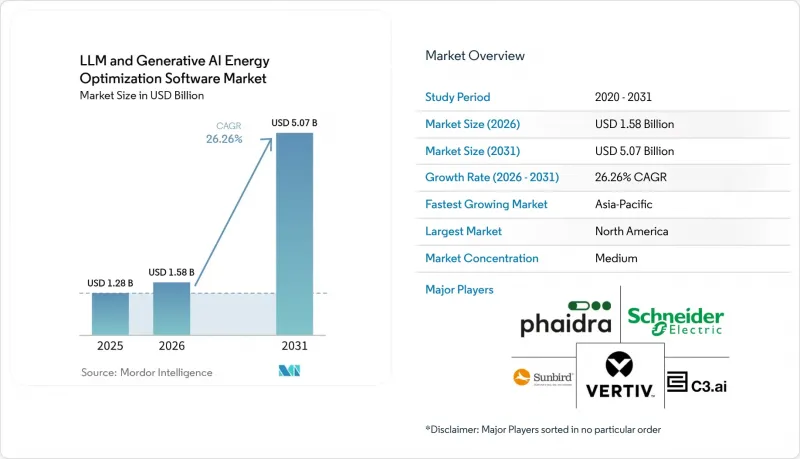

Mordor Intelligence에 의하면, LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장 규모는 2025년 12억 8,000만 달러에서 2026년에는 15억 8,000만 달러로 확대되어 2031년까지 50억 7,000만 달러에 이를 것으로 예상되고 있어 2026-2031년까지 CAGR 26.26%로 성장할 전망입니다.

본 보고서는 솔루션 유형(AI 에너지 분석·관측 가능성 등), 도입 형태(클라우드 기반, 하이브리드형, On-Premise형), 최종 사용자(하이퍼스케일 클라우드·AI 인프라 제공업체 등), 최적화 목적(에너지·탄소 최적화, 비용 최적화 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장 동향과 인사이트

데이터센터 내 AI 집약형 워크로드의 급속한 확대

LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장은 현대 데이터센터에서 훈련 및 추론 워크로드가 급속히 확대됨에 따라 성장하고 있습니다. 정격 열 설계 전력(TDP)이 10.2 kW인 NVIDIA H100 GPU 노드 1대는 실측 테스트에서 트랜스포머 모델 훈련 중에 해당 정격치의 불과 76%만 소비했습니다. 이 사실은 정격값만을 바탕으로 계획을 수립할 경우, 운영 담당자가 실제 전력 동향에 대해 잘못된 인식을 가질 가능성이 있음을 여실히 보여주고 있습니다. 클러스터 규모에서는 이러한 불일치가 계획상의 오류나 유휴 용량을 초래합니다. 왜냐하면 시설에는 실시간 워크로드 변동에 대응하기 위한 충분한 열적·전기적 여유 공간이 여전히 필요하기 때문입니다. 기존의 모니터링 도구는 보다 안정적인 엔터프라이즈 부하를 위해 구축되어 있어 급격한 변동을 동일한 정확도로 관리할 수 없기 때문에 LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장은 이러한 변화의 혜택을 누리고 있습니다. 국제에너지기구(IEA)는 AI 전용 데이터센터의 전력 사용량이 2030년까지 2025년 대비 3배로 증가할 것으로 예측하고 있으며, 이는 향후 수년 동안 계산 부하와 이용 가능한 전력·냉각 자원을 적절히 매칭시키는 소프트웨어가 필요할 것임을 시사합니다. 그 결과, LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장은 인프라가 이를 따라잡을 때까지 설비를 유휴 상태로 두는 대신, 운영자가 새로운 GPU 용량을 지속적으로 가동할 수 있는지 여부에 점점 더 좌우되고 있습니다.

AI 인프라 사업자의 전력 비용 리스크 증가

LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장은 전력 비용에 대한 노출이 인프라 전략의 핵심으로 부상하고 있다는 사실로부터도 혜택을 보고 있습니다. 국제에너지기구(IEA)의 보고서에 따르면, 데이터센터의 전력 수요는 2025년 한 해 동안만 17% 급증했으며, AI 전용 시설에서는 더욱 빠른 증가세를 보임에 따라 사업자가 실시간으로 관리해야 하는 비용 부담이 증가했습니다. 해당 보고서에 따르면, 주요 기술 기업 5곳의 2025년 설비 투자액은 4,000억 달러를 넘어설 전망이며, 2026년에는 이보다 75% 더 증가할 것으로 예측됩니다. 이는 LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장이 단순한 공과금 절감에 그치지 않고, 수익 보호 측면에서도 그 중요성이 커지고 있음을 의미합니다. Hammerhead AI는 오케스트레이션을 통해 회수된 잉여 전력 1메가와트당, 인프라가 포화 상태인 시장에서는 2,000만-5,000만 달러의 가치가 있다고 밝히며, 이로 인해 최적화 투자에 내재된 가치 논리가 변화할 것이라고 설명했습니다. 이러한 프레임워크를 통해 LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장은 이사회 차원의 투자 결정 과정에서 더욱 중요한 역할을 담당하게 될 것입니다. 왜냐하면 회수된 전력은 새로운 송전망에 연결될 때까지 기다릴 필요 없이, 생산성이 더 높은 컴퓨팅을 지원할 수 있기 때문입니다. 또한, 대응이 늦어지면 고가의 AI 자원이 충분히 활용되지 못한 채 방치될 가능성이 있으므로, 구매자가 실시간 제어 소프트웨어에 더 적극적으로 투자하는 이유도 바로 여기에 있습니다.

DCIM, BMS 및 IT 스택 전반에 걸친 고도의 통합이 지닌 복잡성

LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장은 여전히 중대한 제약에 직면해 있습니다. 바로 시설 시스템, IT 운영 및 워크로드 제어를 하나의 운영 가능한 루프로 통합하는 데 따르는 어려움입니다. 많은 구매자들은 대응을 안전하게 자동화하기 위해 자산 데이터, 전력 텔레메트리, 오케스트레이션 계층 간의 양방향 연결을 필요로 하고 있으며, 이로 인해 도입이 지연되고 가치 입증(PoV) 주기가 길어지고 있습니다. 각 벤더사는 보다 광범위한 운영 플랫폼에서 이에 대응하고 있으며, Nlyte는 단일 인터페이스를 통해 데이터센터, 코로케이션, 하이브리드 클라우드, 엣지에 대한 가시성을 제공하는 Operational AI 솔루션을 제공합니다. 이는 시장이 어디에서 마찰을 해소하려 하고 있는지를 보여줍니다. 그렇긴 하지만, LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장에서는 시스템 간 데이터 업데이트 빈도, 제어 권한, 벤더 인터페이스가 일치하지 않을 경우 여전히 문제가 발생하고 있습니다. 미래의 데이터센터 운영에 관한 조사에서도, 불완전하거나 일관성이 없는 텔레메트리 데이터를 바탕으로 조치를 취하는 것에 대한 우려를 반영하여, 운영자들이 AI 시스템에 더 많은 권한을 부여하는 데 신중한 태도를 보이고 있다는 점이 지적되었습니다. 통합이 용이해질 때까지는 LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장에서 기존 기업 환경이나 복잡한 코로케이션 환경에서의 도입은 계속해서 완만한 속도에 그칠 것으로 보입니다.

부문별 분석

2025년, AI 에너지 분석 및 관측 가능성은 LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장의 29.85%를 차지하며 가장 큰 솔루션 유형이 되었습니다. 이는 대부분의 운영 담당자가 개입을 자동화하기 전에 먼저 시각화 작업부터 시작하기 때문입니다. 회로 수준의 거의 실시간 텔레메트리 데이터가 없다면 워크로드 오케스트레이션이나 열 제어를 신뢰하기 어렵기 때문에 이 범주는 계속해서 LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장의 기반 계층을 형성하고 있습니다. Verdigris에 따르면, 이 회사의 센싱 플랫폼은 한 포춘 500대 기업의 운영자가 60곳 이상의 시설에서 1MW가 넘는 미활용 용량을 회복하는 데 기여했습니다. 또한 T-Mobile은 표준 경보 시스템 없이도 UPS 정류기 그룹의 4%에서 고장이 발생하기 21일 전에 성능 저하를 파악했습니다. 이러한 사례들은 구매자가 우선 측정에 투자하는 이유를 보여줍니다. 숨겨진 용량이나 조기 고장 위험이 가시화됨으로써, 도입에 대한 비즈니스 타당성이 더욱 탄탄해지기 때문입니다. 실제로, LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장에서 여전히 가장 큰 점유율을 차지하는 것은 데이터 품질, 전력 인텔리전스, 그리고 지속적인 가시성입니다.

지속가능성 인텔리전스 리포팅 시장은 2031년까지 연평균 성장률(CAGR) 27.34%로 확대될 것으로 예상되며, LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장에서 가장 빠르게 성장하는 솔루션 유형이 될 것입니다. 이러한 성장은 공시 의무 및 감사 요구 사항과 밀접한 관련이 있으며, 특히 유럽의 규정에 따라 데이터센터의 성과를 표준화된 형식으로 보고해야 하는 경우에 두드러집니다. 또한, LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장에서는 사업자들이 초기 도입 단계를 지나 와트당 연산 성능을 어떻게 높일 것인가라는 과제에 착수함에 따라, 오케스트레이션, 열 최적화, 디지털 트윈 도구에 대한 관심이 높아지고 있습니다. NVIDIA와 Jacobs는 AI 팩토리의 디지털 트윈을 활용한 프로젝트를 발표했습니다. 이는 실제 도입에 앞서 시설 설비의 효율, 열 성능, 처리량을 시뮬레이션하는 것으로, 계획 주도형 최적화로의 이러한 전환을 뒷받침합니다. LLM 및 생성형 AI 에너지 최적화 소프트웨어 시장 전반에서 각 기능을 별도의 도구로 분리하는 대신 관측 가능성, 스케줄링, 열 반응 및 보고 기능을 연계한 통합 제품군으로 나아가는 것이 일반적인 추세입니다.

2025년, LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장에서 클라우드 기반 솔루션이 66.41%의 점유율을 차지했습니다. 이는 집중형 배포 모델을 통해 분산된 환경 전체에 소프트웨어를 쉽게 배포할 수 있다는 장점을 반영한 것입니다. 많은 운영 사업자들이 여전히 지속적인 업데이트, 광범위한 원격 가시성, 그리고 여러 시설에 걸친 도입 부담 경감을 요구하고 있기 때문에 이 입지는 계속해서 견고하게 유지되고 있습니다. 그렇긴 하지만, LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장은 로컬 제어와 클라우드 분석이 공존할 수 있는 하이브리드 구조로 전환되고 있습니다. 이는 추론 지연이 문제가 되는 경우나, 시설의 제어 신호를 퍼블릭 클라우드의 엔드포인트에 전적으로 의존해서는 안 되는 경우에 특히 중요합니다. 이러한 환경에서 LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장은 알고리즘의 품질뿐만 아니라 아키텍처 선택에 의해서도 형성되고 있습니다.

하이브리드 방식은 2031년까지 연평균 성장률(CAGR) 26.92%를 나타낼 것으로 예측되며, LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장에서 가장 빠르게 성장하는 형태로 자리 잡고 있습니다. 그 주된 이유는 운영 사업자가 냉각 시스템이나 전력 시스템에 대한 로컬 제어와, 사이트 및 워크로드를 아우르는 광범위한 분석 중 하나를 선택해야 하는 상황을 원치 않기 때문입니다. Nlyte는 데이터센터, 코로케이션, 하이브리드 클라우드, 엣지 운영을 중심으로 Operational AI 플랫폼을 포지셔닝하고 있으며, 이는 각 벤더들이 이러한 수요 패턴에 맞추어 자사 제품을 조정하고 있는 현실을 반영하고 있습니다. 또한, 데이터 소재지, 네트워크 격리, 최적화 로직의 직접 제어가 여전히 필수적인 규제 대상 부문이나 국가 주도의 AI 프로그램의 경우, LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장에서도 On-Premise형 모델이 여전히 중요한 위치를 차지하고 있습니다. 그 결과, LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장의 도입 수요는 SaaS의 편의성 덕분에, AI 인프라가 실제로 구축·관리되고 있는 상황을 반영한 보다 혼합형 아키텍처로 확대되고 있습니다.

지역별 분석

2025년, 북미는 LLM 및 생성형 AI용 에너지 최적화 소프트웨어 시장 점유율의 34.56%를 차지하며 최대 지역 시장이 되었습니다. 해당 지역은 하이퍼스케일 및 클라우드 AI 인프라가 집중되어 있을 뿐만 아니라, 에너지, 냉각 및 컴퓨팅 관리를 통합한 솔루션에 대한 초기부터의 대규모 수요가 있었기 때문에 이러한 우위를 유지할 수 있었습니다. 백악관은 2025년 7월, 데이터센터 인프라 및 송전과 관련된 연방 정부의 허가 절차를 신속히 처리하기 위한 대통령령을 발령하여, 초기 단계부터 최적화 시스템이 필요한 AI 캠퍼스의 지속적인 확장을 지원했습니다. 캐나다에서는 2026년 초 연방 정부가 100MW를 초과하는 국가 AI 데이터센터에 대한 제안을 공모함에 따라 공공 부문 수요층이 추가되었습니다. 이러한 요인들이 복합적으로 작용하여, 2025년에도 북미는 시장의 중심적인 위치를 유지했으며, 2026년에 이르기까지 새로운 소프트웨어 수요를 지속적으로 뒷받침했습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 27.45%를 기록하며 성장할 것으로 예상되며, 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 일본은 경제산업성(METI)의 정책 개편과 소프트웨어 정의형 수냉식 시설을 위한 공동 프로그램을 통해 효율화 노력을 강화했습니다. 중국은 T/CCSA 619-2025에 따라 공식적인 평가 체계를 도입하고, 데이터센터의 에너지 효율 평가를 위한 AI 기반 방법을 마련했습니다. 한국에서는 선진적인 국가 AI 프로그램이 추진되고 있으며, Lablup과 Upstage가 국가 AI 기반 모델 프로젝트의 1단계 평가를 통과했습니다. 이러한 추세에 따라 아시아태평양에서는 규제적 압력, 인프라 구축, 국가 차원의 AI 투자가 맞물려 도입이 촉진되고 있습니다.

유럽은 생산 능력 확대와 체계적인 효율성, 그리고 보고 요건을 결합하고 있기 때문에 전략적으로 중요한 위치를 계속 차지하고 있습니다. 독일은 2026년 3월 국가 데이터센터 전략을 승인하고, 2030년까지 총 용량을 2배, AI 연산 능력을 4배로 확대하는 것을 목표로 하는 한편, 신규 자산에 대해 엄격한 효율성 및 재생에너지 활용 요건을 부과하고 있습니다. EU 차원의 체계 또한 대규모 데이터센터에 대해 표준화된 보고 요건을 부과함으로써 도입을 촉진하고 있으며, 이에 따라 소프트웨어 기반의 측정 및 정보 공개가 필수적입니다. 한편, 중동 및 아프리카 및 남미는 여전히 초기 단계의 기회를 제공하고 있으며, 각국의 AI 인프라 구축, 새로운 용량 확대 계획, 그리고 지속가능성과 연계된 인프라 조달에 대한 관심이 높아짐에 따라 도입이 진행될 것으로 전망됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the LLM and generative AI energy optimization software market size is expected to increase from USD 1.28 billion in 2025 to USD 1.58 billion in 2026 and reach USD 5.07 billion by 2031, growing at a CAGR of 26.26% over 2026-2031.

This report is Segmented by Solution Type (AI Energy Analytics and Observability, and More), Deployment Mode (Cloud-Based, Hybrid, and On-Premise), End User (Hyperscale Cloud and AI Infrastructure Providers, and More), Optimization Objective (Energy and Carbon Optimization, Cost Optimization, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global LLM and Generative AI Energy Optimization Software Market Trends and Insights

Rapid Growth of AI-Heavy Workloads In Data Centers

The LLM and generative AI energy optimization software market is being driven by the rapid expansion of training and inference workloads in modern data centers. A single NVIDIA H100 GPU node rated at 10.2 kW thermal design power drew only 76% of that level during transformer model training in measured tests, underscoring why planning based solely on nameplate ratings can leave operators with a distorted view of actual power behavior. At the cluster scale, that mismatch creates both planning errors and stranded capacity, because facilities still need enough thermal and electrical headroom to cover real-time workload swings. The LLM and generative AI energy optimization software market benefits from this shift because legacy monitoring tools were built for steadier enterprise loads and cannot manage rapid variation with the same precision. The International Energy Agency projected that electricity use from AI-focused data centers would triple by 2030 relative to 2025, underscoring the multi-year need for software that matches compute intensity with available power and cooling resources. As a result, the LLM and generative AI energy optimization software market is increasingly tied to whether operators can keep new GPU capacity active instead of leaving equipment underused while infrastructure catches up.

Rising Electricity Cost Exposure for AI Infrastructure Operators

The LLM and generative AI energy optimization software market is also benefiting from the fact that electricity exposure has moved closer to the center of infrastructure strategy. The International Energy Agency reported that data center electricity demand surged 17% in 2025 alone, while AI-focused facilities grew even faster, which raised the cost base that operators must manage in real time. The same update stated that capital expenditure by 5 large technology companies exceeded USD 400 billion in 2025 and is set to rise another 75% in 2026, which means the LLM and generative AI energy optimization software market now sits closer to revenue protection than simple utility savings. Hammerhead AI stated that each additional megawatt of stranded power recovered through orchestration can be worth USD 20 million to USD 50 million in constrained infrastructure markets, which changes the value logic behind optimization spending. That framing gives the LLM and generative AI energy optimization software market a stronger role in board-level investment decisions, because recovered power can support more productive compute without waiting for a new grid connection. It also explains why buyers are more willing to fund real-time control software when delayed action can leave expensive AI capacity underutilized.

High Integration Complexity Across DCIM, BMS, And IT Stack

The LLM and generative AI energy optimization software market still faces a significant restraint: the difficulty of integrating facility systems, IT operations, and workload controls into a single usable loop. Many buyers need bidirectional connections across asset data, power telemetry, and orchestration layers before they can safely automate any response, which slows deployment and lengthens proof-of-value cycles. Vendors are responding with broader operational platforms, and Nlyte positioned its Operational AI offering around data center, colocation, hybrid cloud, and edge visibility from a single interface, which shows where the market is trying to remove friction. Even so, the LLM and generative AI energy optimization software market still encounters problems when data refresh rates, control permissions, and vendor interfaces do not align across systems. Research on future data center operations also pointed to operator caution about granting more authority to AI systems, reflecting concern about acting on incomplete or inconsistent telemetry. Until integration becomes easier, the LLM and generative AI energy optimization software market will continue to see slower adoption in legacy enterprise estates and complex colocation environments.

Other drivers and restraints analyzed in the detailed report include:

- Regulation-Driven Need for Auditable Energy And Carbon Optimization

- Shift From Rule-Based DCIM to Agentic AI Orchestration

- Cybersecurity And Control-Plane Risk In Autonomous Optimization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

AI Energy Analytics and Observability held 29.85% of the LLM- and generative-AI energy-optimization software market in 2025, making it the largest solution type, as most operators start with visibility before automating any intervention. The category remains the base layer of the LLM and generative AI energy-optimization software market, since workload orchestration and thermal control are difficult to trust without circuit-level, near-real-time telemetry. Verdigris stated that its sensing platform helped one Fortune 500 operator recover more than 1 MW of stranded capacity across more than 60 facilities, while T-Mobile identified degradation in 4% of its UPS rectifier fleet 21 days before failure without standard alarms. Those examples show why buyers first spend on measurement: the operational case becomes stronger once hidden capacity and early failure risk become visible. In practice, the largest slice of the LLM and generative AI energy optimization software market still starts with data quality, electrical intelligence, and continuous observability.

Sustainability Intelligence and Reporting is expected to expand at a 27.34% CAGR through 2031, which makes it the fastest-growing solution type in the LLM and generative AI energy optimization software market. Its growth is tied to mandatory disclosure and audit needs, especially where data center performance must be reported in standardized formats under European rules. The LLM and generative AI energy optimization software market is also seeing stronger interest in orchestration, thermal optimization, and digital twin tools as operators move beyond first deployments and begin asking how to raise compute output per watt. NVIDIA and Jacobs announced work around AI factory digital twins to simulate facility equipment efficiency, thermal performance, and throughput before physical deployment, which supports this shift toward planning-led optimization. Across the LLM and generative AI energy optimization software market, the common direction is toward integrated suites that link observability, scheduling, thermal response, and reporting rather than keeping each function in a separate tool.

Cloud-Based solutions held 66.41% of the LLM and generative AI energy optimization software market in 2025, reflecting the ease of rolling out software across distributed estates through centralized delivery models. That position remains strong because many operators still want continuous updates, broad remote visibility, and lower deployment friction across multiple facilities. Even so, the LLM and generative AI energy optimization software market is moving toward hybrid setups where local control and cloud analytics can coexist. This is especially important where inference latency is sensitive or where facility control signals should not depend entirely on public cloud endpoints. In those environments, the LLM and generative AI energy optimization software market is being shaped by architecture choices as much as by algorithm quality.

Hybrid deployments are projected to grow at a 26.92% CAGR through 2031, which makes them the fastest-growing mode in the LLM and generative AI energy optimization software market. The main reason is that operators do not want to choose between local control over cooling and power systems and broader analytics that span sites and workloads. Nlyte positioned its Operational AI platform around data center, colocation, hybrid cloud, and edge operations, which reflects how vendors are adapting their products to this demand pattern. On-premises models also remain relevant in the LLM and generative AI energy optimization software market for regulated sectors and sovereign AI programs where data residency, network isolation, and direct control of optimization logic remain essential. As a result, deployment demand in the LLM and generative AI energy optimization software market is broadening from SaaS convenience toward a more mixed architecture that mirrors how AI infrastructure is actually being built and governed.

Complete Report Scope:

- By Solution Type

- AI Energy Analytics and Observability

- AI Workload Orchestration and Scheduling

- Thermal and Infrastructure Optimization

- Digital Twin and Simulation Platforms

- Sustainability Intelligence and Reporting

- By Deployment Mode

- Cloud Based

- Hybrid

- On Premises

- By End User

- Hyperscale Cloud and AI Infrastructure Providers

- Colocation Data Center Operators

- Enterprise Data Centers

- Sovereign and Government AI Infrastructure Operators

- By Optimization Objective

- Energy And Carbon Optimization

- Performance Optimization

- Cost Optimization

- Reliability And Availability Optimization

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America held 34.56% of the LLM and generative AI energy optimization software market share in 2025, making it the largest regional market. The region maintained this lead thanks to its concentration of hyperscale and cloud AI infrastructure, alongside early large-scale demand for integrated energy, cooling, and compute management. The White House issued an executive order in July 2025 to accelerate federal permitting for data center infrastructure and energy transmission, supporting continued expansion of AI campuses that require optimization systems from the outset. Canada added a public-sector demand layer when the federal government sought proposals for sovereign AI data centers above 100 MW in early 2026. Together, these factors kept North America at the center of the market in 2025 and sustained new software demand into 2026.

Asia-Pacific is projected to grow at a 27.45% CAGR through 2031, making it the fastest-growing geography in the market. Japan strengthened its efficiency efforts through METI policy updates and collaborative programs for software-defined liquid-cooling facilities. China introduced a formal evaluation framework with T/CCSA 619-2025, setting AI-based methods for data center energy-saving evaluation. South Korea's advanced national AI programs, with Lablup and Upstage passing Phase 1 evaluation under the sovereign AI foundation model project. These developments give Asia-Pacific a mix of regulatory pressure, infrastructure buildout, and national AI investment, driving adoption.

Europe remains strategically important because it combines capacity expansion with structured efficiency and reporting requirements. Germany approved a national data center strategy in March 2026, aiming to double total capacity and quadruple AI compute capacity by 2030, while tying new assets to strict efficiency and renewable power expectations. The wider EU framework also supports adoption by imposing standardized reporting requirements for larger data centers, making software-based measurement and disclosure unavoidable. Meanwhile, the Middle East, Africa, and South America remain earlier-stage opportunities, with adoption likely to follow sovereign AI buildouts, new capacity programs, and rising interest in sustainability-linked infrastructure procurement.

- Phaidra Inc.

- Sunbird Software, Inc.

- EkkoSense Limited

- Verdigris Technologies, Inc.

- GridPoint, Inc.

- Lancium Technologies

- Gridmatic

- WattTime

- C3.ai, Inc.

- Modius, Inc.

- Virtual Power Systems, Inc.

- FieldView Solutions, Inc.

- Equilibrium Energy, Inc.

- Tyba Energy, Inc.

- Verse, Inc.

- J4 Energy AG

- Hammerhead AI, Inc.

- Lablup, Inc.

- Enverus, Inc.

- Nlyte Software, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope Of The Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Growth Of AI-Heavy Workloads In Data Centers

- 4.2.2 Rising Electricity Cost Exposure For AI Infrastructure Operators

- 4.2.3 Regulation-Driven Need For Auditable Energy And Carbon Optimization

- 4.2.4 Shift From Rule-Based DCIM To Agentic AI Orchestration

- 4.2.5 Hidden Power And Cooling Stranding In GPU-Dense Facilities

- 4.2.6 Demand For Real-Time Workload Placement Across Compute And Energy Constraints

- 4.3 Market Restraints

- 4.3.1 High Integration Complexity Across DCIM, BMS, And IT Stack

- 4.3.2 Cybersecurity And Control-Plane Risk In Autonomous Optimization

- 4.3.3 Data Fragmentation Limits Model Accuracy And ROI Visibility

- 4.3.4 Long Procurement Cycles In Mission-Critical Infrastructure Environments

- 4.4 Impact Of Macroeconomic Factors On The Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power Of Buyers

- 4.8.2 Bargaining Power Of Suppliers

- 4.8.3 Threat Of New Entrants

- 4.8.4 Threat Of Substitutes

- 4.8.5 Intensity Of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution Type

- 5.1.1 AI Energy Analytics and Observability

- 5.1.2 AI Workload Orchestration and Scheduling

- 5.1.3 Thermal and Infrastructure Optimization

- 5.1.4 Digital Twin and Simulation Platforms

- 5.1.5 Sustainability Intelligence and Reporting

- 5.2 By Deployment Mode

- 5.2.1 Cloud Based

- 5.2.2 Hybrid

- 5.2.3 On Premises

- 5.3 By End User

- 5.3.1 Hyperscale Cloud and AI Infrastructure Providers

- 5.3.2 Colocation Data Center Operators

- 5.3.3 Enterprise Data Centers

- 5.3.4 Sovereign and Government AI Infrastructure Operators

- 5.4 By Optimization Objective

- 5.4.1 Energy And Carbon Optimization

- 5.4.2 Performance Optimization

- 5.4.3 Cost Optimization

- 5.4.4 Reliability And Availability Optimization

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Phaidra Inc.

- 6.4.2 Sunbird Software, Inc.

- 6.4.3 EkkoSense Limited

- 6.4.4 Verdigris Technologies, Inc.

- 6.4.5 GridPoint, Inc.

- 6.4.6 Lancium Technologies

- 6.4.7 Gridmatic

- 6.4.8 WattTime

- 6.4.9 C3.ai, Inc.

- 6.4.10 Modius, Inc.

- 6.4.11 Virtual Power Systems, Inc.

- 6.4.12 FieldView Solutions, Inc.

- 6.4.13 Equilibrium Energy, Inc.

- 6.4.14 Tyba Energy, Inc.

- 6.4.15 Verse, Inc.

- 6.4.16 J4 Energy AG

- 6.4.17 Hammerhead AI, Inc.

- 6.4.18 Lablup, Inc.

- 6.4.19 Enverus, Inc.

- 6.4.20 Nlyte Software, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space And Unmet-Need Assessment