|

시장보고서

상품코드

2072898

방광암 진단 키트 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Bladder Cancer Detection Kits - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

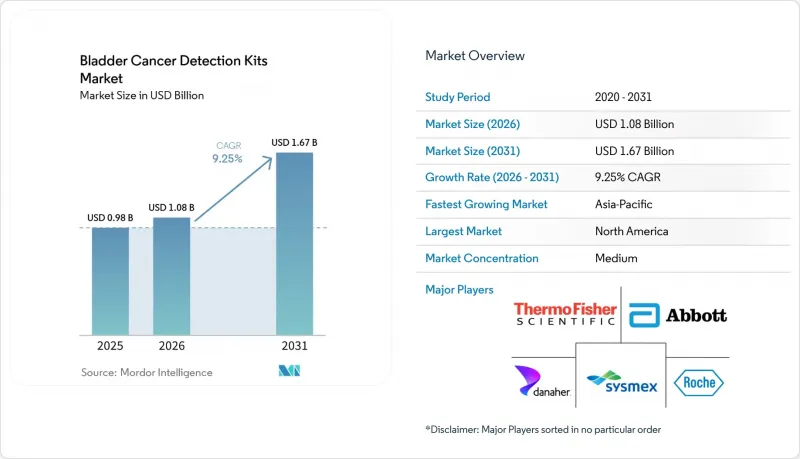

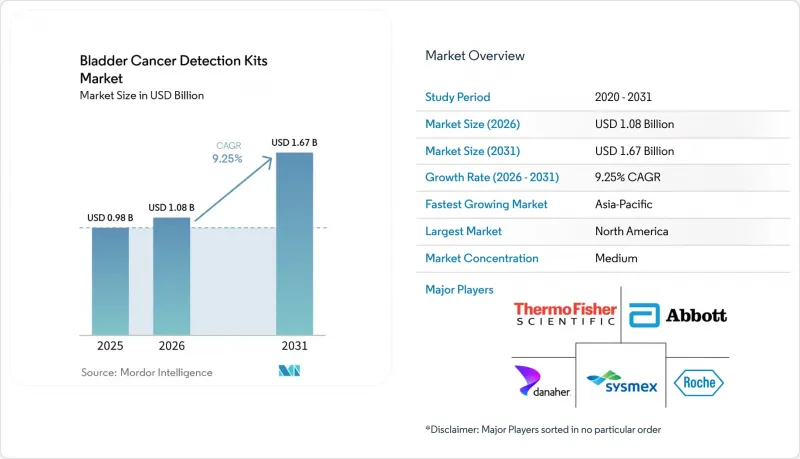

Mordor Intelligence에 의하면, 방광암 진단 키트 시장 규모는 2025년에 9억 8,000만 달러, 2026년에 10억 8,000만 달러가 되어, 2031년까지 16억 7,000만 달러에 이를 것으로 예측되며, 2026-2031년까지 CAGR 9.25%로 성장할 전망입니다.

본 보고서는 제품 유형(소변 검사용, 혈액 검사용, 조직 검사용, 기타), 기술(FISH, 면역 측정, 분자진단, DNA 메틸화·RNA 시그니처, 기타), 최종 사용자(병원·비뇨기과 클리닉, 진단 검사 기관, 암 연구 기관, 기타), 지역(북미, 유럽, 아시아태평양, 기타)별로 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

전 세계 방광암 진단 키트 시장 동향 및 인사이트

방광암 선별검사의 부담 증가

방광암 검출 키트 시장은 55세 이상 성인의 방광암 환자 수가 지난 30년 동안 22만 6,421건에서 48만 3,234건으로 증가함에 따라, 선별 검사 대상 인구의 확대라는 혜택을 누리고 있습니다. 이는 고령 환자가 가장 높은 위험군을 형성하고 있으며, 진단 및 치료 후에도 지속적으로 평가를 받아야 하는 주요 대상 집단으로 남아 있기 때문에 중요한 의미를 지닙니다. 또한, 재발 역시 검사 건수를 높은 수준으로 유지하는 요인이 되고 있습니다. 비근층침윤성 방광암(NMIBC) 환자 1명당 평생 평균 6.6회의 재발이 예상되므로, 신규 진단 건수 증가세가 둔화되더라도 지속적인 모니터링에 대한 수요는 계속 발생할 것입니다. 북미와 서유럽 등 고소득 지역은 여전히 가장 높은 유병률 부담을 안고 있으며, 이는 보험 환급 제도가 잘 갖춰져 있고 검사 역량이 뛰어난 시장에서 검사 이용이 꾸준히 증가하고 있음을 뒷받침합니다. 중국 역시 방광암 진단 키트 시장에 지속적인 수요 기반을 제공하고 있으며, 남성의 발병률은 2021년 10만 명당 9.1명에서 2035년까지 11.2명으로 증가할 것으로 예측됩니다.

비침습적 소변 검사로의 전환

방광암 검출 키트 시장은 2025년 AUA(미국비뇨기과학회)가 방광경 검사를 연기하기를 희망하는 중등도 위험군의 현미경적 혈뇨 환자를 위한 대안으로, 소변 내 바이오마커를 이용한 종양 마커 검사를 권장함에 따라 뚜렷한 임상적 호재를 얻었습니다. 이 권고가 중요한 이유는 소변 바이오마커 검사 결과가 음성일 경우, 해당 환자군의 암 발병 확률을 0.2-3.1%에서 0.1-0.4%로 낮출 수 있기 때문이며, 이로 인해 검사 대상자의 상당수에서 임상적 경과 관찰 방침이 변경되기 때문입니다. 또한, UroFollow 연구에서는 소변 내 마커와 초음파 검사를 결합함으로써, 저위험 및 중위험 비근층침윤성 방광암(NMIBC) 환자에서 백색광 방광경 검사를 대체할 수 있는 임상적으로 비열등한 경과 관찰법으로 유효함이 입증되었습니다. 이러한 전환을 뒷받침할 만큼 기술적 성능이 향상되었으며, 다중 표적 소변 DNA 검사의 경우, 이중 맹검 다기관 공동 전향적 임상시험에서 민감도 91.37%, 특이도 95.09%, AUC 0.9583이 보고되었습니다. 방광경 검사와 함께 시행되던 검사에서 개별적으로 의뢰되는 소변 검사로 판단 기준이 전환됨에 따라, 방광암 검출 키트 시장은 단독 키트 공급업체와 집중 검사 기관에게 더 광범위한 상업적 기반을 확보해 가고 있습니다.

진단의 기반으로서 방광경 검사에 대한 의존이 여전히 지속되고 있습니다.

방광암 검출 키트 시장은 여전히 구조적인 한계에 직면해 있습니다. 이는 2025년판 EAU NMIBC 지침에서 정기적인 추적 관찰 시 유연 방광경 검사는 세포진 검사나 기타 비침습적 검사로 대체할 수 없습니다고 명시되어 있기 때문입니다. 이러한 입장은 다발성 병변이나 고악성도 병변을 가진 환자에서 검출 누락에 대한 우려가 여전히 존재함을 반영하고 있으며, 검사 전 위험도가 높은 경우 음성 예측도는 여전히 낮은 수준을 유지하고 있습니다. 상업적인 측면에서 볼 때, 소변 마커는 진정한 대체 수단이라기보다는 보조 수단으로 채택되는 경우가 많으며, 이로 인해 방광경 검사 비용을 키트 기반 검사로 전환할 수 있는 범위가 제한되고 있습니다. 또한, 기존의 경과 관찰 관행 역시 이러한 경향을 더욱 강화하고 있습니다. 방광경 검사 실시 건수가 많기 때문에 내시경 검사가 계속해서 추적 관리의 중심에 자리 잡고 있으며, 바이오마커 데이터를 뒷받침하는 지표가 개선되더라도 변화 속도는 더디기 때문입니다. 이러한 상황에서 UroFollow 연구는 향후 경과 관찰의 방식을 바꿀 가능성이 있는 무작위 배정 임상시험을 통해 근거를 확립하기 위한 가장 강력한 노력 중 하나이므로, 중요한 의미를 지닙니다.

부문별 분석

2025년, 소변 검사 키트는 제품 유형별 매출의 52.31%를 차지하며 방광암 검출 키트 시장에서 가장 큰 점유율을 기록했습니다. 이러한 주도적인 위상은 일상적인 배뇨 시 방광 종양이 세포나 바이오마커를 소변으로 직접 방출한다는 이 질환의 생물학적 특성에 소변 검체가 얼마나 부합하는지를 반영하고 있습니다. 이러한 검체의 장점 덕분에, 소변 검사는 초기 혈뇨 검사, 비근층 침윤성 방광암(NMIBC)의 재발 모니터링, 그리고 치료 후 경과 관찰에 있어 실용적인 역할을 수행하고 있습니다. 조직 검사용 키트는 조직학적 확인이나 TURBT(경요도적 방광 종양 절제술) 후 평가에서 그 역할은 제한적이긴 하지만 안정적인 위치를 유지하고 있는 반면, 복잡성이 낮은 스트립 형태의 키트는 분자 검사 시설에 대한 접근이 제한된 환경에서 현장 진단(Point-of-Care) 분야에서 입지를 다지고 있습니다.

혈액 검사용 검출 키트는 2026년부터 2031년까지 연평균 성장률(CAGR) 11.38%를 나타낼 것으로 예측되며, 방광암 검출 키트 업계에서 가장 빠르게 성장하는 제품 부문이 될 전망입니다. BIOSPACE 2026년 5월, FDA가 방광 전적출술 후 근층 침윤성 방광암(MIBC) 환자를 대상으로, ctDNA를 통한 MRD(미세 잔존 병변)를 지표로 한 보조 치료로서 Signatera CDx와 Tecentriq의 병용 요법을 승인함에 따라 성장 국면이 바뀌었습니다. 이 결정으로 인해, 비근층침윤성 방광암(NMIBC)의 경우 비뇨기과 의사가 주도하는 소변 검사를 통한 경과 관찰과는 달리, 종양내과 의사가 주도하는 혈액 검사에 대한 수요가 생겨났습니다. 따라서 방광암 검출 키트 시장의 제품 구성은 소변 검사에서 벗어나기보다는 오히려 다양화되고 있습니다. 이는 이 두 가지 검사 방식이 서로 다른 질병 단계나 임상적 판단에 대응하기 때문입니다.

지역별 분석

북미는 2025년 방광암 검출 키트 시장의 38.22%를 차지하고 있으며, 방광암 바이오마커 보조 검사 분야에서 여전히 가장 확고한 지역 거점으로 자리 잡고 있습니다. 이 지역은 CLIA 인증 검사실의 촘촘한 네트워크, 비뇨기과 의사의 진료 건수가 많다는 점, 그리고 보험 적용 범위와 코딩이 명확해지면 새로운 검사를 수용할 수 있는 보험자 구조의 혜택을 누리고 있습니다. 미국은 특정 검사 방식에 대한 접근성을 신속하게 확대하거나 축소할 수 있는 급여 결정이 이루어지기 때문에 해당 수요의 대부분을 주도하고 있습니다. 2026년 5월 Tecentriq과 Signatera CDx의 병용 요법이 승인됨에 따라, 근층 침윤성 방광암 환자의 방광 전적출술 후 명확한 치료 결정과 혈액 기반 MRD 검사를 연계함으로써 북미 시장에 새로운 상업적 기회가 열렸습니다.

유럽은 방광암 진단 키트 시장에서 여전히 중요한 지역적 거점이며, 특히 독일은 증거 기반 연구와 검사실 준비 태세 면에서 두드러진 성과를 보이고 있습니다. UroFollow 연구는 독일 각지의 의료기관에서 실시되었으며, 이 지역에는 일상 진료에서 마커를 기반으로 한 감시 체계를 검증하는 데 필요한 임상 인프라가 갖춰져 있음이 밝혀졌습니다. 또한, 유럽은 가이드라인에 대한 영향력을 통해 도입을 주도하고 있습니다. EAU(유럽비뇨기과학회)의 권고안은 비근층침윤성 방광암(NMIBC)의 추적 관찰 과정에서 방광경 검사와 소변 마커를 어떻게 병행해야 하는지를 지속적으로 정의하고 있기 때문입니다. 이에 따라 해당 지역은 수요의 중심지일 뿐만 아니라, 향후 보험사들이 더 광범위하게 이를 수용하도록 뒷받침할 근거를 검증하는 장소로서도 상업적으로 중요한 위치를 계속 차지하고 있습니다.

아시아태평양은 방광암 진단 키트 시장에서 가장 빠르게 성장하고 있는 지역으로, 2031년까지 연평균 성장률(CAGR) 11.65%로 확대될 것으로 전망됩니다. 중국은 이러한 성장 추세의 중심적인 역할을 하고 있으며, 2021년에는 4만 5,114명의 사망자와 57만 636명의 방광암 유병자를 기록한 데 이어, 남성의 발병률은 2035년까지 계속 증가할 것으로 예측되고 있습니다. 2025년 4월, 중국 최초로 메틸화와 유전자 변이를 병행하여 요로상피암을 검출하는 제품이 출시된 것은 현지 질병 부담 증가에 따라 현지에서의 제품 개발이 본격화되기 시작했음을 보여줍니다. 일본에서는 고령화에 따라 정기적인 감시 조사의 필요성이 높아지고 있으며, 후속 검사를 위한 안정적인 환자 기반이 형성되어 있어 향후 수요가 더욱 증가할 것으로 예측됩니다. 남미, 중동 및 아프리카는 여전히 시장 규모가 작을 뿐만 아니라, 주요 도시권 이외의 지역에서는 집중형 분자 검사 시설에 대한 접근성이 제한적이기 때문에 이들 지역에서의 성장 속도는 여전히 둔화되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.09According to Mordor Intelligence, the bladder cancer detection kits market size is projected to be USD 0.98 billion in 2025, USD 1.08 billion in 2026, and reach USD 1.67 billion by 2031, growing at a CAGR of 9.25% from 2026 to 2031.

This report is Segmented by Product Type (Urine-Based, Blood-Based, Tissue-Based, Other), Technology (FISH, Immunoassay, Molecular Diagnostic, DNA Methylation and RNA Signature, Other), End User (Hospitals and Urology Clinics, Diagnostic Labs, Cancer Research Institutes, Other), and Geography (North America, Europe, Asia-Pacific, and More). Forecasts are Provided in Terms of Value (USD).

Global Bladder Cancer Detection Kits Market Trends and Insights

Rising Bladder Cancer Surveillance Burden

The bladder cancer detection kits market is benefiting from a larger surveillance population because bladder cancer cases in adults aged 55 and older rose from 226,421 to 483,234 over the past three decades. This matters because older patients form the highest-risk group and remain the core population for repeated evaluation after diagnosis and treatment. Recurrence also keeps testing volumes elevated, since each NMIBC patient faces a lifetime average of 6.6 recurrences, which creates repeated monitoring demand even when new diagnosis growth slows. High-income regions in North America and Western Europe still carry the heaviest incidence burden, which supports steady utilization in markets with stronger reimbursement and laboratory capacity. China adds another durable volume base to the bladder cancer detection kits market, with male incidence projected to rise from 9.1 per 100,000 in 2021 to 11.2 per 100,000 by 2035.

Shift Toward Non-Invasive Urine-Based Testing

The bladder cancer detection kits market gained a clear clinical tailwind in 2025 when the AUA endorsed urinary biomarker tumor markers as an option for intermediate-risk microscopic hematuria patients who prefer to defer cystoscopy. That recommendation matters because a negative urinary biomarker result can reduce cancer probability for these patients from 0.2-3.1% to 0.1-0.4%, which changes the clinical path for a meaningful part of the workup population. The UroFollow trial also showed that urine markers combined with ultrasound can support a clinically non-inferior surveillance alternative to white-light cystoscopy in low- and intermediate-risk NMIBC patients. Technical performance has improved enough to support this shift, with multitarget urine DNA tests reporting 91.37% sensitivity, 95.09% specificity, and 0.9583 AUC in double-blinded multicenter prospective testing. As more decisions move from bundled cystoscopy encounters to separately ordered urine tests, the bladder cancer detection kits market is gaining a broader commercial base for standalone kit suppliers and centralized laboratories.

Persistent Dependence on Cystoscopy as Diagnostic Anchor

The bladder cancer detection kits market still faces a structural ceiling because the 2025 EAU NMIBC Guidelines state that flexible cystoscopy cannot be replaced by cytology or any other non-invasive test in routine surveillance. That position reflects continued concern over missed detection in patients with multifocal disease or high-grade lesions, where negative predictive value remains under pressure at higher pre-test risk. The commercial effect is that urine markers are often adopted as adjuncts rather than as true substitutes, which limits how much cystoscopy spending can move into kit-based testing. Existing surveillance practice also reinforces itself, because high cystoscopy volumes keep the endoscopic visit at the center of follow-up care and make change slower even when supporting biomarker data improve. The UroFollow trial is important in this setting because it is one of the strongest efforts to produce randomized evidence that could shift future surveillance pathways.

Other drivers and restraints analyzed in the detailed report include:

- AI-Assisted Risk Stratification in Hematuria Workups

- Reimbursement Support for Adjunctive Urothelial Tests

- Limited Clinical Standardization Across Biomarker Panels

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Urine-Based Detection Kits held 52.31% of product-type revenue in 2025, giving them the largest share in the bladder cancer detection kits market. Their leading position reflects how closely urine sampling fits the disease biology, since bladder tumors shed cells and biomarkers directly into urine during routine voiding. That specimen advantage gives urine assays a practical role across initial hematuria workups, NMIBC recurrence surveillance, and follow-up after treatment. Tissue-based kits still retain a narrower but stable role in histological confirmation and post-TURBT assessment, while lower-complexity strip formats keep a point-of-care presence in settings with limited molecular laboratory access.

Blood-Based Detection Kits are projected to grow at an 11.38% CAGR from 2026 to 2031, making them the fastest-growing product segment in the bladder cancer detection kits industry. BIOSPACE The growth step changed in May 2026, when the FDA approved Signatera CDx together with Tecentriq for ctDNA MRD-guided adjuvant treatment in post-cystectomy MIBC patients. That decision created oncologist-led blood test demand that is distinct from the urologist-led urine surveillance pathway in NMIBC. The product mix in the bladder cancer detection kits market is therefore becoming broader rather than shifting away from urine, because the two formats are serving different disease stages and clinical decisions.

Complete Report Scope:

- By Product Type

- Urine-Based Detection Kits

- Blood-Based Detection Kits

- Tissue-Based Detection Kits

- Other Product Types

- By Technology

- Fluorescence In Situ Hybridization Kits

- Immunoassay Kits

- Molecular Diagnostic Kits

- DNA Methylation and RNA Signature Kits

- Other Technologies

- By End User

- Hospitals and Urology Clinics

- Diagnostic Laboratories

- Cancer Research Institutes

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 38.22% of the bladder cancer detection kits market share in 2025 and remains the most established regional base for adjunctive bladder cancer biomarker testing. The region benefits from a dense network of CLIA-certified laboratories, high urologist encounter volumes, and payer structures that can absorb new tests once coverage and coding become clear. The United States drives most of that demand because reimbursement decisions there can quickly widen or narrow access to specific assay formats. The May 2026 approval of Tecentriq with Signatera CDx adds a new commercial path in North America by linking blood-based MRD testing to a defined post-cystectomy treatment decision in muscle-invasive disease.

Europe remains a significant regional pillar in the bladder cancer detection kits market, with Germany standing out for evidence generation and laboratory readiness. The UroFollow trial was conducted across German centers, which shows that the region has the clinical infrastructure needed to test marker-guided surveillance pathways in routine practice. Europe also shapes adoption through guideline influence, since EAU recommendations continue to define how urine markers are used against cystoscopy in NMIBC follow-up. This keeps the region commercially important both as a demand center and as a proving ground for evidence that can support broader payer acceptance later.

Asia-Pacific is the fastest-growing region in the bladder cancer detection kits market and is projected to expand at an 11.65% CAGR through 2031. China is central to that trajectory because it carried 45,114 deaths and 570,636 prevalent bladder cancer cases in 2021, while male incidence is still projected to rise through 2035. The April 2025 launch of China's first dual methylation-plus-gene-mutation urothelial carcinoma detection product shows that local development is beginning to move alongside local disease burden. Japan adds another layer of demand because its aging population supports recurring surveillance needs and creates a stable patient base for follow-up testing. South America and the Middle East and Africa remain smaller opportunity pools, but the pace of expansion there is still limited by weaker access to centralized molecular laboratories outside major urban centers.

- Abbott Laboratories

- Beckton Dickinson

- Beckton Dickinson

- Bio-Rad Laboratories

- Cancer Diagnostics, Inc.

- Cxbladder / Pacific Edge Limited

- Danaher

- Exact Sciences

- Roche

- Hologic

- NanoString Technologies

- Nonagen Bioscience, Inc.

- Photocure ASA

- QIAGEN

- Siemens Healthineers

- Sysmex

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Bladder Cancer Surveillance Burden

- 4.2.2 Shift Toward Non-Invasive Urine-Based Testing

- 4.2.3 AI-Assisted Risk Stratification in Hematuria Workups

- 4.2.4 Reimbursement Support for Adjunctive Urothelial Tests

- 4.2.5 Rising Demand for Recurrence Monitoring in NMIBC

- 4.3 Market Restraints

- 4.3.1 Persistent Dependence on Cystoscopy as Diagnostic Anchor

- 4.3.2 Limited Clinical Standardization Across Biomarker Panels

- 4.3.3 Reimbursement Variability Across Health Systems

- 4.3.4 High Validation Cost for Novel Assays

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Urine-Based Detection Kits

- 5.1.2 Blood-Based Detection Kits

- 5.1.3 Tissue-Based Detection Kits

- 5.1.4 Other Product Types

- 5.2 By Technology

- 5.2.1 Fluorescence In Situ Hybridization Kits

- 5.2.2 Immunoassay Kits

- 5.2.3 Molecular Diagnostic Kits

- 5.2.4 DNA Methylation and RNA Signature Kits

- 5.2.5 Other Technologies

- 5.3 By End User

- 5.3.1 Hospitals and Urology Clinics

- 5.3.2 Diagnostic Laboratories

- 5.3.3 Cancer Research Institutes

- 5.3.4 Other End Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Abbott

- 6.3.2 Beckman Coulter, Inc.

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Bio-Rad Laboratories, Inc.

- 6.3.5 Cancer Diagnostics, Inc.

- 6.3.6 Cxbladder / Pacific Edge Limited

- 6.3.7 Danaher Corporation

- 6.3.8 Exact Sciences Corporation

- 6.3.9 F. Hoffmann-La Roche Ltd

- 6.3.10 Hologic, Inc.

- 6.3.11 NanoString Technologies, Inc.

- 6.3.12 Nonagen Bioscience, Inc.

- 6.3.13 Photocure ASA

- 6.3.14 Qiagen N.V.

- 6.3.15 Siemens Healthineers AG

- 6.3.16 Sysmex Corporation

- 6.3.17 Thermo Fisher Scientific Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-Space and Unmet-Need Assessment