|

시장보고서

상품코드

2072900

전자상거래 의류 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)E Commerce Apparel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

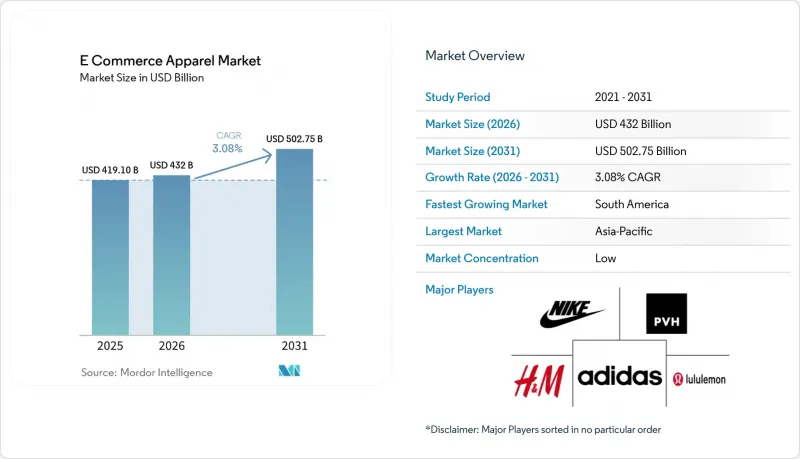

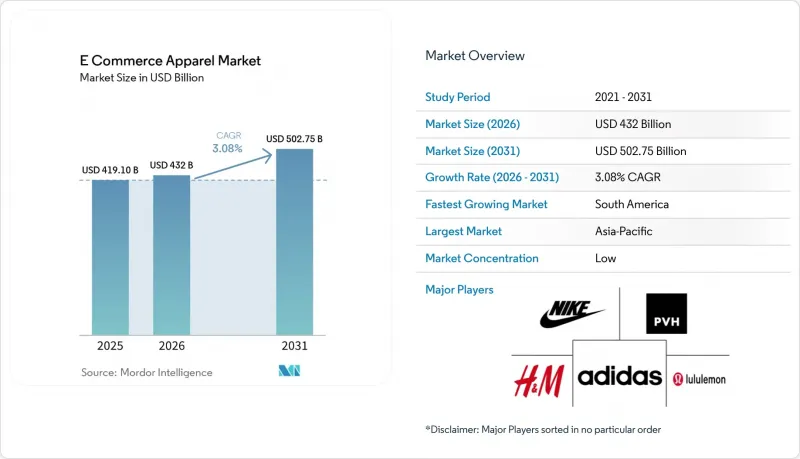

Mordor Intelligence에 의하면, 전자상거래 의류 시장은 2025년 4,191억 달러에서 2026년에는 4,320억 달러로 성장하여 2031년까지 5,027억 5,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 기간 CAGR은 3.08%를 나타낼 전망입니다.

본 보고서는 제품 유형(정장, 캐주얼 의류 등), 최종 사용자(남성, 여성, 아동), 원단 소재(면, 폴리에스터 등), 카테고리(대중 시장 및 프리미엄), 플랫폼 유형(제3자 마켓플레이스 및 자체 운영 플랫폼), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 전자상거래 의류 시장 동향과 인사이트

인터넷 및 스마트폰 보급률의 상승

인터넷과 스마트폰 보급률이 높아짐에 따라 디지털 연결성이 강화되어, 더 많은 소비자가 온라인 쇼핑 플랫폼에 손쉽게 접근할 수 있게 되었습니다. 스마트폰의 보급은 사용자가 언제든지 모바일 앱이나 웹사이트를 통해 패션 컬렉션을 둘러보고, 상품을 비교하며, 개인 맞춤형 추천을 받아 거래를 완료할 수 있게 함으로써 의류 구매 행태에 큰 영향을 미치고 있습니다. 국제전기통신연합(ITU)에 따르면, 2025년에는 전 세계 10세 이상 인구의 82%가 휴대전화를 소유하고 있었습니다. 보급률이 95% 이상의 ‘보편적 소유권”는 전 세계적으로 디지털 기기에 대한 접근이 점점 더 쉬워지고 있음을 보여줍니다. 스마트폰 사용자층의 확대는 모바일 상거래의 보급을 뒷받침하고 있으며, 의류 소매업체들은 디지털 마케팅, 소셜 커머스, 앱 기반 쇼핑 플랫폼을 통해 더 폭넓은 고객층에 접근할 수 있게 되었습니다.

디지털 결제 솔루션의 보급 확대

디지털 결제 솔루션의 보급이 확대됨에 따라, 더욱 신속하고 안전하며 편리한 온라인 쇼핑 경험이 가능해졌으며, 이는 의류 분야의 전자상거래 시장 확대를 뒷받침하고 있습니다. 디지털 지갑, 신용카드 및 직불카드, 실시간 결제 시스템, 그리고 “지금 구매, 후불(BNPL)”서비스와 같은 결제 기술의 발전으로 온라인 거래가 효율화되면서, 디지털 플랫폼을 통한 의류 구매에 대한 소비자의 신뢰가 높아지고 있습니다. 국제결제은행(BIS)에 따르면, 전 세계 무현금 거래액은 1조 9,768억에 달하며, 디지털 및 비접촉식 결제 수단으로의 전환이 두드러지고 있습니다. 안전한 결제 게이트웨이, 원클릭 결제 옵션, 부정 이용 방지 시스템, 유연한 결제 수단의 이용 가능성이 높아짐에 따라 거래 장벽이 낮아지고, 구매 완료율이 향상되고 있습니다.

소비자의 사이즈 및 착용감에 대한 우려

사이즈나 착용감에 대한 우려는 여전히 전자상거래 의류 시장에 있어 큰 과제로 남아 있습니다. 구매 전에 실제로 상품을 입어볼 수 없기 때문에 소비자들은 망설이거나 구매에 대한 확신을 잃는 경우가 종종 있습니다. 브랜드별 사이즈 기준의 차이, 체형의 차이, 의류 치수의 일관성 부족 등의 요인으로 인해, 소비자가 온라인에서 적절한 사이즈를 선택하기는 어렵습니다. 이 문제는 상품 반품 및 교환률 증가와 고객 불만으로 이어지며, 결과적으로 의류 소매업체의 업무 복잡성을 가중시키고 있습니다. 또한, 원단의 촉감이나 착용감에 대한 우려, 실제 상품과 온라인상의 표시가 다른 점도 구매 결정에 영향을 미치고 있습니다. 사이즈 문제로 인한 잦은 반품은 역물류, 재고 관리, 상품 취급과 관련된 비용을 증가시키고 있습니다.

부문별 분석

2025년, 캐주얼 의류는 제품 유형별 시장 점유율의 38.23%를 차지했습니다. 이는 진화하는 패션과 라이프스타일 트렌드에 발맞추어, 편안하고 활용도가 높으며 일상적으로 입을 수 있는 의류에 대한 소비자의 선호도가 높아지고 있기 때문입니다. 편안한 스타일로의 변화로 인해 기능성과 미적 매력을 겸비한 의류에 대한 수요가 증가하면서, 캐주얼 의류는 일상 생활, 사교 활동, 여가 활동은 물론 유연한 근무 환경에서도 인기 있는 선택지가 되고 있습니다. 온라인 플랫폼의 편의성은 소비자에게 다양한 스타일, 핏, 색상, 디자인을 접할 기회를 제공하고, 간편한 비교와 맞춤형 쇼핑 경험을 가능하게 함으로써 그 보급을 더욱 촉진하고 있습니다. 또한, 디지털 패션 트렌드에 대한 노출 증가, 소셜 미디어를 통한 스타일링 영감, 그리고 소비자의 취향 변화로 인해 정기적인 의류 구매와 옷장 업데이트 주기가 단축되고 있습니다.

스포츠웨어는 가장 빠르게 성장하고 있는 제품 유형으로, 2026년부터 2031년까지 연평균 성장률(CAGR) 4.11%를 나타낼 것으로 전망됩니다. 이러한 성장은 피트니스, 웰니스, 활동적인 라이프스타일이 소비자의 일상생활에 점점 더 깊이 스며들고 있는 데 기인합니다. 스포츠, 운동, 레크리에이션 활동에 참여하는 사람들이 늘어나면서, 운동 시뿐만 아니라 일상생활에서도 착용하기에 적합하고 기능성과 편안함을 겸비한 의류에 대한 수요가 크게 증가하고 있습니다. 미국 노동통계청에 따르면, 2024년 미국 남성의 약 94.2%가 스포츠나 여가 활동에 참여하고 있으며, 이는 활동적인 라이프스타일에 대한 소비자들의 강한 선호를 반영할 뿐만 아니라 스포츠웨어의 추가적인 보급을 촉진하고 있습니다. 또한, 기능성과 편안함, 스타일을 모두 갖춘 옷을 찾는 ‘애슬레저”에 대한 관심이 높아짐에 따라, 스포츠웨어의 활용 범위는 기존의 피트니스 목적을 넘어 확대되고 있습니다.

2025년에는 온라인 패션 플랫폼 이용의 확대와 다양한 상황 및 취향에 맞춘 다채로운 의류 스타일에 대한 강력한 수요에 힘입어, 최종 사용자 시장의 54.53%를 여성이 차지했습니다. 디지털 쇼핑 채널의 보급으로 인해 소비자들은 일상복, 비즈니스 복장, 상황에 맞는 옷차림, 트렌드를 중시하는 패션 등 폭넓은 컬렉션을 접할 수 있게 되었으며, 이로 인해 빈번한 구매 행위가 촉진되고 있습니다. 소셜 미디어의 영향력, 디지털 패션 컨텐츠, 유명인의 동향, 그리고 개인 맞춤형 스타일링 제안은 패션 탐색을 더욱 촉진하고 온라인 의류 구매를 활성화시켰습니다. 또한, 폭넓은 상품 라인업, 포용적인 사이즈 구성, 맞춤형 추천 기능, 고객 리뷰, 편리한 반품 정책 등의 특징이 쇼핑에 대한 신뢰감을 높여 온라인 이용을 촉진했습니다.

아동복 부문은 2026년부터 2031년까지 연평균 성장률(CAGR) 3.59%를 나타낼 것으로 예측되며, 최종 사용자 카테고리 중 가장 빠른 성장이 전망됩니다. 이러한 성장은 디지털 쇼핑 플랫폼을 통해 다양한 아동복에 손쉽게 접근하고자 하는 수요가 증가함에 기인합니다. 성장에 따른 의류 수요의 변화, 계절별 요구 사항, 그리고 스타일 선호도의 변화에 따라 온라인 채널을 통한 의류 구매가 증가하고 있습니다. 일상복, 특별한 날을 위한 옷, 학교 관련 옷, 특정 활동을 위한 옷 등 다양한 컬렉션이 갖춰져 있어, 소비자들은 다양한 연령대와 요구에 맞는 제품을 찾을 수 있습니다. 사이즈 가이드, 상품 추천, 고객 리뷰, 간편한 비교 도구, 간소화된 반품 절차 등 온라인 쇼핑 기능이 강화됨에 따라, 아동복을 온라인으로 구매하는 것에 대한 소비자의 신뢰는 더욱 높아지고 있습니다.

지역별 분석

2025년, 아시아태평양은 전 세계 전자상거래 의류 매출의 37.55%를 차지했습니다. 이는 디지털 쇼핑 생태계의 급속한 성장, 모바일 상거래의 높은 보급률, 그리고 온라인 패션 플랫폼에 대한 소비자의 참여 증가에 힘입은 결과입니다. 이러한 견고한 시장 지위는 인터넷에 대한 광범위한 접근성, 첨단 디지털 결제 시스템, 그리고 편의성이 뛰어난 의류 쇼핑 경험에 대한 선호도가 높아짐에 힘입어 유지되고 있습니다. 중화인민공화국 국무원에 따르면, 2025년 말 기준 중국의 인터넷 사용자 수는 11억 2,000만 명에 달하며, 온라인 소매의 성장을 견인하는 거대한 디지털 소비자 기반의 존재가 부각되고 있습니다. 다양한 패션 컬렉션 제공, 소셜 커머스 통합, 인플루언서 주도형 상품 탐색, 그리고 맞춤형 추천 및 라이브 스트리밍 쇼핑과 같은 기술을 활용한 쇼핑 기능은 아시아태평양이 전자상거래 의류 시장에서 주도적인 입지를 더욱 공고히 하고 있습니다.

남미는 2026년부터 2031년까지 연평균 성장률(CAGR) 5.11%를 기록하며 가장 빠르게 성장하는 지역이 될 것으로 전망됩니다. 이러한 성장은 디지털 기술의 보급 확대, 온라인 소매 인프라 확충, 그리고 편의성이 뛰어난 의류 구매 채널에 대한 소비자들의 선호도 증가에 힘입어 이루어지고 있습니다. 모바일 쇼핑 플랫폼, 안전한 결제 시스템, 물류 역량, 배송 네트워크의 강화로 인해 접근성이 향상되면서, 더 많은 소비자들이 온라인 패션 구매로 전환하도록 유도되고 있습니다. 소셜 미디어와 디지털 프로모션의 영향력이 커지고, 트렌드 주도형 패션 소비가 의류 전자상거래 플랫폼의 보급을 더욱 가속화함에 따라, 남미는 예측 기간 동안 가장 빠르게 성장하는 지역 시장이 될 전망입니다.

북미와 유럽은 성숙기에 접어든 전략적으로 중요한 시장으로, AI를 활용한 개인화, 옴니채널 소매 전략, 그리고 프리미엄 디지털 쇼핑 경험을 통해 성장이 점점 더 가속화되고 있습니다. 가상 피팅 솔루션, 예측형 추천, 데이터 기반 고객 참여 도구와 같은 첨단 기술이 온라인 의류 분야의 전환율을 높이고 소비자의 충성도를 높이고 있습니다. 중동 및 아프리카(MEA) 지역에서는 디지털 전환의 진전, 모바일 상거래의 확산, 물류 인프라의 개선, 그리고 온라인 패션 플랫폼의 입지 강화에 힘입어 성장세가 가속화되고 있습니다. 결제 솔루션의 확충, 의류 제품에 대한 접근성 향상, 그리고 ‘디지털 퍼스트’ 쇼핑 경험을 추구하는 소비자의 취향 변화가 이러한 신흥 시장에서 의류 전자상거래의 지속적인 성장을 뒷받침할 것으로 예측됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.09According to Mordor Intelligence, the e-Commerce apparel market is projected to grow from USD 419.10 billion in 2025 to USD 432 billion in 2026, with an anticipated value of USD 502.75 billion by 2031, registering a CAGR of 3.08% during the period 2026-2031.

This report is Segmented by Product Type (Formal Wear, Casual Wear, and More), End User (Men, Women, and Children), Fabric Material (Cotton, Polyester, and More), Category (Mass and Premium), Platform Type (Third-Party Marketplace and Company-Owned Platform) and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global E Commerce Apparel Market Trends and Insights

Rising internet and smartphone penetration

Increasing internet and smartphone penetration is enhancing digital connectivity, enabling more consumers to access online shopping platforms with ease. The widespread use of smartphones has significantly influenced apparel purchasing behavior by allowing users to browse fashion collections, compare products, receive personalized recommendations, and complete transactions through mobile applications and websites at any time. According to the International Telecommunication Union (ITU), in 2025, 82% of individuals aged 10 years or older globally owned a mobile phone . Universal ownership, defined as a penetration rate exceeding 95%, highlights the growing accessibility of digital devices worldwide. The expanding base of smartphone users is driving the adoption of mobile commerce, allowing apparel retailers to reach a broader audience through digital marketing, social commerce, and app-based shopping platforms.

Increasing adoption of digital payment solutions

The growing adoption of digital payment solutions is driving the expansion of the e-commerce apparel market by enabling faster, safer, and more convenient online shopping experiences. The development of payment technologies, such as digital wallets, credit and debit cards, instant payment systems, and buy-now-pay-later (BNPL) services, has streamlined online transactions and enhanced consumer trust in purchasing apparel through digital platforms. According to the Bank for International Settlements (BIS), global cashless transactions reached 1,976.8 billion, underscoring the shift toward digital and contactless payment methods. The increasing availability of secure payment gateways, one-click checkout options, fraud protection systems, and flexible payment alternatives is reducing transaction barriers and boosting purchase completion rates.

Size and fit uncertainty among consumers

Size and fit uncertainty remains a significant challenge for the e-commerce apparel market. The inability of consumers to physically try on products before purchase often leads to hesitation and diminished confidence. Factors such as varying sizing standards across brands, differences in body shapes, and inconsistencies in garment measurements make it difficult for shoppers to choose the correct fit online. This issue contributes to higher rates of product returns, exchanges, and customer dissatisfaction, thereby increasing operational complexities for apparel retailers. Furthermore, concerns about fabric feel, comfort, and discrepancies between the actual product and its online representation also impact purchasing decisions. Frequent returns due to sizing issues add to costs related to reverse logistics, inventory management, and product handling.

Other drivers and restraints analyzed in the detailed report include:

- Growth of virtual try-on and augmented reality (AR) technologies

- Influence of social media platforms and celebrity endorsements

- High product return and exchange challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Casual wear accounted for a 38.23% share of the product-type market in 2025, driven by increasing consumer preference for comfortable, versatile, and everyday apparel that aligns with evolving fashion and lifestyle trends. The shift toward relaxed dressing styles has fueled demand for clothing that combines functionality with aesthetic appeal, making casual apparel a popular choice for daily use, social activities, leisure, and flexible working environments. The convenience of online platforms has further supported adoption by offering consumers access to a wide range of styles, fits, colors, and designs, enabling easy comparison and personalized shopping experiences. Additionally, growing exposure to digital fashion trends, social media-driven styling inspiration, and frequent changes in consumer preferences have encouraged regular apparel purchases and faster wardrobe refresh cycles.

Sportswear is the fastest-growing product type, with a CAGR of 4.11% projected for 2026-2031. This growth is driven by the increasing integration of fitness, wellness, and active lifestyles into consumers' daily routines. Rising participation in sports, exercise, and recreational activities has significantly increased demand for performance-oriented and comfortable apparel suitable for both athletic and everyday use. According to the Bureau of Labor Statistics, in 2024, approximately 94.2% of men in the United States engaged in sports and leisure activities, reflecting a strong consumer inclination toward active lifestyles and supporting greater adoption of sportswear . Furthermore, the growing popularity of athleisure trends, where consumers seek clothing that combines functionality, comfort, and style, has expanded sportswear usage beyond traditional fitness purposes.

In 2025, women accounted for 54.53% of the end-user market, driven by increased engagement with online fashion platforms and strong demand for a wide variety of apparel styles catering to different occasions and preferences. The growing adoption of digital shopping channels has provided consumers with access to extensive collections, including everyday clothing, professional attire, occasion wear, and trend-focused fashion, fostering frequent purchasing behavior. Social media influence, digital fashion content, celebrity trends, and personalized styling recommendations have further supported fashion discovery and boosted online apparel purchases. Additionally, features such as broader product selections, inclusive sizing, customized recommendations, customer reviews, and convenient return policies have enhanced shopping confidence and encouraged online adoption.

The children's segment is expected to be the fastest-growing end-user category, with a projected CAGR of 3.59% during 2026-2031. This growth is attributed to the rising demand for convenient access to a wide range of children's apparel through digital shopping platforms. Frequent changes in children's clothing needs due to growth, seasonal requirements, and evolving style preferences are driving increased apparel purchases via online channels. The availability of diverse collections, including everyday wear, occasion wear, school-related clothing, and activity-specific apparel, enables consumers to find suitable products for various age groups and needs. Enhanced online shopping features, such as size guides, product recommendations, customer reviews, easy comparison tools, and simplified return processes, are further boosting consumer confidence in purchasing children's apparel online.

Complete Report Scope:

- By Product Type

- Formal Wear

- Casual Wear

- Sportswear

- Nightwear

- Intimate and Loungewear

- Other Product Types

- By End User

- Men

- Women

- Children

- By Fabric Material

- Cotton

- Polyester

- Nylon

- Denim

- Other Fabric Types

- By Category

- Mass

- Premium

- By Platform Type

- Third-Party Marketplace

- Company-owned Platform

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Geography Analysis

Asia-Pacific accounted for a 37.55% share of global e-commerce apparel revenues in 2025, driven by the rapid growth of digital shopping ecosystems, high mobile commerce adoption, and increasing consumer engagement with online fashion platforms. This strong market position is supported by widespread internet accessibility, advanced digital payment systems, and a growing preference for convenient apparel shopping experiences. According to the State Council of the People's Republic of China, China had 1.12 billion internet users by the end of 2025, underscoring the significant digital consumer base fueling online retail growth . The availability of diverse fashion collections, integration of social commerce, influencer-driven product discovery, and technology-enabled shopping features such as personalized recommendations and livestream shopping further reinforce Asia-Pacific's leadership in the e-commerce apparel market.

South America is projected to be the fastest-growing region, with a CAGR of 5.11% during 2026-2031. This growth is supported by increasing digital adoption, expanding online retail infrastructure, and a rising consumer preference for convenient apparel purchasing channels. Enhancements in mobile shopping platforms, secure payment systems, logistics capabilities, and delivery networks are improving accessibility and encouraging more consumers to transition to online fashion purchases. The growing influence of social media, digital promotions, and trend-driven fashion consumption is further accelerating the adoption of e-commerce apparel platforms, positioning South America as the fastest-expanding regional market during the forecast period.

North America and Europe represent mature yet strategically significant markets, where growth is increasingly driven by AI-powered personalization, omnichannel retail strategies, and premium digital shopping experiences. Advanced technologies such as virtual fitting solutions, predictive recommendations, and data-driven customer engagement tools are enhancing online apparel conversion rates and fostering consumer loyalty. The Middle East and Africa (MEA) region is gaining traction through rising digital transformation, increasing mobile commerce adoption, improved logistics infrastructure, and the growing presence of online fashion platforms. Enhanced payment solutions, broader apparel accessibility, and evolving consumer preferences for digital-first shopping experiences are expected to support the continued growth of e-commerce apparel in these emerging markets.

- Nike, Inc.

- Adidas AG

- H & M Hennes & Mauritz AB

- Inditex, S.A.

- Lululemon Athletica Inc.

- PVH Corp.

- VF Corporation

- Gap Inc.

- Ralph Lauren Corporation

- Under Armour, Inc.

- ASICS Corporation

- Puma SE

- Levi Strauss and Co.

- Hanesbrands Inc.

- Gildan Activewear Inc.

- Fast Retailing Co., Ltd.

- Kering S.A.

- Burberry Group plc

- Moncler S.p.A.

- Tapestry, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising internet and smartphone penetration

- 4.2.2 Increasing adoption of digital payment solutions

- 4.2.3 Growth of virtual try-on and augmented reality (AR) technologies

- 4.2.4 Influence of social media platforms and celebrity endorsements

- 4.2.5 Demand for fast fashion and frequent style updates

- 4.2.6 Direct-to-consumer (DTC) brand growth

- 4.3 Market Restraints

- 4.3.1 Size and fit uncertainty among consumers

- 4.3.2 High product return and exchange challenges

- 4.3.3 Concerns regarding product quality and authenticity

- 4.3.4 Data privacy and cybersecurity concerns

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Formal Wear

- 5.1.2 Casual Wear

- 5.1.3 Sportswear

- 5.1.4 Nightwear

- 5.1.5 Intimate and Loungewear

- 5.1.6 Other Product Types

- 5.2 By End User

- 5.2.1 Men

- 5.2.2 Women

- 5.2.3 Children

- 5.3 By Fabric Material

- 5.3.1 Cotton

- 5.3.2 Polyester

- 5.3.3 Nylon

- 5.3.4 Denim

- 5.3.5 Other Fabric Types

- 5.4 By Category

- 5.4.1 Mass

- 5.4.2 Premium

- 5.5 By Platform Type

- 5.5.1 Third-Party Marketplace

- 5.5.2 Company-owned Platform

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.1.4 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 Italy

- 5.6.2.4 France

- 5.6.2.5 Spain

- 5.6.2.6 Netherlands

- 5.6.2.7 Poland

- 5.6.2.8 Belgium

- 5.6.2.9 Sweden

- 5.6.2.10 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 Indonesia

- 5.6.3.6 South Korea

- 5.6.3.7 Thailand

- 5.6.3.8 Singapore

- 5.6.3.9 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Colombia

- 5.6.4.4 Chile

- 5.6.4.5 Peru

- 5.6.4.6 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 United Arab Emirates

- 5.6.5.4 Nigeria

- 5.6.5.5 Egypt

- 5.6.5.6 Morocco

- 5.6.5.7 Turkey

- 5.6.5.8 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Nike, Inc.

- 6.4.2 Adidas AG

- 6.4.3 H & M Hennes & Mauritz AB

- 6.4.4 Inditex, S.A.

- 6.4.5 Lululemon Athletica Inc.

- 6.4.6 PVH Corp.

- 6.4.7 VF Corporation

- 6.4.8 Gap Inc.

- 6.4.9 Ralph Lauren Corporation

- 6.4.10 Under Armour, Inc.

- 6.4.11 ASICS Corporation

- 6.4.12 Puma SE

- 6.4.13 Levi Strauss and Co.

- 6.4.14 Hanesbrands Inc.

- 6.4.15 Gildan Activewear Inc.

- 6.4.16 Fast Retailing Co., Ltd.

- 6.4.17 Kering S.A.

- 6.4.18 Burberry Group plc

- 6.4.19 Moncler S.p.A.

- 6.4.20 Tapestry, Inc.