|

시장보고서

상품코드

2072957

저전력 소프트웨어 설계 프레임워크 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Low-Power Software Design Framework - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

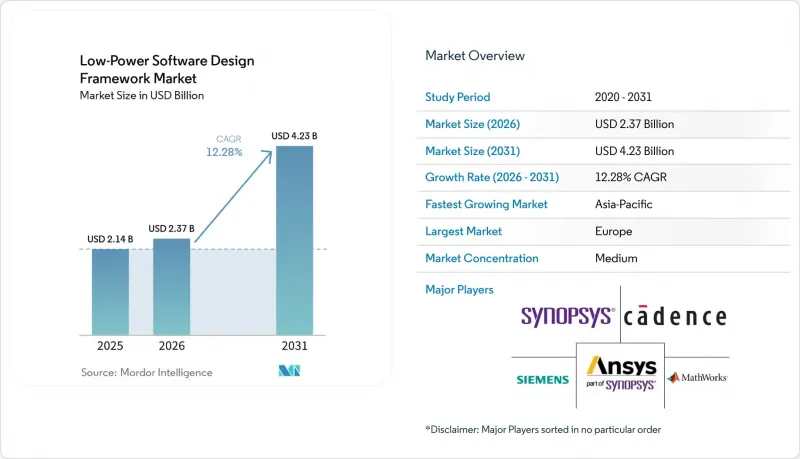

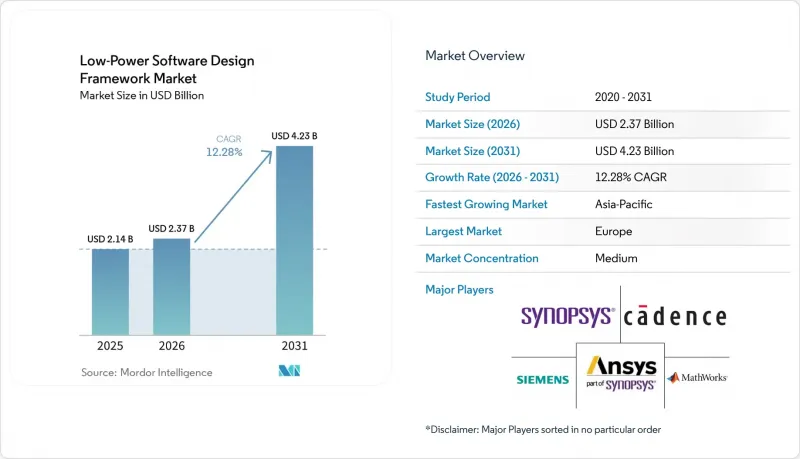

Mordor Intelligence에 의하면, 저전력 소프트웨어 설계 프레임워크 시장 규모는 2025년 21억 4,000만 달러에서 2026년에는 23억 7,000만 달러로 확대되어 2031년까지 42억 3,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 12.28%로 성장할 전망입니다.

본 보고서는 제품 유형(설계·아키텍처 소프트웨어 등), 기술(모델 기반 설계 등), 도입 모델(On-Premise, 클라우드 기반, 하이브리드), 용도(소비자용 전자기기, 자동차 등), 최종 사용자(반도체 및 팹리스 설계 회사 등), 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

전 세계 저전력 소프트웨어 설계 프레임워크 시장 동향 및 인사이트

에너지 효율이 뛰어난 엣지 AI 도입

에너지 효율이 뛰어난 엣지 AI의 도입은 저전력 소프트웨어 설계 프레임워크 시장 수요를 견인하는 가장 뚜렷한 시장 성장 촉진요인 중 하나로 자리 잡고 있습니다. 현재 신경망 추론은 센서 및 컨트롤러 수준으로 점차 이동하고 있으며, 이 수준에서는 장치가 밀리와트 또는 서브밀리와트 수준에서 작동하기 때문에 비효율적인 펌웨어 동작은 용납되지 않습니다. 이러한 변화로 인해 엔지니어링 팀은 설계 주기의 이전보다 훨씬 더 이른 단계에서 모델 압축, 메모리 사용량 및 전원 상태 제어를 연계해야만 합니다. 율리히 연구센터(Forschungszentrum Julich)는 2026년 하노버 메세에서 "Automaton Engine" 프로젝트를 발표했습니다. 이 프로젝트에서는 와트당 지연 시간을 핵심 최적화 목표로 삼아, 엣지 AI 설계의 우선순위가 최고 연산 성능을 추구하는 것에서 실용적인 에너지 효율로 점차 전환되고 있음을 입증했습니다. MathWorks는 2026년 4월, 이러한 방향성을 한층 더 강화하여 Simulink Copilot이 탑재된 R2026a를 출시했습니다. 이를 통해 엔지니어들은 AI 지원 개발 기능이 통합된 공통 워크플로우 내에서 모델의 동작과 임베디드 코드 생성을 검증할 수 있게 되었습니다. TinyML 런타임의 표준화가 진행됨에 따라, 저전력 소프트웨어 설계 프레임워크 시장에서는 단순한 기본 추론 배포뿐만 아니라, 훈련 및 배포 전 검증 단계에서의 툴체인 수준의 에너지 프로파일링을 둘러싸고 더욱 치열한 경쟁이 펼쳐질 것으로 예측됩니다.

커넥티드 기기의 배터리 수명 최적화

커넥티드 기기의 배터리 수명 최적화는 저전력 소프트웨어 설계 프레임워크 시장을 더욱 심층적인 소프트웨어 중심의 에너지 관리 방향으로 이끌고 있습니다. 대규모 센서 군, 웨어러블 기기 및 원격 노드는 수동으로 배터리를 교체하는 데 비용이 많이 들거나 현실적으로 불가능한 장소에서 작동하는 경우가 많기 때문에 제품 팀은 더 이상 배터리 수명을 하드웨어만의 문제로만 다루지 않습니다. 2025년에 발표된 조사에 따르면, NB-IoT의 저전력 매개변수에 적용된 적응형 소프트 액터-크리티컬 강화 학습을 통해 하드웨어를 변경하지 않고도 배터리 수명을 3배 이상 연장할 수 있는 것으로 나타났습니다. 이로 인해 펌웨어 정책 설계 및 검증 도구의 가치가 더욱 높아지고 있습니다. Nordic Semiconductor는 2026년 3월, nRF Fuel Gauge v2.0을 발표하며 이러한 추세를 가속화했습니다. 이 제품에는 변화하는 방전 조건에 대응하는 적응형 배터리 상태 모니터링 기능과 실시간 상태 보고 기능이 도입되었습니다. 더 넓은 의미에서 보면, 간헐적이고 적응적인 에너지 거동은 사후적으로 측정할 뿐만 아니라 소프트웨어를 통해 관리해야 한다는 것입니다. 따라서 저전력 소프트웨어 설계 프레임워크 시장에서는 연결된 기기의 에너지 공급 불확실성에 대응할 수 있는 체크포인트 기능, 상태 유지 및 실행 시 스케줄링 기법에 대한 수요가 증가하고 있습니다.

도메인 간 전력 모델 검증에 따르는 막대한 부담

크로스 도메인 전력 모델에 따른 높은 검증 부담은 저전력 소프트웨어 설계 프레임워크 시장에 여전히 큰 제약 요인으로 작용하고 있습니다. SoC 및 임베디드 아키텍처에서 전기적, 열적, 기계적 거동이 더욱 밀접하게 통합됨에 따라, 각 엔지니어링 그룹이 개별적으로 관리하는 고립된 워크플로를 통해 전력 거동을 검증하는 것은 더 이상 불가능해졌습니다. 이 과제는 특정 도메인의 설계 변경이 다른 도메인의 타이밍, 발열, 누설 전류, 신뢰성에 영향을 미칠 수 있는 자동차, 산업용 자동화 및 첨단 노드 반도체 프로그램에서 더욱 심각해집니다. 시노프시스는 2026년, Ansys 2026 R1과 그 “Multiphysics Fusion”이 접근 방식을 도입했을 때 이 문제를 강조했습니다. 이 접근 방식은 다중 물리 엔진을 EDA 툴과 연동하는 것으로, 2026년 시점에서도 고객들의 시범 도입이 확대되고 있었습니다. 통합이 개선되더라도, 전력 소비 도메인으로의 변경이나 AI를 활용한 레이아웃 결정이 이루어질 때마다, 전력 소비 의도 준수 및 사인오프의 일관성을 확인해야 하는 상호작용의 수가 증가합니다. 즉, 저전력 소프트웨어 설계 프레임워크 시장은 가장 까다로운 프로그램의 경우, 설계 자동화의 발전 속도가 완벽한 검증 능력의 향상을 앞지르는 현실적인 한계에 직면해 있습니다.

부문별 분석

2025년 기준으로, 저전력 소프트웨어 설계 프레임워크 시장 규모의 28.74%를 "전력 소비 분석 및 최적화 소프트웨어"가 차지하고 있는 반면, "도입 및 수명 주기 관리 소프트웨어"는 2031년까지 연평균 성장률(CAGR) 13.45%로 성장할 것으로 전망됩니다. "전력 소비 분석 및 최적화 소프트웨어"가 시장을 선도하고 있는 배경에는 특히 첨단 노드의 경우, 소비 전력 사인오프가 테이프아웃 전의 마지막 단계 중 하나이며, 이를 간과할 경우 막대한 비용이 드는 재설계를 초래할 수 있다는 인식이 있습니다. 저전력 소프트웨어 설계 프레임워크 시장에서 이 분야는 누설 전류, 상태 전환 및 열적 상호작용이 더 이상 부차적인 튜닝 문제가 아니라 양산상의 위험 요소로 간주되게 되었다는 사실로부터 혜택을 보고 있습니다. 이러한 입지 덕분에, 인접한 카테고리가 성장세를 보이고 있는 상황에서도 전력 분석 도구는 견실한 수익 기반을 유지하고 있습니다.

케이던스는 2025년 3월, 자사의 "Conformal AI Low Power" 기능을 탑재한 “Conformal AI Studio”을 발표하고, 파워 사인오프 환경에서 계층적이며 분산형 검증 흐름이 설계 규모 관리에 어떻게 활용되는지를 입증했습니다. 설계·아키텍처, 소프트웨어, 시뮬레이션, 모델링 소프트웨어는 사인오프 시작 전에 초기 단계의 탐색이 필요하기 때문에 계속해서 안정적으로 도입되고 있습니다. 검증 및 승인용 소프트웨어 역시 자동차 및 산업용 프로그램의 문서화 요건 강화로 인한 혜택을 누리고 있습니다. 이러한 분야에서는 안전성 및 보안 요구사항과 마찬가지로, 전력 소비 동향도 추적 가능해야 합니다. 동시에, 저전력 소프트웨어 설계 프레임워크 업계에서는 배포 및 라이프사이클 관리용 소프트웨어의 성장이 가속화되고 있습니다. 이는 무선 업데이트(OTA) 계획, 차량군의 에너지 소비 양상, 그리고 기기의 장기 유지보수가 동일한 밸류체인의 일부가 되어가고 있기 때문입니다. 지멘스는 2026년, 제조 적합성과 설계 워크플로우를 더욱 긴밀하게 연계한 "Fuse EDA AI Agent"을 발표하며, 이러한 방향성을 뒷받침했습니다. 이는 설계 단계와 운영 단계 간의 전력 관리 경계가 점차 좁아지고 있음을 시사하는 것이었습니다.

2025년에는 모델 기반 설계가 27.63%의 점유율을 차지했으나, AI 지원형 저전력 설계는 2031년까지 14.12%라는 가장 높은 연평균 성장률(CAGR)을 나타낼 전망입니다. 모델 기반 설계는 추적 가능성이 보장된 워크플로를 제공하고, 규제 대상 엔지니어링 환경을 지원하며, 팀이 시뮬레이션과 코드 생성을 연계하는 데 도움을 주기 때문에 저전력 소프트웨어 설계 프레임워크 시장에서 여전히 핵심적인 위치를 차지하고 있습니다. 자동차 및 항공우주 분야의 도입 기반은 일관된 모델에서 코드로 이어지는 계보와 확립된 검증 절차에 의존하고 있기 때문에 단기간 내에 이를 대체하기는 어렵습니다. 저전력 소프트웨어 설계 프레임워크 시장에서 이는 새로운 AI 중심 기법이 확산되고 있는 상황에서도 기존 모델 기반 워크플로우에 확고한 입지를 확보해 주고 있습니다.

MathWorks는 2026년 4월, Simulink Copilot이 탑재된 R2026a를 출시하고, 르네사스 플랫폼을 위한 임베디드 지원을 확대함으로써 이 부문을 강화했습니다. 이를 통해 AI를 활용한 개발과 하드웨어 중심의 실행 흐름 간의 연계가 더욱 직접적으로 이루어지게 되었습니다. 하드웨어 인 더 루프(HIL) 시뮬레이션, 신속 제어 프로토타이핑 및 임베디드 시스템 프로토타이핑은 전력 검증의 범위가 논리 동작에 그치지 않고 보다 현실적인 작동 조건까지 확대됨에 따라 계속해서 주목을 받고 있습니다. AI를 활용한 저전력 설계는 합성 후 튜닝 단계에서 프런트엔드 설계 거버넌스 단계로 전환됨에 따라 더욱 빠르게 발전하고 있습니다. 이로 인해 전력 소비 제한이 더 이른 단계에서 도입되어, 보다 체계적으로 다루어지고 있습니다. 또한, 분산된 펌웨어 팀들이 버전 관리, 시뮬레이션, 그리고 각 거점 간의 전력 소비 분석을 위한 공유 환경을 점점 더 필요로 하고 있기 때문에 클라우드 네이티브 공동 개발도 진전되고 있습니다. 따라서 저전력 소프트웨어 설계 프레임워크 업계는 성숙한 워크플로가 기존 고객 기반을 안정화시키는 한편, AI를 활용한 기법이 복잡성 증가와 신규 프로젝트 출범에 대응하는 '양극화' 단계에 접어들었습니다.

지역별 분석

2025년, 아시아태평양은 저전력 소프트웨어 설계 프레임워크 시장의 36.45%를 차지하며 지역별 시장에서 1위를 차지했습니다. 이 지역은 중국, 일본, 한국, 대만에서 활발하게 진행되고 있는 반도체 설계 활동의 혜택을 받고 있으며, 이들 지역에서는 첨단 노드 프로그램과 대량 생산되는 임베디드 제품의 파이프라인이 파워 사인오프, 시뮬레이션 및 검증 도구에 대한 안정적인 수요를 창출하고 있습니다. 저전력 소프트웨어 설계 프레임워크 시장은 아시아태평양에서 특히 견조한 성장세를 보이고 있습니다. 이 지역에서는 각국이 최첨단 칩 설계 생태계와 대규모 하류 제조 및 제품 개발 역량을 모두 갖추고 있습니다. 또한 방갈로르, 하이데라바드, 푸네 등의 도시에서 엔지니어링 서비스 제공업체들이 사업을 확장함에 따라 인도의 중요성도 높아지고 있으며, 개발, 프로토타이핑 및 규정 준수 대응을 위한 소프트웨어 환경에 대한 수요가 증가하고 있습니다. 호주는 지속 가능한 원격 감지 및 에너지 수확 기술을 갖춘 커넥티드 시스템에 대한 조사 및 시범 사업을 통해, 규모는 작지만 중요한 역할을 수행하고 있습니다.

북미는 하이퍼스케일러의 실리콘 프로그램, 자동차용 반도체 분야의 활동, 그리고 주요 EDA 공급업체들의 지역적 입지에 힘입어 저전력 소프트웨어 설계 프레임워크 시장에서 2위를 차지했습니다. 많은 플랫폼 공급업체, 선진적인 설계 팀, AI 기반 검증 프로그램이 이 지역에 집중되어 있기 때문에 미국은 여전히 중심적인 위치를 차지하고 있습니다. 시노프시스는 2026년 5월, 20개 고객사가 25종 이상의 전문 AI 에이전트를 아우르는 에이전트 기반 설계 솔루션을 평가 중이라고 발표했습니다. 이는 해당 지역에서 차세대 EDA 기법에 대한 활발한 검증이 이루어지고 있음을 반영합니다. 캐나다와 멕시코는 팹리스 설계의 성장과 전자기기 제조 서비스를 통해 수요를 뒷받침하고 있으며, 이로 인해 라이프사이클 및 도입에 중점을 둔 도구에 대한 지역적 수요가 증가하고 있습니다.

유럽은 2031년까지 연평균 성장률(CAGR) 13.92%를 나타낼 것으로 예측되며, 저전력 소프트웨어 설계 프레임워크 시장에서 가장 두드러진 성장을 보일 지역 부문이 될 전망입니다. 주요 촉진요인은 생산량에 기반한 것이 아니라 규제나 산업적 요인에 기인한 것이며, 새로운 대기 전력 규제 및 사이버 보안 의무로 인해 제품 팀이 펌웨어와 검증 도구의 사양을 정의하는 방식이 변화하고 있습니다. EU는 2025년 5월부터 시행되는 규정에 따라 대기 전력 제한 기준을 개정했으며, 이에 따라 네트워크 연결 기기 및 소비자용 기기의 조달 결정 과정에서 에너지 예산 수립 및 검증의 우선순위가 높아졌습니다. 또한, '사이버 회복탄력성법'에 따라 2026년 9월부터 취약점 보고 및 소프트웨어 문서화 의무가 추가됨에 따라, 전원 상태 관리 외에도 감사 가능한 펌웨어 설계 및 소프트웨어 부품 목록(SBOM)의 실천을 지원할 수 있는 프레임워크에 대한 수요가 높아지고 있습니다. 독일은 산업 자동화와 첨단 EDA(전자 설계 자동화) 간의 연계가 활발히 이루어지고 있어, 여전히 이 지역의 중심지로 자리 잡고 있습니다. 한편, 중동 및 아프리카 및 남미는 주로 특정 스마트시티나 엣지 센싱 도입과 관련된, 아직 초기 단계에 머무르는 비즈니스 기회 수준에 그치고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.03According to Mordor Intelligence, the low-power software design framework market size is expected to increase from USD 2.14 billion in 2025 to USD 2.37 billion in 2026 and reach USD 4.23 billion by 2031, growing at a CAGR of 12.28% over 2026-2031.

This report is Segmented by Product Type (Design and Architecture Software, and More), Technology (Model-Based Design, and More), Deployment Model (On-Premises, Cloud-Based, and Hybrid), Application (Consumer Electronics, Automotive, and More), End User (Semiconductor and Fabless Design Houses, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Low-Power Software Design Framework Market Trends and Insights

Energy-Efficient Edge AI Adoption

Energy-efficient edge AI adoption is becoming one of the clearest drivers of demand for the low-power software design framework market. Neural network inference is now moving closer to the sensor and controller levels, where devices operate at milliwatt or sub-milliwatt levels and cannot tolerate inefficient firmware behavior. That shift is forcing engineering teams to link model compression, memory use, and power-state control much earlier in the design cycle than before. Forschungszentrum Julich presented its Automaton Engine project at Hannover Messe 2026, with latency per watt as a core optimization target, demonstrating how edge AI design priorities are moving away from peak compute claims and toward usable energy efficiency. MathWorks reinforced this direction in April 2026, releasing R2026a with Simulink Copilot, which allows engineers to examine model behavior and embedded code generation within a common workflow that now includes AI-assisted development support. As TinyML runtimes become more standardized, the low-power software design framework market is likely to see stronger competition around toolchain-level energy profiling during training and pre-deployment validation, rather than just basic inference deployment.

Battery Lifetime Optimization in Connected Devices

Battery lifetime optimization in connected devices is pushing the low-power software design framework market toward deeper software-centric energy management. Product teams are no longer treating battery life as a hardware-only issue because large sensor fleets, wearables, and remote nodes often operate in places where manual battery replacement is expensive or impractical. Research published in 2025 showed that adaptive soft-actor-critic reinforcement learning applied to NB-IoT power-saving parameters could extend battery life by more than 3x without hardware changes, which shifts more value toward firmware policy design and verification tools. Nordic Semiconductor added to this trend in March 2026 with nRF Fuel Gauge v2.0, which introduced adaptive battery health monitoring and real-time state-of-health reporting across changing discharge conditions. The broader implication is that intermittent and adaptive energy behavior must now be managed in software, not just measured after the fact. That is why the low-power software design framework market is benefiting from demand for checkpointing, state retention, and runtime scheduling methods that can respond to the uncertainty of energy availability in connected devices.

High Verification Burden For Cross-Domain Power Models

The high verification burden for cross-domain power models remains a significant restraint on the market for low-power software design frameworks. As SoC and embedded architectures combine electrical, thermal, and mechanical behavior more tightly, teams can no longer validate power behavior through isolated workflows owned by separate engineering groups. The challenge becomes more severe in automotive, industrial automation, and advanced-node semiconductor programs where design changes in one domain can affect timing, heat, leakage, and reliability in another. Synopsys highlighted this issue in 2026 when it introduced Ansys 2026 R1 and its Multiphysics Fusion approach, which links multiphysics engines with EDA tools and was still in the process of expanding customer trials during 2026. Even with better integration, every change to power domains or AI-assisted layout decisions expands the number of interactions that must be checked for power-intent compliance and sign-off consistency. This means the low-power software design framework market faces a practical ceiling where design automation is advancing faster than full verification capacity in the most demanding programs.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Energy-Harvesting MCU Toolchains

- Software-Defined Power Budgeting in Always-On Devices

- Fragmented Toolchains Across MCU, RTOS, And Compiler Stacks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Power Analysis and Optimization Software held 28.74% of the low-power software design framework market size in 2025, while Deployment and Lifecycle Management Software is projected to grow at a 13.45% CAGR through 2031. The leadership of Power Analysis and Optimization Software recognizes that power sign-off remains one of the final gates before tapeout, especially at advanced nodes, where missed violations can trigger costly redesigns. In the low-power software design framework market, this type benefits from the fact that leakage, state transitions, and thermal interactions are now being treated as production risks rather than secondary tuning issues. That position gives power analysis tools a durable revenue base even as adjacent categories gain momentum.

Cadence introduced Conformal AI Studio in March 2025, featuring its Conformal AI Low Power capability, demonstrating how hierarchical and distributed verification flows are used to manage design scale in power sign-off environments. Design and Architecture, Software, Simulation, and Modeling Software continue to see stable adoption because teams still need early-stage exploration before sign-off begins. Verification and Sign-Off Software is also benefiting from stronger documentation requirements in automotive and industrial programs, where power behavior has to be traceable alongside safety and security expectations. At the same time, the low-power software design framework industry is seeing stronger growth in Deployment and Lifecycle Management Software because over-the-air update planning, fleet energy behavior, and long-term device maintenance are becoming part of the same value chain. Siemens supported this direction in 2026 with its Fuse EDA AI Agent, which more closely linked manufacturing readiness and design workflows and signaled that the boundary between design-time and operational power management is narrowing.

Model-Based Design accounted for 27.63% share in 2025, while AI-Assisted Low-Power Design is projected to record the fastest CAGR of 14.12% through 2031. Model-Based Design remains central to the low-power software design framework market because it offers traceable workflows, supports regulated engineering environments, and helps teams connect simulation with code generation. Its installed base in automotive and aerospace is difficult to displace quickly because those programs depend on consistent model-to-code lineage and established validation routines. In the low-power software design framework market, this gives incumbent model-based workflows a defensible position even as newer AI-centric methods expand.

MathWorks strengthened this segment in April 2026 when it released R2026a with Simulink Copilot and extended embedded support for Renesas platforms, which connected AI-assisted development more directly with hardware-oriented execution flows. Hardware-In-The-Loop Simulation, Rapid Control Prototyping, and Embedded System Prototyping continue to gain attention because power validation now extends beyond logic behavior into more realistic operating conditions. AI-Assisted Low-Power Design is advancing faster as it shifts from post-synthesis tuning toward front-end design governance, where power limits are introduced earlier and handled more systematically. Cloud-Native Collaborative Development is also advancing because distributed firmware teams increasingly need shared environments for versioning, simulation, and cross-site power analysis. The low-power software design framework industry is therefore entering a two-speed phase where mature workflows keep the installed base stable while AI-assisted methods capture incremental complexity and new project starts.

Complete Report Scope:

- By Product Type

- Design and Architecture Software

- Simulation and Modeling Software

- Verification and Sign-Off Software

- Power Analysis and Optimization Software

- Deployment and Lifecycle Management Software

- By Technology

- Model-Based Design

- Hardware-In-The-Loop Simulation

- Rapid Control Prototyping

- Embedded System Prototyping

- AI-Assisted Low-Power Design

- Cloud-Native Collaborative Development

- By Deployment Model

- On-Premises

- Cloud-Based

- Hybrid

- By Application

- Consumer Electronics

- Automotive

- Industrial Automation

- Healthcare and Wearables

- Aerospace and Defense

- IoT and Smart Devices

- By End User

- Semiconductor and Fabless Design Houses

- Electronic OEMs

- Engineering Service Providers

- Academic and Research Institutions

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Turkey

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

Asia-Pacific accounted for 36.45% of the low-power software design framework market in 2025, making it the leading regional market. The region benefits from dense semiconductor design activity across China, Japan, South Korea, and Taiwan, where advanced-node programs and large-volume embedded product pipelines create a steady demand for power-signoff, simulation, and verification tools. The low-power software design framework market is particularly strong in Asia-Pacific, where countries combine leading chip design ecosystems with major downstream manufacturing and product development capacity. India is also becoming more important as engineering service providers expand in cities such as Bangalore, Hyderabad, and Pune, which increases demand for development, prototyping, and compliance-oriented software environments. Australia adds a smaller but relevant layer through research and pilot activity around sustainable remote sensing and energy-harvesting connected systems.

North America ranked second in the low-power software design framework market, supported by hyperscaler silicon programs, automotive semiconductor activity, and the regional presence of major EDA vendors. The United States remains central because many platform vendors, advanced design teams, and AI-driven verification programs are concentrated there. Synopsys stated in May 2026 that 20 customers were evaluating agentic design solutions across more than 25 specialized AI agents, reflecting the strong testing of next-generation EDA methods in the region. Canada and Mexico add supporting demand through fabless design growth and electronics manufacturing services, which increase the regional need for lifecycle- and deployment-focused tools.

Europe is projected to expand at a 13.92% CAGR through 2031, making it the fastest-growing regional segment in the low-power software design framework market. The main drivers are regulatory and industrial rather than volume-based, with new standby power rules and cybersecurity obligations changing how product teams specify firmware and validation tools. The EU updated standby power limits with a regulation effective from May 2025, which raised the priority of energy budgeting and verification in procurement decisions for networked and consumer devices. The Cyber Resilience Act also adds vulnerability reporting and software documentation obligations from September 2026, which increases demand for frameworks that can support auditable firmware design and software bill of materials practices alongside power-state management. Germany remains the regional center of gravity because industrial automation and advanced EDA collaboration are strong there, while the Middle East, Africa, and South America remain earlier-stage opportunities tied mainly to selective smart-city and edge-sensing deployments.

- Synopsys, Inc.

- Cadence Design Systems, Inc.

- Siemens Industry Software Inc.

- Ansys, Inc.

- The MathWorks, Inc.

- Keysight Technologies, Inc.

- Altair Engineering Inc.

- Altium Limited

- Zuken Inc.

- Silvaco Group, Inc.

- Aldec, Inc.

- COMSOL AB

- Dassault Systemes

- Imperas Software Ltd.

- IAR Systems AB

- Xpeedic Technology Co., Ltd.

- Empyrean Technology Co., Ltd.

- Typhoon HIL, Inc.

- PTC Inc.

- Vector Informatik GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Energy-Efficient Edge AI Adoption

- 4.2.2 Battery Lifetime Optimization in Connected Devices

- 4.2.3 Rise of Energy-Harvesting MCU Toolchains

- 4.2.4 Software-Defined Power Budgeting in Always-On Devices

- 4.2.5 Model-Based Design Adoption for Early Power Validation

- 4.2.6 Secure-By-Design Firmware and Compliance Pressure

- 4.3 Market Restraints

- 4.3.1 High Verification Burden for Cross-Domain Power Models

- 4.3.2 Fragmented Toolchains Across MCU, RTOS, and Compiler Stacks

- 4.3.3 Shortage of Low-Power Embedded Verification Talent

- 4.3.4 Higher Qualification Cost for AI-Assisted Autogeneration

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Design and Architecture Software

- 5.1.2 Simulation and Modeling Software

- 5.1.3 Verification and Sign-Off Software

- 5.1.4 Power Analysis and Optimization Software

- 5.1.5 Deployment and Lifecycle Management Software

- 5.2 By Technology

- 5.2.1 Model-Based Design

- 5.2.2 Hardware-In-The-Loop Simulation

- 5.2.3 Rapid Control Prototyping

- 5.2.4 Embedded System Prototyping

- 5.2.5 AI-Assisted Low-Power Design

- 5.2.6 Cloud-Native Collaborative Development

- 5.3 By Deployment Model

- 5.3.1 On-Premises

- 5.3.2 Cloud-Based

- 5.3.3 Hybrid

- 5.4 By Application

- 5.4.1 Consumer Electronics

- 5.4.2 Automotive

- 5.4.3 Industrial Automation

- 5.4.4 Healthcare and Wearables

- 5.4.5 Aerospace and Defense

- 5.4.6 IoT and Smart Devices

- 5.5 By End User

- 5.5.1 Semiconductor and Fabless Design Houses

- 5.5.2 Electronic OEMs

- 5.5.3 Engineering Service Providers

- 5.5.4 Academic and Research Institutions

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Turkey

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 United Arab Emirates

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Synopsys, Inc.

- 6.4.2 Cadence Design Systems, Inc.

- 6.4.3 Siemens Industry Software Inc.

- 6.4.4 Ansys, Inc.

- 6.4.5 The MathWorks, Inc.

- 6.4.6 Keysight Technologies, Inc.

- 6.4.7 Altair Engineering Inc.

- 6.4.8 Altium Limited

- 6.4.9 Zuken Inc.

- 6.4.10 Silvaco Group, Inc.

- 6.4.11 Aldec, Inc.

- 6.4.12 COMSOL AB

- 6.4.13 Dassault Systemes

- 6.4.14 Imperas Software Ltd.

- 6.4.15 IAR Systems AB

- 6.4.16 Xpeedic Technology Co., Ltd.

- 6.4.17 Empyrean Technology Co., Ltd.

- 6.4.18 Typhoon HIL, Inc.

- 6.4.19 PTC Inc.

- 6.4.20 Vector Informatik GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment