|

시장보고서

상품코드

2073003

난소암 치료제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Ovarian Cancer Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

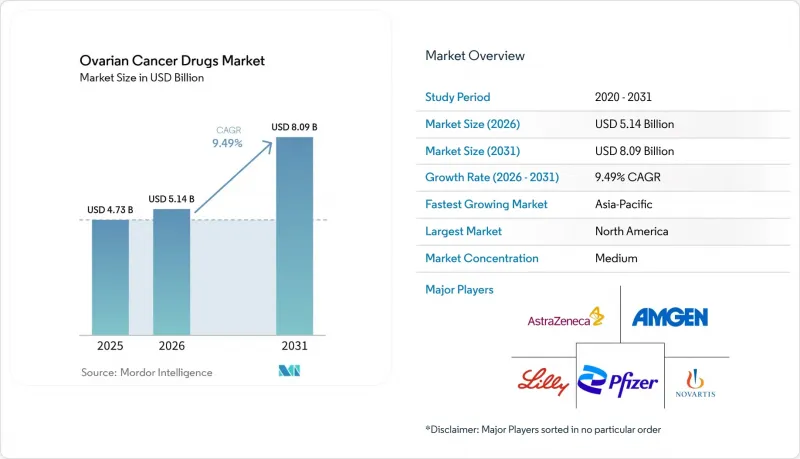

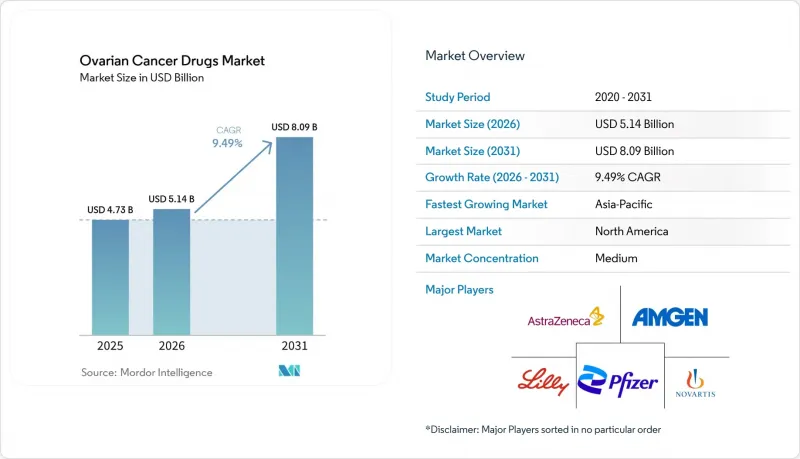

Mordor Intelligence에 의하면, 난소암 치료제 시장 규모는 2025년 47억 3,000만 달러에서 2026년에는 51억 4,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 9.49%로 성장을 지속하여, 2031년에는 80억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 종양의 유형(상피성, 생식세포성, 간질세포성), 약제의 유형(알킬화제, 유사분열 억제제, VEGF/VEGFR 억제제, PARP 억제제, 기타), 유통 채널(병원 약국, 드럭스토어, 기타), 최종 사용자(병원 등), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 난소암 치료제 시장 동향 및 분석

BRCA 및 HRD에 기반한 PARP 억제제 사용 확대

난소암 치료제 시장은 1차 치료 및 유지 요법 분야에서 HRD와 관련된 치료 적응증의 확대에 힘입어 계속해서 혜택을 보고 있습니다. 2026년 3월, 니라파리브용 MyChoice CDx가 FDA 승인을 받음에 따라, HRD 양성 환자를 선별하기 위한 진단적 근거가 강화되었으며, 공식적인 검사 워크플로우 하에서 PARP 치료 대상으로 특정할 수 있는 환자 수가 증가했습니다. 장기 생존에 관한 근거 또한, 특히 유지 요법이 일상 진료에 정착된 경우, BRCA 변이를 가진 질환의 치료 계획에서 PARP 억제제가 계속해서 중심적인 위치를 차지하는 요인이 되고 있습니다. 동시에, 내성 관련 조사 결과에 따르면 치료 순서나 과거 화학요법 이력이 이후 PARP 억제제에 대한 반응에 영향을 미칠 가능성이 있으므로, 환자 선정만으로는 향후 보급 여부가 결정되는 것은 아니라는 점이 밝혀졌습니다. 따라서 난소암 치료제 시장은 의사가 바이오마커 데이터를 치료 방침 결정에 어떻게 반영하느냐에 더욱 좌우되고 있습니다. 또한, 이는 진단 정확도 향상, 치료 순서 전략, 그리고 장기 유지 요법에 관한 추적 증거에 대한 지속적인 투자를 뒷받침하는 것입니다.

백금 내성 질환에서 FRa 표적 ADC의 적용 확대

난소암 치료제 시장은 백금 내성 질환에서 FRa를 표적으로 하는 항체-약물 복합체(ADC)를 통해 새로운 성장 동력을 확보하고 있습니다. 밀베투크시맙·솔라반타신과 관련된 생존 기간에 대한 더욱 강력한 근거는 그동안 지속적인 효과를 기대할 수 있는 차별화된 치료 옵션이 거의 없었던 상황에서 FRa를 표적으로 하는 치료의 역할을 한층 더 공고히 했습니다. 이는 중요한 의미를 지닙니다. 이는 백금 내성 질환에 대한 미충족 의료 수요가 크며, 치료법이 임상적 유효성과 명확한 환자 선정 기준을 모두 충족할 경우 빠르게 보급되는 경향이 있기 때문입니다. 또한, 난소암 치료제 시장에서는 특히 고가의 생물학적 제제가 승인 단계에서 국민건강보험 적용 단계로 전환되는 과정에서 임상시험 데이터와 마찬가지로 보험 급여 및 의료기술평가가 도입 여부를 좌우하고 있음이 밝혀졌습니다. 이에 따라, 특히 생존율이나 삶의 질(QOL)에 관한 근거가 접근 결정의 지침이 되는 의료 제도에서 승인 후 가치 입증을 위한 상업적 중요성이 더욱 커지고 있습니다. 또한, 이는 표적 치료제를 보유한 개발 기업이 판매 규모를 확대하기 위해서는 가격 책정의 유연성, 바이오마커의 명확화, 그리고 지역별 접근 계획이 필요함을 의미합니다.

PARP 내성 및 교차 내성의 급속한 출현

난소암 치료제 시장은 PARP 내성 메커니즘에 대한 규명이 가속화되고 있는 탓에 뚜렷한 성장 제약을 겪고 있습니다. 최근 연구에서는 동형 재조합 복구의 회복, 복제 포크의 안정화, 약물 배출의 변화 등 여러 가지 내성 기전이 규명되었습니다. 이는 내성이 보다 명확하게 정의되어, 치료 계획 수립 시 이를 무시하기 어려워졌음을 의미합니다. 또한, PARP 억제제에 내성을 보이는 종양은 고유한 생물학적 취약성을 발달시킬 가능성이 있는 것으로 밝혀졌으며, 이는 내성이 단일 현상이 아니며 획일적인 대응만으로는 관리할 수 없다는 사실이 입증되었습니다. 상업적인 측면에서 볼 때, 이로 인해 동일한 약물군에서 이용할 수 있는 효과적인 치료 옵션의 수가 줄어들게 되며, 환자 1인당 창출할 수 있는 수익 기간이 제한됩니다. 따라서 난소암 치료제 시장은 암이 진행된 후 동일한 계열의 약물을 반복적으로 사용하는 것보다는 차세대 치료제나 보다 명확하게 정의된 치료 순서 체계로 나아가고 있습니다. 이러한 압력으로 인해, 지속적인 표적 치료의 혜택을 여전히 누릴 수 있는 환자를 식별할 수 있는 동반 바이오마커와 임상 모니터링 도구의 가치도 높아지고 있습니다.

부문별 분석

2025년, 상피성 난소암은 매출의 63.21%를 차지하며, 난소암 치료제 시장에서 여전히 가장 큰 비중을 차지하는 암 유형이었습니다. 이러한 집중도는 도입 요법, 유지 요법, 재발 치료의 각 단계에서 고악성도 장액성 종양이 임상적으로 큰 비중을 차지하고 있음을 반영하고 있습니다. 또한, 상피성 종양은 BRCA 변이 양성 및 HRD 양성 환자의 비율이 가장 높기 때문에 이 부문에서는 정밀 의학이 가장 중요하게 여겨지고 있습니다. 그 결과, 난소암 치료제 업계는 여전히 상업적 및 임상적 노력의 대부분을 상피성 질환에 집중하고 있습니다. 이러한 집중 경향은 검사, 치료 알고리즘, 근거 창출이 모두 이 분야에서 더욱 성숙해짐에 따라, 제약 기업에게 사업 확장을 위한 길을 더욱 명확하게 제시하고 있습니다.

배아세포성 난소암은 2031년까지 연평균 성장률(CAGR) 9.81%를 나타낼 것으로 예측되며, 난소암 치료제 시장에서 가장 빠르게 성장하는 종양 유형 하위 부문이 될 전망입니다. 이러한 성장은 현재의 환자 수보다는 기존에는 광범위한 화학요법으로 치료되어 왔던 희귀한 아형의 분자적 특성에 대한 규명이 진전된 데 기인합니다. 디스게르미노마 및 관련 종양에 대한 잠재적 표적 관련 연구 결과는 많은 환자에서 화학요법이 여전히 높은 반응률을 보인다는 점을 바탕으로, 보다 정밀한 치료법의 단계적 도입을 뒷받침하고 있습니다. 또한, 간질성 종양 역시 호르몬과 관련된 생물학적 특성으로 인해 보다 전문적인 개발 경로의 가능성이 넓어지고 있어 주목을 받고 있습니다. 따라서 난소암 치료제 시장은 상피성 질환의 범위를 넘어 확대되고 있지만, 이러한 희귀 아형 시장 규모는 여전히 작으며, 검사의 심도, 의뢰 패턴, 전문 의료 센터에서의 도입 현황에 크게 좌우되고 있습니다.

2025년, PARP 억제제는 매출의 42.83%를 차지하며, 약물 유형별 난소암 치료제 시장 점유율에서 1위를 차지하고 있습니다. 이러한 강점은 일선 유지 요법에서의 확립된 사용 실적, 명확한 바이오마커와의 연관성, 그리고 선별된 환자군에서 지속적으로 입증되는 유효성을 뒷받침하는 장기 추적 데이터에 있습니다. 동반 진단 기술의 발전 또한 환자 선별 정확도를 높이고, 처방과 정식 검사 절차를 연계함으로써 이 약물 군의 효과를 강화하고 있습니다. 넓은 적응증 범위와 진단 지원이 결합되어, 내성 압력이 높아지는 상황 속에서도 PARP 억제제는 난소암 치료제 시장에서 여전히 중심적인 위치를 차지하고 있습니다. 기존의 세포독성 약제도 임상적으로는 여전히 중요하지만, 그 가치의 상당 부분이 표적 치료로 이동함에 따라 가격 결정권이나 제품 차별화의 여지는 제한적입니다.

VEGF 및 VEGFR 억제제는 2031년까지 연평균 성장률(CAGR) 11.43%를 나타낼 것으로 예측되며, 난소암 치료제 시장 규모 구성에서 각 약물군 중 가장 빠른 성장세를 보일 것으로 전망됩니다. 이러한 전망은 베바시주맙 병용 요법의 보급 확대, 가격에 민감한 지역에서의 저비용 버전 접근성 향상, 그리고 새로운 항혈관신생 병용 요법에 관한 파이프라인 활동에 힘입어 뒷받침되고 있습니다. 이 약물군은 좁은 범위의 단일 적응증이 아닌, 여러 치료 단계에 걸쳐 유용성을 발휘한다는 장점을 가지고 있습니다. ADC나 면역요법을 주축으로 하는 치료법을 포함한 기타 약물 유형도 그 세를 넓혀가고 있지만, 작용기전이나 적응증에 따라 여전히 세분화되어 있습니다. 예측 기간 동안 난소암 치료제 시장에서는 적응증이 넓고, 임상적 근거, 접근성, 독성 부담이 관리 가능한 약물군이 우위를 점할 것으로 예측됩니다.

지역별 분석

2025년, 북미는 매출의 39.41%를 차지하며 난소암 치료제 시장에서 계속해서 가장 큰 비중을 차지하는 지역이 되었습니다. 이 지역은 활발한 임상시험 활동, BRCA 및 HRD 검사의 광범위한 활용, 그리고 새로운 치료법에 대한 조기 접근을 가능하게 하는 규제 환경의 혜택을 누리고 있습니다. 미국은 여전히 많은 난소암 치료법에 있어 최초의 주요 출시 시장으로서의 역할을 수행하고 있으며, 이를 통해 조기 수익 창출과 의료진의 치료법에 대한 이해 증진이 뒷받침되고 있습니다. 이러한 입장은 향후 다른 지역에서의 도입에 영향을 미칠 치료 경로를 확립하는 과정에서 북미의 역할을 더욱 공고히 하고 있습니다.

유럽은 난소암 치료제 시장에서 여전히 2위를 차지하고 있지만, 국가별로 치료 접근 조건에는 큰 차이가 있습니다. 규제 당국 간의 조정을 통해 승인 일관성은 확보되고 있지만, 보험 급여 시기와 의료기술평가(HTA)에 따라 치료의 접근성에는 여전히 불균형이 발생하고 있습니다. 이 점은 중요합니다. 왜냐하면, 특정 치료법이 유럽 전역에서 승인되었더라도 각국의 자금 조달 결정에 따라 환자에게 전달되는 속도가 달라질 수 있기 때문입니다. 따라서 난소암 치료제 시장은 특히 강력한 가치 제안을 필요로 하는 고비용 치료법의 경우, 임상적 혁신성이 시사하는 만큼 유럽에서 급속히 확대되지는 않고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 11.26%로 확대될 것으로 예상되며, 난소암 치료제 시장 규모 전망에서 가장 빠르게 성장하는 지역 부문으로 꼽히고 있습니다. 중국은 이러한 성장에 중심적인 역할을 하고 있으며, 여러 PARP 억제제에 대한 보험 급여 지원과 분자 검사 인프라 확충을 통해 실제 접근성이 개선되고 있기 때문입니다. 또한, 국내 생산 및 바이오시밀러와의 경쟁으로 인해 항혈관신생 요법의 사용이 확대되는 한편, 일부 유통 경로에서는 실세 가격이 하락할 가능성이 있습니다. 일본과 한국은 강력한 종양 센터, 체계화된 검사 절차, 그리고 전문 의료 서비스에 대한 높은 이용률을 통해 시장의 성장세를 뒷받침하고 있습니다. 중동 및 아프리카에서도 각국 정부가 종양 의료 체계에 대한 투자를 확대함에 따라, 난소암 치료제 시장은 점차 확대되고 있습니다. 남미에서는 여전히 치료 접근성이 더 제한적이며, 경제적 부담과 정교한 바이오마커 검사의 보급이 표적 치료의 광범위한 활용을 제한하고 있기 때문에 PARP 억제제의 보급률보다 베바시주맙의 채택률이 더 높습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the ovarian cancer drugs market size is expected to grow from USD 4.73 billion in 2025 to USD 5.14 billion in 2026 and is forecast to reach USD 8.09 billion by 2031 at 9.49% CAGR over 2026-2031.

This report is Segmented by Tumor Type (Epithelial, Germ Cell, Stromal Cell), Drug Type (Alkylating Agents, Mitotic Inhibitors, VEGF/VEGFR Inhibitors, PARP Inhibitors, Other), Distribution Channel (Hospital Pharmacies, Drug Stores, Other), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Ovarian Cancer Drugs Market Trends and Insights

Rising BRCA and HRD-Guided PARP Inhibitor Use

The ovarian cancer drugs market continues to benefit from broader HRD-linked treatment eligibility in frontline and maintenance settings. FDA clearance of MyChoice CDx for niraparib in March 2026 strengthened the diagnostic basis for selecting HRD-positive patients and raised the number of patients who can be identified for PARP therapy under formal testing workflows. Long-run survival evidence has also kept PARP inhibitors central to treatment planning for BRCA-mutated disease, especially where maintenance therapy is established in routine care. At the same time, resistance research is showing that patient selection alone will not determine future uptake because treatment sequencing and prior chemotherapy exposure can influence later PARP response. That makes the ovarian cancer drugs market more dependent on how physicians combine biomarker data with line-of-therapy decisions. It also supports continued investment in diagnostic depth, sequencing strategy, and follow-up evidence for long-duration maintenance use.

Expansion of FRa-Targeted ADC Adoption in Platinum-Resistant Disease

The ovarian cancer drugs market is gaining a new growth layer from FRa-targeted antibody drug conjugates in platinum-resistant disease. Stronger survival evidence for mirvetuximab soravtansine has reinforced the role of FRa-directed treatment in a setting that previously had few differentiated options with durable benefit. This matters because platinum-resistant disease carries a high unmet need and often drives rapid adoption when a therapy shows both clinical activity and clearer patient selection. The ovarian cancer drugs market is also showing that reimbursement and health technology assessment now shape uptake as much as trial data, especially when premium-priced biologics move from approval to funded access. That raises the commercial importance of value demonstration after approval, particularly in systems where survival and quality-of-life evidence guide access. It also means developers with targeted assets need pricing flexibility, biomarker clarity, and region-specific access planning to scale volume.

Rapid Emergence of PARP Resistance and Cross-Resistance

The ovarian cancer drugs market faces a clear growth constraint from faster characterization of PARP resistance mechanisms. Recent research identified multiple resistance pathways, including homologous recombination repair restoration, replication fork stabilization, and drug efflux changes, which means resistance is now better defined and harder to ignore in treatment planning. Additional work has also shown that PARP inhibitor-resistant tumors may develop distinct biological vulnerabilities, which confirms that resistance is not a single event and cannot be managed with a uniform response. Commercially, this reduces the number of effective lines available for the same drug class and limits the duration of revenue that each patient can generate. The ovarian cancer drugs market is therefore being pushed toward next-generation assets and better-defined sequencing logic rather than repeat use of the same class after progression. That pressure also increases the value of companion biomarkers and real-world monitoring tools that can identify which patients still benefit from continued targeted treatment.

Other drivers and restraints analyzed in the detailed report include:

- Earlier-Line Use of Maintenance Combination Regimens

- Broader Molecular Testing and Companion Diagnostics Access

- High Annual Therapy Cost and Reimbursement Pressure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epithelial ovarian cancer held 63.21% of revenue in 2025 and remained the largest tumor type in the ovarian cancer drugs market. This concentration reflects the clinical weight of high-grade serous disease across induction, maintenance, and relapse treatment pathways. Epithelial tumors also carry the largest share of BRCA-mutated and HRD-positive patients, which keeps precision therapies most relevant in this segment. As a result, the ovarian cancer drugs industry continues to direct most commercial and clinical effort toward epithelial disease. This concentration also gives drug makers a clearer route to scale because testing, treatment algorithms, and evidence generation are all more mature in this setting.

Germ cell ovarian cancer is projected to grow at a 9.81% CAGR through 2031, making it the fastest-growing tumor type sub-segment in the ovarian cancer drugs market. Growth here is tied less to current volume and more to improved molecular characterization of rare subtypes that were historically treated with broader chemotherapy approaches. Targetable findings in dysgerminoma and related tumors are supporting incremental use of more precise treatments, even though chemotherapy still delivers strong responses in many patients. Stromal tumors are also drawing attention because their hormone-linked biology creates room for more specialized development paths. The ovarian cancer drugs industry is therefore widening beyond epithelial disease, but these rare subtypes remain smaller commercial opportunities that depend heavily on testing depth, referral patterns, and specialist center adoption.

PARP inhibitors held 42.83% of revenue in 2025, which gave them the leading position in the ovarian cancer drugs market share by drug type. Their strength comes from established use in first-line maintenance, clear biomarker links, and long follow-up data that continue to support benefit in selected patients. Companion diagnostic progress has also reinforced this class by improving patient identification and keeping prescribing tied to formal testing pathways. That combination of label breadth and diagnostic support keeps PARP inhibitors central to the ovarian cancer drugs market even as resistance pressures rise. Older cytotoxic classes still matter clinically, but they offer less room for pricing power or product differentiation because most value has shifted toward targeted therapy.

VEGF and VEGFR inhibitors are projected to grow at an 11.43% CAGR through 2031, giving them the fastest expansion profile among drug classes in the ovarian cancer drugs market size mix. Their outlook is supported by broader use of bevacizumab combinations, rising access to lower-cost versions in price-sensitive regions, and pipeline activity around new antiangiogenic combinations. This class benefits from relevance across multiple treatment stages rather than a narrow single indication. Other drug types, including ADCs and immunotherapy-led regimens, are also adding momentum, but they remain more fragmented by mechanism and patient selection. Over the forecast period, the ovarian cancer drugs market is likely to reward drug classes that combine broader eligibility with manageable evidence, access, and toxicity burdens.

Complete Report Scope:

- By Tumor Type

- Epithelial Ovarian Cancer

- Serous Carcinoma

- Endometrioid Carcinoma

- Clear Cell Carcinoma

- Mucinous Carcinoma

- Germ Cell Ovarian Cancer

- Dysgerminoma

- Yolk Sac Tumor

- Teratoma

- Embryonal Carcinoma

- Stromal Cell Ovarian Cancer

- Granulosa Cell Tumor

- Sertoli-Leydig Cell Tumor

- Thecoma

- Fibroma

- Epithelial Ovarian Cancer

- By Drug Type

- Alkylating Agents

- Mitotic Inhibitors

- VEGF and VEGFR Inhibitors

- PARP Inhibitors

- Other Drug Types

- By Distribution Channel

- Hospital Pharmacies

- Drug Stores

- Other Distribution Channels

- By End User

- Hospitals

- Oncology Clinics

- Specialty Cancer Centers

- Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 39.41% of revenue in 2025 and remained the largest regional contributor to the ovarian cancer drugs market. The region benefits from dense clinical trial activity, wider use of BRCA and HRD testing, and a regulatory environment that often delivers earlier access to new therapies. The United States continues to act as the first major launch market for many ovarian therapies, which supports earlier revenue capture and stronger physician familiarity. This position also reinforces North America's role in setting treatment pathways that later influence adoption elsewhere.

Europe remained the second-largest regional block in the ovarian cancer drugs market, but access conditions vary sharply across countries. Regulatory coordination helps align approvals, yet reimbursement timing and health technology review still create uneven treatment availability. That matters because a therapy may be approved across Europe but still reach patients at different speeds depending on local funding decisions. The ovarian cancer drugs market therefore expands more slowly in Europe than its clinical innovation would suggest, especially for high-cost therapies that need stronger value arguments.

Asia-Pacific is projected to expand at an 11.26% CAGR through 2031 and is the fastest-growing regional segment in the ovarian cancer drugs market size outlook. China is central to that growth because reimbursement support for multiple PARP inhibitors and broader molecular testing infrastructure are improving practical access. Domestic manufacturing and biosimilar competition are also likely to expand the use of antiangiogenic therapy while lowering realized pricing in some channels. Japan and South Korea add momentum through strong oncology centers, structured testing pathways, and high participation in specialist care. The ovarian cancer drugs market is also broadening gradually in the Middle East and Africa as governments invest in oncology capacity. South America remains more selective in access, with stronger bevacizumab uptake than PARP penetration because affordability and advanced biomarker testing still limit broader targeted therapy use.

- Abbvie

- Amgen

- AstraZeneca

- BeiGene, Ltd.

- Bristol-Myers Squibb

- Clovis Oncology, Inc.

- Daiichi Sankyo

- Eisai

- Eli Lilly and Company

- Roche

- Genmab

- GlaxoSmithKline

- Innovent Biologics, Inc.

- Jiangsu Hengrui Medicine Co., Ltd.

- Johnson & Johnson

- Merck

- Novartis

- Pfizer

- Pharma Mar, S.A.

- Verastem, Inc.

- Zai Lab Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising BRCA and HRD-Guided PARP Inhibitor Use

- 4.2.2 Expansion of FRa-Targeted ADC Adoption in Platinum-Resistant Disease

- 4.2.3 Earlier-Line Use of Maintenance Combination Regimens

- 4.2.4 Broader Molecular Testing and Companion Diagnostics Access

- 4.2.5 Pipeline Readouts in KRAS-Mutant, CCNE1-Amplified, and Rare Subtypes

- 4.2.6 Real-World Evidence Support for Sequencing After First PARP Exposure

- 4.3 Market Restraints

- 4.3.1 Rapid Emergence of PARP Resistance and Cross-Resistance

- 4.3.2 High Annual Therapy Cost and Reimbursement Pressure

- 4.3.3 Biomarker Fragmentation Shrinking Eligible Patient Pools

- 4.3.4 Hematologic and Ocular Toxicity Limiting Long-Term Use

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Tumor Type

- 5.1.1 Epithelial Ovarian Cancer

- 5.1.1.1 Serous Carcinoma

- 5.1.1.2 Endometrioid Carcinoma

- 5.1.1.3 Clear Cell Carcinoma

- 5.1.1.4 Mucinous Carcinoma

- 5.1.2 Germ Cell Ovarian Cancer

- 5.1.2.1 Dysgerminoma

- 5.1.2.2 Yolk Sac Tumor

- 5.1.2.3 Teratoma

- 5.1.2.4 Embryonal Carcinoma

- 5.1.3 Stromal Cell Ovarian Cancer

- 5.1.3.1 Granulosa Cell Tumor

- 5.1.3.2 Sertoli-Leydig Cell Tumor

- 5.1.3.3 Thecoma

- 5.1.3.4 Fibroma

- 5.1.1 Epithelial Ovarian Cancer

- 5.2 By Drug Type

- 5.2.1 Alkylating Agents

- 5.2.2 Mitotic Inhibitors

- 5.2.3 VEGF and VEGFR Inhibitors

- 5.2.4 PARP Inhibitors

- 5.2.5 Other Drug Types

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Drug Stores

- 5.3.3 Other Distribution Channels

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Oncology Clinics

- 5.4.3 Specialty Cancer Centers

- 5.4.4 Research Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Amgen Inc.

- 6.3.3 AstraZeneca plc

- 6.3.4 BeiGene, Ltd.

- 6.3.5 Bristol-Myers Squibb Company

- 6.3.6 Clovis Oncology, Inc.

- 6.3.7 Daiichi Sankyo Company, Limited

- 6.3.8 Eisai Co., Ltd.

- 6.3.9 Eli Lilly and Company

- 6.3.10 F. Hoffmann-La Roche Ltd.

- 6.3.11 Genmab A/S

- 6.3.12 GSK plc

- 6.3.13 Innovent Biologics, Inc.

- 6.3.14 Jiangsu Hengrui Medicine Co., Ltd.

- 6.3.15 Johnson and Johnson

- 6.3.16 Merck & Co., Inc.

- 6.3.17 Novartis AG

- 6.3.18 Pfizer Inc.

- 6.3.19 Pharma Mar, S.A.

- 6.3.20 Verastem, Inc.

- 6.3.21 Zai Lab Limited

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment