|

시장보고서

상품코드

2073039

혈액 투석 카테터 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Hemodialysis Catheters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

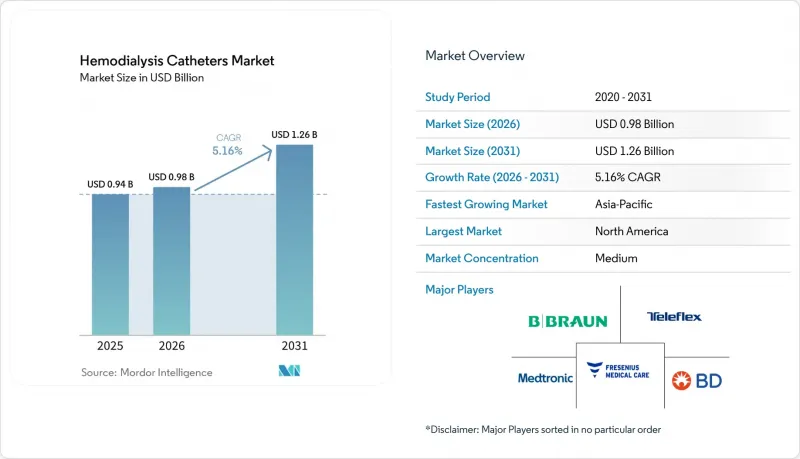

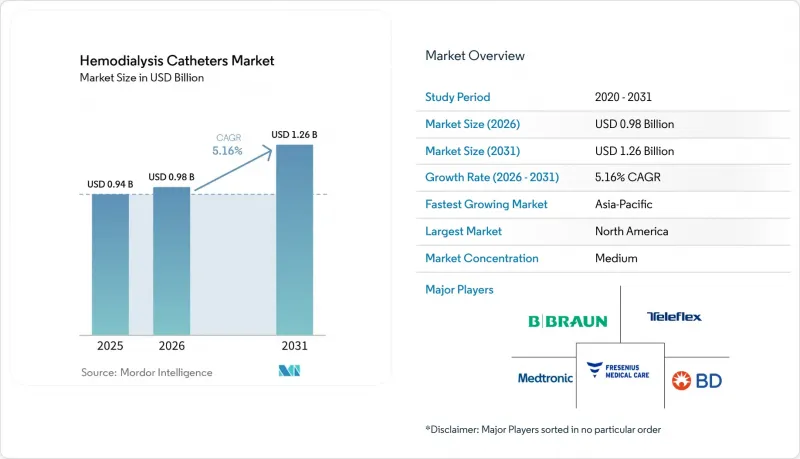

Mordor Intelligence에 의하면, 혈액 투석 카테터 시장 규모는 2025년 9억 4,000만 달러에서 2026년에는 9억 8,000만 달러로 확대되어 2026-2031년까지 CAGR 5.16%로 성장을 지속하여, 2031년에는 12억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(터널형, 비터널형, 기타), 소재(폴리우레탄, 실리콘, 기타), 팁 형태(스텝 팁, 스플릿 팁, 기타), 용도(만성 혈액 투석, 기타), 최종 사용자(병원, 투석 센터, 기타), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 혈액 투석 카테터 시장 동향 및 분석

만성 신장 질환(CKD)과 말기 신부전의 부담 증가가 수요를 구조적으로 뒷받침하고 있습니다.

세계적으로 만성 신장 질환(CKD)의 유병률이 증가함에 따라 혈액 투석 카테터 시장 수요가 증가하고 있습니다. 2025년에는 전 세계적으로 7억 8,800만 명의 성인이 만성 신장 질환(CKD)을 앓고 있는 것으로 보고되어, 의료 시스템 계획에서 이 질환의 중요성이 점점 더 커지고 있음이 부각되고 있습니다. 이 질환의 유병률은 높지만, 치료 접근성이 제한된 지역에서는 여러 문제에 직면하고 있으며, 그 결과 환자의 진료가 지연되거나 계획적인 누공 수술 대신 응급 카테터 삽입에 의존할 수밖에 없는 상황이 발생하고 있습니다. 미국에서는 최신 USRDS(미국 신장 데이터 시스템) 업데이트 데이터를 통해, 주로 당뇨병과 고혈압으로 인한 말기 신장 질환(ESRD)의 신규 환자 수와 유병자 수가 계속해서 증가하고 있는 것으로 나타났습니다. 현재 치료 대상자 중 고령 환자의 비율이 증가하고 있으며, 허약이나 동반 질환으로 인해 기존 접근법의 신뢰성이 떨어지고 있습니다. 이로 인해 장기간에 걸친 터널형 카테터의 사용이 증가하고 있으며, 이는 시장 성장을 뒷받침하고 있습니다.

급성기 의료 현장에서는 카테터를 이용한 혈액 투석의 시작이 여전히 임상적 표준으로 자리 잡고 있습니다.

지침에서는 사전 계획을 통한 지속적인 접근을 권장하고 있음에도 불구하고, 많은 환자들이 응급 상황에서 혈액 투석을 시작하고 있으며, 이것이 혈액 투석 카테터에 대한 수요를 뒷받침하고 있습니다. 급성 신장 손상이나 예기치 못한 말기 신부전(ESRD)의 발병으로 인해, 병원 및 응급실에서는 비터널형 중심정맥 카테터가 가장 실용적인 선택지로 자리 잡고 있습니다. CMS의 2025년 ESRD 지급 기준 개정에 따라, 급성 신장 손상과 관련된 재택 투석에 대한 메디케어 적용 범위가 확대되어 카테터 삽입 치료 환경이 넓어졌습니다. 인도에서는 2025년과 2026년에 투석 수용 능력이 대폭 확대되어, 텔랑가나 주의 공립병원에 79곳의 새로운 투석 센터가 개설되었으며, 2025년 12월까지 PMNDP(총리 투석 개발 계획)에 따라 4.12 라크하 세션을 통해 6,425명 이상의 환자에게 투석 서비스가 제공되었습니다. 신흥 시장에서는 누공 형성 수술 능력이 제한적이기 때문에 응급용 카테터의 사용 기간이 길어지는 경우가 많아, 투석 네트워크의 확장과 더불어 시장 성장을 견인하고 있습니다.

CRBSI와 혈전증이 초래하는 임상적, 규제적, 상업적 비용

카테터 관련 혈류 감염(CRBSI)과 혈전증은 환자의 안전에 영향을 미치고, 병원 비용을 증가시키며, 조달 결정에도 영향을 줌으로써 혈액 투석 카테터 시장에 중대한 과제를 안겨주고 있습니다. 2025년에 실시된 연구에 따르면, 중탄산나트륨 락이 구연산 겐타마이신 락과 동등한 감염 제로 카테터 생존율을 달성했으며, 헤파린 락보다 우수한 결과를 보인 것으로 밝혀졌습니다. 혈전증은 생물막 형성을 촉진하고, 혈류를 저하시켜, 의료기기의 폐기 위험을 높임으로써 이러한 문제들을 더욱 심각하게 만듭니다. 현재 병원 측은 엄격한 카테터 관리, 관찰, 무균 조작을 강조하는 CDC(미국 질병통제예방센터)의 투석 안전 지침에 힘입어, 프리미엄 제품에 대해 측정 가능한 성능 지표를 요구하고 있습니다. 이러한 엄격한 모니터링으로 인해, 가격과 시장 점유율을 지켜야 하는 제조업체들에게 경쟁의 장벽은 더욱 높아지고 있습니다.

부문별 분석

2025년, 터널형 카테터는 혈액 투석 카테터 시장에서 39.81%의 점유율을 차지하며 주요 제품 유형으로서의 입지를 유지했습니다. 이러한 장점은 인공 투석 경로 형성에 어려움이 있는 만성 환자, 접근 부위가 성숙되기를 기다리는 환자, 혹은 외과적 접근이 적합하지 않은 환자들 사이에서 널리 사용되고 있다는 점에 기인합니다. 임상의들은 비터널형 기기로는 얻을 수 없는 안정적인 혈류와 장기간의 삽입 기간을 이유로 터널형 시스템을 선호하여 사용하고 있습니다. 이 카테고리 내에서는 수요 변화를 반영하여, 커프가 부착된 디자인의 제품이 2031년까지 연평균 성장률(CAGR) 6.90%를 나타낼 것으로 예측됩니다.

커프가 부착된 설계는 탈락 위험을 줄여주고, 커프 주변 조직의 침입으로 인한 세균 이동을 막아주는 장벽을 형성할 수 있다는 점에서 주목을 받고 있습니다. Mozarc Medical의 “Palindrome Precision” 시리즈와, Teleflex의 항균 기술이 적용된 “Arrow ErgoPack”시스템 등의 제품은 기능이 풍부한 제품으로의 전환이 진행되고 있는 이 부문의 진화를 상징하고 있습니다. 비터널형 카테터는 삽입 속도가 매우 중요한 응급실이나 중환자실 현장에서 여전히 필수적입니다. 투석 환자의 고령화로 인해 터널형 커프가 장착된 기기의 중요성은 더욱 커지고 있습니다. 많은 고령 환자들이 예상보다 오랫동안 카테터에 의존하기 때문에 응급 사용의 필요성과 만성기 치료의 가치 간에 균형이 잡혀 있기 때문입니다.

2025년, 폴리우레탄은 혈액 투석 카테터 시장의 46.35%를 차지하며 주요 소재로 자리매김했습니다. 그 기계적 강도, X선 불투과성, 멸균 및 코팅 공정과의 적합성 덕분에 급성기 및 만성기 모두의 카테터 형태에 적합합니다. 폴리우레탄의 선도적 지위는 주요 공급업체들이 자사의 표준 제품군에 이를 채택한 데에도 기인합니다. 한편, 실리콘은 2031년까지 연평균 성장률(CAGR) 7.25%를 기록하며 성장할 것으로 예상되며, 가장 빠르게 성장하는 소재 부문이 될 전망입니다.

소재 간경쟁 구도는 변화하고 있으며, 향후 발전 방향은 폴리우레탄이나 실리콘을 대체하는 것이 아니라 개질 폴리머 화학에 초점이 맞추어질 가능성이 높습니다. 단기적으로는 폴리우레탄이 주도적인 위치를 유지할 것으로 예상되는 반면, 실리콘은 장기 삽입 시의 쾌적성과 생체 적합성을 중시하는 용도에서 그 입지가 확대될 것으로 전망됩니다. 두 재료 모두 각자의 임상적 요구 사항에 있어 앞으로도 중요한 역할을 할 것으로 예측됩니다.

지역별 분석

2025년, 북미는 혈액 투석 카테터 시장에서 42.55%의 점유율을 차지하며 지역별 최대 시장으로서의 위상을 유지했습니다. 미국은 투석 환자 수가 많고, 고도의 카테터 삽입 기술을 보유하고 있으며, 만성기 치료에서 터널형 카테터를 광범위하게 사용함으로써 이러한 우위를 이끌어 냈습니다. CMS의 2025 회계연도(CY 2025) ESRD 지급 기준 개정에서는 급성 신장 손상(AKI) 환자의 재택 투석에 대한 지급 기준이 균등화되었으며, 타우롤리딘 헤파린 락 용액에 대한 새로운 HCPCS 코드가 도입되어 카테터 관리 환경이 강화되었습니다. MedPAC은 2026 회계연도 투석 서비스에 대한 메디케어 기본 지급률을 1.7% 인상할 것으로 전망하고 있으며, 이는 해당 시설에 긍정적인 경제적 전망을 시사합니다. 캐나다에서는 이식 제한으로 인해 다수의 만성 혈액 투석 환자들이 장기 치료를 계속할 수밖에 없었기 때문에 수요가 유지되었습니다.

유럽은 고령화와 만성 신장 질환(CKD)으로 인한 막대한 부담을 배경으로, 2025년에도 혈액 투석 카테터 시장에서 주요한 역할을 계속 수행했습니다. 2025년 1월 기준으로 EU 인구의 21.6%가 65세 이상이며, 이것이 신장 대체 요법에 대한 안정적인 수요를 뒷받침하고 있습니다. CKD에 관한 분석에 따르면, 동유럽과 중부 유럽의 유병률 중앙값은 12.8%로 보고되어, 이 지역이 안고 있는 신장 질환 문제가 부각되고 있습니다. 독일, 영국, 프랑스가 시장을 주도했으나, 상환 제도와 조달 방침의 차이로 인해 프리미엄 코팅 카테터의 도입 현황에는 편차가 나타났습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 6.26%를 나타낼 것으로 예측되며, 혈액 투석 카테터 시장에서 가장 높은 성장세를 보일 것으로 전망됩니다. 중국과 인도는 충족되지 않은 신장 치료 수요에 대응하기 위해 투석 능력을 확대함으로써 이러한 성장을 주도하고 있습니다. 2025년, 중국의 투석 환자 수는 134만 명에 달했으며, 국내 제조업체들이 현지 공급에서 차지하는 역할을 확대함으로써 공급량 증가를 뒷받침하고 수입 의존도를 낮추고 있습니다. 인도의 “플라단 만트리 국가 투석 프로그램”는 2025년까지 1,200곳 이상의 지역 병원 센터를 설치함으로써 치료 접근성을 향상시키고, 신뢰할 수 있는 카테터 조달에 대한 수요를 높였습니다. 일본은 여전히 임상적으로 수준이 높으며, 엄격한 기준을 유지하고 있습니다. 한편, 남미, 중동 및 아프리카에서는 공적 신장 의료 프로그램과 엄선된 민간 네트워크의 확대를 통해 시장이 성장하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the hemodialysis catheters market size is expected to grow from USD 0.94 billion in 2025 to USD 0.98 billion in 2026 and is forecast to reach USD 1.26 billion by 2031 at 5.16% CAGR over 2026-2031.

This report is Segmented by Product Type (Tunneled, Non-Tunneled, and More), Material (Polyurethane, Silicone, and More), Tip Configuration (Step-Tip, Split-Tip, and More), Application (Chronic Hemodialysis, and More), End User (Hospitals, Dialysis Centers, and More), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Hemodialysis Catheters Market Trends and Insights

Rising CKD and End-Stage Renal Disease Burden Structurally Anchors Demand

The hemodialysis catheters market is experiencing increased demand due to the rising global prevalence of chronic kidney disease (CKD). In 2025, 788 million adults worldwide were reported to have CKD, highlighting its growing importance in health system planning. Regions with high disease prevalence but limited treatment access face challenges, leading to late patient arrivals and reliance on emergency catheter placements instead of planned fistula surgeries. In the U.S., the latest USRDS update showed a continued rise in both incident and prevalent end-stage renal disease (ESRD) cases, primarily driven by diabetes and hypertension. Older patients now represent a larger share of the treatment pool, with frailty and comorbidities making traditional access methods less reliable. This has led to increased use of tunneled catheters for extended periods, supporting market growth.

Catheter-Based Hemodialysis Initiation Remains the Clinical Default in Acute Settings

Despite guidelines favoring preplanned permanent access, many patients begin hemodialysis in urgent settings, sustaining demand for hemodialysis catheters. Acute kidney injury and unplanned ESRD presentations make non-tunneled central venous catheters the most practical option in hospitals and emergency units. The CMS 2025 ESRD payment update expanded Medicare coverage for home dialysis related to acute kidney injury, broadening treatment settings for catheter placement. In India, dialysis capacity expanded significantly in 2025 and 2026, with 79 new dialysis centers in Telangana government hospitals and over 6,425 patients served through 4.12 lakh sessions under the PMNDP by December 2025. In emerging markets, limited surgical capacity for fistula creation often results in prolonged use of emergency catheters, driving market growth alongside dialysis network expansion.

CRBSI and Thrombosis Impose Clinical, Regulatory, and Commercial Costs

Catheter-related bloodstream infections (CRBSI) and thrombosis significantly challenge the hemodialysis catheters market by impacting patient safety, increasing hospital costs, and influencing procurement decisions. A 2025 study highlighted that sodium bicarbonate locks achieved infection-free catheter survival rates comparable to gentamicin citrate locks and better than heparin locks. Thrombosis exacerbates these issues by promoting biofilm development, reducing flow, and increasing device abandonment risks. Hospitals now demand measurable performance metrics for premium products, driven by CDC dialysis safety guidance emphasizing strict catheter care, observation, and aseptic practices. This scrutiny raises the competitive bar for manufacturers defending price and market share.

Other drivers and restraints analyzed in the detailed report include:

- Antimicrobial and Biocompatible Catheter Engineering Becomes a Differentiator

- Home Hemodialysis Growth Reshapes Catheter Design Requirements

- Arteriovenous Fistula Prioritization Redirects, but Does Not Eliminate, Catheter Use

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, tunneled catheters held a 39.81% share of the hemodialysis catheters market, maintaining their position as the leading product type. Their dominance is driven by their widespread use among chronic patients who face challenges with fistula creation, are awaiting access maturation, or are unsuitable for surgical access. Clinicians prefer tunneled systems for their stable flow and extended dwell period, which non-tunneled devices cannot provide. Within this category, cuffed designs are projected to grow at a 6.90% CAGR through 2031, reflecting a shift in demand.

Cuffed designs are gaining traction due to their ability to reduce dislodgement risks and create a barrier against bacterial migration through tissue ingrowth around the cuff. Products like Mozarc Medical's Palindrome Precision line and Teleflex's Arrow ErgoPack systems with antimicrobial technology highlight the segment's evolution toward feature-rich offerings. Non-tunneled catheters remain essential in emergency and ICU settings, where placement speed is critical. The aging dialysis population further drives the relevance of tunneled cuffed devices, as many elderly patients remain catheter-dependent longer than anticipated, balancing urgent-use volume with chronic-care value.

In 2025, polyurethane accounted for 46.35% of the hemodialysis catheters market, making it the leading material. Its mechanical strength, radiopacity, and compatibility with sterilization and coating processes make it suitable for both acute and chronic catheter formats. Polyurethane's leadership is also linked to its adoption in standard product families from major suppliers. Silicone, however, is projected to grow at a 7.25% CAGR through 2031, making it the faster-growing material category.

Material competition is evolving, with future advancements likely to focus on modified polymer chemistry rather than replacing polyurethane or silicone. Polyurethane is expected to maintain its leadership in the short term, while silicone gains traction in applications prioritizing long-dwell comfort and biocompatibility. Both materials are expected to remain relevant for distinct clinical needs.

Complete Report Scope:

- By Product Type

- Tunneled Hemodialysis Catheters

- Cuffed Tunneled Catheters

- Non-Cuffed Tunneled Catheters

- Non-Tunneled Hemodialysis Catheters

- Single Lumen Non-Tunneled Catheters

- Double Lumen Non-Tunneled Catheters

- Triple Lumen Non-Tunneled Catheters

- By Material

- Polyurethane

- Silicone

- Composite and Other Polymer Materials

- By Tip Configuration

- Step-Tip Catheters

- Split-Tip Catheters

- Symmetric Catheters

- Pre-Curved Catheters

- By Application

- Chronic Hemodialysis

- Acute Hemodialysis

- Home Hemodialysis

- By End User

- Hospitals

- Dialysis Centers

- Ambulatory Surgical Centers

- Home Care Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America held a 42.55% share of the hemodialysis catheters market, maintaining its position as the largest regional player. The United States led this dominance due to its extensive dialysis patient base, advanced insertion capabilities, and widespread use of tunneled catheters in chronic care. The CMS CY 2025 ESRD payment update, which introduced AKI home dialysis payment parity and a new HCPCS code for taurolidine heparin locking solutions, strengthened the catheter care environment. MedPAC projected a 1.7% increase in the 2026 Medicare base payment rate for dialysis services, signaling a positive economic outlook for facilities. In Canada, transplant limitations sustained demand by keeping a significant chronic hemodialysis population in long-term treatment.

Europe remained a key player in the hemodialysis catheters market in 2025, driven by an aging population and a significant CKD burden. As of January 2025, 21.6% of the EU population was aged 65 or older, supporting consistent demand for renal replacement therapies. A CKD analysis reported a median prevalence of 12.8% in Eastern and Central Europe, highlighting the region's renal disease challenges. Germany, the UK, and France led the market, though the adoption of premium-coated catheters varied due to differing reimbursement and procurement policies.

Asia-Pacific is projected to grow at a 6.26% CAGR through 2031, making it the fastest-growing regional segment in the hemodialysis catheters market. China and India are driving this growth by expanding dialysis capacity to address unmet renal care needs. In 2025, China's dialysis population reached 1.34 million, with domestic producers increasing their role in local supply, supporting volume growth and reducing import dependency. India's Pradhan Mantri National Dialysis Programme, with over 1,200 district hospital centers by 2025, enhanced treatment access and increased demand for reliable catheter procurement. Japan remains clinically advanced with stringent standards, while South America and the Middle East and Africa are expanding through public renal care programs and selective private network growth.

- Amecath Medical Technologies

- AngioDynamics

- Asahi Kasei

- B. Braun

- Baxter

- Beckton Dickinson

- Cook Group

- Fresenius Medical Care AG and Co. KGaA

- JMS Co., Ltd.

- Joline GmbH and Co. KG

- Medical Components, Inc.

- Medtronic

- Merit Medical Systems

- Mozarc Medical Holding LLC

- Nikkiso Co., Ltd.

- Nipro

- Poly Medicure Ltd.

- Teleflex

- Toray Medical Co., Ltd.

- Vygon

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Chronic Kidney Disease and End-Stage Renal Disease Burden

- 4.2.2 Growing Reliance on Catheter-Based Initiation of Hemodialysis

- 4.2.3 Expansion of Dialysis Capacity in Emerging Markets

- 4.2.4 Rising Demand for Antimicrobial and Biocompatible Catheters

- 4.2.5 Increased Home Hemodialysis Adoption and Portable Access Needs

- 4.2.6 Greater Use of Catheter Kits and Procedure-Efficiency Solutions

- 4.3 Market Restraints

- 4.3.1 Catheter-Related Bloodstream Infections and Thrombosis Risk

- 4.3.2 Shift Toward Arteriovenous Fistula First Pathways

- 4.3.3 Shortage of Skilled Vascular Access Operators

- 4.3.4 Hospital Budget Pressure and Reimbursement Sensitivity

- 4.4 Value/Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Product Type

- 5.1.1 Tunneled Hemodialysis Catheters

- 5.1.2 Cuffed Tunneled Catheters

- 5.1.3 Non-Cuffed Tunneled Catheters

- 5.1.4 Non-Tunneled Hemodialysis Catheters

- 5.1.5 Single Lumen Non-Tunneled Catheters

- 5.1.6 Double Lumen Non-Tunneled Catheters

- 5.1.7 Triple Lumen Non-Tunneled Catheters

- 5.2 By Material

- 5.2.1 Polyurethane

- 5.2.2 Silicone

- 5.2.3 Composite and Other Polymer Materials

- 5.3 By Tip Configuration

- 5.3.1 Step-Tip Catheters

- 5.3.2 Split-Tip Catheters

- 5.3.3 Symmetric Catheters

- 5.3.4 Pre-Curved Catheters

- 5.4 By Application

- 5.4.1 Chronic Hemodialysis

- 5.4.2 Acute Hemodialysis

- 5.4.3 Home Hemodialysis

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Dialysis Centers

- 5.5.3 Ambulatory Surgical Centers

- 5.5.4 Home Care Settings

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Amecath Medical Technologies

- 6.3.2 AngioDynamics, Inc.

- 6.3.3 Asahi Kasei Medical Co., Ltd.

- 6.3.4 B. Braun SE

- 6.3.5 Baxter International Inc.

- 6.3.6 Becton, Dickinson and Company

- 6.3.7 Cook Medical, Inc.

- 6.3.8 Fresenius Medical Care AG and Co. KGaA

- 6.3.9 JMS Co., Ltd.

- 6.3.10 Joline GmbH and Co. KG

- 6.3.11 Medical Components, Inc.

- 6.3.12 Medtronic plc

- 6.3.13 Merit Medical Systems, Inc.

- 6.3.14 Mozarc Medical Holding LLC

- 6.3.15 Nikkiso Co., Ltd.

- 6.3.16 Nipro Corporation

- 6.3.17 Poly Medicure Ltd.

- 6.3.18 Teleflex Incorporated

- 6.3.19 Toray Medical Co., Ltd.

- 6.3.20 Vygon SA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment