|

시장보고서

상품코드

2073042

올리고뉴클레오티드 CDMO 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Oligonucleotide CDMO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

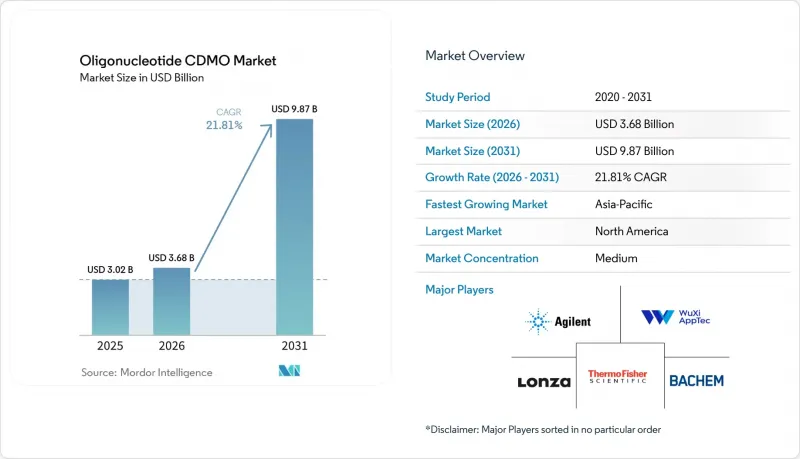

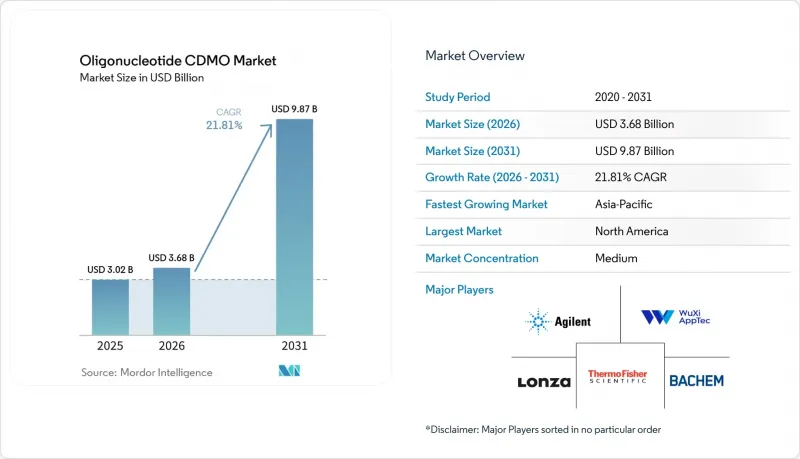

Mordor Intelligence에 의하면, 올리고뉴클레오티드 CDMO 시장 규모는 2025년에 30억 2,000만 달러로 평가되었고 2026년 36억 8,000만 달러에서 2031년까지 98억 7,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 21.81%를 나타낼 전망입니다.

본 보고서는 서비스 유형(수탁 제조, 위탁 개발, 품질 관리, 규제 대응 지원), 올리고뉴클레오티드 유형(ASO, siRNA, GRNA, 앰프타머, 기타), 용도(치료, 연구, 진단, 기타), 최종 사용자(제약, 생명공학, 진단, 학술 기관, 유전자 치료, 기타), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

세계 올리고뉴클레오티드 CDMO 시장 동향 및 인사이트

RNA를 표적으로 하는 의약품의 임상 파이프라인 확대

2026년 중반까지 200개가 넘는 기관이 전 세계 올리고뉴클레오티드 임상 파이프라인에 기여하고 있으며, 이는 올리고뉴클레오티드 CDMO 시장에 폭넓은 고객 기반을 제공합니다. IND 단계 및 후기 임상시험 단계에 있는 모든 프로그램은 승인 및 상용화에 앞서 GMP 기준을 준수하는 원료를 필요로 합니다. 파이프라인은 더 광범위한 심혈관 및 대사 질환 분야의 기회로 전환되고 있으며, 배치 규모가 증가함에 따라 상업적 공급 계획에 대한 압박이 커지고 있습니다. 기존의 합성 설비는 만성 질환 치료제를 위한 Kg에서 톤 단위 수요에 대응하도록 설계되지 않았기 때문에 의뢰사는 상당한 기간 전부터 생산 능력을 확보해야 하며, 그 결과 전 세계 GMP 슬롯의 여유 상황이 매우 촉박해지고 있습니다. 현재 파이프라인의 품질, 시기, 양은 과학적 준비 상황과 더불어 상업 계약을 형성하는 중요한 요소가 되고 있습니다.

복잡한 올리고뉴클레오티드 합성 및 충전·마감 공정의 아웃소싱 전환

복잡한 올리고뉴클레오티드 합성을 사내에서 관리할 때 발생하는 과제가 아웃소싱 추세를 부추기고 있습니다. GalNAc 결합 siRNA의 제조에는 여러 단계에 걸친 정밀한 제어가 필요하며, 각 단계마다 기술적 복잡성이 증가하고 있습니다. 2025년 상반기까지 WuXi AppTec의 TIDES 플랫폼은 API 및 의약품 제형 서비스 분야에서 69종의 분자를 지원하게 되었으며, 이 수치는 2년 전과 비교해 2배 이상 증가했습니다. 제품이 피하 투여나 프리필드 형태로 전환됨에 따라, 충전 및 마무리 공정의 중요성이 점점 더 커지고 있으며, API 합성 이상의 무균 제조 능력이 요구되고 있습니다. Asymchem사의 TJ4 시설은 2026년에 연간 4,500만 개의 프리필드 주사기를 생산할 예정이며, 이는 API에서 의약품 제제에 이르는 통합 솔루션으로 시장 전환을 여실히 보여주며, 소규모 공급업체들 시장 진입 장벽을 높이고 있습니다.

장쇄 올리고뉴클레오티드 공정에서 나타나는 높은 복잡성과 수율에 대한 민감성

올리고뉴클레오티드 CDMO 시장은 한 번에 하나의 뉴클레오티드를 추가하는 단계적 합성 공정으로 인해 중대한 기술적 과제에 직면해 있습니다. 예를 들어, 20-mer ASO는 최소 20회의 커플링 주기를 거치는데, 각 단계에서 약간의 효율 저하가 발생하기만 해도 전체 수율이 현저히 떨어질 가능성이 있습니다. 이러한 복잡성은 포스포티오에이트 골격, 2'-플루오로 치환기 또는 GalNAc 리간드와 같은 수정이 가해지면 더욱 커져, 부반응이나 분석상의 어려움을 초래합니다. 펩타이드나 저분자 분야에서 시장에 진입하는 공급업체들은 전환에 소요되는 기간, 불순물 관리, 배치 실패의 위험을 과소평가하는 경향이 있으며, 그 결과 수요가 활발함에도 불구하고 생산 능력 확대가 지연되고 맙니다. 이것이 바로 상업적 공급이 확실한 실적을 보유한 경험 많은 기업에 계속 집중되고 있는 이유입니다.

부문별 분석

2025년, 수탁 제조(Contract Manufacturing)는 올리고뉴클레오티드 CDMO 시장 점유율의 51.68%를 차지하고 있으며, 이는 승인된 제품 및 후기 임상 프로그램에서 업계가 GMP 생산에 의존하고 있음을 반영합니다. 스폰서가 2상, 3상 및 시판 준비 단계로 나아감에 따라, 시장에서는 탐색적인 지원보다 확실한 생산 규모가 우선시되고 있습니다. 부벤도르프에 위치한 바켐사의 K동에서는 2026년에 GMP 기준에 부합하는 상업 생산이 시작되어, 유럽 네트워크에 Kg 규모공급 능력이 추가되었습니다. ST 파마가 연간 14몰을 목표로 1억 2,600만 달러를 투자해 실시한 생산 능력 확충은 핵심적인 차별화 요인으로서 상업적 제조의 중요성이 높아지고 있음을 여실히 보여주고 있습니다. 매출액은 상장 계획에 부합하는 충분한 규모로 일관된 GMP 품질의 생산이 가능한 기업에 의해 지속적으로 뒷받침되고 있습니다.

수탁 개발(Contract Development)은 올리고뉴클레오티드 CDMO 시장에서 가장 빠르게 성장하고 있는 부문으로, 2031년까지 연평균 성장률(CAGR)이 22.90%를 나타낼 것으로 전망됩니다. 후원 기업들은 특히 백본이 수정된 프로그램이나 신흥 화학 기술을 활용한 프로그램의 경우, 초기 개발 단계에서 상용화 준비 단계로 원활하게 전환되는 공정 설계를 점점 더 요구하고 있습니다. 불순물 관리, 공정 이관 및 분석에 관한 요건에 대해서는 현재 주요 임상시험의 상당히 초기 단계부터 주의를 기울여야 할 필요가 있습니다. 분석 및 품질 관리 서비스는 매출 규모는 작지만, 출시 전략이 제조 가능성이나 규제 일정에 영향을 미치기 때문에 개발에 있어 필수적인 요소로 자리 잡고 있습니다. 또한, 스폰서들이 공정 작업이나 품질 패키지를 효율화하기 위해 단일 파트너를 선호하는 경향이 있기 때문에 규제 및 CMC 지원 서비스도 주목을 받고 있습니다.

2025년에는 중추신경계, 간, 심장 대사계 적응증에 대한 수요에 힘입어, 안티센스 올리고뉴클레오티드(ASO)가 올리고뉴클레오티드 CDMO 시장의 58.23%를 차지했습니다. 아이오니스사는 2026년 기준으로 12건의 신경계 질환 후보 약물 파이프라인을 유지하고 있으며, 이는 ASO와 관련된 아웃소싱 수요가 강하다는 점을 뒷받침하고 있습니다. 확립된 화학 기술 덕분에 공정은 간소화되었지만, 기술 이전, 스케일업, 검증에는 여전히 경험이 풍부한 CDMO가 필요하며, 새로운 치료 방식에 대한 관심이 높아지고 있음에도 불구하고 ASO는 여전히 최대의 수익원입니다.

소간섭 RNA(siRNA)는 2031년까지 연평균 성장률(CAGR)이 23.25%를 나타낼 것으로 예측되는 가장 빠르게 성장하고 있는 올리고뉴클레오티드 중 하나입니다. 이러한 성장은 상업적 포트폴리오의 확대와 후기 임상 단계 파이프라인의 진전에 힘입어 이루어지고 있습니다. 알니람사의 상업적 전개와 애로우헤드사의 심장 대사 질환에 대한 3상 임상시험의 진전이 siRNA를 중심으로 한 제조 수요를 견인하고 있습니다. 가이드 RNA나 앰프타머는 규모는 작지만, 유전자 편집 기술의 발전에 따라 그 중요성이 커지고 있습니다. PMO나 스플라이스 스위칭 방식 등 기타 올리고뉴클레오티드 유형은 여전히 틈새 분야에 머물러 있지만, 전문 공급업체에게는 상업적으로 성사 가능한 시장이 되고 있습니다. ASO가 여전히 수익의 대부분을 차지하고 있지만, 시장은 점차 다양화되고 있습니다.

지역별 분석

2025년, 북미는 올리고뉴클레오티드 CDMO 시장의 39.55% 점유율을 차지했습니다. 이는 미국 및 캐나다에 RNA를 표적으로 하는 의약품 개발 기업이 집중되어 있고, 확립된 GMP 시설이 존재하기 때문입니다. 알니람, 아이오니스, 애로우헤드, 웨이브 라이프 사이언시스 등의 기업뿐만 아니라, 애질런트와 서모피셔 사이언티픽과 같은 대형 제조업체들이 이 지역 시장을 뒷받침하고 있습니다. 애지런트가 2026년에 캐나다의 BIOVECTRA와 콜로라도주의 Nucleic Acid Solutions를 통합하여 설립한 "Agilent Advanced Therapeutics"를 출범시킴으로써 북미의 CDMO 서비스 체제가 강화되었습니다. FDA 규정에 대한 깊은 이해와 다년간의 GMP 실적을 바탕으로, 해당 지역은 신약 승인 신청(NDA) 획득 및 시판과 관련된 공급 분야에서 우선적인 파트너로 자리매김하고 있습니다. 그러나 전 세계 생산 능력의 확대와 납기 측면에서의 우위가 약화됨에 따라, 그 선도적 위치는 축소될 가능성이 있습니다.

유럽은 올리고뉴클레오티드 CDMO 시장의 주요 기술 거점으로 자리매김하고 있으며, 독일과 스위스가 고순도 API 제조와 지속적인 설비 투자를 주도하고 있습니다. BioSpring사는 오펜바흐에 15,200 m² 규모의 부지를 갖춘 새로운 핵산 API 생산 시설에 1억 유로를 투자하고 있으며, 이 시설은 2027년 말까지 완공될 예정입니다. Bachem사는 2025년에 3억 3,260만 스위스 프랑을 투자하고, 2026년에 "Building K" 를 상업 생산 단계로 전환하는 한편, 2026년에는 4억 스위스 프랑 이상의 추가 설비 투자를 계획하고 있습니다. 론자는 2026년 매출 성장률을 11-12%로 전망하고 있으며, 네덜란드 오스 사업장에서 첨단 합성 기술 및 항체·올리고뉴클레오티드 복합체의 제조 역량을 지속적으로 강화하고 있습니다. 유럽의 강점은 기술적 전문 지식, 엄격한 규제, 그리고 까다로운 품질 요건을 충족시키는 능력에 있습니다.

아시아태평양은 올리고뉴클레오티드 CDMO 시장에서 가장 빠르게 성장하고 있는 지역으로, 중국, 한국, 일본의 생산 능력 확대에 힘입어 2031년까지 연평균 성장률(CAGR)이 24.56%를 나타낼 것으로 전망됩니다. 2026년에 가동을 시작한 아심켐(Asymchem)의 톈진(TJ4) 시설은 첨단 가공 장비와 통합된 의약품 제조 시설을 갖추고 있으며, 연간 180몰의 올리고뉴클레오티드 생산 능력을 보유하고 있습니다. WuXi AppTec의 창저우 및 타이싱에 위치한 API 생산 거점은 2025년에 FDA 감사를 통과하여 미국으로의 지속적인 공급을 확보하고 있습니다. 일본의 일본촉매(日本触媒)는 GMP 기준을 준수하는 핵산 API 생산 능력을 10배로 확대되고 있습니다. 남미와 중동 및 아프리카는 여전히 신흥 시장이며, 주로 북미, 유럽, 아시아태평양의 허브를 통한 수입에 의존하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the oligonucleotide CDMO market size was valued at USD 3.02 billion in 2025 and is estimated to grow from USD 3.68 billion in 2026 to reach USD 9.87 billion by 2031, at a CAGR of 21.81% during the forecast period (2026-2031).

This report is Segmented by Service Type (Contract Manufacturing, Contract Development, Quality Control, Regulatory Support), Oligonucleotide Type (ASO, Sirna, GRNA, Aptamers, Others), Application (Therapeutic, Research, Diagnostic, Others), End User (Pharma, Biotech, Diagnostics, Academic, Gene Therapy, Others), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts in Value (USD).

Global Oligonucleotide CDMO Market Trends and Insights

Expanding Clinical Pipelines For RNA-Targeted Medicines

By mid-2026, over 200 organizations were contributing to the global oligonucleotide clinical pipeline, offering a broad customer base for the oligonucleotide CDMO market. Every IND-stage and late-stage program requires GMP material before approval and commercialization. The pipeline is shifting toward larger cardiometabolic opportunities, increasing batch sizes and adding pressure on commercial supply planning. Traditional synthesis setups are not designed for kilogram-to-tonne level demands for chronic conditions, leading sponsors to reserve capacity well in advance, tightening global GMP slot availability. Pipeline quality, timing, and volume are now critical factors shaping commercial contracts alongside scientific readiness.

Outsourcing Shift For Complex Oligonucleotide Synthesis And Fill-Finish

Challenges in managing complex oligonucleotide synthesis internally are driving an outsourcing trend. Manufacturing GalNAc-conjugated siRNA requires precise control across multiple stages, each adding technical complexity. By the first half of 2025, WuXi AppTec's TIDES platform supported 69 molecules for API and drug product services, more than doubling its count from two years earlier. The fill-finish step is becoming crucial as products transition to subcutaneous and prefilled formats, requiring sterile capacities beyond API synthesis. Asymchem's TJ4 facility, with an annual output of 45 million pre-filled syringe units in 2026, highlights the market's shift toward integrated API-to-drug-product solutions, raising entry barriers for smaller providers.

High Process Complexity And Yield Sensitivity In Long-Chain Oligonucleotides

The oligonucleotide CDMO market faces significant technical challenges due to the stepwise synthesis process, where one nucleotide is added at a time. For example, a 20-mer ASO undergoes at least 20 coupling cycles, and even minor efficiency losses at each step can lead to a noticeable drop in full-length yield. The complexity increases with modifications like phosphorothioate backbones, 2'-fluoro substitutions, or GalNAc ligands, which introduce side reactions and analytical difficulties. Providers transitioning from peptides or small molecules often underestimate transfer timelines, impurity management, and batch failure risks, resulting in slower capacity ramp-up despite strong demand. This explains why commercial supply remains concentrated among experienced companies with established operational histories.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand For Precision Medicine And Rare-Disease Programs

- Scale-Up Pressure From Dual-Route Manufacturing, Clinical And GMP

- Stringent Purity, Impurity, And Potency Control Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Contract Manufacturing held 51.68% of the oligonucleotide CDMO market share, reflecting the industry's reliance on GMP production for approved products and late-stage clinical programs. As sponsors advance into Phase 2, Phase 3, and launch preparation, the market prioritizes assured scale over exploratory support. Bachem's Building K in Bubendorf began GMP commercial production ramp-up in 2026, adding kilogram-scale supply to the European network. ST Pharm's USD 126 million capacity expansion, targeting 14 moles annually, highlights the growing importance of commercial manufacturing as a core differentiator. Revenue remains anchored by companies capable of consistent GMP-quality production at scales sufficient for launch planning.

Contract Development is the fastest-growing segment in the oligonucleotide CDMO market, with a 22.90% CAGR projected through 2031. Sponsors increasingly seek seamless process design transitions from early development to commercial readiness, especially for programs with modified backbones or emerging chemistries. Impurity control, process transfer, and analytical expectations now require attention well before pivotal studies. Analytical and Quality Control Services, though smaller in revenue, are becoming integral to development as release strategies impact manufacturability and regulatory timelines. Regulatory and CMC Support Services are also gaining traction as sponsors prefer single partners to streamline process work and quality packages.

In 2025, Antisense Oligonucleotides (ASOs) accounted for 58.23% of the oligonucleotide CDMO market, driven by demand in central nervous system, hepatic, and cardiometabolic indications. Ionis maintained a 12-candidate neurology pipeline in 2026, underscoring the strong outsourcing demand tied to ASOs. Established chemistry simplifies processes but still requires experienced CDMOs for transfer, scale-up, and validation, keeping ASOs as the largest revenue contributor despite growing interest in newer modalities.

Small Interfering RNA (siRNA) is the fastest-growing oligonucleotide type, with a 23.25% CAGR projected through 2031. This growth is fueled by expanding commercial portfolios and advancing late-stage pipelines. Alnylam's commercial footprint and Arrowhead's Phase 3 progress in cardiometabolic diseases are driving siRNA-oriented manufacturing needs. Guide RNA and aptamers, though smaller categories, are gaining relevance as gene editing programs advance. Other oligonucleotide types, such as PMOs and splice-switching formats, remain niche but commercially viable for specialized providers. The market is diversifying, even as ASOs continue to dominate revenue.

Complete Report Scope:

- By Service Type

- Contract Manufacturing

- Clinical Stage

- Commercial Stage

- Contract Development

- Analytical and Quality Control Services

- Regulatory and CMC Support Services

- By Oligonucleotide Type

- Antisense Oligonucleotides

- Small Interfering RNA

- Guide RNA

- Aptamers

- Other Oligonucleotide Types

- By Application

- Therapeutic Applications

- Rare Diseases

- Oncology

- Neurology

- Cardiometabolic Diseases

- Infectious Diseases

- Research Applications

- Diagnostic Applications

- Others

- By End User

- Pharmaceutical and Biotechnology Companies

- Diagnostic Companies

- Academic and Research Institutes

- Gene Therapy and Cell Therapy Developers

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America held a 39.55% share of the oligonucleotide CDMO market, driven by a concentration of RNA-targeted drug developers and established GMP sites in the U.S. and Canada. Companies like Alnylam, Ionis, Arrowhead, and Wave Life Sciences, along with manufacturing leaders such as Agilent and Thermo Fisher Scientific, anchor the region's market. Agilent's 2026 launch of Agilent Advanced Therapeutics, integrating BIOVECTRA in Canada and Nucleic Acid Solutions in Colorado, strengthened North America's CDMO offerings. Familiarity with FDA regulations and long GMP track records make the region a preferred partner for NDA-enabling and launch-related supplies. However, its lead may narrow as global capacities expand and delivery time advantages diminish.

Europe remains a key technical hub in the oligonucleotide CDMO market, led by Germany and Switzerland with high-purity API manufacturing and sustained capital investments. BioSpring's EUR 100 million investment in a new nucleic acid API facility in Offenbach, spanning 15,200 m2, is set for completion by late 2027. Bachem invested CHF 332.6 million in 2025, advancing Building K to commercial production in 2026, with over CHF 400 million in additional 2026 CapEx planned. Lonza, projecting 11-12% sales growth for 2026, continues to enhance advanced synthesis and antibody-oligonucleotide conjugate capabilities at its Oss site in the Netherlands. Europe's strength lies in its technical expertise, regulatory rigor, and ability to meet stringent quality demands.

Asia-Pacific is the fastest-growing region in the oligonucleotide CDMO market, with a 24.56% CAGR projected through 2031, driven by capacity expansions in China, South Korea, and Japan. Asymchem's TJ4 facility in Tianjin, launched in 2026, offers 180 mol per year of oligonucleotide capacity with advanced processing tools and an integrated drug product facility. WuXi AppTec's API sites in Changzhou and Taixing passed FDA inspections in 2025, ensuring continued U.S. supply. Japan's Nippon Shokubai is expanding GMP-compliant nucleic acid API capacity tenfold. South America and the Middle East & Africa remain emerging markets, primarily relying on imports from North America, Europe, and Asia-Pacific hubs.

- Agilent Technologies

- Ajinomoto Co., Inc.

- Almac Group Limited

- Asymchem Laboratories (Tianjin) Co., Ltd.

- Bachem Holding

- BioSpring GmbH

- Corden Pharma International

- Curia Global, Inc.

- Danaher

- EUROAPI S.A.

- Eurofins

- Genscript

- Kaneka

- Lonza Group

- Maravai LifeSciences Holdings, Inc.

- Merck

- PolyPeptide Group AG

- ST Pharm Co., Ltd.

- Syngene International

- Thermo Fisher Scientific

- WuXi AppTec Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Clinical Pipelines for RNA-Targeted Medicines

- 4.2.2 Outsourcing Shift for Complex Oligonucleotide Synthesis and Fill-Finish

- 4.2.3 Rising Demand for Precision Medicine and Rare-Disease Programs

- 4.2.4 Scale-Up Pressure From Dual-Route Manufacturing, Clinical and Commercial

- 4.2.5 Analytical Release Burden for Modified and Conjugated Oligomers

- 4.2.6 Supply Localization for Nucleoside, Phosphoramidite, and Specialty Raw Materials

- 4.3 Market Restraints

- 4.3.1 High Process Complexity and Yield Sensitivity in Long-Chain Oligo Synthesis

- 4.3.2 Stringent Purity, Impurity, and Potency Control Requirements

- 4.3.3 Limited Availability of Specialized Talent and Qualified GMP Capacity

- 4.3.4 Raw-Material Dependency and Batch-Level Supply Volatility

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Service Type

- 5.1.1 Contract Manufacturing

- 5.1.2 Clinical Stage

- 5.1.3 Commercial Stage

- 5.1.4 Contract Development

- 5.1.5 Analytical and Quality Control Services

- 5.1.6 Regulatory and CMC Support Services

- 5.2 By Oligonucleotide Type

- 5.2.1 Antisense Oligonucleotides

- 5.2.2 Small Interfering RNA

- 5.2.3 Guide RNA

- 5.2.4 Aptamers

- 5.2.5 Other Oligonucleotide Types

- 5.3 By Application

- 5.3.1 Therapeutic Applications

- 5.3.2 Rare Diseases

- 5.3.3 Oncology

- 5.3.4 Neurology

- 5.3.5 Cardiometabolic Diseases

- 5.3.6 Infectious Diseases

- 5.3.7 Research Applications

- 5.3.8 Diagnostic Applications

- 5.3.9 Others

- 5.4 By End User

- 5.4.1 Pharmaceutical and Biotechnology Companies

- 5.4.2 Diagnostic Companies

- 5.4.3 Academic and Research Institutes

- 5.4.4 Gene Therapy and Cell Therapy Developers

- 5.4.5 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Agilent Technologies, Inc.

- 6.3.2 Ajinomoto Co., Inc.

- 6.3.3 Almac Group Limited

- 6.3.4 Asymchem Laboratories (Tianjin) Co., Ltd.

- 6.3.5 Bachem Holding AG

- 6.3.6 BioSpring GmbH

- 6.3.7 CordenPharma International

- 6.3.8 Curia Global, Inc.

- 6.3.9 Danaher Corporation

- 6.3.10 EUROAPI S.A.

- 6.3.11 Eurofins Scientific SE

- 6.3.12 GenScript Biotech Corporation

- 6.3.13 Kaneka Corporation

- 6.3.14 Lonza Group Ltd

- 6.3.15 Maravai LifeSciences Holdings, Inc.

- 6.3.16 Merck KGaA

- 6.3.17 PolyPeptide Group AG

- 6.3.18 ST Pharm Co., Ltd.

- 6.3.19 Syngene International Limited

- 6.3.20 Thermo Fisher Scientific Inc.

- 6.3.21 WuXi AppTec Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment