|

시장보고서

상품코드

2073059

건축용 폴리비닐부티랄(PVB) 중간층 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Architectural Polyvinyl Butyral (PVB) Interlayers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

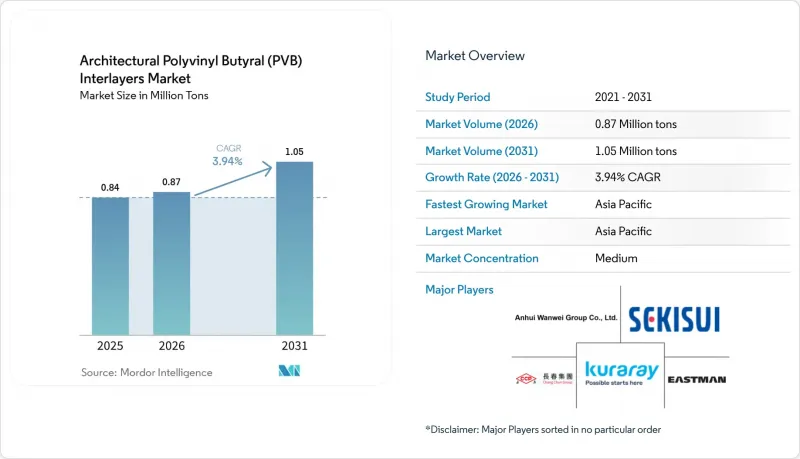

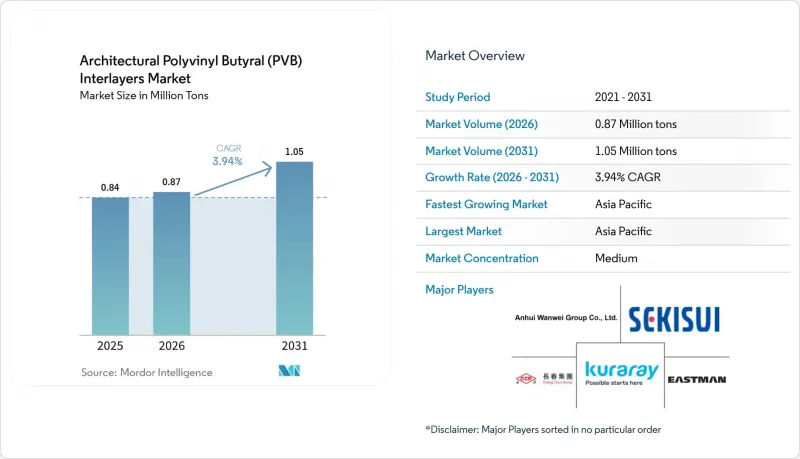

Mordor Intelligence에 의하면, 건축용 폴리비닐부티랄 중간층 시장 규모는 2025년에 84만 톤, 2026년에 87만 톤이 되어, 2031년까지 105만 톤에 이를 것으로 예측되며, 2026-2031년까지 CAGR 3.94%로 성장할 전망입니다.

본 보고서는 중간층 유형(투명, 착색, 기타), 용도(파사드/커튼월, 발코니 및 난간, 실내 칸막이, 루프라이트/스카이라이트), 최종 사용자 부문(상업시설, 주택, 공공시설), 지역(아시아태평양, 북미, 기타)별로 분류되어 있습니다. 시장 전망은 수량(톤) 기준으로 제시되어 있습니다.

전 세계 건축용 폴리비닐부티랄(PVB) 중간층 시장 동향 및 분석

현대 건축에서 안전 및 방범용 유리에 대한 수요 증가

2024년부터 2025년까지 개정된 건축기준법에 따라 난간, 가드, 경사 유리에는 접합유리의 사용이 의무화되었으며, 중간층의 최소 두께는 0.76mm로 규정되어 있습니다. ASTM E2358-24 규격에서는 파손 후의 휨 성능이 향상되었으며, 이에 따라 설계자에게는 유리가 파손된 후에도 파편이 흩어지지 않도록 보장하는 이오노머 또는 고강성 PVB 필름의 채택이 간접적으로 권장되고 있습니다. 2025년에 실시된 현장 검사 결과, 이오노머 코어를 갖춘 3층 적층 유리는 고온 환경에서도 큰 선하중을 견딜 수 있는 반면, 기본적인 PVB를 사용한 강화 단층 유리는 파손되는 것으로 밝혀졌습니다. 싱가포르에서는 당국이 유리가 완전히 파손되었을 경우 상단 가장자리의 총 처짐량에 대한 제한을 규정하고 있습니다. 표준 PVB의 경우, 대규모 다층 구조를 채택하지 않는 한 이 기준을 충족하기 어렵습니다. 검사관들이 영구적인 표시나 추적 가능한 검사 보고서를 점점 더 요구함에 따라 문서화 요건이 더욱 엄격해지고 있으며, 인증을 받은 브랜드에는 뚜렷한 경쟁 우위가 생기고 있습니다.

확대되는 아시아태평양 건설 부문

중국의 “듀얼 카본”정책에 따라 고성능 유리의 채택이 대폭 증가함에 따라, 추가적인 제조 공간을 확보하지 않아도 접합유리의 생산량이 증가하고 있습니다. 중국에서는 국내 생산량의 3분의 2를 차지하는 모듈식 커튼월 공장에서 자동화된 생산 라인을 위해 설계된 점착성이 균일한 PVB 롤이 현재 사용되고 있습니다. 인도, 베트남, 인도네시아의 건설사들은 소음 대책 및 안전 기준 개정을 목적으로 고층 빌딩의 개보수 공사를 진행하고 있습니다. 지역 공급망의 긴박함을 여실히 드러내듯, 안후이 완웨이(Anhui Wanwei) 등 국내 수지 공급업체들은 생산 능력을 확대하고 있으며, 이는 업스트림 단계인 폴리비닐알코올 원료 시장에서 아시아태평양의 우위를 뒷받침하고 있습니다.

높은 생산 비용과 대체재 선택의 유연성 부족

이오노머는 가격이 비싸지만, 표준 PVB보다 훨씬 높은 전단 탄성률을 가지고 있습니다. 2026년 5월, 쿠라레는 에너지 비용과 첨가제 비용의 상승을 이유로 PVB 및 이오노머 제품 모두에 대해 전 세계적인 가격 인상을 발표했습니다. 일단 이오노플라스트를 사용한 난간 설계가 승인되면, PVB로 되돌리려면 ASTM E2358에 따른 새로운 검사가 필요하기 때문에 그러한 변경은 거의 이루어지지 않습니다. 오토클레이브 예비 설비를 갖추지 못한 중규모 라미네이트 제조업체들은 설비 투자 문제에 직면해 있으며, 이로 인해 시장 진입이 지연되면서 건축용 폴리비닐부티랄(PVB) 중간층 시장에서 중간 정도의 집중 현상이 나타나고 있습니다.

부문별 분석

2025년까지 투명 등급은 시장 규모의 57.5%를 차지했습니다. 유리와의 매끄러운 접합, 중립적인 광학적 특성, 기존 오토클레이브 사이클과의 호환성 덕분에 주류 파사드 분야에서 최적의 선택지로서의 입지를 확고히 다졌습니다. 건축용 폴리비닐부티랄(PVB) 중간층 시장, 특히 투명 필름 시장은 건설 GDP의 추이에 따라 완만한 성장세를 보이고 있습니다.

기초 규모가 비교적 작았음에도 불구하고, 아이오노머 필름은 가장 강력한 성장세를 보이며 2026-2031년의 예측 기간 동안 연평균 성장률(CAGR) 5.19%를 기록했습니다. 이러한 성장은 파손된 난간의 처짐을 억제하기 위한 규제 조항에 힘입어 이루어졌습니다. 2025년 현장 시험에서 8mm 두께의 열강화 프라이 사이에 3.04mm 두께의 이오노플라스트 코어를 끼운 적층재가 1.5kN/m의 하중을 견뎌냈으며, 상부 난간이 없어도 안전성이 입증되었습니다. 착색 및 그라데이션 PVB는 브랜드 이미지와 사생활 보호라는 두 가지 요구를 충족시키며, 변색에 강한 화학 성분을 활용하여 자외선의 99%를 차단했습니다. 더 부드러운 코어를 특징으로 하는 방음용 PVB는 차음 등급(STC)을 2-5포인트 향상시켰습니다. 이러한 성능 향상 덕분에 주택 리모델링에 있어 최적의 선택지가 되었으며, 집주인은 조용한 공간을 제공함으로써 더 높은 임대료를 책정할 수 있게 되었습니다. 마지막으로, 적외선 차단 기능을 갖춘 기능성 일사 제어용 PVB는 가시광선 투과율을 80%로 유지하면서, 피크 시간대의 냉방 부하를 10-15W/m² 줄였습니다.

지역별 분석

아시아태평양은 2025년에 전 세계 출하량의 45.43%를 차지할 것으로 예상되며, 2026년부터 2031년까지의 예측 기간 동안 연평균 성장률(CAGR) 4.87%를 기록할 전망입니다. 중국은 환경 대책을 강화하기 위해 에너지 기준을 개정하고, 추운 지역의 U값을 0.8W/m²·K로 제한했습니다. 또한, 공공 프로젝트 입찰을 친환경 제품 인증과 연계함으로써, 접합 유리의 중요성을 높이고 있습니다. 인도에서는 2025년 안전 기준 개정에 따라, 높이 15미터를 초과하는 건물의 발코니 난간에 접합 유리를 사용하는 것이 권장되었습니다. 아세안(ASEAN)에서는 신규 지하철 노선 주변의 소음 규제가 강화됨에 따라 수요가 현저히 증가했습니다. 북미에서는 허리케인, 내진, 방범용 유리에 관한 규제가 수요를 견인했습니다. 유럽에서는 Level(s)에 따른 전체 수명 주기에 걸친 탄소 배출량 보고 활동과 각국의 난간 기준 준수를 통해 수요의 성장세가 유지되었습니다. 마찬가지로, 라틴아메리카와 중동에서도 고급 고층 아파트 단지에서 수요가 급증하면서, 수입된 프리미엄 중산층이 점점 더 선호되게 되었습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.07According to Mordor Intelligence, the architectural polyvinyl butyral interlayers market size is projected to be 0.84 million tons in 2025, 0.87 million tons in 2026, and reach 1.05 million tons by 2031, growing at a CAGR of 3.94% from 2026 to 2031.

This report is Segmented by Interlayer Type (Transparent, Colored, and More), Application (Facade/Curtain Wall, Balcony and Balustrade, Interior Partitions, and Roof-lights/Skylights), End-User Sector (Commercial, Residential, and Institutional Buildings), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

Global Architectural Polyvinyl Butyral (PVB) Interlayers Market Trends and Insights

Rising Demand for Safety and Security Glazing in Modern Architecture

During 2024-2025, updated building codes mandate the use of laminated glass in handrails, guards, and sloped glazing, specifying a minimum interlayer thickness of 0.76 mm. The ASTM E2358-24 standard improves post-breakage deflection performance, subtly encouraging designers to adopt ionomer or stiff-PVB films, which ensure the glass remains intact after fracturing. Field tests conducted in 2025 reveal that triple-layer laminates with ionomer cores can handle significant line loads at high temperatures, whereas tempered monoliths with basic PVB fail. In Singapore, authorities establish a limit for total top-edge deflection in cases of complete glass loss. Standard PVB struggles to meet this benchmark without extensive multi-ply constructions. As inspectors increasingly require permanent markings and traceable test reports, documentation demands intensify, providing certified brands with a notable advantage.

Expanding APAC Construction Sector

China's dual-carbon policy has significantly increased the adoption of high-performance glass, resulting in higher laminated volumes without requiring additional raw floor space. In China, modular curtain-wall factories, which produce two-thirds of the nation's output, are now using consistent-tack PVB rolls designed for their automated production lines. Builders in India, Vietnam, and Indonesia are retrofitting high-rise towers for noise control and updating safety codes. Highlighting the tightness of the regional supply chains, domestic resin suppliers, such as Anhui Wanwei, have expanded their capacities, underscoring the dominance of the Asia-Pacific region in the upstream polyvinyl alcohol feedstock market.

High Production Cost and Limited Substitution Flexibility

Ionomers command a premium price, yet they offer a shear modulus that is significantly greater than that of standard PVB. In May 2026, Kuraray, citing rising energy and additive costs, announced a global price increase for both PVB and ionomer products. Once a balustrade design is approved for ionoplast, reverting to PVB requires fresh testing under ASTM E2358, making such changes infrequent. Medium-sized laminators, lacking autoclave redundancy, face capital challenges, which delay their market entry and result in a moderate concentration in the architectural polyvinyl butyral (PVB) interlayers market.

Other drivers and restraints analyzed in the detailed report include:

- Tightening Energy-Efficiency Codes Driving Laminated Facade Adoption

- Aesthetic Differentiation via Gradient and Colored Interlayers

- Moisture Sensitivity and Edge-Stability Issues in Harsh Climates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

By 2025, transparent grades captured 57.5% of the market volume. Their seamless welding with glass, neutral optical properties, and compatibility with existing autoclave cycles cemented their position as the preferred choice for mainstream facades. The market for architectural polyvinyl butyral (PVB) interlayers, particularly transparent films, has seen modest growth in alignment with the construction GDP.

Starting from a smaller base, ionomer films showcased the strongest growth, boasting a 5.19% CAGR during the forecast period of 2026-2031. This uptick was spurred by regulatory code clauses that curtailed deflection in broken balustrades. In 2025 field trials, laminates with 3.04 mm ionoplast cores, nestled between 8 mm heat-strengthened plies, withstood 1.5 kN/m loads, validating safety without top rails. Colored and gradient PVBs addressed twofold demands: branding and privacy, utilizing colorfast chemistries to block 99% of UV rays. Acoustic PVBs, featuring softer cores, boosted the Sound Transmission Class (STC) by 2-5 points. This enhancement has made them a top pick for residential retrofits, enabling landlords to charge premium rents for quieter spaces. Lastly, functional solar-control PVBs, equipped with infrared blockers, curbed peak cooling loads by 10-15 W/m2, all while permitting 80% visible light transmission.

Complete Report Scope:

- By Interlayer Type

- Transparent

- Coloured

- Opaque

- Frosted/Matte

- Gradient and White Gradient (incl. Cielora and similar products)

- Acoustic PVB

- Functional/Solar PVB

- Ionomer Interlayer

- By Application

- Facade/Curtain Wall

- Balcony and Balustrade/Guard-rail

- Interior Partitions and Privacy Screens

- Roof-lights/Skylights/Canopies

- By End-user Sector

- Commercial Buildings

- Residential Buildings

- Institutional Buildings

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Nordic Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- United Arab Emirates

- Rest of Middle-East and Africa

- Asia-Pacific

Geography Analysis

Asia-Pacific, projected to account for 45.43% of the global volume in 2025, is set to register a 4.87% CAGR during the forecast period of 2026-2031. In a bid to strengthen its green initiatives, China revised its energy code, capping U-values at 0.8 W/m2*K in its colder provinces. Additionally, the nation linked public project bids to green product certifications, increasing the prominence of laminated glass. In India, a 2025 safety amendment endorsed laminated glass for balcony rails in buildings exceeding 15 meters in height. The ASEAN region, responding to heightened acoustic specifications near new metro lines, saw a notable surge in demand. North America benefited from regulations on hurricane, seismic, and security glazing. Europe sustained its momentum through whole-life carbon reporting initiatives under Level(s) and compliance with national balustrade standards. Similarly, Latin America and the Middle-East experienced a demand spike from boutique high-rise clusters, which increasingly favored imported premium interlayers.

- Anhui Wanwei Group Co., Ltd.

- Chang Chun Group

- Eastman Chemical Company

- EVERLAM

- Genau Manufacturing Company LLP

- HTS PVB

- Huakai Plastic (Chongqing) Co., Ltd.

- KB PVB

- Kuraray Co., Ltd.

- Qingdao Huayijin New Material Co., Ltd.

- SEKISUI Chemical Co., Ltd.

- Suzhou ShinNord New Material Co., Ltd.

- Suzhou Xiaoshi Technology Co., Ltd.

- Zhejiang Decent New Material Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for safety and security glazing in modern architecture

- 4.2.2 Expanding APAC construction sector

- 4.2.3 Tightening energy-efficiency codes driving laminated facade adoption

- 4.2.4 Aesthetic differentiation via gradient andcolored interlayers

- 4.2.5 Growing retrofit market for acoustic comfort in dense cities

- 4.3 Market Restraints

- 4.3.1 High production cost andlimited substitution flexibility

- 4.3.2 Moisture sensitivity and edge-stability issues in harsh climates

- 4.3.3 Volatility in PVB-resin feedstock supply

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Interlayer Type

- 5.1.1 Transparent

- 5.1.2 Coloured

- 5.1.2.1 Opaque

- 5.1.2.2 Frosted/Matte

- 5.1.2.3 Gradient and White Gradient (incl. Cielora and similar products)

- 5.1.3 Acoustic PVB

- 5.1.4 Functional/Solar PVB

- 5.1.5 Ionomer Interlayer

- 5.2 By Application

- 5.2.1 Facade/Curtain Wall

- 5.2.2 Balcony and Balustrade/Guard-rail

- 5.2.3 Interior Partitions and Privacy Screens

- 5.2.4 Roof-lights/Skylights/Canopies

- 5.3 By End-user Sector

- 5.3.1 Commercial Buildings

- 5.3.2 Residential Buildings

- 5.3.3 Institutional Buildings

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Nordic Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Anhui Wanwei Group Co., Ltd.

- 6.4.2 Chang Chun Group

- 6.4.3 Eastman Chemical Company

- 6.4.4 EVERLAM

- 6.4.5 Genau Manufacturing Company LLP

- 6.4.6 HTS PVB

- 6.4.7 Huakai Plastic (Chongqing) Co., Ltd.

- 6.4.8 KB PVB

- 6.4.9 Kuraray Co., Ltd.

- 6.4.10 Qingdao Huayijin New Material Co., Ltd.

- 6.4.11 SEKISUI Chemical Co., Ltd.

- 6.4.12 Suzhou ShinNord New Material Co., Ltd.

- 6.4.13 Suzhou Xiaoshi Technology Co., Ltd.

- 6.4.14 Zhejiang Decent New Material Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Integration of smart andfunctional interlayers in next-generation facade systems