|

시장보고서

상품코드

2073081

의료기기 CDMO 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Medical Device CDMO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

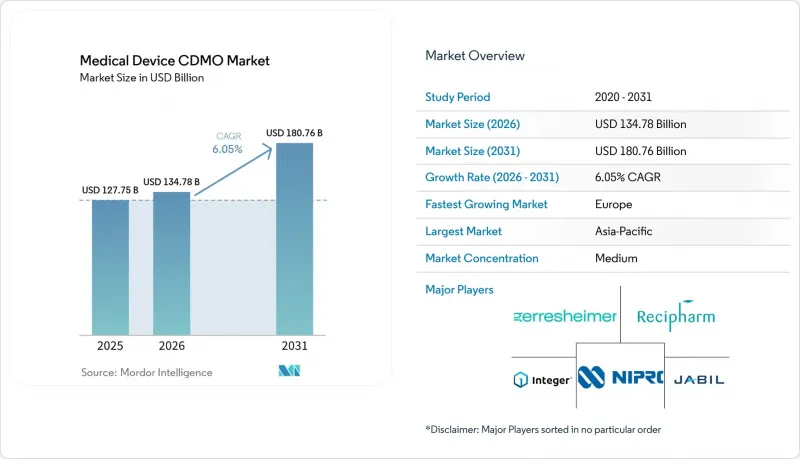

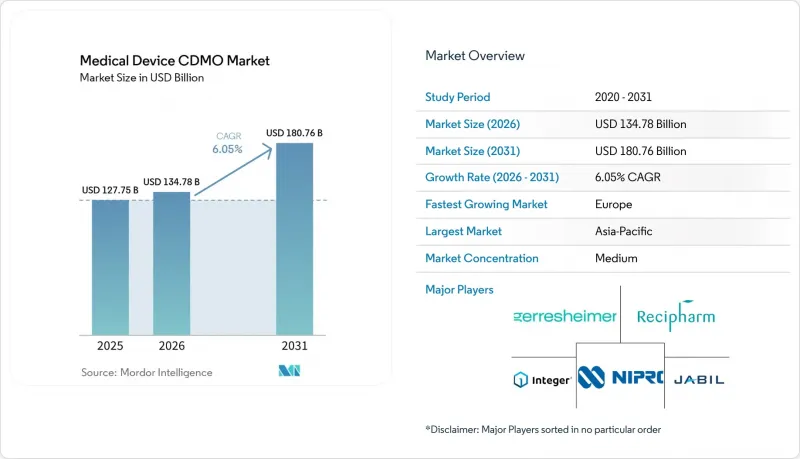

Mordor Intelligence에 의하면, 의료기기 CDMO 시장 규모는 2025년에 1,277억 5,000만 달러로 평가되었고 2026년 1,347억 8,000만 달러에서 2031년까지 1,807억 6,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 6.05%를 나타낼 전망입니다.

본 보고서는 제품 유형(진단용, 치료용, 의약품 및 의료기기 조합), 서비스(수탁 개발, 수탁 제조, 포장, 기타), 의료기기 등급(등급 I, II, III), 용도(심혈관, 정형외과, 외과, 기타), 최종 용도(OEM, 제약회사, 기타), 지역(북미, 유럽, 기타)별로 분류되어 있습니다. 시장 전망치는 금액(달러) 단위로 제시되어 있습니다.

세계 의료기기 CDMO 시장 동향과 인사이트

복잡한 의료기기의 개발 및 제조 외주

의료기기 CDMO 시장은 많은 OEM 업체들이 더 이상 자사 네트워크 내에서 프로그램을 완전히 관리하기를 원하지 않게 되면서 복잡한 프로그램이 꾸준히 증가하고 있는 데 힘입어 호조를 보이고 있습니다. 소형화, 연결성 및 전기·기계 복합 설계를 통해, 사내 제조 거점이 필요한 검증 절차를 준수하면서 모든 제조 공정을 아우르는 것이 점점 더 어려워지고 있습니다. Integer Holdings사는 2026년 1분기 실적 발표에서 고객들이 계속해서 아웃소싱 확대를 요구하고 있다고 밝혔으며, 이는 이러한 추세가 2026년에도 여전히 지속되고 있음을 보여줍니다. 또한 Plexus사는 2026 회계연도 2분기 헬스케어 및 생명과학 부문의 매출이 목표 범위를 상회하는 성장세를 보였습니다고 보고했으며, 이는 전문적인 외부 생산 지원에 대한 견조한 수요를 뒷받침하고 있습니다. OEM 각사가 사내 금형 개발 능력이나 공정 엔지니어링의 대응 범위를 축소하면, 해당 프로그램을 다시 사내로 되돌릴 수 있는 능력은 약화됩니다. 이로 인해 의료기기 CDMO 시장의 거래 관계 주기가 장기화됨에 따라, 설계 인계부터 검증 완료된 생산에 이르기까지 책임의 단절 없이 프로그램을 수행할 수 있는 공급업체가 유리한 입장에 서게 됩니다.

복합 제품 및 약물 전달 시스템에 대한 수요 증가

의료기기 CDMO 시장에서는 의약품 및 의료기기 복합 제품에 대한 수요가 증가하고 있습니다. 이는 이러한 프로그램에서 의료기기 엔지니어링, 무균 공정 관리, 그리고 의약품 관련 규정 준수가 동시에 요구되기 때문입니다. 2026년 2월 FDA의 품질 관리 시스템 규정이 시행됨에 따라, 의료기기 및 의약품 분야의 요건을 모두 충족해야 하는 제조업체에 대한 규정 준수 기준이 강화되었습니다. 또한, FDA 복합제품국은 2025년 6월, 복합제품에 대한 고유 의료기기 식별자(UDI) 요건에 관한 지침 초안을 발표하며, 이 범주에 대한 규제 당국의 지속적인 관심을 보여주었습니다. 이러한 이중 부담으로 인해 의료기기 CDMO 시장에서 규모와 통합된 품질 시스템의 가치가 높아지고 있습니다. 왜냐하면 소규모 전문 업체의 경우, 이에 대응할 수 있는 의약품 인프라가 부족한 경우가 많기 때문입니다. 2025년 2월 Jabil이 Pharmaceutics International을 인수한 사례는 이미 입지를 다진 의료기기 전문 공급업체가 경쟁 압박에 대응하기가 더욱 어려워지기 전에 어떻게 의약품 제조 역량을 구축하고 있는지를 보여줍니다. 그 결과, 시장의 성장 추세가 물리적 의료기기와 규제 대상 의약품의 인터페이스를 모두 단일 운영 모델 내에서 처리할 수 있는 공급업체로 이동하고 있습니다.

여러 관할 구역에 걸쳐 진행되는 프로그램에서 발생하는 규제상 검증 부담

의료기기 CDMO 시장에서는 하나의 프로그램이 FDA, EU MDR 및 각국의 요건을 동시에 충족해야 하는 경우, 여전히 막중한 규제 부담에 직면해 있습니다. 2026년 2월에 발효된 FDA의 품질 관리 시스템 규정(QMSR)은 ISO 13485를 참조 기준으로 반영하여, 외부 위탁 프로세스 및 공급업체 관리에 관한 문서화된 관리의 중요성을 강조했습니다. RAPS의 보고서에 따르면, QMSR 도입 초기 감사에서 외부 위탁 및 구매 관리가 양식 483의 주요 지적 사항으로 거론되었으며, 이는 규제 당국이 외부 제조에 대한 감독을 얼마나 직접적으로 심사하고 있는지를 뒷받침하고 있습니다. 2026년 BVMed가 발표한 "독일 메드테크 전망"에 따르면, 독일 의료기기 제조업체의 93%가 중소기업인 것으로 나타났습니다. 이는 소규모 조직일수록 문서화 부담을 더 크게 느끼기 때문에 중요한 점입니다. 의료기기 CDMO 시장에서는 사내에 규제 대응 팀을 보유한 공급업체에게 유리한 환경이 조성되고 있지만, 한편으로는 업계 전체의 고정 운영 비용도 상승시키고 있습니다. 그 결과, 규정 준수 대응 능력이 공장 규모만큼이나 중요해지고 있는 시장이 형성되고 있습니다.

부문별 분석

2025년, 의약품 및 의료기기 복합 제품은 의료기기 CDMO 시장 점유율의 56.21%를 차지하며 제품 수요의 중심으로서 두드러졌습니다. 이러한 선도적인 위상은 자동 주사기, 프리필드 주사기, 흡입형 의약품 및 의료기기 시스템, 그리고 임플란트 연동형 투여 형태의 보급을 반영하고 있습니다. 의료기기 CDMO 시장에서 이러한 프로그램들은 단순한 생산량 이상의 중요성을 지닙니다. 왜냐하면, 장치 엔지니어링뿐만 아니라 의약품 규정 준수 요건과 무균 공정에 대한 기대치도 모두 충족하고 있기 때문입니다. 이 범주에 해당하는 공급업체는 제품 전반에 걸쳐 일관된 품질 관리 체계를 유지해야 하므로, 이에 따라 적격 공급업체의 선택 폭이 좁아집니다. 이러한 공급업체 기반의 축소로 인해, 고객들은 이미 통합 프로그램 인증을 취득한 사업자에 대한 의존도를 높이고 있습니다.

치료제 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 6.81%로 성장할 것으로 전망되며, 이는 향후 수요가 만성 질환을 위한 투여법이나 임플란트를 활용한 치료 방식으로 전환되고 있음을 보여줍니다. 바이오시밀러용 웨어러블 투여 플랫폼 및 새로운 이식형 치료법의 등장으로, 더 긴 제품 수명 주기 동안 정밀한 조립 과정을 관리할 수 있는 제조 파트너에 대한 수요가 증가하고 있습니다. 진단 분야는 매출 규모 면에서는 여전히 소규모이지만, 마이크로플루이딕스 기술, 소형 센서, 내장형 분석 기능을 갖춘 현장 진단(PoC) 플랫폼 분야에서 그 중요성이 커지고 있습니다. 2026년 1월 Jabil이 TxSphere와 체결한 제조 제휴(1차 의약품 패키지의 충전 및 마무리 공정 지원 포함)는 의료기기 CDMO 시장이 복합 프로그램을 위한 단일 통합 생산 체인으로 전환되고 있음을 보여줍니다. 이러한 점들을 종합해 보면, 제품 수요 측면에서는 치료, 기기, 패키징의 인터페이스를 단일 통합 운영 모델로 관리할 수 있는 공급업체를 점점 더 중요하게 여기는 경향이 있습니다.

2025년 의료기기 CDMO 시장 규모에서 수탁 개발은 42.83%의 점유율을 차지하고 있는 반면, 수탁 제조는 2031년까지 연평균 성장률(CAGR) 7.94%를 나타낼 것으로 예측됩니다. 개발 기반의 확대는 OEM 각사가 설계 이전, 시험, 검증 계획, 품질 문서화 측면에서 여전히 외부 지원에 크게 의존하고 있음을 보여줍니다. 이러한 서비스를 통해 고객사는 모든 제품 유형에 걸쳐 고도의 엔지니어링 역량을 자체적으로 유지할 필요가 없어, 시장 출시까지의 시간적 압박을 줄일 수 있습니다. 또한, 이러한 조치들은 초기 단계에서 협력의 기회를 창출하며, 향후 장기적인 생산 계약으로 이어질 가능성이 있습니다. 의료기기 CDMO 시장에서 초기 단계부터 참여하는 것은 상업 생산 수주가 확정되기 훨씬 전에 공급업체 선정에 영향을 미치는 경우가 많습니다.

OEM 업체들이 고정 생산 자산과 전문적인 조립 작업을 기존 인프라를 갖춘 외부 파트너에게 지속적으로 이전하고 있기 때문에 수탁 제조의 성장 속도가 가속화되고 있습니다. 의료기기의 제조 및 조립은 완제품부터 추적성 및 엄격한 공정 관리가 필요한 고도의 하위 조립체에 이르기까지 여전히 가장 광범위한 프로젝트를 아우르고 있습니다. 심혈관 및 신경 조절 분야에서는 범용 공장 내 공차 관리나 정밀 가공의 규모 확대가 어렵기 때문에 부품 제조의 중요성이 커지고 있습니다. 또한, 고객들이 단일 상업 계약 하에서 신청 지원 및 제조 조정을 요청하는 경향이 강해지고 있어, 포장 및 의약품 관련 업무도 더욱 전략적인 위치를 차지하고 있습니다. 따라서 의료기기 CDMO 시장은 프로그램을 여러 공급업체에 분산시키지 않고, 개발 단계에서 지속적인 공급 단계로 원활하게 전환할 수 있는 풀서비스형 플랫폼을 지향하는 추세입니다.

지역별 분석

북미는 주요 OEM 기업의 입지, 규제 당국과의 근접성, 그리고 고도로 숙련된 제조 인력의 풍부한 기반을 모두 갖추고 있어, 의료기기 CDMO 시장에서 여전히 가장 높은 부가가치를 창출하는 지역 중 하나로 자리매김하고 있습니다. 미국은 이 시장에서 계속해서 대규모 투자를 유치하고 있으며, 게레스하이머사가 조지아주 피치트리시티에서 사업을 확장한 것은 미국 내 클린룸 및 의료기기 자동화 생산 능력에 대한 지속적인 신뢰를 보여주는 것입니다. 인테저 홀딩스(Integer Holdings) 역시 2026년 1분기에 전기생리학, 구조적 심장 질환, 신경혈관, 신경조절 분야에 대한 지속적인 집중을 보여주고 있으며, 이는 해당 지역의 아웃소싱 수요를 뒷받침하는 고부가가치 부문과 일치합니다. 멕시코는 확립된 의료 제조 클러스터를 통해 니어쇼어링에 대한 관심 증가를 흡수하고 있으며, 이는 미국 고객들의 국경을 초월한 생산 전략을 뒷받침하고 있습니다. 코스타리카는 엄밀히 말해 북미에 속하지는 않지만, 북미의 조달 결정과 밀접하게 연계되어 있으며, 규제를 준수하는 저비용 생산 능력을 통해 지역 공급망을 강화하고 있습니다.

유럽은 2031년까지 연평균 성장률(CAGR) 7.82%를 나타낼 것으로 전망되며, 의료기기 CDMO 시장에서 지역별로는 가장 빠른 성장세를 보이고 있습니다. 이러한 성장은 해당 지역의 규정 준수 환경과 밀접한 관련이 있습니다. EU의 MDR 요건이 강화됨에 따라, 더 많은 OEM 및 제약사 고객들이 검증된 유럽 생산 거점과 확실한 규제 대응 실적을 갖춘 공급업체를 찾고 있기 때문입니다. BVMed의 데이터에 따르면, 독일 의료 기술 제조업체의 93%가 중소기업이며, 이것이 해당 지역 전체에서 외부 기관을 통한 규제 대응 및 제조 지원의 중요성이 높아지고 있는 이유 중 하나입니다. 아일랜드는 주목할 만한 서브 허브로 부상하고 있으며, 퀘이서 메디컬의 골웨이 시설 인수는 중재적 의료기기 프로그램 분야에서 이 회사의 유럽 내 입지를 한층 더 공고히 했습니다. 스페인, 프랑스, 이탈리아는 특히 정형외과, 치과, 정밀 부품 분야에서 이미 산업 기반이 확립되어 있어, 여전히 확고한 아웃소싱 거점으로 자리 잡고 있습니다.

아시아태평양은 2025년 의료기기 CDMO 시장 점유율의 39.41%를 차지하며, 매출 기준 최대 지역 거점으로서의 위상을 유지했습니다. 이 지위는 중국, 인도, 한국 및 기타 제조 거점들의 지원을 바탕으로 한 클래스 I 및 복잡도가 낮은 클래스 II 의료기기의 대량 생산 분야에서 해당 지역이 오랫동안 수행해 온 역할을 반영하고 있습니다. Plexus사는 2026 회계연도 2분기에 샤먼(Xiamen) 거점을 위한 차세대 현장 진단용 초음파 프로그램을 수주했습니다. 이는 아시아 거점이 기술적으로 더 복잡한 업무도 수주하고 있음을 보여줍니다. 중동 및 아프리카 및 남미는 의료기기 CDMO 시장에서 여전히 규모가 작은 편이지만, 브라질은 예외입니다. 해당 국가에서는 국내 의료기기 관련 활동과 현지 등록 요건으로 인해, 해당 지역 내 제조 파트너십에 대한 관심이 높아지고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the medical device CDMO market size was valued at USD 127.75 billion in 2025 and is estimated to grow from USD 134.78 billion in 2026 to reach USD 180.76 billion by 2031, at a CAGR of 6.05% during the forecast period (2026-2031).

This report is Segmented by Product Type (Diagnostics, Therapeutics, Drug-Device Combinations), Service (Contract Development, Contract Manufacturing, Packaging, Others), Device Class (Class I, II, III), Application (Cardiovascular, Orthopedic, Surgical, Others), End Use (OEMs, Pharma Companies, Others), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Value (USD).

Global Medical Device CDMO Market Trends and Insights

Outsourcing of Complex Device Development and Manufacturing

The medical device CDMO market is gaining support from the steady rise in complex programs that many OEMs no longer want to manage fully inside their own networks. Miniaturization, connectivity, and mixed electromechanical design are making it harder for internal plants to cover every manufacturing step with the needed validation discipline. Integer Holdings stated in its first quarter 2026 earnings release that customers are continuing to look for more outsourcing, which shows that this shift is still active in 2026. Plexus also reported Healthcare and Life Sciences revenue growth ahead of its target range in fiscal second quarter 2026, which points to healthy demand for specialist external production support. Once OEMs narrow internal tooling depth and process engineering coverage, the ability to bring those programs back in-house becomes weaker. That creates a longer relationship cycle in the medical device CDMO market, and it favors suppliers that can take a program from design transfer into validated production without a break in responsibility.

Rising Demand for Combination Products and Drug Delivery Systems

The medical device CDMO market is seeing stronger demand from drug-device combinations because these programs require device engineering, sterile process control, and drug-side compliance at the same time. The FDA Quality Management System Regulation became effective in February 2026, and that raised the compliance standard for manufacturers operating across device and drug requirements. The FDA Office of Combination Products also issued draft guidance on Unique Device Identifier requirements for combination products in June 2025, which signaled continued regulatory attention on this category. That dual burden makes scale and integrated quality systems more valuable in the medical device CDMO market because smaller specialists often lack matching pharmaceutical infrastructure. Jabil's February 2025 acquisition of Pharmaceutics International showed how established device-focused suppliers are building drug manufacturing capability before competitive pressure becomes harder to manage. As a result, growth is moving toward suppliers that can handle both the physical device and the regulated drug interface within one operating model.

Regulatory Validation Burden Across Multi-Jurisdiction Programs

The medical device CDMO market still faces a heavy regulatory burden when one program must satisfy the FDA, EU MDR, and national requirements at the same time. The FDA Quality Management System Regulation took effect in February 2026 and incorporated ISO 13485 by reference, which increased the importance of documented control over outsourced processes and supplier management. RAPS reported that outsourcing and purchasing controls appeared among the main Form 483 observation areas during early QMSR-era inspections, which reinforces how directly regulators are reviewing external manufacturing oversight. BVMed data published in the 2026 German MedTech outlook showed that 93% of German MedTech manufacturers are SMEs, and that matters because smaller organizations feel the documentation burden more sharply. In the medical device CDMO market, the environment favors providers with in-house regulatory teams, but it also raises fixed operating costs across the sector. The result is a market where compliance capability is becoming as important as factory footprint.

Other drivers and restraints analyzed in the detailed report include:

- Pharma-Medtech Convergence and Integrated Development Models

- Reshoring and Supply Chain Risk Rebalancing for Critical Devices

- Long Qualification Cycles for High-Risk and Class III Devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Drug-device combination products held 56.21% of the medical device CDMO market share in 2025, which made them the clear center of product demand. That leadership reflects the wider use of autoinjectors, pre-filled syringes, inhaled drug-device systems, and implant-linked delivery formats. In the medical device CDMO market, these programs carry more than volume, because they also combine device engineering with pharmaceutical compliance and sterile process expectations. Suppliers that serve this category must maintain aligned quality systems across both sides of the product, which narrows the pool of eligible vendors. That narrower supplier base supports stronger customer dependence on operators that already passed qualification for integrated programs.

Therapeutics is projected to grow at a 6.81% CAGR from 2026 to 2031, which shows that future demand is moving toward chronic disease delivery and implant-enabled treatment formats. Biosimilar wearable delivery platforms and newer implantable therapeutic modalities are expanding the need for manufacturing partners that can manage precision assembly over longer product lifecycles. Diagnostics remains smaller in revenue terms, but it is becoming more relevant where point-of-care platforms include microfluidics, compact sensing, and embedded analytics. Jabil's January 2026 manufacturing partnership with TxSphere, including fill-finish support for primary drug packs, showed how the medical device CDMO market is moving toward one coordinated production chain for combination programs. Taken together, product demand is increasingly favoring suppliers that can manage therapy, device, and packaging interfaces as one integrated operating model.

Contract development accounted for 42.83% share of the medical device CDMO market size in 2025, while contract manufacturing is projected to grow at a 7.94% CAGR through 2031. The larger development base shows that OEMs still depend heavily on outside support for design transfer, testing, validation planning, and quality documentation. These services reduce time-to-market pressure without requiring customers to keep full engineering depth across every program type. They also create early engagement points that can later convert into long production contracts. In the medical device CDMO market, front-end involvement often shapes supplier selection well before a commercial manufacturing award is finalized.

Contract manufacturing is growing faster because OEMs continue to shift fixed production assets and specialized assembly work toward external partners with existing infrastructure. Device manufacturing and assembly still cover the broadest range of projects, from finished units to advanced subassemblies that need traceability and controlled process discipline. Component manufacturing is gaining importance in cardiovascular and neuromodulation work, where tolerance control and precision machining are harder to scale inside generalist plants. Packaging and regulatory affairs are also becoming more strategic, because customers increasingly want submission support and manufacturing coordination under one commercial agreement. That keeps the medical device CDMO market oriented toward full-service platforms that can move from development into supply continuity without handing the program across multiple vendors.

Complete Report Scope:

- By Product Type

- Diagnostics

- Therapeutics

- Drug-Device Combination Products

- By Service

- Contract Development

- Product Design and Development Services

- Testing and Validation

- Quality Management

- Others

- Contract Manufacturing

- Accessories Manufacturing

- Assembly Manufacturing

- Component Manufacturing

- Device Manufacturing

- Packaging

- Regulatory Affairs

- Contract Development

- By Device Class

- Class I

- Class II

- Class III

- By Application

- Cardiovascular Devices

- Orthopedic Devices

- Ophthalmic Devices

- Diagnostic Devices

- Respiratory Devices

- Surgical Instruments

- Dental

- Others

- By End Use

- Original Equipment Manufacturers

- Pharmaceutical and Biopharmaceutical Companies

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America remains one of the most value-dense parts of the medical device CDMO market because it combines large OEM presence, regulatory proximity, and a deep base of advanced manufacturing talent. The United States continues to attract premium investment in this market, and Gerresheimer's expansion in Peachtree City, Georgia, showed continued confidence in domestic cleanroom and automated device production capacity. Integer Holdings also pointed to continued focus on electrophysiology, structural heart, neurovascular, and neuromodulation in the first quarter of 2026, which aligns with the higher-value segments that support outsourcing demand in the region. Mexico is absorbing added nearshoring interest through its established medical manufacturing clusters, and that supports cross-border production strategies for U.S. customers. Costa Rica, while outside formal North America, remains tightly linked to North American sourcing decisions and strengthens the regional supply chain through compliant, lower-cost production capacity.

Europe is projected to grow at a 7.82% CAGR through 2031, giving it the fastest regional pace in the medical device CDMO market. That growth is tied closely to the region's compliance environment, because stricter EU MDR requirements are pushing more OEM and pharma customers toward suppliers with validated European manufacturing sites and established regulatory experience. BVMed data showed that 93% of German MedTech manufacturers are SMEs, which helps explain why external regulatory and manufacturing support is becoming more important across the region. Ireland has become a notable sub-hub, and Quasar Medical's acquisition of the Galway facility added scale to its European position in interventional device programs. Spain, France, and Italy remain established outsourcing bases, especially where orthopedic, dental, and precision component work already has an industrial foundation.

Asia-Pacific held 39.41% of the medical device CDMO market share in 2025, which kept it as the largest regional base by revenue. That position reflects the region's long-standing role in high-volume production for Class I and lower-complexity Class II devices, supported by facilities across China, India, South Korea, and other manufacturing centers. Plexus secured a next-generation point-of-care ultrasound program for its Xiamen facility in the fiscal second quarter of 2026, which showed that Asian sites are also winning more technically complex work. The Middle East and Africa and South America remain smaller in the medical device CDMO market, with Brazil standing out, where domestic device activity and local registration needs are supporting greater interest in regional manufacturing partnerships.

- Benchmark Electronics, Inc.

- Celestica

- Cogmedix, Inc.

- Flex

- Gerresheimer

- Integer Holdings

- Jabil

- Kimball Electronics, Inc.

- Mack Molding Co., Inc.

- Nipro

- Nortech Systems

- Phillips-Medisize Corporation

- Plexus Corp.

- Recipharm

- Sanmina Corporation

- Synecco Ltd

- Stryker

- TE Connectivity Ltd.

- Thermo Fisher Scientific

- Viant Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Outsourcing of Complex Device Development and Manufacturing

- 4.2.2 Rising Demand for Combination Products and Drug Delivery Systems

- 4.2.3 Expansion of High-Precision, Low-Touch Manufacturing Capabilities

- 4.2.4 Pharma-Medtech Convergence and Integrated Development Models

- 4.2.5 Sustainability-Led Material Substitution in Device Components

- 4.2.6 Reshoring and Supply Chain Risk Rebalancing for Critical Devices

- 4.3 Market Restraints

- 4.3.1 Regulatory Validation Burden Across Multi-Jurisdiction Programs

- 4.3.2 IP Leakage Risk in Shared Design and Tooling Environments

- 4.3.3 Long Qualification Cycles for High-Risk and Class III Devices

- 4.3.4 Capacity Bottlenecks in Sterile, Cleanroom, and Specialized Assembly

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Diagnostics

- 5.1.2 Therapeutics

- 5.1.3 Drug-Device Combination Products

- 5.2 By Service

- 5.2.1 Contract Development

- 5.2.1.1 Product Design and Development Services

- 5.2.1.2 Testing and Validation

- 5.2.1.3 Quality Management

- 5.2.1.4 Others

- 5.2.2 Contract Manufacturing

- 5.2.2.1 Accessories Manufacturing

- 5.2.2.2 Assembly Manufacturing

- 5.2.2.3 Component Manufacturing

- 5.2.2.4 Device Manufacturing

- 5.2.3 Packaging

- 5.2.4 Regulatory Affairs

- 5.2.1 Contract Development

- 5.3 By Device Class

- 5.3.1 Class I

- 5.3.2 Class II

- 5.3.3 Class III

- 5.4 By Application

- 5.4.1 Cardiovascular Devices

- 5.4.2 Orthopedic Devices

- 5.4.3 Ophthalmic Devices

- 5.4.4 Diagnostic Devices

- 5.4.5 Respiratory Devices

- 5.4.6 Surgical Instruments

- 5.4.7 Dental

- 5.4.8 Others

- 5.5 By End Use

- 5.5.1 Original Equipment Manufacturers

- 5.5.2 Pharmaceutical and Biopharmaceutical Companies

- 5.5.3 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Benchmark Electronics, Inc.

- 6.3.2 Celestica Inc.

- 6.3.3 Cogmedix, Inc.

- 6.3.4 Flex Ltd.

- 6.3.5 Gerresheimer AG

- 6.3.6 Integer Holdings Corporation

- 6.3.7 Jabil Inc.

- 6.3.8 Kimball Electronics, Inc.

- 6.3.9 Mack Molding Co., Inc.

- 6.3.10 Nipro Corporation

- 6.3.11 Nortech Systems, Inc.

- 6.3.12 Phillips-Medisize Corporation

- 6.3.13 Plexus Corp.

- 6.3.14 Recipharm AB

- 6.3.15 Sanmina Corporation

- 6.3.16 Synecco Ltd

- 6.3.17 Stryker Corporation

- 6.3.18 TE Connectivity Ltd.

- 6.3.19 Thermo Fisher Scientific Inc.

- 6.3.20 Viant Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment