|

시장보고서

상품코드

2073084

반추동물용 사료 첨가제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Ruminant Feed Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

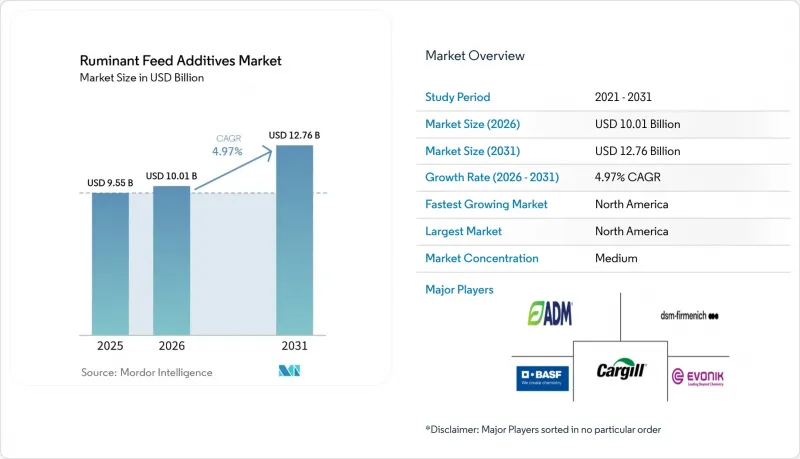

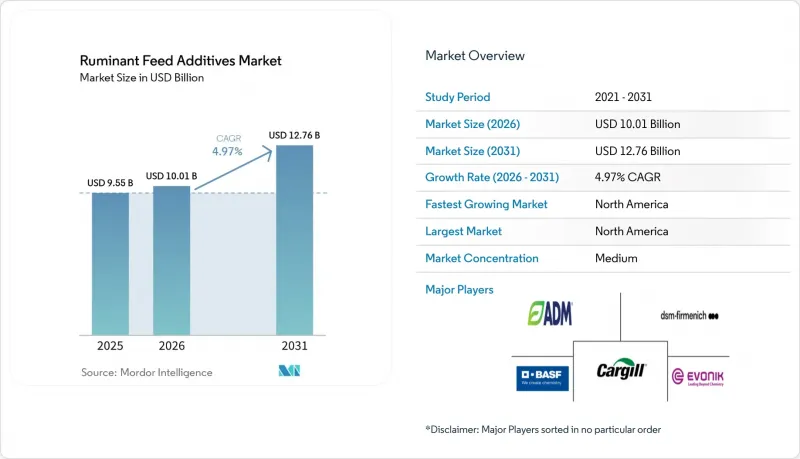

Mordor Intelligence에 의하면, 반추동물용 사료 첨가제 시장 규모는 2025년에 95억 5,000만 달러로 평가되었고 2026년 100억 1,000만 달러에서 2031년까지 127억 6,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 4.97%를 나타낼 전망입니다.

본 보고서는 첨가제별(산미제, 아미노산, 항생제, 항산화제, 미네랄, 결합제, 효소, 기타), 가축별(육우, 젖소, 기타 반추동물), 지역별(아프리카, 아시아태평양, 유럽, 중동, 북미, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러)과 수량(톤)으로 제시되어 있습니다.

세계 반추동물용 사료 첨가제 시장 동향과 인사이트

유제품 및 육류 생산성 향상에 대한 수요 증가

반추동물용 사료 첨가제 시장은 상업용 소 사육군에서 우유 생산량, 우유 고형분 함량, 성장률, 사료 전환율 향상이라는 수요에 힘입어 계속해서 가장 안정적인 지지를 얻고 있습니다. 올텍(Alltech)사의 보고서에 따르면, 2025년 전 세계 혼합사료 생산량은 14억 4,000만 톤을 넘어설 것으로 예상되며, 반추동물용 사료는 특수 첨가제가 표준 배합보다 톤당 더 높은 부가가치를 제공하는 부문 중 하나로 자리매김하고 있습니다. 낙농 시스템에서는 고생산형 젖소의 유전적 개량을 통해 사료가 공급할 수 있는 영양소와 동물이 필요로 하는 영양소 간의 격차가 줄어들고 있으며, 보호 아미노산, 미네랄, 비타민, 루멘 지원 제품에 대한 수요는 견조한 추세를 보이고 있습니다. 또한, 1두당 생산량이 증가하면 생산되는 우유나 육류 1Kg당 배출 강도가 낮아지기 때문에 생산성 목표와 지속가능성 목표 간의 연관성도 점점 더 강해지고 있습니다. 이러한 시너지 효과로 인해 프리미엄 영양 프로그램의 역할이 강화되었으며, 반추동물용 사료 첨가제 시장은 단기적인 사료 주기뿐만 아니라 구조적인 효율화 목표와도 밀접하게 연계된 상태를 유지하고 있습니다.

항생제 무사용 생산이 기능성 첨가물에 대한 수요를 촉진하고 있습니다.

반추동물용 사료 첨가제 시장은 젖소와 육우 생산 현장에서 항생제를 사용하지 않는 생산 시스템으로의 전환이 진행되고 있는 데 힘입어 호황을 누리고 있습니다. 항생제계 성장 촉진제의 사용 중단 및 엄격한 제한에 따라, 생산자들은 소화 기능, 장내 환경, 면역력, 안정적인 생산 성능을 뒷받침할 대체 방안을 모색하고 있습니다. 『Journal of Advanced Research』지에 게재된 2025년 메타분석에 따르면, 항생제가 포함되지 않은 사료 첨가제의 조합은 다양한 가축 종에서 성장 성적과 면역 기능에 통계적으로 유의미한 개선을 가져왔습니다고 보고되었습니다. 이러한 추세에 따라 시판되는 반추동물용 사료에서 프로바이오틱스, 프리바이오틱스, 피토제닉, 효소, 산 생성제, 다성분 배합제의 사용이 증가하고 있습니다. 이러한 변화는 주목할 만합니다. 생산자들은 단일 성분을 다른 단일 성분으로 대체하는 방식에서 벗어나, 여러 가지 기능적 작용기전을 결합한 통합적인 프로그램을 채택하고 있기 때문입니다. 이러한 접근 방식에 따라 많은 대규모 사육 군에서 개체당 평균 지출이 증가하고 있으며, 반추동물용 사료 첨가제 시장은 기본적인 미네랄 및 비타민 공급이라는 범위를 넘어 발전하고 있습니다.

특수 첨가제의 높은 비용과 기존 프리믹스와의 비교

반추동물용 사료 첨가제 시장에서 특수 제품과 기존 미네랄·비타민 프리믹스를 비교할 때, 여전히 뚜렷한 가격 장벽이 존재합니다. 에보닉 인더스트리즈는 2026년 3월, MetAMINO의 전 세계 순가격을 10% 인상한다고 발표했습니다. 이는 보호 아미노산 및 합성 영양 부문이 여전히 생산 비용 압박에 시달리고 있음을 보여줍니다. 소규모 농업 종사자나 준상업적 생산 시스템의 경우, 사료 예산이 빠듯하고 개체별 생산 효과를 측정하기 어렵기 때문에 이러한 가격 차이가 더 큰 문제가 됩니다. 이러한 생산 체계 하에서는 특수 배합을 통해 생산성이 향상되는 것으로 확인되더라도, 생산자들은 더 단순한 프리믹스를 계속 사용하는 경우가 많습니다. 상업적인 과제는 가격이 적정한지 여부뿐만 아니라, 특히 자문 지원이 제한적인 경우 농장 차원에서의 가치 입증에도 있습니다. 즉, 비용에 민감한 지역에서 반추동물용 사료 첨가제 시장이 더욱 빠르게 성장하기 위해서는 공급업체가 고부가가치 제품과 실용적인 서비스, 보다 명확한 효과 측정 지표, 구하기 쉬운 포장을 결합해야 합니다.

부문별 분석

2025년, 아미노산은 반추동물용 사료 첨가제 시장 점유율의 20.7%를 차지하며, 이 산업에서 가장 큰 첨가제 부문이 되었습니다. 이러한 우위는 단백질 균형이 치밀하게 관리되는 고생산성 젖소의 사료 배합에서 루멘 보호형 라이신과 메티오닌이 일관되게 사용되고 있음을 반영합니다. 이 카테고리의 주요 제품으로는 에보닉 인더스트리즈 AG의 ‘메프론”, 아디세오 프랑스 SAS의 “스마트아민”와 “메타스마트”, 아지노모토 주식회사의 “아지프로-L” 등이 있습니다. 또한, 비타민, 프로바이오틱스, 피토제닉은 건강의 안정화를 촉진하고 신진대사를 지원하며, 다양한 가축 사육 시스템에서 항생제를 사용하지 않는 사료 공급을 가능하게 하는 역할을 수행하고 있어 중요한 위치를 차지하고 있습니다. 카테고리 구성의 변화는 반추동물용 사료 첨가제 시장이 단순히 광범위하게 배합되는 제품뿐만 아니라, 특정 생산성이나 건강상의 성과를 지원하도록 설계된 원료에 의해 점점 더 주도되고 있음을 보여줍니다.

산도 조절제는 2031년까지의 기간 동안 반추동물용 사료 첨가제 시장에서 각 첨가제 유형 중 가장 높은 연평균 성장률(CAGR)인 5.8%를 기록하며 성장할 것으로 전망됩니다. 이러한 성장은 항생제를 사용하지 않는 사료 배합 방식을 도입하고, 장내 환경을 개선하며 초기 소화기 계통의 스트레스를 완화하기 위한 송아지용 스타터 프로그램의 활용을 확대한 데 기인합니다. 산 첨가제가 혼합된 제품은 위생 관리와 루멘 적응이라는 두 가지 이점으로 인해 인기가 높아지고 있으며, 생산 주기의 다양한 단계에서 그 가치를 발휘하고 있습니다. 또한, 기후 변화가 사료의 품질에 영향을 미치고, 첨단 사료 공급 시스템을 통해 소화율 향상을 보다 정확하게 정량화할 수 있게 됨에 따라, 미코톡신 관리와 효소 사용의 중요성이 커지고 있습니다. 그 결과, 산업은 단일 용도의 원료에서 다기능 제품 포트폴리오로 전환되고 있습니다. 이러한 추세에 따라 더욱 폭넓은 프리미엄 제품 라인업 개발이 촉진되고 있으며, 성장은 건강, 정밀 사료 공급, 지속가능성 목표에 부합하는 카테고리에 점점 더 집중되고 있습니다.

지역별 분석

북미는 2025년 반추동물용 사료 첨가제 시장 점유율의 38.0%를 차지하고 있으며, 2031년까지 지역별 가장 높은 연평균 성장률(CAGR)인 6.1%로 성장할 것으로 전망됩니다. 성숙한 지역으로서는 이례적인 리더십이지만, 이는 반추동물용 사료 첨가제 시장의 구조와 부합합니다. 북미에는 대규모 낙농장, 대규모 비육장, 높은 첨가제 보급률, 특수 제품에 대한 높은 수용성이 복합적으로 작용하고 있기 때문입니다. 미국이 그 수요의 대부분을 주도하고 있는데, 이는 소 사육 규모, 상업적 영양 서비스, 환경에 가해지는 부담과 같은 요소들이 모두 같은 방향으로 작용하고 있기 때문입니다. 캐나다는 조직화된 낙농 시스템과 규제 체계가 특수 첨가물의 도입을 뒷받침하고 있어, 이 지역에 더욱 깊은 의미를 더하고 있습니다. 멕시코는 낙농 및 육우 사육 사업이 더욱 상업화되고, 정식 프리믹스 공급과의 연계가 강화되고 있어 여전히 중요한 성장 거점으로 자리 잡고 있습니다. 이러한 상황으로 인해 북미는 반추동물용 사료 첨가제 시장에서 가장 규모가 크고 가장 빠르게 성장하는 지역으로서 이중의 역할을 계속해서 수행하고 있습니다.

아시아태평양은 두 번째로 큰 지역 시장입니다. 중국, 인도, 호주는 대규모 가축 사육 두수와 생산량 확대, 현대화, 정규 사료 사용 증가와 같은 꾸준한 성장 요인에 힘입어 수요를 주도하고 있습니다. 2025년 8월, DSM-Firmenich는 인도 자드체르라에 새로운 동물 영양·건강 공장을 설립하고, 해당 지역을 위해 “Mycofix”를 현지에서 생산할 수 있는 체제를 구축했습니다. 이는 장기적인 수요와 현지화된 공급망이 가져다주는 이점에 대한 해당 회사의 확신을 보여주는 것입니다. 이 지역은 반추동물용 사료 첨가제 시장에서 중요한 역할을 하고 있습니다. 동물성 단백질 소비 증가와 가축 사육의 현대화로 인해, 첨단 낙농 시스템에 그치지 않고 상업적 기반이 확대되고 있기 때문입니다. 도입 현황은 농장 규모에 따라 다르지만, 체계적인 생산이 확대되고 더 많은 생산자들이 기본적인 보충제에서 기능성 영양 프로그램으로 전환하고 있는 만큼, 전반적인 추세는 호조를 보이고 있습니다.

유럽에서는 사료의 안전성, 동물 건강, 환경 성능에 관한 엄격한 규제를 배경으로 꾸준한 성장이 예상됩니다. 이러한 요인들로 인해 유럽은 프리미엄 사료 첨가제의 주요 시장이 되었습니다. 규제를 준수하기 위해서는 견고한 기술 지원과 입증된 효능을 갖춘 제품이 요구되는 경우가 많기 때문입니다. 남미 역시 브라질과 아르헨티나를 필두로 꾸준한 성장이 예상됩니다. 이 국가들에서는 수출 지향적인 쇠고기 및 유우 생산 시스템이 효율성과 규모 확대를 촉진하고 있습니다. 중동 및 아프리카는 인프라 부족이나 높은 수입 의존도 등의 과제에 직면해 있지만, 완만한 속도로 성장할 것으로 전망됩니다. 다만, 이들 지역 중 일부의 낙농 및 비육 클러스터는 서서히 발전하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the ruminant feed additives market size was valued at USD 9.55 billion in 2025 and is projected to grow from USD 10.01 billion in 2026 to reach USD 12.76 billion by 2031, at a CAGR of 4.97% during the forecast period (2026-2031).

This report is Segmented by Additive (Acidifiers, Amino Acids, Antibiotics, Antioxidants, Minerals, Binders, Enzymes, and More), by Animal (Beef Cattle, Dairy Cattle, and Other Ruminants), and by Geography (Africa, Asia-Pacific, Europe, Middle East, North America, and South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Global Ruminant Feed Additives Market Trends and Insights

Rising Demand for Milk and Meat Productivity Gains

The ruminant feed additives market continues to draw its most stable support from the need to improve milk yield, milk solids, growth rates, and feed conversion in commercial herds. Alltech reported that global compound feed production exceeded 1.44 billion metric tons in 2025, and ruminant feed remains one of the areas where specialty additives offer a higher value per ton than standard formulations . In dairy systems, higher-yielding genetics narrow the nutritional gap between what forage can supply and what the animal needs, keeping demand firm for protected amino acids, minerals, vitamins, and rumen support products. Productivity targets are also becoming more closely linked to sustainability targets because higher output per animal lowers the emissions intensity of each kilogram of milk or meat produced. That combination reinforces the role of premium nutrition programs and keeps the ruminant feed additives market tied to structural efficiency goals rather than short-term feed cycles alone.

Antibiotic-Free Production Shifting Demand Toward Functional Additives

The ruminant feed additives market is benefiting from the growing shift toward antibiotic-free production systems in both dairy and beef operations. With the removal or strict limitation of antibiotic growth promoters, producers are seeking alternative solutions to support digestion, gut health, immunity, and consistent performance. A 2025 meta-analysis published in the Journal of Advanced Research reported that non-antibiotic feed additive combinations resulted in statistically significant improvements in livestock growth performance and immune function across various species. This trend is driving increased use of probiotics, prebiotics, phytogenics, enzymes, acidifiers, and multi-component formulations in commercial ruminant diets. The shift is notable as producers are moving away from replacing single ingredients with another single ingredient, instead adopting integrated programs that combine multiple functional modes of action. This approach is increasing the average expenditure per animal in many organized herds and is steering the ruminant feed additives market beyond basic mineral and vitamin supplementation.

High Cost of Specialty Additives Versus Conventional Premixes

The ruminant feed additives market still faces a clear price barrier when specialty products are compared with conventional mineral and vitamin premixes. Evonik Industries AG announced a 10% global net price increase for MetAMINO in March 2026, indicating that protected amino acids and synthetic nutrition remain exposed to production pressures. In smallholder and semi-commercial systems, that price gap matters more because feed budgets are tighter and product returns are harder to measure on an animal-by-animal basis. Producers in those systems often stay with simpler premixes even when performance benefits from specialty formulations are known. The commercial issue is not only affordability, but also proof of value at the farm level, especially where advisory support is limited. This means the ruminant feed additives market can grow faster in cost-sensitive regions only when suppliers pair higher-value products with practical service, clearer response metrics, and more accessible packaging.

Other drivers and restraints analyzed in the detailed report include:

- Methane-Reduction Economics Improving Return on Specialty Additives

- Growth of Young Animal Nutrition Programs in Commercial Herds

- Slower Commercial Adoption Outside Large-Scale Herds

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Amino acids accounted for 20.7% of the ruminant feed additives market share in 2025, making them the largest additive category in the industry. This dominance reflects the consistent use of rumen-protected lysine and methionine in high-producing dairy rations, where protein balance is carefully managed. Key products in this category include Mepron from Evonik Industries AG, Smartamine and MetaSmart from Adisseo France SAS, and AjiPro-L from Ajinomoto Co., Inc. Additionally, vitamins, probiotics, and phytogenics hold significant positions due to their roles in promoting health stability, supporting metabolism, and enabling antibiotic-free feeding practices across diverse herd systems. The evolving category mix indicates that the ruminant feed additives market is increasingly driven by ingredients designed to support specific production or health outcomes, rather than solely by broad inclusion products.

Acidifiers are projected to grow at a compound annual growth rate (CAGR) of 5.8%, the fastest among additive types in the ruminant feed additives market through 2031. This growth is attributed to the adoption of antibiotic-free formulation practices and the increased use of calf starter programs to improve gut health and reduce early digestive stress. Acidifier blends are gaining popularity due to their dual benefits of hygiene control and rumen adaptation, making them valuable across various stages of the production cycle. Additionally, the importance of mycotoxin management and enzyme use is rising as climate variability impacts feed quality and as advanced feeding systems enable better quantification of digestibility improvements. Consequently, the industry is shifting towards multi-functional product portfolios rather than single-purpose ingredients. This trend is driving the development of a broader premium product mix, with growth increasingly focused on categories aligned with health, precision feeding, and sustainability objectives.

Complete Report Scope:

- By Additive

- Acidifiers

- Fumaric Acid

- Lactic Acid

- Propionic Acid

- Other Acidifiers

- Amino Acids

- Lysine

- Methionine

- Threonine

- Tryptophan

- Other Amino Acids

- Antibiotics

- Bacitracin

- Penicillins

- Tetracyclines

- Tylosin

- Other Antibiotics

- Antioxidants

- Butylated Hydroxyanisole (BHA)

- Butylated Hydroxytoluene (BHT)

- Citric Acid

- Ethoxyquin

- Propyl Gallate

- Tocopherols

- Other Antioxidants

- Binders

- Natural Binders

- Synthetic Binders

- Enzymes

- Carbohydrases

- Phytases

- Other Enzymes

- Flavors & Sweeteners

- Flavors

- Sweeteners

- Minerals

- Macrominerals

- Microminerals

- Mycotoxin Detoxifiers

- Binders

- Biotransformers

- Phytogenics

- Essential Oil

- Herbs & Spices

- Other Phytogenics

- Pigments

- Carotenoids

- Curcumin & Spirulina

- Prebiotics

- Fructo Oligosaccharides

- Galacto Oligosaccharides

- Inulin

- Lactulose

- Mannan Oligosaccharides

- Xylo Oligosaccharides

- Other Prebiotics

- Probiotics

- Bifidobacteria

- Enterococcus

- Lactobacilli

- Pediococcus

- Streptococcus

- Other Probiotics

- Vitamins

- Vitamin A

- Vitamin B

- Vitamin C

- Vitamin E

- Other Vitamins

- Yeast

- Live Yeast

- Selenium Yeast

- Spent Yeast

- Torula Dried Yeast

- Whey Yeast

- Yeast Derivatives

- Acidifiers

- By Animal

- Beef Cattle

- Dairy Cattle

- Other Ruminants

- By Geography

- Africa

- Egypt

- Kenya

- South Africa

- Rest of Africa

- Asia-Pacific

- Australia

- China

- India

- Indonesia

- Japan

- Philippines

- South Korea

- Thailand

- Vietnam

- Rest of Asia-Pacific

- Europe

- France

- Germany

- Italy

- Netherlands

- Russia

- Spain

- Turkey

- United Kingdom

- Rest of Europe

- Middle East

- Iran

- Saudi Arabia

- Rest of Middle East

- North America

- Canada

- Mexico

- United States

- Rest of North America

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Africa

Geography Analysis

North America held 38.0% of the ruminant feed additives market share in 2025 and is also projected to grow with the fastest regional CAGR of 6.1% through 2031. That leadership is unusual for a mature region, but it aligns with the structure of the ruminant feed additives market, as North America combines large dairy farms, large feedlots, high additive penetration, and greater readiness for specialty products. The United States drives most of that demand because herd scale, commercial nutrition services, and environmental pressure have all moved in the same direction. Canada adds further depth to the region, as organized dairy systems and regulatory development support the adoption of specialty additives. Mexico remains an important growth pocket because dairy and beef operations are becoming more commercial and more connected to formal premix supply. These conditions keep North America in a dual role as the largest and fastest-growing regional contributor to the ruminant feed additives market.

Asia-Pacific is the second-largest regional market. China, India, and Australia drive demand due to their large herd bases and steady growth factors, including output expansion, modernization, and increased use of formal feed. In August 2025, DSM-Firmenich inaugurated a new Animal Nutrition and Health plant in Jadcherla, India, to locally produce Mycofix for the region, demonstrating confidence in long-term demand and the benefits of a localized supply chain. The region plays a significant role in the ruminant feed additives market, as rising animal protein consumption and herd modernization are expanding the commercial base beyond advanced dairy systems. While adoption varies across farm sizes, the overall trend is positive, with organized production growing and more producers transitioning from basic supplementation to functional nutrition programs.

Europe is projected to grow steadily, driven by stringent regulations on feed safety, animal health, and environmental performance. These factors make Europe a key market for premium additives, as compliance often requires products with robust technical support and proven efficacy. South America is also projected to experience steady growth, led by Brazil and Argentina, where export-oriented beef and dairy systems are enhancing efficiency and scale. Africa and the Middle East are projected to grow at a moderate pace, though both regions face challenges such as limited infrastructure and higher import dependency. However, selected dairy and feedlot clusters in these regions are gradually developing.

- Cargill, Incorporated

- Archer Daniels Midland Company

- DSM-Firmenich

- Evonik Industries AG

- BASF SE

- Alltech, Inc.

- Nutreco N.V.

- Adisseo France SAS

- Kemin Industries, Inc.

- Ajinomoto Co., Inc.

- Novonesis

- Lallemand Inc.

- Zinpro Corporation

- Elanco Animal Health Incorporated

- FutureFeed

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for milk and meat productivity gains

- 4.2.2 Antibiotic-free production shifting demand toward functional additives

- 4.2.3 Methane-reduction economics improving return on specialty additives

- 4.2.4 Expansion of precision feeding in dairy and feedlot operations

- 4.2.5 Growth of young animal nutrition programs in commercial herds

- 4.2.6 Rising use of rumen health and microbiome modulation solutions

- 4.3 Market Restraints

- 4.3.1 High cost of specialty additives versus conventional premixes

- 4.3.2 Feed ingredient price volatility compressing formulator margins

- 4.3.3 Slower commercial adoption outside large-scale herds

- 4.3.4 Lengthy approval and labeling requirements for novel actives

- 4.4 Technological Outlook

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Additive

- 5.1.1 Acidifiers

- 5.1.1.1 Fumaric Acid

- 5.1.1.2 Lactic Acid

- 5.1.1.3 Propionic Acid

- 5.1.1.4 Other Acidifiers

- 5.1.2 Amino Acids

- 5.1.2.1 Lysine

- 5.1.2.2 Methionine

- 5.1.2.3 Threonine

- 5.1.2.4 Tryptophan

- 5.1.2.5 Other Amino Acids

- 5.1.3 Antibiotics

- 5.1.3.1 Bacitracin

- 5.1.3.2 Penicillins

- 5.1.3.3 Tetracyclines

- 5.1.3.4 Tylosin

- 5.1.3.5 Other Antibiotics

- 5.1.4 Antioxidants

- 5.1.4.1 Butylated Hydroxyanisole (BHA)

- 5.1.4.2 Butylated Hydroxytoluene (BHT)

- 5.1.4.3 Citric Acid

- 5.1.4.4 Ethoxyquin

- 5.1.4.5 Propyl Gallate

- 5.1.4.6 Tocopherols

- 5.1.4.7 Other Antioxidants

- 5.1.5 Binders

- 5.1.5.1 Natural Binders

- 5.1.5.2 Synthetic Binders

- 5.1.6 Enzymes

- 5.1.6.1 Carbohydrases

- 5.1.6.2 Phytases

- 5.1.6.3 Other Enzymes

- 5.1.7 Flavors & Sweeteners

- 5.1.7.1 Flavors

- 5.1.7.2 Sweeteners

- 5.1.8 Minerals

- 5.1.8.1 Macrominerals

- 5.1.8.2 Microminerals

- 5.1.9 Mycotoxin Detoxifiers

- 5.1.9.1 Binders

- 5.1.9.2 Biotransformers

- 5.1.10 Phytogenics

- 5.1.10.1 Essential Oil

- 5.1.10.2 Herbs & Spices

- 5.1.10.3 Other Phytogenics

- 5.1.11 Pigments

- 5.1.11.1 Carotenoids

- 5.1.11.2 Curcumin & Spirulina

- 5.1.12 Prebiotics

- 5.1.12.1 Fructo Oligosaccharides

- 5.1.12.2 Galacto Oligosaccharides

- 5.1.12.3 Inulin

- 5.1.12.4 Lactulose

- 5.1.12.5 Mannan Oligosaccharides

- 5.1.12.6 Xylo Oligosaccharides

- 5.1.12.7 Other Prebiotics

- 5.1.13 Probiotics

- 5.1.13.1 Bifidobacteria

- 5.1.13.2 Enterococcus

- 5.1.13.3 Lactobacilli

- 5.1.13.4 Pediococcus

- 5.1.13.5 Streptococcus

- 5.1.13.6 Other Probiotics

- 5.1.14 Vitamins

- 5.1.14.1 Vitamin A

- 5.1.14.2 Vitamin B

- 5.1.14.3 Vitamin C

- 5.1.14.4 Vitamin E

- 5.1.14.5 Other Vitamins

- 5.1.15 Yeast

- 5.1.15.1 Live Yeast

- 5.1.15.2 Selenium Yeast

- 5.1.15.3 Spent Yeast

- 5.1.15.4 Torula Dried Yeast

- 5.1.15.5 Whey Yeast

- 5.1.15.6 Yeast Derivatives

- 5.1.1 Acidifiers

- 5.2 By Animal

- 5.2.1 Beef Cattle

- 5.2.2 Dairy Cattle

- 5.2.3 Other Ruminants

- 5.3 By Geography

- 5.3.1 Africa

- 5.3.1.1 Egypt

- 5.3.1.2 Kenya

- 5.3.1.3 South Africa

- 5.3.1.4 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 Australia

- 5.3.2.2 China

- 5.3.2.3 India

- 5.3.2.4 Indonesia

- 5.3.2.5 Japan

- 5.3.2.6 Philippines

- 5.3.2.7 South Korea

- 5.3.2.8 Thailand

- 5.3.2.9 Vietnam

- 5.3.2.10 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 France

- 5.3.3.2 Germany

- 5.3.3.3 Italy

- 5.3.3.4 Netherlands

- 5.3.3.5 Russia

- 5.3.3.6 Spain

- 5.3.3.7 Turkey

- 5.3.3.8 United Kingdom

- 5.3.3.9 Rest of Europe

- 5.3.4 Middle East

- 5.3.4.1 Iran

- 5.3.4.2 Saudi Arabia

- 5.3.4.3 Rest of Middle East

- 5.3.5 North America

- 5.3.5.1 Canada

- 5.3.5.2 Mexico

- 5.3.5.3 United States

- 5.3.5.4 Rest of North America

- 5.3.6 South America

- 5.3.6.1 Argentina

- 5.3.6.2 Brazil

- 5.3.6.3 Chile

- 5.3.6.4 Rest of South America

- 5.3.1 Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Cargill, Incorporated

- 6.4.2 Archer Daniels Midland Company

- 6.4.3 DSM-Firmenich

- 6.4.4 Evonik Industries AG

- 6.4.5 BASF SE

- 6.4.6 Alltech, Inc.

- 6.4.7 Nutreco N.V.

- 6.4.8 Adisseo France SAS

- 6.4.9 Kemin Industries, Inc.

- 6.4.10 Ajinomoto Co., Inc.

- 6.4.11 Novonesis

- 6.4.12 Lallemand Inc.

- 6.4.13 Zinpro Corporation

- 6.4.14 Elanco Animal Health Incorporated

- 6.4.15 FutureFeed