|

시장보고서

상품코드

2073086

경카테터 심장판막 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Transcatheter Heart Valve - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

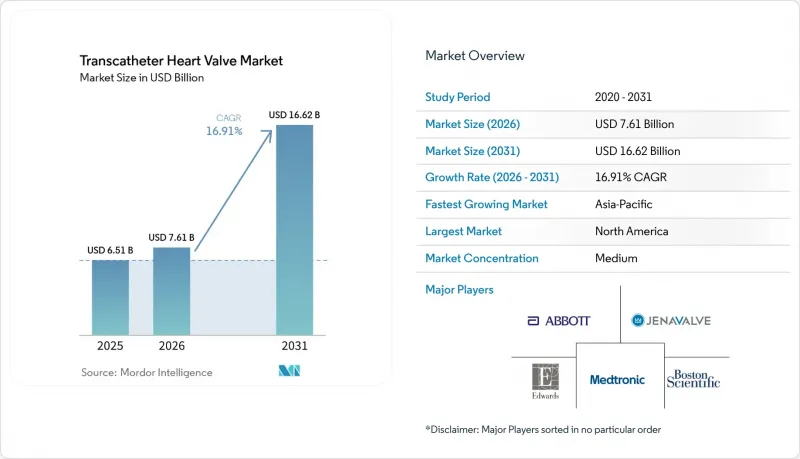

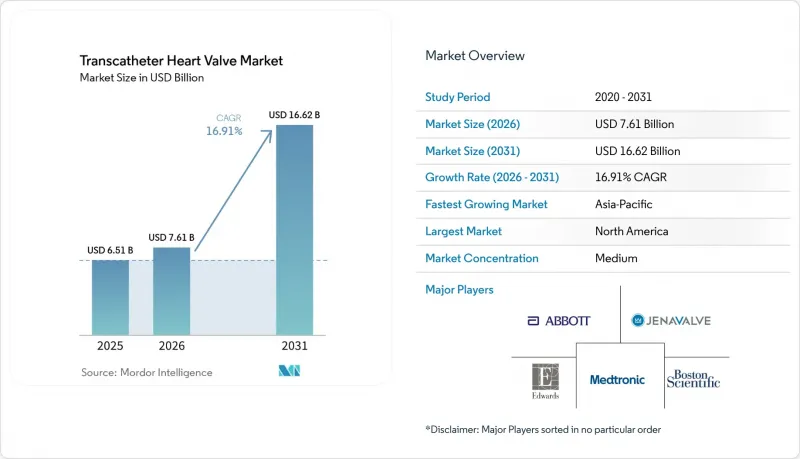

Mordor Intelligence에 의하면, 경카테터 심장판막 시장 규모는 2025년에 65억 1,000만 달러로 평가되었고 2026년 76억 1,000만 달러에서 2031년까지 166억 2,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 16.91%를 나타낼 전망입니다.

본 보고서는 제품 유형(경카테터 대동맥판막, 경카테터 승모판막, 기타), 판막 기술(풍선 확장형 판막, 기타), 전달 경로(대퇴동맥 경로, 심첨부 경로, 심실중격 경로, 경정맥 경로), 최종 사용자(병원, 외래수술센터(ASC), 기타), 지역(북미, 유럽, 아시아태평양, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 경카테터 심장판막 시장 동향 및 인사이트

고령화와 중증 대동맥판막 협착증으로 인한 부담 증가

경카테터 심장판막 시장은 고령화에 따른 중증 대동맥판막협착증 유병률 증가의 혜택을 받고 있습니다. 이 질환의 발병률은 나이가 들면서 급격히 증가하기 때문에 치료 수요를 이끌고 있습니다. 임상적 논의는 안전성 단계를 넘어, 7년에 걸친 PARTNER 3 추적 조사 결과, 저위험 환자군에서 경카테터 판막 치환술과 외과적 판막 치환술 간에 전사인 사망률이나 신체 장애를 동반하는 뇌졸중 발생률에 유의미한 차이는 나타나지 않았습니다. 이를 통해 조기 진료를 장려하고, 의사에 대한 신뢰를 높이며, 복잡하고 치료비가 많이 드는 상태를 예방하기 위한 적시 치료의 중요성이 강조되고 있습니다. 체계적인 심장 질환 추적 시스템을 갖춘 국가들의 전국 등록 제도는 병원과 보험사에 명확한 치료 성과 증거를 제공함으로써, 임상 현장에서의 도입을 더욱 가속화하고 있습니다. 이처럼 시장은 고령화의 진행과 중증 판막 질환에 대한 보다 확실한 치료 경로에 힘입어 성장하고 있습니다.

저위험 환자군으로의 확대

경카테터 심장판막 시술 시장은 치료 대상이 고위험 수술 적응증 환자를 넘어, 더 낮은 위험군으로 확대됨에 따라 성장하고 있습니다. 2025년 메타분석에서는 경카테터 대동맥판막 치환술(TAVR)을 받은 젊은 연령대의 저위험 환자에서 사망이나 장애를 동반하는 뇌졸중 측면에서 외과 수술과 동등한 결과가 나타났을 뿐만 아니라, 심기능 분류 및 삶의 질(QOL)의 개선도 확인되었다는 점이 강조되었습니다. “Evolut Low Risk”검사의 5년 추적 결과에 따르면, TAVR의 모든 원인에 의한 사망률은 15.5%, 외과 수술의 경우 16.4%로 나타났으며, 이에 따라 TAVR의 보다 광범위한 활용에 대한 거부감이 점차 줄어들고 있습니다. 이러한 근거는 치료 건수를 외과 수술에서 카테터 치료로 전환할 뿐만 아니라, 대상 환자층을 확대하고 조기 개입을 가능하게 함으로써 시장 성장을 주도하고 있습니다.

청소년 환자의 평생 관리에 대한 우려

경카테터 심장판막 시장은 첫 이식 후 평생에 걸친 관리상의 과제가 아직 해결되지 않아, 젊은 환자들에게는 한계에 직면해 있습니다. 2025년, 미국 흉부외과학회(Society of Thoracic Surgeons)는 특히 수술을 통해 합병증 발생률을 낮게 억제할 수 있고, 향후 중재 시술을 위한 계획을 수립하기 쉬운 경우, 젊은 환자에게는 외과적 대동맥판막 치환술을 우선적인 선택지로 권장했습니다. 이는 60대 중반의 환자가 많은 최신 기기에 대해 현재 이용 가능한 근거의 유효 기간을 초과하여 생존할 가능성이 있다는 우려를 부각시키고 있습니다. 또한, 밸브 인 밸브 시술은 첫 번째 인공판막 삽입 후 관상동맥에 접근하거나 향후 재시술을 수행하는 것을 복잡하게 만듭니다. 기술의 발전에도 불구하고, 보수적인 심장 의료진은 연령, 해부학적 특징, 장기적인 재시술 전략을 우선시할 것으로 예상되며, 이는 젊은 환자층에서 경카테터 심장판막 시술의 도입을 지연시키는 요인이 될 것으로 보입니다.

부문별 분석

2025년, 경카테터 대동맥판막은 경카테터 심장판막 시장의 61.67%를 차지하고 있으며, 이는 확고한 임상 실적, 의료진의 높은 숙련도, 중증 대동맥판막 협착증에 대한 확립된 TAVR 프로토콜에 힘입어 해당 제품이 확고한 입지를 차지하고 있음을 반영합니다. 대동맥 분야는 주요 플랫폼 간의 치열한 경쟁의 혜택을 누리고 있으며, 이는 첨단 심장 센터에서의 혁신과 시술에 대한 신뢰를 촉진하고 있습니다. 폐동맥 및 삼첨판용 제품은 매출 규모는 작지만, 기존 외과적 치료만으로는 충분히 충족되지 않았던 환자들의 중요한 요구를 충족시키고 있습니다. 에드워즈사는 2026년 3월, EVOQUE 시스템에 대해 환자에게 지속적인 이점과 사망률 감소를 입증한 2년간의 TRISCEND II 데이터를 발표하며, 삼첨판 부문을 강화했습니다. 이로 인해 의사들 사이에서 이 기술이 더욱 널리 채택되고 있습니다.

경카테터 승모판 치환술은 2031년까지 연평균 성장률(CAGR) 18.90%를 나타낼 것으로 예측되며, 경카테터 심장판막 시장에서 중요한 성장 부문으로 자리매김하고 있습니다. 2025년 5월, 애보트사의 “Tendyne”가 FDA 승인을 획득함에 따라, 외과적 치료 옵션이 없는 환자를 위한 저침습성 승모판 치환술이 도입되었습니다. 이에 이어, 에드워즈사는 2025년 12월에 “SAPIEN M3”에 대한 FDA 승인을 획득하여, 외과적 치료가 적합하지 않은 환자를 대상으로 중등도에서 중증의 승모판 역류증에 대한 경중격 치료를 제공했습니다.

2025년에는 메드트로닉사의 ‘Evolut” 플랫폼과 애보트사의 “Navitor”시스템에 힘입어, 자가팽창형 밸브가 63.91%의 점유율로 시장을 주도했습니다. 이 제품들의 장점은 카테터 통과 프로파일이 작아 해부학적 문제가 있는 사례에도 적용할 수 있다는 점에 있으며, 이는 수년간의 시술자 경험을 통해 입증되었습니다. 그러나 관심은 초기 편의성보다는 장기적인 성능 쪽으로 점차 옮겨가고 있습니다. 에드워즈사는 2026년 1분기 세계 TAVR 시장에서 자사의 입지가 소폭 개선되었다고 보고했습니다. 이것은 메드트로닉사의 ‘에볼루트”에 관한 재개입률을 둘러싼 논의도 한 원인이 되고 있습니다.

벌룬 확장형 밸브 시장은 2031년까지 연평균 성장률(CAGR) 19.25%를 나타낼 것으로 예측되며, 이는 시장 역학의 변화를 시사합니다. 이러한 성장은 에드워즈사의 “SAPIEN” 시리즈와 생체 판막의 동작을 모방한 차세대 설계에 힘입어 발전하고 있습니다. 안테리스 테크놀로지스는 “DurAVR”로 시장에 진출했으며, FDA는 2025년 11월에 “PARADIGM”의 피보탈 임상시험을 승인했습니다. 이 플랫폼은 내구성과 혈역학적 문제에 대한 우려를 해소함으로써 의료진의 지지를 얻고 있습니다. 시장은 플랫폼에 익숙해짐에 따라, 밸브의 장기적인 성능과 구조적 내구성에 대한 관심으로 점차 옮겨가고 있습니다.

지역별 분석

2025년, 북미는 경카테터 심장판막 시장의 42.55%를 차지하며, 지역별 최대 기여 지역으로서의 위상을 유지했습니다. 이 지역은 성숙한 보험 환급 제도, 탄탄한 중재적 심장학 기반, 그리고 첨단 심장 센터로 구성된 광범위한 네트워크의 혜택을 누리고 있습니다. 미국은 여전히 매우 중요한 역할을 수행하고 있으며, 보험 적용 범위와 등록 요건으로 인해 치료는 고도의 의료 역량을 갖춘 병원 시스템에 집중되어 있습니다.

유럽은 독일, 프랑스, 영국, 이탈리아, 스페인에서 시행되고 있는 일관된 상환 정책과 구조적 심장 질환 프로그램의 견고한 기반에 힘입어, 경카테터 심장판막 시장에 계속해서 안정적인 기여를 하고 있습니다. TAVR 분야에서 의사들이 수년에 걸쳐 축적한 전문 지식을 바탕으로, 성숙하고 표준화된 시술 절차가 확립되어 있습니다. 대형 제조업체는 규제 및 규정 준수 요건을 효과적으로 관리하고, 공급의 지속성과 시장 점유율을 확보할 수 있다는 점에서 우위를 점하고 있습니다. 도입 시기가 비교적 최근인 지역에 비해 성장 속도는 완만하지만, 유럽은 여전히 신뢰할 수 있는 판매량 기반을 형성하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 19.22%를 기록하며 성장할 것으로 예상되며, 경카테터 심장판막 시장에서 가장 빠른 성장세를 보일 것으로 전망됩니다. 중국 내 승인 절차가 진전됨에 따라, 병원용 제품의 구하기 쉬움과 가격 경쟁력이 향상되고 있습니다. MicroPort의 “VitaFlow Liberty Flex”는 2025년 1월에 NMPA의 승인을 획득했으며, Genesis MedTech의 “J-VALVE TF”(중국 최초의 대동맥판막 역류증 치료용 대퇴동맥 경유 TAVR 시스템)은 2025년 9월에 승인되었습니다.” 일본에서는 국민건강보험이 치료 접근성을 지원하고 있으며, 한국에서는 치료 거점 네트워크 확대를 통해 구조적 심장 질환 치료 체계를 확충하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.07According to Mordor Intelligence, the transcatheter heart valve market size was valued at USD 6.51 billion in 2025 and is estimated to grow from USD 7.61 billion in 2026 to reach USD 16.62 billion by 2031, at a CAGR of 16.91% during the forecast period (2026-2031).

This report is Segmented by Product Type (Transcatheter Aortic Valve, Transcatheter Mitral Valve, and More), Valve Technology (Balloon-Expandable Valves, and More), Delivery Route (Transfemoral, Transapical, Transseptal, Transjugular), End User (Hospitals, Ascs, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Transcatheter Heart Valve Market Trends and Insights

Aging Population and Rising Severe Aortic Stenosis Burden

The transcatheter heart valve market benefits from the increasing prevalence of severe aortic stenosis in aging populations, as disease incidence rises sharply with age, driving procedural demand. Clinical discussions have progressed beyond safety, with findings from the 7-year PARTNER 3 follow-up showing no significant difference in all-cause mortality or disabling stroke between transcatheter and surgical valve replacements in low-risk patients. This supports earlier referrals, enhances physician confidence, and emphasizes timely treatment to prevent complex and costly conditions. National registry systems in countries with organized cardiac tracking further accelerate clinical adoption by providing hospitals and payers with clear outcome evidence. The market is thus supported by aging demographics and a more assured treatment pathway for severe valve diseases.

Expansion Into Lower-Risk Patient Populations

The transcatheter heart valve market is expanding as treatments extend to lower-risk groups beyond high-risk surgical candidates. A 2025 meta-analysis highlighted that younger, low-risk patients undergoing transcatheter aortic valve replacement (TAVR) achieved comparable outcomes in terms of death or disabling stroke compared to surgery, along with improvements in functional class and quality of life. The 5-year Evolut Low Risk results reported 15.5% all-cause mortality for TAVR and 16.4% for surgery, reducing resistance to broader TAVR use. This evidence not only shifts volume from surgery to catheter-based care but also broadens the patient pool, enabling earlier interventions and driving market growth.

Lifetime Management Concerns in Younger Patients

The transcatheter heart valve market faces limitations in younger patients due to unresolved lifetime management challenges after the initial implant. In 2025, the Society of Thoracic Surgeons recommended surgical aortic valve replacement as the preferred option for younger patients, especially when surgery ensures low morbidity and better planning for future interventions. This highlights concerns that patients in their mid-60s may outlive the current evidence available for many modern devices. Additionally, valve-in-valve procedures complicate coronary access and future reinterventions after the first prosthesis placement. Despite advancements, conservative heart teams are expected to prioritize age, anatomy, and long-term reintervention strategies, slowing the adoption of transcatheter heart valves among younger patients.

Other drivers and restraints analyzed in the detailed report include:

- Next-Generation Valve Durability, Repositionability, and Coronary Access Innovation

- Earlier Intervention Enabled by Trial Evidence and Label Expansion

- Reimbursement and Coverage Variability Across Healthcare Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, transcatheter aortic valves held 61.67% of the transcatheter heart valve market, reflecting their strong position driven by a robust clinical history, physician familiarity, and established TAVR protocols for severe aortic stenosis. The aortic segment benefits from intense competition among leading platforms, fostering innovation and procedural confidence in advanced cardiac centers. Pulmonary and tricuspid products, though smaller in revenue, address critical patient needs previously underserved by surgical options. Edwards strengthened the tricuspid segment in March 2026 with 2-year TRISCEND II data showing sustained patient benefits and reduced mortality for the EVOQUE system, supporting broader physician adoption.

Transcatheter mitral valves are projected to grow at an 18.90% CAGR through 2031, marking a significant growth area in the transcatheter heart valve market. Abbott's FDA approval for Tendyne in May 2025 introduced a minimally invasive mitral replacement for patients lacking surgical options. Edwards followed with FDA approval for SAPIEN M3 in December 2025, offering a transseptal treatment for moderate-to-severe mitral regurgitation in non-surgical candidates.

Self-expandable valves led the market with a 63.91% share in 2025, driven by Medtronic's Evolut platform and Abbott's Navitor system. Their appeal lies in a lower crossing profile and adaptability to challenging anatomies, supported by years of operator experience. However, the focus is shifting toward long-term performance over initial convenience. Edwards reported a slight improvement in its global TAVR position in Q1 2026, partly due to discussions around Medtronic's Evolut reintervention profile.

Balloon-expandable valves are expected to grow at a 19.25% CAGR through 2031, signaling a shift in market dynamics. This growth is fueled by Edwards' SAPIEN franchise and next-generation designs mimicking native valve behavior. Anteris Technologies entered the market with DurAVR, and the FDA approved the PARADIGM global pivotal trial in November 2025. The platform addresses durability and hemodynamic concerns, driving physician preference. The market is evolving from platform familiarity to long-term valve performance and structural durability.

Complete Report Scope:

- By Product Type

- Transcatheter Aortic Valve

- Transcatheter Mitral Valve

- Transcatheter Tricuspid Valve

- Transcatheter Pulmonary Valve

- By Valve Technology

- Balloon-Expandable Valves

- Self-Expandable Valves

- Others

- By Delivery Route

- Transfemoral

- Transapical

- Transseptal

- Transjugular

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Cardiac Centers

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America accounted for 42.55% of the transcatheter heart valve market, maintaining its position as the largest regional contributor. The region benefits from mature reimbursement systems, a strong interventional cardiology base, and an extensive network of advanced cardiac centers. The U.S. remains pivotal, with coverage and registry requirements concentrating treatments within highly capable hospital systems.

Europe continues to be a stable contributor to the transcatheter heart valve market, supported by consistent reimbursement policies in Germany, France, the U.K., Italy, and Spain, along with a solid base of structural heart programs. Years of physician expertise in TAVR have ensured mature and standardized procedural pathways. Larger manufacturers hold an advantage due to their ability to manage regulatory and compliance demands effectively, ensuring supply continuity and market coverage. Despite slower growth compared to newer adoption regions, Europe remains a reliable volume base.

Asia-Pacific is projected to grow at a 19.22% CAGR through 2031, marking the fastest expansion in the transcatheter heart valve market. China's improving domestic approvals are enhancing product availability and affordability for hospitals. MicroPort's VitaFlow Liberty Flex received NMPA approval in January 2025, and Genesis MedTech's J-VALVE TF, the first transfemoral TAVR system for aortic regurgitation in China, was approved in September 2025. Japan's national health insurance supports procedural access, while South Korea is expanding structural heart capacity through a broader network of centers.

- 4C Medical Technologies, Inc.

- Abbott Laboratories

- Alterra Medical, Inc.

- Anteris Technologies Ltd.

- Biosensors International Group, Ltd.

- Boston Scientific

- Braile Biomedica Industria, Comercio e Representacoes Ltda.

- CardiaQuest, Inc.

- Cephea Valve Technologies, Inc.

- Edward Lifesciences

- HighLife SAS

- Jenavalve Technology

- Medtronic

- Memryx, Inc.

- Meril Life Science

- MicroPort

- Navigate Medical, Inc.

- Neovasc Inc.

- P and F Products and Features GmbH

- Valcare Medical Inc.

- Venus Medtech

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Population and Rising Severe Aortic Stenosis Burden

- 4.2.2 Expansion Into Lower-Risk Patient Populations

- 4.2.3 One-Step Pathway From Diagnosis to Intervention Through Multidisciplinary Heart Teams

- 4.2.4 Next-Generation Valve Durability, Repositionability, and Delivery Precision

- 4.2.5 Earlier Intervention Enabled by Trial Evidence and Label Expansion

- 4.2.6 Hospital Economics Favoring Shorter Length of Stay and Reduced Resource Intensity

- 4.3 Market Restraints

- 4.3.1 Lifetime Management Concerns in Younger Patients

- 4.3.2 Anatomical Complexity in Native Aortic Regurgitation, Mitral, and Tricuspid Indications

- 4.3.3 Reimbursement and Coverage Variability Across Health Systems

- 4.3.4 High Capital, Imaging, and Structural Heart Program Costs

- 4.4 Value/Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Product Type

- 5.1.1 Transcatheter Aortic Valve

- 5.1.2 Transcatheter Mitral Valve

- 5.1.3 Transcatheter Tricuspid Valve

- 5.1.4 Transcatheter Pulmonary Valve

- 5.2 By Valve Technology

- 5.2.1 Balloon-Expandable Valves

- 5.2.2 Self-Expandable Valves

- 5.2.3 Others

- 5.3 By Delivery Route

- 5.3.1 Transfemoral

- 5.3.2 Transapical

- 5.3.3 Transseptal

- 5.3.4 Transjugular

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Specialty Cardiac Centers

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 4C Medical Technologies, Inc.

- 6.3.2 Abbott Laboratories

- 6.3.3 Alterra Medical, Inc.

- 6.3.4 Anteris Technologies Ltd.

- 6.3.5 Biosensors International Group, Ltd.

- 6.3.6 Boston Scientific Corporation

- 6.3.7 Braile Biomedica Industria, Comercio e Representacoes Ltda.

- 6.3.8 CardiaQuest, Inc.

- 6.3.9 Cephea Valve Technologies, Inc.

- 6.3.10 Edwards Lifesciences Corporation

- 6.3.11 HighLife SAS

- 6.3.12 JenaValve Technology, Inc.

- 6.3.13 Medtronic plc

- 6.3.14 Memryx, Inc.

- 6.3.15 Meril Life Sciences Pvt. Ltd.

- 6.3.16 MicroPort Scientific Corporation

- 6.3.17 Navigate Medical, Inc.

- 6.3.18 Neovasc Inc.

- 6.3.19 P and F Products and Features GmbH

- 6.3.20 Valcare Medical Inc.

- 6.3.21 Venus Medtech (Hangzhou) Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment