|

시장보고서

상품코드

2073088

로봇 수술 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Robotic Surgical Procedures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

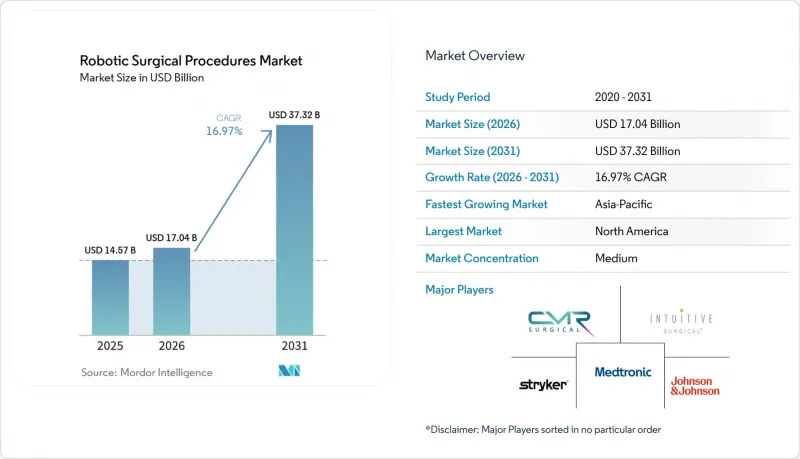

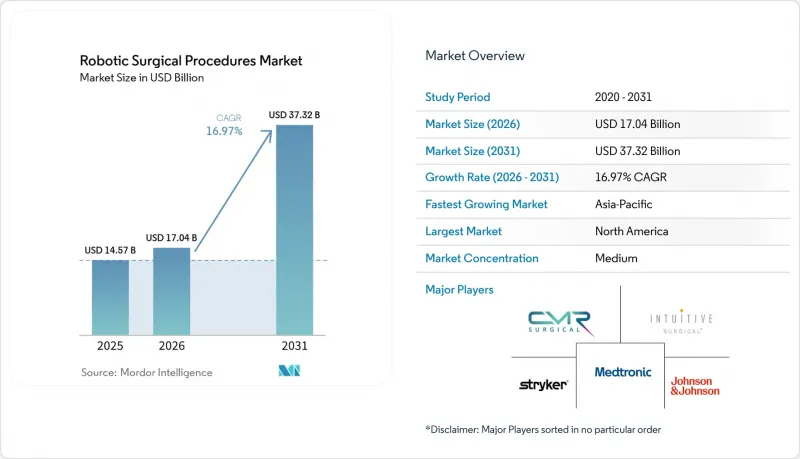

Mordor Intelligence에 의하면, 로봇 수술 시장 규모는 2025년에 145억 7,000만 달러로 평가되었고 2026년 170억 4,000만 달러에서 2031년까지 373억 2,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 16.97%를 나타낼 전망입니다.

본 보고서는 용도별(비뇨기과, 일반외과, 기타), 수술 유형별(저침습 복강경 수술, 기타), 최종 사용자별(대규모 병원 그룹, 독립 및 사립 병원, 기타), 지역별(북미, 유럽, 아시아태평양, 기타)로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계 로봇 수술 시장 동향과 인사이트

비뇨기과를 넘어선 임상적 유효성의 확대

로봇 수술 시장은 비뇨기과에 대한 의존에서 벗어나, 여러 전문 분야에 걸쳐 더 광범위하게 도입되는 방향으로 전환되고 있습니다. 2026년에는 아쿠아브레이션에 관한 지침이 강화됨에 따라 양성 전립선 비대증에 대한 로봇 치료에 대한 신뢰도가 높아졌으며, 이로 인해 비뇨기과 부문에서의 활용이 촉진되었습니다. 일반외과 및 산부인과에서도 도입이 확대되고 있으며, 존슨앤드존슨의 FORTE 연구에서는 30명의 위우회술 환자를 대상으로 한 코호트에서 안전성 및 성능 기준을 충족했습니다. 복잡한 비만 수술 사례에서 로봇 수술이 보여주는 안정적인 성능은 보험사 및 의료 제공업체들이 관련 수술에 로봇 수술을 더욱 적극적으로 도입하도록 촉진하여 시장의 잠재력을 확대할 것으로 기대됩니다.

AI를 활용한 수술 계획 및 워크플로우의 표준화

인공지능(AI)은 로봇 수술 시장을 하드웨어 중심의 구매 방식에서 워크플로우를 중시하는 모델로 변화시키고 있습니다. 메드트로닉사의 “Stealth AXiS”시스템은 2026년 2월 FDA 승인을, 2026년 4월 CE 마크를 획득했으며, 계획, 내비게이션, 로봇을 통한 수술 수행을 단일 플랫폼에 통합하고 있습니다. 2026년 6월에 출시된 Moon Surgical의 “Maestro”소프트웨어 버전 2.7에서는 수술실 자동 설정, 내비게이션, 수술 후 기록 기능이 도입되었습니다. 이러한 발전으로 운영이 간소화됨에 따라, 그동안 인력 배치의 복잡성을 이유로 도입을 주저해 왔던 의료기관들에게도 로봇 시스템의 매력이 커지고 있습니다.

막대한 초기 투자 비용과 수술마다 발생하는 지속적인 비용 부담

로봇 수술은 막대한 비용 장벽에 직면해 있으며, 이로 인해 주요 의료 센터 이외의 곳에서는 보급이 저해되고 있습니다. 재정적 부담은 로봇 시스템의 도입 비용에만 그치지 않습니다. 기구, 일회용 소모품, 업그레이드에 드는 비용도 각 수술의 경제성 측면에서 매우 중요한 역할을 하고 있습니다. 이 문제는 보험사가 복강경 수술과 비교해 로봇 수술에 대해서는 보험금 지급을 제공하지 않을 경우 더욱 심각해집니다. 그 결과, 의료 제공업체들은 직접적인 금전적 인센티브가 아닌 효율성이나 환자의 치료 결과를 바탕으로 로봇 수술 도입을 추진할 수밖에 없는 상황에 놓여 있습니다. 그 대표적인 예가 스미스 앤 네퓨사의 ‘CORI XT” 플랫폼입니다. 이 플랫폼은 어깨 수술로의 적용 범위를 확대하고 있는 반면, 정형외과 수술 건수를 여전히 늘려가고 있는 의료기관에게는 막대한 설비 투자라는 큰 과제를 안겨주고 있습니다. 그 결과, 로봇 수술의 도입은 주로 3차 의료기관, 전문 클리닉, 일부 환자 수가 많은 외래 센터로 한정되어 있습니다.

부문별 분석

2025년, 비뇨기과는 로봇 수술 시장 전체의 31.76%를 차지하며 주요 용도 부문으로서의 위상을 유지했습니다. 이러한 우위는 로봇 전립선 전적출술이 광범위하게 도입되었고, 다른 특수 수술에 비해 임상 현장에서 빠르게 받아들여졌기 때문입니다. 2026년에 아쿠아브레이션에 대한 진료 지침에 대한 지지가 높아짐에 따라, 시장에서 로봇 보조 비뇨기과 의료의 역할은 더욱 강화되었습니다. 병원 입장에서는 새로운 진료과를 신설하지 않고도 수술 건수를 늘릴 수 있기 때문에 이 부문은 매력적인 시장으로 자리 잡고 있습니다.

정형외과는 가장 빠르게 성장하고 있는 부문으로, 2031년까지의 예상 연평균 성장률(CAGR)은 17.90%입니다. 최근의 기술 발전으로 인해 시스템의 설치 면적, 영상에 대한 의존도, 설치 관련 문제가 완화되면서 정형외과용 로봇이 외래 진료 현장에도 도입되기 시작했습니다. 스트라이커사의 “Mako RPS”와 스미스 앤 네퓨사의 “CORI XT”는 이러한 변화를 상징하는 예입니다. 일반외과 및 산부인과 분야도 확대되고 있으며, 2026년 1월 OTTAVA가 FDA에 신청서를 제출한 점과 위 우회 수술에 관한 임상시험에서 양호한 결과가 나온 점은 이 플랫폼의 적용 범위가 더욱 넓어질 것임을 시사합니다. 신경외과와 척추외과는 여전히 소규모 분야이지만, 메드트로닉사의 ‘Stealth AXiS”는 공통 플랫폼이 병원의 자본 효율성을 어떻게 향상시킬 수 있는지를 보여줍니다.

지역별 분석

2025년, 북미는 로봇 수술 시장 전체의 43.55%를 차지하며 지역별 최대 기여도를 유지했습니다. 이 지역은 로봇 비뇨기과 수술에 대한 충실한 보험 환급 제도, 설치 시스템당 높은 이용률, 외과 의사 및 의료진을 위한 확립된 교육 체계와 같은 이점을 누리고 있습니다. 인튜이티브사는 2025년 미국 내 다빈치 수술 건수가 15% 증가했을 뿐만 아니라, 2026년 1분기에는 근무 시간 외 수술 이용률이 31% 상승했다고 보고했습니다. 이는 시장의 성장이 단순히 신규 도입뿐만 아니라 기존 시스템의 활용도 향상에 의해서도 주도되고 있음을 보여줍니다. 캐나다와 멕시코도 진전을 보이고 있지만, 수술 건수, 보험 급여, 플랫폼 승인 측면에서 볼 때 미국이 여전히 이 지역을 선도하고 있습니다.

유럽은 로봇 수술 시장에서 2위의 점유율을 차지하고 있습니다. 이 지역은 탄탄한 임상 연구, 국민건강보험 제도, 제조 거점의 집중이라는 강점을 활용하고 있습니다. 그러나 북미와 비교할 때 보험 환급 제도는 여전히 일관성이 부족하며, 기존의 결제 구조 하에서 로봇 수술의 이점이 충분히 반영되지 않을 경우, 병원은 더 큰 경제적 위험에 노출될 수밖에 없습니다. 그럼에도 불구하고, 유럽에서는 특히 정형외과 및 최소 침습 수술 분야에서 장기적인 활용을 뒷받침할 플랫폼의 선택적 도입이 진행되고 있습니다. 예산 제약이 엄격한 유럽에서의 성공은 공급업체로 하여금 전 세계적인 보급 확대에 대한 전망을 더욱 확고히 하게 합니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 17.45%를 나타낼 것으로 예측되어, 로봇 수술 시장에서 가장 빠른 성장이 전망됩니다. 해당 지역은 특히 중국의 경우, 수입 의존에서 국내 경쟁 심화로 전환되고 있습니다. 동남아시아의 다빈치 수술 건수는 2025년에 24% 증가했으며, 이는 북미나 유럽에 비해 도입 대수가 적은 시장에서도 이용이 확대되고 있음을 반영하고 있습니다. 중국의 국내 수술용 로봇 시장은 성장세를 보이고 있으며, 이는 가격 책정 및 플랫폼 접근 방식에 변화를 가져올 가능성이 있습니다. 인도와 한국은 만성 질환 부담 증가와 민간 병원에 대한 투자를 통해 지역 성장에 기여하고 있는 반면, 중동 및 아프리카와 남미는 여전히 초기 단계에 머물러 있으며, 의료 관광, 병원 현대화, 엄선된 플랫폼 도입에 중점을 두고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the robotic surgical procedures market size was valued at USD 14.57 billion in 2025 and is estimated to grow from USD 17.04 billion in 2026 to reach USD 37.32 billion by 2031, at a CAGR of 16.97% during the forecast period (2026-2031).

This report is Segmented by Application (Urology, General Surgery, and More), Procedure Type (Minimally Invasive Laparoscopic, and More), End User (Large Hospital Systems, Standalone and Private Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Robotic Surgical Procedures Market Trends and Insights

Expanded Clinical Validation Beyond Urology

The robotic surgical procedures market is transitioning from its reliance on urology to broader adoption across multiple specialties. In 2026, enhanced guidelines for Aquablation increased confidence in robotic treatments for benign prostatic hyperplasia, driving its use in urology. General surgery and gynecology are also gaining traction, with Johnson & Johnson's FORTE study meeting safety and performance benchmarks in a 30-patient gastric bypass cohort. Stable robotic performance in complex bariatric cases is expected to encourage payers and providers to extend adoption to related procedures, expanding the market's potential.

AI-Enabled Surgical Planning and Workflow Standardization

Artificial intelligence is transforming the robotic surgical procedures market from hardware-driven purchases to workflow-focused models. Medtronic's Stealth AXiS system, cleared by the FDA in February 2026 and CE Mark in April 2026, integrates planning, navigation, and robotic execution into a single platform. Moon Surgical's Maestro Software Version 2.7, launched in June 2026, introduced automated operating room setup, navigation, and post-procedure documentation. These advancements simplify operations, making robotic systems more appealing to facilities previously deterred by staffing complexities.

High Capital and Recurring Per-Procedure Cost Burden

Robotic surgical procedures grapple with significant cost hurdles, hindering their uptake beyond major medical centers. The financial strain extends beyond just acquiring the robotic system; costs for instruments, disposables, and upgrades play a pivotal role in the economics of each procedure. This challenge intensifies when insurers don't offer premium reimbursements for robotic surgeries compared to their laparoscopic counterparts. Consequently, medical providers are left to advocate for robotic adoption based on efficiency and patient outcomes rather than direct financial incentives. A case in point is Smith+Nephew's CORI XT platform, which, while expanding capabilities to shoulder surgeries, introduces a substantial capital challenge for facilities still ramping up their orthopedic volumes. Consequently, adoption of robotic procedures is largely confined to tertiary hospitals, specialized clinics, and a select few busy outpatient centers.

Other drivers and restraints analyzed in the detailed report include:

- Ambulatory Surgical Center Platform Fit and Throughput

- Value-Based Procurement Tied to Measurable Outcomes

- OR Integration Complexity and Staff Training Dependencies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, urology accounted for 31.76% of the robotic surgical procedures market, maintaining its position as the leading application segment. This dominance stems from the widespread adoption of robotic prostatectomies and faster clinical acceptance compared to other specialties. The growing guideline support for Aquablation in 2026 further strengthened robotic urologic care's role in the market. Hospitals find this segment appealing as they can increase procedure volumes without creating new clinical categories.

Orthopedics is the fastest-growing segment, with a forecast CAGR of 17.90% through 2031. Recent advancements have reduced system footprints, image dependency, and setup challenges, enabling orthopedic robots to move into outpatient settings. Stryker's Mako RPS and Smith+Nephew's CORI XT exemplify this shift. General surgery and gynecology are also expanding, with OTTAVA's FDA submission in January 2026 and positive gastric bypass study results signaling broader platform applications. Neurosurgery and spine remain smaller segments, but Medtronic's Stealth AXiS demonstrates how shared platforms can enhance hospitals' capital efficiency.

Complete Report Scope:

- By Application

- Urology

- General Surgery

- Gynecology

- Orthopedics

- Cardiothoracic Surgery

- Neurosurgery

- Ear, Nose, and Throat Surgery

- Bariatric and Metabolic Surgery

- Other Applications

- By Procedure Type

- Minimally Invasive Laparoscopic Robotic-Assisted Procedures

- Percutaneous and Catheter-Based Robotic Procedures

- Endoscopic Robotic Procedures

- Open-Assisted Hybrid Procedures

- Other Procedure Types

- By End User

- Large Hospital Systems

- Standalone and Private Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America accounted for 43.55% of the robotic surgical procedures market, maintaining its position as the largest regional contributor. The region benefits from strong reimbursement frameworks in robotic urology, higher utilization rates per installed system, and a well-established training base for surgeons and care teams. Intuitive reported a 15% increase in US da Vinci procedures in 2025, alongside a 31% rise in after-hours procedure utilization in Q1 2026. This indicates that market growth is driven by better utilization of existing systems rather than solely by new installations. While Canada and Mexico are progressing, the US continues to lead the region in terms of volume, reimbursement, and platform approvals.

Europe held the second-largest share in the robotic surgical procedures market. The region benefits from strong clinical research, universal healthcare systems, and a significant manufacturing presence. However, reimbursement remains less consistent compared to North America, exposing hospitals to higher economic risks when robotic benefits are not fully covered under existing payment structures. Despite this, Europe is advancing through selective platform adoption, particularly in orthopedic and minimally invasive applications, which support long-term utilization. Success in Europe under tighter budget constraints strengthens vendors' prospects for broader global adoption.

Asia-Pacific is projected to witness the fastest growth in the robotic surgical procedures market, with a CAGR of 17.45% through 2031. The region is transitioning from import reliance to stronger domestic competition, especially in China. Da Vinci procedures in Southeast Asia grew by 24% in 2025, reflecting increased utilization even in markets with smaller installed bases compared to North America and Europe. China's domestic surgical robot market is gaining traction, potentially reshaping pricing and platform access. India and South Korea contribute to regional growth through rising chronic disease burdens and private hospital investments, while the Middle East, Africa, and South America remain in early stages, focusing on medical tourism, hospital modernization, and selective platform adoption.

- Asensus Surgical, Inc.

- Brain Lab

- CMR Surgical Ltd.

- Curexo, Inc.

- Distalmotion SA

- Globus Medical

- Intuitive Surgical, Inc.

- Johnson & Johnson

- Medical Microinstruments S.p.A.

- Medtronic

- Monteris Medical Corporation

- Neocis Inc.

- PROCEPT BioRobotics Corporation

- Renishaw plc

- Siemens Healthineers

- Smiths Group

- SS Innovations International, Inc.

- Stryker

- THINK Surgical, Inc.

- Zimmer Biomet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanded Clinical Validation Beyond Urology

- 4.2.2 Ambulatory Surgical Center Platform Fit and Throughput Economics

- 4.2.3 AI-Enabled Surgical Planning and Workflow Standardization

- 4.2.4 Value-Based Procurement Tied to Measurable Outcome Improvement

- 4.2.5 Multi-Specialty Utilization of Single Robotic Platforms

- 4.2.6 Surgeon Retention and Talent Attraction Through Robotic Capability

- 4.3 Market Restraints

- 4.3.1 High Capital and Recurring Per-Procedure Cost Burden

- 4.3.2 OR Integration Complexity and Staff Training Dependency

- 4.3.3 Cybersecurity and Software Validation Requirements for Connected Robots

- 4.3.4 Uneven Reimbursement and Procedure Economics Across Health Systems

- 4.4 Value and Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Application

- 5.1.1 Urology

- 5.1.2 General Surgery

- 5.1.3 Gynecology

- 5.1.4 Orthopedics

- 5.1.5 Cardiothoracic Surgery

- 5.1.6 Neurosurgery

- 5.1.7 Ear, Nose, and Throat Surgery

- 5.1.8 Bariatric and Metabolic Surgery

- 5.1.9 Other Applications

- 5.2 By Procedure Type

- 5.2.1 Minimally Invasive Laparoscopic Robotic-Assisted Procedures

- 5.2.2 Percutaneous and Catheter-Based Robotic Procedures

- 5.2.3 Endoscopic Robotic Procedures

- 5.2.4 Open-Assisted Hybrid Procedures

- 5.2.5 Other Procedure Types

- 5.3 By End User

- 5.3.1 Large Hospital Systems

- 5.3.2 Standalone and Private Hospitals

- 5.3.3 Ambulatory Surgical Centers

- 5.3.4 Specialty Clinics

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Asensus Surgical, Inc.

- 6.3.2 Brainlab AG

- 6.3.3 CMR Surgical Ltd.

- 6.3.4 Curexo, Inc.

- 6.3.5 Distalmotion SA

- 6.3.6 Globus Medical, Inc.

- 6.3.7 Intuitive Surgical, Inc.

- 6.3.8 Johnson & Johnson

- 6.3.9 Medical Microinstruments S.p.A.

- 6.3.10 Medtronic plc

- 6.3.11 Monteris Medical Corporation

- 6.3.12 Neocis Inc.

- 6.3.13 PROCEPT BioRobotics Corporation

- 6.3.14 Renishaw plc

- 6.3.15 Siemens Healthineers AG

- 6.3.16 Smith & Nephew plc

- 6.3.17 SS Innovations International, Inc.

- 6.3.18 Stryker Corporation

- 6.3.19 THINK Surgical, Inc.

- 6.3.20 Zimmer Biomet Holdings, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White Space and Unmet Need Assessment