|

시장보고서

상품코드

2073104

정부 및 공공 부문용 그린 IT 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Government and Public Sector Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

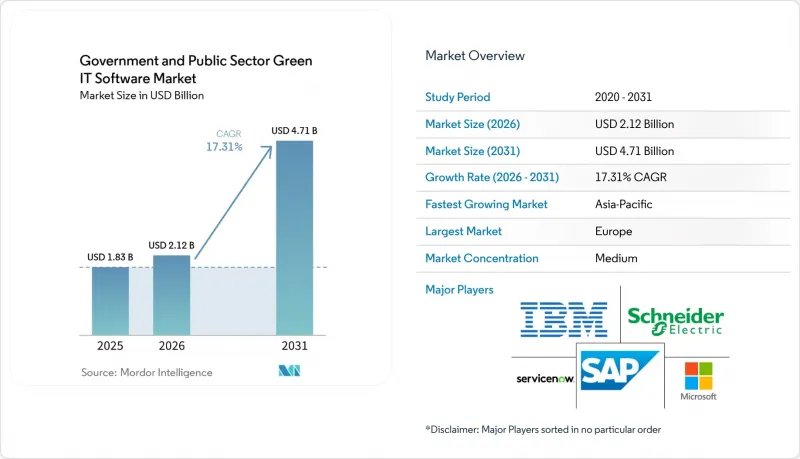

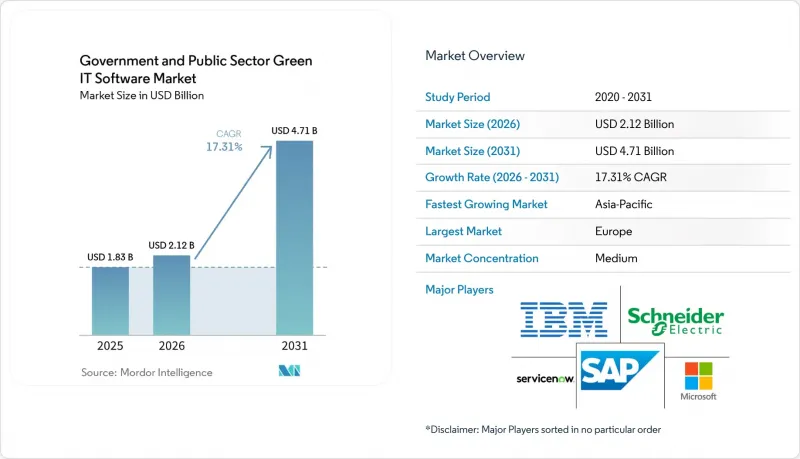

Mordor Intelligence에 의하면, 정부 및 공공 부문용 그린 IT 소프트웨어 시장 규모는 2025년 18억 3,000만 달러에서 2026년에는 21억 2,000만 달러로 확대되어 2031년까지 47억 1,000만 달러에 이를 것으로 예상되고 있어 2026-2031년까지 CAGR 17.31%로 성장할 전망입니다.

본 보고서는 제공 형태(소프트웨어 및 서비스), 도입 형태(클라우드, On-Premise, 하이브리드), 최종 사용자(중앙·연방 정부, 주·지방 자치단체, 유틸리티·공공기관, 기타), 용도(탄소 데이터 수집·공개, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 정부 및 공공 부문용 그린 IT 소프트웨어 시장 동향과 인사이트

공공 부문의 탄소중립 조달 요건이 계약 기준을 재편하고 있습니다.

공공 조달 규정에 따라, 정부 및 공공 부문용 그린 IT 소프트웨어 시장은 자발적인 보고에서 계약상 구속력이 있는 배출량 보고로 전환되고 있습니다. 영국에서는 2025년 2월 24일 이후 공고되는 주요 정부 계약에 PPN 006을 적용하고 있으며, 이 규정에 따라 500만 영국 파운드(659만 달러)를 초과하는 계약공급업체에게는 참여 조건으로 탄소 감축 계획 제출을 의무화하고 있습니다. 이러한 요인으로 인해 소프트웨어에 대한 수요가 변화하고 있습니다. 이는 각 기관이 조달 팀이 검증 가능한 형태로 공급업체와 함께 운영상 배출량 데이터를 수집·저장·제시할 수 있는 시스템을 필요로 하기 때문입니다. 또한, 이를 통해 조달, 법무, 재무, 지속가능성 각 팀이 단일 워크플로우를 통해 협업하게 됨에 따라, 정부 및 공공 부문용 그린 IT 소프트웨어 시장에서 통합된 보고 및 감사 추적 기록의 가치가 부각되고 있습니다. 따라서 이미 공식적인 공공 조달 절차에 부합하는 공급업체는 각 기관이 입찰을 평가할 때, 기능의 충실도와 마찬가지로 중요한 의미를 지닌 접근성 면에서의 우위를 확보하게 됩니다.

정부의 디지털 현대화 의무화가 플랫폼 통합을 가속화

지속가능성 요건이 보다 광범위한 기술 갱신 과제에 통합됨에 따라, 디지털 현대화 프로그램은 정부 및 공공 부문용 그린 IT 소프트웨어 시장의 예산 규모를 확대되고 있습니다. 영국 환경·식량·농촌지역부(Defra)가 수립한 “디지털 지속가능성 전략 2025-2030”에서는 2030년까지 IT 관련 이산화탄소 배출량을 16% 감축한다는 목표가 설정되었으며, 연간 계약액이 100만 영국 파운드(132만 달러)를 초과하는 디지털 서비스 제공업체에 대해 외부 기관의 검증을 거친 탄소 발자국 및 탄소 중립 계획을 제출할 의무가 부과되었습니다. 이 전략에 따르면, Defra 그룹의 IT 운영으로 인해 2024년에 1만 톤의 이산화탄소 환산 배출량이 발생할 것으로 예상되며, 이는 해당 부처의 총 배출량의 13%에 해당합니다. 이 사실은 소프트웨어를 활용한 추적 관리가 IT 거버넌스의 핵심으로 자리 잡아가고 있는 이유를 보여줍니다. 미국에서는 2025년 12월 GSA가 SAP와 체결한 ‘OneGov”계약에 따라 연방 정부 기관에 데이터베이스, 통합, 분석, 클라우드 도구 전반에 걸쳐 최대 80%의 할인이 제공되며, 1억 6,500만 달러의 비용 절감이 예상됩니다. 이러한 움직임은 이미 승인된 조달 및 엔터프라이즈 기술 스택에 통합된 공급업체를 우대하는 것이며, 정부 및 공공 부문용 그린 IT 소프트웨어 시장 전반에 걸친 플랫폼 통합을 촉진하고 있습니다.

예산 및 조달 주기의 세분화가 재량적 도입을 지연시킵니다.

연간 예산 편성 체계로 인해 정부 및 공공 부문용 그린 IT 소프트웨어 시장의 성장세가 여전히 둔화되고 있습니다. 이는 지속가능성 도구가 동일한 자금 조달 주기 내에서 우선순위가 높은 IT 프로젝트와 경쟁하는 경우가 많기 때문입니다. 많은 기관에서 예산 심의 시 사이버 보안, 인사 시스템, 레거시 시스템의 현대화가 여전히 탄소 관리 플랫폼보다 우선순위가 높게 책정되고 있어, 그 결과 의무화 조치가 명확함에도 불구하고 도입이 지연되는 상황이 발생하고 있습니다. GSA와 SAP 간의 “OneGov”계약은 대폭적인 할인을 통해 도입 비용을 절감하여 1억 6,500만 달러의 절감 효과가 예상되었으나, 이 계약은 단기적인 조달 기간이 도입 시기와 갱신 위험에 영향을 미칠 수도 있음을 보여주었습니다. 이와 유사한 과제는 지방 자치단체 차원에서도 발생하고 있습니다. 시, 군, 주의 예산 일정은 국가의 보고 요건과 일치하지 않는 경우가 많으며, 그 결과 예산이 승인되기 전에 정책상의 요건이 부과되는 경우가 있습니다. 단계적 도입, 시범 운영 범위 설정, 모듈식 가격 책정을 제공하는 공급업체는 정부 및 공공 부문용 그린 IT 소프트웨어 시장에서 이러한 제약을 극복하는 데 적합합니다.

부문별 분석

2025년, 탄소 회계 및 보고 소프트웨어는 정부 및 공공 부문용 그린 IT 소프트웨어 시장 점유율의 28.74%를 차지하며, 예측 기간 시작 시점에서 가장 큰 비중을 차지하는 솔루션 유형이 되었습니다. 이 지침은 공공기관 업무의 실제 절차를 반영하고 있습니다. 왜냐하면 공공 기관은 감축 목표 설정, 공급업체 비교, 또는 보조금과 관련된 공시의 정당성을 입증하기 전에, 먼저 측정 가능하고 감사 가능한 배출량 기준선을 확립해야 하기 때문입니다. 또한, 규정 준수 의무의 확대에 따라 감사의 추적 가능성과 체계적인 기록이 사용자 기능만큼 중요하게 여겨지게 되면서, 이 범주는 정부 조달 담당자가 시스템을 평가하는 방식에서도 혜택을 보고 있습니다. SAP가 2026년 5월, 자사의 탄소 회계 솔루션이 IDC MarketScape에서 다시 한 번 평가를 받았다고 발표한 것은 배출량 기록을 재무 관리 실무와 더욱 긴밀하게 연계시키는 ERP 네이티브 아키텍처의 매력을 입증하는 것입니다.

에너지 및 전력 관리 소프트웨어도 이 주요 카테고리와 함께 주목을 받고 있습니다. 이는 각 기관이 지속가능성 관련 노력을 운영 효율성이나 데이터센터의 성과 목표와 연계해야 할 필요성을 이전보다 더 강하게 느끼고 있기 때문입니다. 친환경 조달 및 공급업체 지속가능성 관리 소프트웨어 시장은 2031년까지 연평균 성장률(CAGR) 18.12%로 확대될 것으로 예상되며, 이는 관련 솔루션군 중 가장 빠른 성장 속도입니다. EcoVadis와 Workiva가 2026년 5월에 제휴를 맺은 것은 이 분야가 급속히 성장하고 있는 이유를 보여줍니다. 공급업체의 탄소 데이터는 개별 조달 시스템 내에 머무르는 것이 아니라, 감사에 대응할 수 있는 보고서로 보다 직접적으로 연동되도록 되어 있기 때문입니다. 또한, 정부 기관은 수작업에 의한 반복적인 집계 없이 회계, 조달, 운영 정보를 일원적으로 관리할 수 있는 단일 환경이 필요하기 때문에 지속가능성 데이터 관리 플랫폼의 중요성도 점점 더 커지고 있습니다.

2025년에는 클라우드 도입이 매출의 65.41%를 차지하며, 정부 및 공공 부문용 그린 IT 소프트웨어 시장에서 다른 배포 모델을 크게 앞질렀습니다. 정부 기관은 가능한 한 클라우드를 우선적으로 도입하고 있습니다. 이는 구독형 서비스를 통해 규정 준수 달성까지 걸리는 시간을 단축할 수 있을 뿐만 아니라, 규정 업데이트, 유지보수 및 릴리스 관리를 공급업체 측에 이관할 수 있기 때문입니다. 이는 내부 IT 팀이 자원 제약에 자주 직면하며, 대규모 재구성을 거치지 않고도 최신 상태를 유지할 수 있는 소프트웨어가 필요한 공공 부문에서 중요한 요소가 됩니다. 또한, 클라우드는 협상을 통한 조달 채널이나 승인된 플랫폼을 활용하여 도입을 가속화하는 정부의 현대화 프로그램보다 더 광범위한 추세와도 부합합니다.

하이브리드 도입은 2026년부터 2031년까지 연평균 성장률(CAGR) 17.95%를 나타낼 것으로 예측되며, 구매자들이 규정 준수의 신속성과 기밀 데이터 관리 간의 균형을 모색하는 가운데 가장 빠르게 성장하는 모델이 될 전망입니다. 유럽연합 집행위원회의 “소버린 클라우드 프레임워크”와 같이, 유럽 외부에 대한 의존도를 줄이기 위한 프랑스의 2026년 지침은 공공 부문 데이터가 어디에서 어떻게 저장·처리되는지에 대한 기준을 강화함으로써 이러한 중도적인 접근 방식을 뒷받침하고 있습니다. 따라서 On-Premise 배포는 더 이상 성장 속도를 주도하는 요소가 아니게 되었더라도, 국방, 국가 안보, 엄격한 운영 데이터 규정을 갖춘 기관에게는 여전히 중요한 선택지로 남아 있습니다. 주권 요건이 유지되는 가운데, 로컬 환경과 규정 준수 요건을 충족하는 클라우드 계층 간에 데이터를 원활하게 이동시킬 수 있는 벤더는 정부 및 공공 부문용 그린 IT 소프트웨어 시장에서 더 큰 시장 점유율을 확보할 가능성이 높을 것으로 보입니다.

지역별 분석

2025년, 유럽은 정부 및 공공 부문용 그린 IT 소프트웨어 시장에서 34.56%의 점유율을 기록하며 지역 시장 중 1위를 유지했습니다. 이 지역의 위상은 환경 규정 준수, 조달 관리, 디지털 거버넌스가 별개의 과제가 아닌 하나의 통합된 체계로 발전하고 있는 치밀한 정책 환경에 의해 뒷받침되고 있습니다. 유럽연합 집행위원회의 “소버린 클라우드 프레임워크”는 퍼블릭 클라우드 조달의 평가 기준 중 하나로 환경의 지속가능성을 제시하는 한편, 도입 결정에 있어 주권 보장을 핵심으로 삼고 있습니다. 영국은 공급업체와 각 부처의 IT 운영에 대해 공식적인 요건을 부과하는 공공 조달 및 디지털 지속가능성 관련 규정을 통해 더욱 탄력을 얻었습니다. 그 결과, 유럽에서는 광범위한 규정 준수 압박과 공공 부문의 심사에 이미 대비하고 있는 공급업체로 지출을 유도할 수 있는 조달 시스템이 결합되어 있습니다.

북미는 2025년 정부 및 공공 부문용 그린 IT 소프트웨어 시장에서 지역별 기준으로 두 번째로 큰 시장을 차지했습니다. 미국에서는 중앙집권적인 조달 방식이 도입에 큰 영향을 미치고 있으며, 이로 인해 대형 벤더들은 각 기관과의 개별 거래보다 더 신속하게 연방 정부의 시스템 환경에 진입할 수 있게 되었습니다. GSA와 SAP 간에 체결된 “OneGov”계약은 연방 기관이 협상을 통한 할인 및 공통 조달 조건을 통해 분석, 통합, 클라우드 기능에 대한 접근성을 어떻게 확대할 수 있는지를 보여주었습니다. 이 시스템은 대규모 도입을 지원하는 한편, 주요 플랫폼과 더불어 공급업체, 자산 또는 정보 공개와 관련된 보다 고도화된 기능을 제공하는 전문 도구가 활용될 여지도 남겨두고 있습니다.

아시아태평양은 2026년부터 2031년까지 연평균 성장률(CAGR) 18.45%로 확대될 것으로 예상되며, 정부 및 공공 부문용 그린 IT 소프트웨어 시장에서 가장 두드러진 성장을 보일 지역 부문이 될 전망입니다. 해당 지역에서는 정책 수립 단계에서 실행 단계로 넘어가고 있으며, 이에 따라 탄소 회계, 수명 주기 추적, 조달 지향적 보고서 작성 도구에 대한 수요가 확대되고 있습니다. NTT 그룹이 2026년 3월에 발표한 소프트웨어 수명 주기 CO₂ 산정 기준은 아시아태평양의 선진 시장에서 소프트웨어 관련 배출량이 보다 공식적으로 다루어지게 되었음을 반영하고 있습니다. 남미와 중동 및 아프리카는 현재로서는 시장 규모가 작지만, Khazna, Agility, 에너지 인프라부와 공동으로 발표된 아랍에미리트의 시범 사업은 정부의 에너지 관리 도입이 이 두 주요 지역 이외의 곳에서도 활발히 실행 단계에 접어들고 있음을 보여주고 있습니다. 이는 유럽과 북미 이외의 지역에서 향후 확장이 우선 대상을 좁힌 공공 프로젝트에서 시작되어, 이후 각 기관이 내부 역량을 구축하고 조달에 대한 이해를 높여감에 따라 점차 확대될 가능성이 높다는 것을 의미합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the government and public sector green IT software market size is expected to increase from USD 1.83 billion in 2025 to USD 2.12 billion in 2026 and reach USD 4.71 billion by 2031, growing at a CAGR of 17.31% over 2026-2031.

This report is Segmented by Offering (Software, and Services), Deployment (Cloud, On-Premises, and Hybrid), End User (Central and Federal Government, State and Local Government, Public Utilities and Public Agencies, and More), Application (Carbon Data Collection and Disclosure, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Government and Public Sector Green IT Software Market Trends and Insights

Public Sector Net-Zero Procurement Requirements Reshape Contract Standards

Public procurement rules are pushing the government and public sector green IT software market away from voluntary reporting and toward contract-bound emissions documentation. The United Kingdom applied PPN 006 to major government contracts advertised from February 24, 2025, and the rule requires suppliers on contracts above GBP 5 million (USD 6.59 million) to submit carbon reduction plans as a condition of participation. That requirement changes software demand because agencies need systems that can collect, retain, and present supplier and operational emissions data in a form procurement teams can verify. It also brings together procurement, legal, finance, and sustainability teams on a single workflow, underscoring the value of centralized reporting and audit trails in the government and public sector green IT software market. Vendors that already fit formal public buying processes therefore gain an access advantage that can matter as much as feature depth when agencies evaluate bids.

Government Digital Modernization Mandates Accelerate Platform Consolidation

Digital modernization programs are widening the budgetary path for the government and public sector green IT software markets, as sustainability requirements are being built into broader technology renewal agendas. The United Kingdom's Defra Digital Sustainability Strategy 2025-2030 set a target to reduce IT carbon emissions by 16% by 2030 and required digital service suppliers with an annual contract value above GBP 1 million (USD 1.32 million) to hold externally verified carbon footprints and net-zero plans. The same strategy stated that Defra group IT operations generated 10,000 tonnes of CO2 equivalent in 2024, equal to 13% of the department's total emissions, which shows why software-backed tracking is moving closer to core IT governance. In the United States, the GSA's OneGov agreement with SAP in December 2025 offered federal agencies discounts of up to 80% across database, integration, analytics, and cloud tools, with projected savings of USD 165 million. These moves favor vendors that already sit within approved procurement and enterprise technology stacks, which support platform consolidation across the government and public-sector green IT software markets.

Fragmented Budget and Procurement Cycles Slow Discretionary Uptake

Annual budgeting structures continue to slow the government and public sector green IT software market, as sustainability tools often compete with higher-priority IT projects within the same funding cycle. In many agencies, cybersecurity, workforce systems, and legacy modernization still rank ahead of carbon management platforms in appropriations reviews, which delays rollouts even when mandates are clear. The GSA's OneGov agreement with SAP lowered entry costs through deep discounts and projected USD 165 million in savings, but the arrangement also showed that short-term procurement windows can shape adoption timing and renewal risk. The same challenge arises at the subnational level, where city, county, and state budget calendars often do not align with national reporting expectations so that the policy requirement can arrive before the budget authority. Vendors that offer phased deployment, pilot scopes, and modular pricing are better suited to move through this constraint in the government and public sector green IT software market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Data Center Energy Costs Shift the Software ROI Case

- Sustainability Reporting Automation Replaces Spreadsheet Workflows

- Data Sovereignty Requirements Create Competing Architecture Demands

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Carbon accounting and reporting software held 28.74% of the government and public sector green IT software market share in 2025, which made it the largest solution type at the start of the forecast period. That lead reflects the practical order of agency work, because public bodies first need a measured and auditable emissions baseline before they can set reduction targets, compare suppliers, or defend grant-linked disclosures. The category also benefits from how government buyers evaluate systems, since audit traceability and structured records matter as much as user features as compliance obligations expand. SAP's May 2026 announcement that its carbon accounting offering was recognized again in the IDC MarketScape reinforces the appeal of ERP-native architectures that align emissions records more closely with financial control practices.

Energy and power management software is gaining traction alongside the leading category, as agencies now face a stronger need to tie sustainability actions to operating efficiency and data center performance targets. Green procurement and supplier sustainability software is projected to expand at 18.12% CAGR through 2031, the fastest pace within the solution mix. EcoVadis and Workiva's May 2026 partnership shows why this category is moving quickly: supplier carbon data is being linked more directly into audit-ready reporting rather than staying in separate procurement systems. Sustainability data management platforms are also becoming increasingly important because agencies need a single environment to bring together accounting, procurement, and operational information without the need for repeated manual consolidation.

Cloud deployment accounted for 65.41% of revenue in 2025, which kept it well ahead of other deployment models in the government and public sector green IT software market. Agencies favor the cloud where possible because subscription delivery can shorten time to compliance and shift rule updates, maintenance, and release management toward the vendor. That matters in public settings, where internal IT teams often face limited capacity and need software that can stay current without extensive reconfiguration. Cloud also fits the wider pattern of government modernization programs that use negotiated procurement channels and approved platforms to accelerate adoption.

Hybrid deployment is projected to grow at 17.95% CAGR during 2026-2031, making it the fastest-rising model as buyers balance compliance speed with control over sensitive data. The European Commission's Sovereign Cloud Framework and France's 2026 directive on reducing extra-European dependencies both support this middle path by raising the bar for where and how public-sector data can be stored and processed. On-premises deployment, therefore, remains relevant for defense, national security, and agencies with strict operational data rules, even if it no longer sets the pace of growth. Vendors that can move data cleanly between local environments and compliant cloud layers are likely to capture a larger share of the government and public sector green IT software market as sovereignty requirements remain in place.

Complete Report Scope:

- By Solution Type

- Carbon Accounting and Reporting Software

- Energy and Power Management Software

- IT Asset Lifecycle Management Software

- Sustainability Data Management Platforms

- Green Procurement and Supplier Sustainability Software

- By Deployment

- Cloud

- On-Premises

- Hybrid

- By End User

- Central and Federal Government

- State and Local Government

- Public Utilities and Public Agencies

- Public Education and Public Healthcare Institutions

- By Application

- Carbon Data Collection and Disclosure

- Energy Optimization and Workload Scheduling

- IT Asset Utilization and Lifecycle Optimization

- Public Procurement and Supplier Emissions Tracking

- Compliance, Audit, and ESG Workflow Automation

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Geography Analysis

Europe accounted for a 34.56% share of the government and public sector green IT software market in 2025, maintaining its lead among regional markets. The region's position is supported by a dense policy landscape in which environmental compliance, procurement controls, and digital governance are advancing together rather than as separate agendas. The European Commission's Sovereign Cloud Framework made environmental sustainability one of the scored dimensions for public cloud procurement while also keeping sovereignty assurance central to adoption decisions. The United Kingdom added further momentum through public procurement and digital sustainability rules that place formal expectations on suppliers and departmental IT operations. As a result, Europe combines broad compliance pressure with procurement systems that can channel spending toward vendors already prepared for public-sector review.

North America was the second-largest regional market for government and public sector green IT software in 2025. In the United States, adoption is being shaped heavily by centralized procurement vehicles, which give large software vendors a faster route into federal estates than one-by-one agency sales. The GSA's OneGov agreement with SAP showed how federal bodies can scale access to analytics, integration, and cloud capabilities through negotiated discounts and common procurement terms. This structure supports volume deployment but also leaves room for specialist tools that provide deeper supplier, asset, or disclosure functionality alongside the main platform.

Asia-Pacific is projected to expand at a 18.45% CAGR during 2026-2031, making it the fastest-growing regional segment in the government and public sector green IT software market. The region is moving from policy planning to implementation, which is broadening demand for carbon accounting, lifecycle tracking, and procurement-oriented reporting tools. NTT Group's March 2026 release of a lifecycle CO2 calculation standard for software reflects a more formal treatment of software-related emissions in advanced Asia-Pacific markets. South America, the Middle East, and Africa are smaller bases today, yet the UAE pilot announced with Khazna, Agility, and the Ministry of Energy and Infrastructure shows that government energy management deployments are moving into active execution outside the two largest regions. This means future expansion outside Europe and North America is likely to begin with targeted public projects and then widen as agencies build internal capacity and procurement familiarity.

- Accenture plc

- Persefoni AI Inc.

- Cority Software Inc.

- Dakota Software Corporation

- Enablon SA

- Enviance, Inc.

- IBM Corporation

- Johnson Controls International plc

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- Schneider Electric SE

- ServiceNow, Inc.

- Siemens AG

- Sphera Solutions, Inc.

- Sustainability Software Group, Inc.

- UL Solutions Inc.

- Workiva Inc.

- Wolters Kluwer N.V.

- Honeywell International Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Digital Modernization Mandates

- 4.2.2 Public Sector Net-Zero Procurement Requirements

- 4.2.3 Rising Utility and Data Center Energy Cost Pressure

- 4.2.4 Shift Toward Sustainability Reporting Automation in Agencies

- 4.2.5 Legacy IT Carbon Visibility Gaps Across Public Institutions

- 4.2.6 Demand for Audit-Ready Carbon Data in Grant-Funded Programs

- 4.3 Market Restraints

- 4.3.1 Fragmented Legacy Procurement and Budget Cycles

- 4.3.2 Data Sovereignty and Public Cloud Approval Constraints

- 4.3.3 Long Software Validation and Change-Management Timelines

- 4.3.4 Limited Internal ESG and Carbon Accounting Skill Depth

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power Of Buyers

- 4.8.2 Bargaining Power Of Suppliers

- 4.8.3 Threat Of New Entrants

- 4.8.4 Threat Of Substitutes

- 4.8.5 Intensity Of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution Type

- 5.1.1 Carbon Accounting and Reporting Software

- 5.1.2 Energy and Power Management Software

- 5.1.3 IT Asset Lifecycle Management Software

- 5.1.4 Sustainability Data Management Platforms

- 5.1.5 Green Procurement and Supplier Sustainability Software

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End User

- 5.3.1 Central and Federal Government

- 5.3.2 State and Local Government

- 5.3.3 Public Utilities and Public Agencies

- 5.3.4 Public Education and Public Healthcare Institutions

- 5.4 By Application

- 5.4.1 Carbon Data Collection and Disclosure

- 5.4.2 Energy Optimization and Workload Scheduling

- 5.4.3 IT Asset Utilization and Lifecycle Optimization

- 5.4.4 Public Procurement and Supplier Emissions Tracking

- 5.4.5 Compliance, Audit, and ESG Workflow Automation

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Persefoni AI Inc.

- 6.4.3 Cority Software Inc.

- 6.4.4 Dakota Software Corporation

- 6.4.5 Enablon SA

- 6.4.6 Enviance, Inc.

- 6.4.7 IBM Corporation

- 6.4.8 Johnson Controls International plc

- 6.4.9 Microsoft Corporation

- 6.4.10 Oracle Corporation

- 6.4.11 SAP SE

- 6.4.12 Schneider Electric SE

- 6.4.13 ServiceNow, Inc.

- 6.4.14 Siemens AG

- 6.4.15 Sphera Solutions, Inc.

- 6.4.16 Sustainability Software Group, Inc.

- 6.4.17 UL Solutions Inc.

- 6.4.18 Workiva Inc.

- 6.4.19 Wolters Kluwer N.V.

- 6.4.20 Honeywell International Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment