|

시장보고서

상품코드

2073190

인도의 의료 콜드체인 물류 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)India Healthcare Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

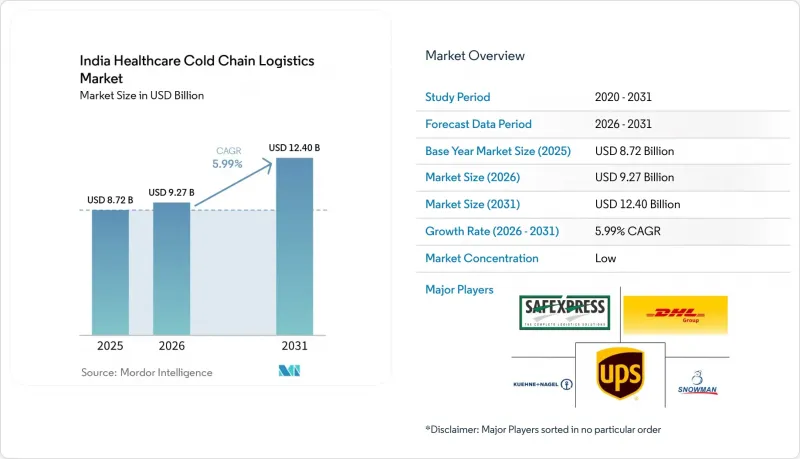

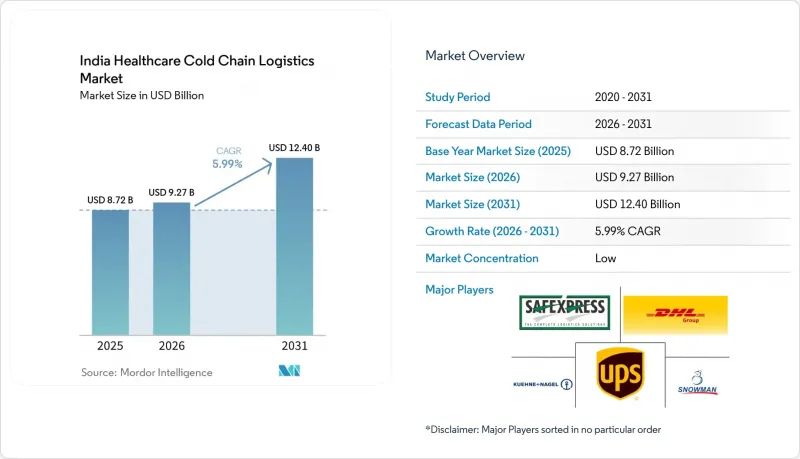

Mordor Intelligence에 의하면, 인도 의료 콜드체인 물류 시장 규모는 2025년 87억 2,000만 달러에서 2026년에는 92억 7,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 5.99%로 성장을 지속하여, 2031년에는 124억 달러에 이를 것으로 예측됩니다.

시장은 의약품의 대량 및 상온 운송에서 백신, 바이오의약품, 특수 주사제 및 기타 온도에 민감한 치료제에 대한 보다 엄격한 취급 방식으로 전환되고 있으며, 이에 따라 검증된 보관, 모니터링이 이루어지는 운송, 그리고 기록된 인계 절차의 중요성이 커지고 있습니다. 본 보고서는 물류 기능별(운송 등), 온도 유형별(냉장, 냉동 등), 제품 유형별(의약품, 바이오의약품 등), 배송지별(국내, 국제), 최종 사용자별(병원 및 진료소 등) 및 지역별(북부, 중부, 서부 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도 의료 콜드체인 물류 시장 동향 및 인사이트

백신 및 예방접종 처리량 확대

인도의 보편적 예방접종 프로그램은 약 30,000곳에 달하는 콜드체인 네트워크와 1.06 lakh대 이상의 냉장·냉동고를 활용하여, 매년 2.9 crore명의 임산부와 2.54 crore명의 신생아를 대상으로 하고 있습니다. 2026년 1월까지 예방접종 완전 접종률은 98.4%에 달했으며, 온도 관리가 이루어지는 유통망이 주요 도시권을 넘어 서비스 제공이 어려운 지역까지 확대되고 있는 것으로 나타났습니다. 또한, 인도는 2026년 2월 28일에 전국적인 HPV 백신 접종 캠페인을 시작함에 따라, 이미 서비스 수준이 한계에 다다른 상황에서 공공 콜드체인에 새로운 계획 수요가 추가되게 되었습니다. eVIN 및 U-WIN의 확대를 통해 재고 가시성, 세션 계획, 유통 관리가 개선되어 인도 의료 콜드체인 물류 시장 전반에 걸쳐 물류 이동의 예측 가능성이 높아지고, 공중보건 서비스에서 발생할 수 있는 온도 관련 위험이 감소할 것입니다. 이러한 수요는 인도의 의료 콜드체인 물류 시장의 민간 부문에도 중요합니다. 왜냐하면 백신 관련 자산은 캠페인이 절정에 달하지 않은 시기에도 인접한 의약품 운송을 지원하는 경우가 많기 때문입니다.

생물학적 제제 및 바이오시밀러의 확대

저분자 의약품에서 생물학적 제제 및 바이오시밀러로의 전환은 인도의 의료 콜드체인 물류 시장에서 자본 배분 방식을 변화시키고 있습니다. 왜냐하면 이러한 치료제는 보관, 취급, 운송의 각 단계에서 보다 엄격한 관리가 필요하기 때문입니다. 대부분의 바이오시밀러는 2℃에서 8℃ 사이의 제어된 온도 조건이 필요합니다. 즉, 철저한 온도 관리는 단순한 유통상의 선호 사항이 아니라 제품 품질의 일부가 된 것입니다. 이 때문에 검증된 운송 경로, 지속적인 모니터링, 감사 대응이 가능한 문서를 제공할 수 있는 GDP 준수 업체에 대한 수요가 증가하고 있는 반면, 소규모이며 전문성이 부족한 업체들은 복잡한 의료 관련 계약 시장에서 점점 더 배제되고 있습니다. 또한, 이러한 추세는 하이데라바드, 벵갈루루, 푸네, 아메다바드에서도 수요를 견인하고 있으며, 이들 지역에서는 의료 물류 업체들이 바이오의약품 생산·수출 거점 근처에 인증된 물류 역량을 구축하고 있습니다. 이러한 변화가 진행됨에 따라, 인도의 의료 콜드체인 물류 시장은 고부가가치의 규정 준수 부문과 저부가가치의 기존 부문으로 양분되고 있으며, 가격 결정권은 점점 더 전자의 그룹에 집중되고 있습니다.

GDP 기준 설비 투자와 에너지 비용 부담

GDP 기준을 준수하는 의약품 콜드체인 인프라에는 검증된 매핑, 이중 전원 공급 장치, 지속적인 로그 기록, 편차 대응에 대한 문서화, 그리고 철저한 시스템 관리가 필요하지만, 많은 소규모 사업자들은 여전히 자금 조달에 어려움을 겪고 있습니다. 인도의 3,500개 이상의 콜드체인 사업자 중 현재 GDP 규정 준수 기준을 충족하는 곳은 불과 8%에서 10%에 불과하며, 고객 요구 사항이 더욱 엄격해지고 있음에도 불구하고 업계 기반이 여전히 얼마나 불균형한지를 보여주고 있어, 이러한 부담은 더욱 심각해지고 있습니다. 이로 인해 인도의 의료 콜드체인 물류 시장에 대한 진입 장벽이 높아지면서, 설비, 모니터링 시스템, 공정 제어에 대규모 자금을 투입할 수 있는 대형 사업자들에게 시장 점유율이 이동하고 있습니다. 또한, 많은 2급 및 3급 도시의 경우, 초기 단계에서 고비용의 규정 준수 대응 자산을 도입할 만한 수익을 기대하기 어렵기 때문에 이러한 지역으로의 사업 확장도 제한되고 있습니다. 단기적인 효과로 주요 물류 회랑의 평균 품질은 향상되겠지만, 그 대가로 제약 업계와 병원이 집중된 주요 지역 이외의 인도 의료 콜드체인 물류 시장의 지리적 확장은 둔화될 것입니다.

부문별 분석

2025년, 운송 부문은 인도 의료 콜드체인 물류 시장 점유율의 52.47%를 차지하며, 계속해서 최대 기능 블록으로서의 지위를 유지했습니다. 의약품 운송의 경우, 병원, 유통업체, 공장, 지역 재고 거점 간을 유연하게 연결하는 포인트-투-포인트 배송이 여전히 필요하기 때문에 도로 운송이 이 부문의 핵심으로 자리 잡고 있습니다. 도로 운송의 강점은 인도의 광활한 지리적 범위와, 항공이나 철도로는 직접 서비스를 제공할 수 없는 소규모 소비 거점에 대한 접근성이 필요하다는 점에 기인합니다. GPS 추적 기능과 데이터 로거를 갖춘 냉장 트럭은 운송 경로의 가시화와 운송 중 온도 관리 기록을 모두 지원하기 때문에 이 운영 모델에서 여전히 핵심적인 역할을 수행하고 있습니다. 이는 고객들이 서비스 품질에 대해 더욱 까다로워지고 있음에도 불구하고, 운송 규모가 여전히 인도 의료 콜드체인 물류 시장의 운송량 기반을 결정하고 있음을 의미합니다. 하이데라바드와 뭄바이를 연결하는 마스쿠의 전용 냉장 철도 서비스는 일정과 컨테이너 규격이 신뢰할 수 있는 경우, 온도 관리가 필요한 의약품 운송을 복합 운송 계획에 통합할 수 있음을 보여주었습니다. 따라서 운송은 여전히 인도 의료 분야 콜드체인 물류 산업의 기반을 이루고 있으며, 한편으로는 운송 수단의 다양화로 인해 네트워크의 깊이가 점차 향상되고 있습니다.

부가가치 서비스는 가장 빠르게 성장하고 있는 분야로, 2031년까지 연평균 성장률(CAGR) 6.74%를 기록하며 확대되고 있습니다. 이는 서비스의 구성이 단순한 운송이나 보관을 넘어 변화하고 있음을 보여줍니다. 고객들은 추적 및 추적 가능성, 디지털 온도 증명서, 위험 경고, 통제된 환경에서의 재포장, 그리고 규격 편차 발생 시 지원 등을 점점 더 요구하고 있습니다. 이러한 기능 덕분에 감사가 간소화되고, 사내 품질 관리 팀의 부담이 줄어들기 때문입니다. 벵갈루루와 하이데라바드에 위치한 퀴네 앤 나겔(Kuehne+Nagel)의 “HealthChain” 인증 시설은 이러한 방향성을 반영하고 있으며, 해당 기업은 관리형 보관 및 크로스독 기능을 보다 광범위한 헬스케어 서비스 패키지에 통합하고 있습니다. 이로 인해, 단순히 간선 운송 가격만으로 경쟁하는 것이 아니라, 민감한 제품의 물류 흐름을 중심으로 여러 서비스를 묶어 제공할 수 있는 사업자에게는 이익률 향상 가능성이 높아지고 있습니다. 실제로 부가가치 서비스는 인도 의료 콜드체인 물류 시장에서 가장 뚜렷한 차별화 요소 중 하나로 자리 잡고 있습니다.

2-8℃의 냉장 보관은 2025년 인도 의료 콜드체인 물류 시장 점유율의 46.11%를 차지하며 주요 온도대가 되었습니다. 이러한 주도적 지위는 백신, 인슐린 및 많은 기존 생물학적 제제와 같이 일상적으로 이 온도 범위 내에서 반복적으로 운송되는 제품군의 존재를 반영하고 있습니다. 또한, 냉장 온도대는 창고, 병원, 유통 거점에 널리 도입되어 있다는 장점도 있어, 의료 분야를 폭넓게 아우르는 데 있어 가장 실용적인 온도 등급입니다. 많은 필수 치료제가 이 온도 요건 범위 내에 속하기 때문에 냉장 취급이야말로 인도 의료 콜드체인 물류 시장의 수익 기반이 되고 있습니다. 또한, 이러한 점은 신규 사업자가 초기 인프라 구축이나 노선 설계에 있어 어떤 우선순위를 정할지를 좌우하는 요인이 되기도 합니다.

영하 18℃에서 0℃ 사이의 냉동 보관 시장은 2031년까지 연평균 성장률(CAGR) 9.91%를 나타낼 것으로 예측되며, 가장 성장세가 두드러지는 온도 구간입니다. 이러한 성장은 의약품 구성의 근본적인 변화를 시사하며, 바이오시밀러 주사제, 단일클론 항체, 혈장 유래 제품이 가치 측면에서 더 큰 역할을 담당하게 되고 있습니다. 따라서 냉동 부문은 인도의 의료 콜드체인 물류 시장에서 전문성이 더욱 요구되는 분야로, 보다 엄격한 공정 관리와 더욱 철저한 고객 선별이 필요합니다. 냉동 제품 수요가 확대됨에 따라, 사업자들은 보관 및 운송 양쪽 모두에서 더 뛰어난 단열 성능, 더 엄격한 적재 절차, 그리고 더 고성능의 경보 대응 시스템을 필요로 하게 됩니다. 그 결과, 인도의 의료 콜드체인 물류 시장 전체에서 온도대 구성은 운영 부담이 큰 방향으로 꾸준히 변화하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.07According to Mordor Intelligence, the india healthcare cold chain logistics market size is expected to grow from USD 8.72 billion in 2025 to USD 9.27 billion in 2026 and is forecast to reach USD 12.40 billion by 2031 at 5.99% CAGR over 2026-2031.

The market is shifting from bulk, ambient drug movement toward more controlled handling for vaccines, biologics, specialty injectables, and other temperature-sensitive therapies, which is raising the value of validated storage, monitored transport, and documented handoffs. This report is Segmented by Logistics Function (Transportation, and More), by Temperature Type (Chilled, Frozen, and More), by Product Type (Pharmaceuticals, Biopharmaceuticals, and More), by Destination (Domestic, International), by End User (Hospitals & Clinics, and More), and by Geography (North, Central, West, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Healthcare Cold Chain Logistics Market Trends and Insights

Vaccine and Immunization Throughput Expansion

India's Universal Immunization Program covers 2.9 crore pregnant women and 2.54 crore newborns each year through a cold chain network spanning nearly 30,000 points and using more than 1.06 lakh ice-lined refrigerators and deep freezers. Full immunization coverage reached 98.4% by January 2026, demonstrating that temperature-controlled distribution has extended beyond the main urban corridors into harder-to-serve districts. India also launched a nationwide HPV vaccination campaign on February 28, 2026, adding a new layer of planned volume to the public cold chain at a time when service levels are already under pressure. The expansion of eVIN and U-WIN improves stock visibility, session planning, and distribution control, which supports more predictable movement across the India healthcare cold chain logistics market and reduces avoidable temperature risk in public health delivery. This demand is also important for the private side of the India healthcare cold chain logistics market because vaccine-linked assets often support adjacent pharmaceutical loads when campaigns are not at peak intensity.

Biologics and Biosimilars Scale-Up

The move from small-molecule medicines toward biologics and biosimilars is changing how the India healthcare cold chain logistics market allocates capital, because these therapies need tighter control during storage, handling, and movement. Most biosimilars depend on controlled 2 °C to 8 °C conditions, which means temperature integrity becomes part of product quality rather than a distribution preference. This is pushing more business toward GDP-capable operators that can offer validated lanes, continuous monitoring, and audit-ready documentation, while smaller non-specialized operators face growing exclusion from complex healthcare contracts. It is also driving demand in Hyderabad, Bengaluru, Pune, and Ahmedabad, where healthcare logistics providers are building certified capacity near biopharma production and export nodes. As that shift continues, the India healthcare cold chain logistics market is separating into a higher-value compliance tier and a lower-value conventional tier, with pricing power increasingly concentrated in the first group.

GDP-Grade Capex and Energy Cost Burden

GDP-grade pharmaceutical cold infrastructure requires validated mapping, redundant power, continuous logging, documented deviation handling, and system discipline that many smaller operators still struggle to fund. The burden is more severe because only 8% to 10% of India's 3,500-plus cold chain operators currently meet GDP compliance benchmarks, which shows how uneven the base has remained even as customer requirements tighten. This raises barriers to entry in the India healthcare cold chain logistics market and shifts share toward larger operators that can finance equipment, monitoring systems, and process control at scale. It also limits expansion into smaller cities, because the revenue available in many Tier-2 and Tier-3 locations does not always justify high-cost compliant assets during the early years. The near-term effect is better average quality in major corridors, but the tradeoff is slower geographic spread for the India healthcare cold chain logistics market outside the strongest pharmaceutical and hospital clusters.

Other drivers and restraints analyzed in the detailed report include:

- Pharma Export Cold-Chain Compliance Demand

- Specialty Injectables and Clinical-Trial Flow Growth

- Rural Last-Mile and Multimodal Cold Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation held 52.47% of the India healthcare cold chain logistics market share in 2025, which kept it as the largest functional block. Road transport remains the core of that segment because pharmaceutical shipments still require flexible point-to-point delivery across hospitals, distributors, plants, and regional stock points. The strength of road movement reflects India's geographic spread and the need to reach smaller consumption centers that air and rail cannot directly serve. Reefer trucks equipped with GPS tracking and data loggers remain central to this operating model because they support both route visibility and documented temperature control during transit. This means transport scale still sets the volume base for the India healthcare cold chain logistics market, even as customers become more selective about service quality. Maersk's dedicated reefer rail service from Hyderabad to Mumbai showed that temperature-controlled pharmaceutical movement can be integrated into multimodal planning when schedules and container standards are reliable. Transportation, therefore, continues to anchor the India healthcare cold chain logistics industry, while modal diversification slowly improves network depth.

Value-added services are the fastest-growing function, expanding at a 6.74% CAGR through 2031, which shows how the service mix is shifting beyond pure movement or storage. Customers increasingly want track-and-trace, digital temperature certificates, risk alerts, repackaging under controlled conditions, and support during deviations, because those features simplify audits and reduce the burden on internal quality teams. Kuehne+Nagel's HealthChain-certified setup in Bengaluru and Hyderabad reflects this direction, as the company has tied controlled storage and cross-dock capability into a broader healthcare service package. This is improving margin potential for operators that can bundle multiple services around sensitive product flows rather than compete only on line-haul price. In practice, value-added services are becoming one of the clearest differentiators inside the India healthcare cold chain logistics market.

Chilled storage at 2 °C to 8 °C accounted for 46.11% of the India healthcare cold chain logistics market share in 2025, which made it the leading temperature band. That leadership reflects the daily operating base of vaccines, insulin, and many conventional biologics, all of which move through this range on a recurring basis. The chilled band also benefits from a wider installed base across warehouses, hospitals, and distribution points, which makes it the most practical temperature class for broad healthcare coverage. Because so many essential therapies sit within this temperature requirement, chilled handling remains the revenue foundation of the India healthcare cold chain logistics market. It also shapes how new operators prioritize their initial infrastructure and route design.

Frozen storage from minus 18 °C to 0 °C is projected to grow at a 9.91% CAGR through 2031, which makes it the fastest-moving temperature type. This growth points to a deeper change in pharmaceutical mix, where biosimilar injectables, monoclonal antibodies, and plasma-derived products are taking a larger role in value terms. The frozen segment, therefore, represents a more specialized layer of the India healthcare cold chain logistics market, one that demands stronger process discipline and more selective customer qualification. As frozen products grow, operators will need better insulation, tighter loading practices, and more capable alarm-response systems across both storage and movement. The result is a temperature mix that is steadily shifting toward higher operational intensity across the India healthcare cold chain logistics market.

Complete Report Scope:

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing and Distribution

- Value-added Services and Others

- Transportation

- By Temperature Type

- Chilled (0-5 °C)

- Frozen (-18-0 °C)

- Ambient

- Deep-Frozen / Ultra-Low (less than-20 °C)

- By Product Type

- Pharmaceuticals

- Prescription and Speciality Drugs

- OTC Drugs

- Biopharmaceuticals (Biologics and Biosimilars)

- Vaccines

- Clinical Trail Materials

- Cell and Gene Therapies

- Medical Devices

- Veterinary Medicine

- Blood, Plasma and Blood Components

- Diagnostic and Laboratory Products

- Organs and Human Tissues

- Others

- Pharmaceuticals

- By Destination

- Domestics

- International

- By End User

- Pharmaceutical Manufacturers

- Biopharmaceutical Manufacturers

- Hospitals and Clinics

- Hospitals and Retail Pharmacies

- Healthcare Distributors and Wholesalers

- Others

- By Region

- North

- Central

- West

- East

- South

List of Companies Covered in this Report:

- DHL Group

- United Parcel Service of America, Inc. (UPS)

- Kuehne+Nagel

- Snowman Logistics

- Safexpress Pvt. Ltd.

- DSV A/S (Including DB Schenker)

- FedEx

- Celcius Logistics

- Indicold

- Allcargo Gati Logistics Pvt. Ltd.

- Mahindra Logistics, Ltd.

- Transport Corporation of India, Ltd.

- Container Corporation of India, Ltd.

- Coldman Logistics

- Parazelsus India

- Glacias Supply Chain

- World Courier

- Biocair India

- NYK Line (Including Yusen Logistics)

- Jeena Criticare Logistics

- Airfield Express

- Harisons Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview and Role of Cold Chain Logistics in Healthcare

- 4.2 Healthcare Spending Trends

- 4.3 Market Drivers

- 4.3.1 Vaccine and Immunization Throughput Expansion

- 4.3.2 Biologics and Biosimilars Scale-Up

- 4.3.3 Pharma Export Cold-Chain Compliance Demand

- 4.3.4 Specialty Injectables and Clinical-Trial Flow Growth

- 4.3.5 Evin and U-WIN Demand-Visibility Gains

- 4.3.6 Emerging Cell and Gene Therapy Lanes

- 4.4 Market Restraints

- 4.4.1 GDP-Grade Capex and Energy Cost Burden

- 4.4.2 Rural Last-Mile and Multimodal Cold Gaps

- 4.4.3 GDP-Trained Talent and SOP Shortages

- 4.4.4 Heat Stress and Backup-Power Vulnerability

- 4.5 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Architecture Analysis

- 4.7 Technology Innovations Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Competitors

- 4.9 Evolution of Healthcare Cold Chain Logistics Requirements

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts

- 5.1 By Logistics Function

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea and Inland Waterways

- 5.1.1.4 Rail

- 5.1.2 Warehousing and Distribution

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Temperature Type

- 5.2.1 Chilled (0-5 °C)

- 5.2.2 Frozen (-18-0 °C)

- 5.2.3 Ambient

- 5.2.4 Deep-Frozen / Ultra-Low (less than-20 °C)

- 5.3 By Product Type

- 5.3.1 Pharmaceuticals

- 5.3.1.1 Prescription and Speciality Drugs

- 5.3.1.2 OTC Drugs

- 5.3.2 Biopharmaceuticals (Biologics and Biosimilars)

- 5.3.3 Vaccines

- 5.3.4 Clinical Trail Materials

- 5.3.5 Cell and Gene Therapies

- 5.3.6 Medical Devices

- 5.3.7 Veterinary Medicine

- 5.3.8 Blood, Plasma and Blood Components

- 5.3.9 Diagnostic and Laboratory Products

- 5.3.10 Organs and Human Tissues

- 5.3.11 Others

- 5.3.1 Pharmaceuticals

- 5.4 By Destination

- 5.4.1 Domestics

- 5.4.2 International

- 5.5 By End User

- 5.5.1 Pharmaceutical Manufacturers

- 5.5.2 Biopharmaceutical Manufacturers

- 5.5.3 Hospitals and Clinics

- 5.5.4 Hospitals and Retail Pharmacies

- 5.5.5 Healthcare Distributors and Wholesalers

- 5.5.6 Others

- 5.6 By Region

- 5.6.1 North

- 5.6.2 Central

- 5.6.3 West

- 5.6.4 East

- 5.6.5 South

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 United Parcel Service of America, Inc. (UPS)

- 6.4.3 Kuehne+Nagel

- 6.4.4 Snowman Logistics

- 6.4.5 Safexpress Pvt. Ltd.

- 6.4.6 DSV A/S (Including DB Schenker)

- 6.4.7 FedEx

- 6.4.8 Celcius Logistics

- 6.4.9 Indicold

- 6.4.10 Allcargo Gati Logistics Pvt. Ltd.

- 6.4.11 Mahindra Logistics, Ltd.

- 6.4.12 Transport Corporation of India, Ltd.

- 6.4.13 Container Corporation of India, Ltd.

- 6.4.14 Coldman Logistics

- 6.4.15 Parazelsus India

- 6.4.16 Glacias Supply Chain

- 6.4.17 World Courier

- 6.4.18 Biocair India

- 6.4.19 NYK Line (Including Yusen Logistics)

- 6.4.20 Jeena Criticare Logistics

- 6.4.21 Airfield Express

- 6.4.22 Harisons Logistics

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment