|

시장보고서

상품코드

2073197

비강내 확장기 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Internal Nasal Dilators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

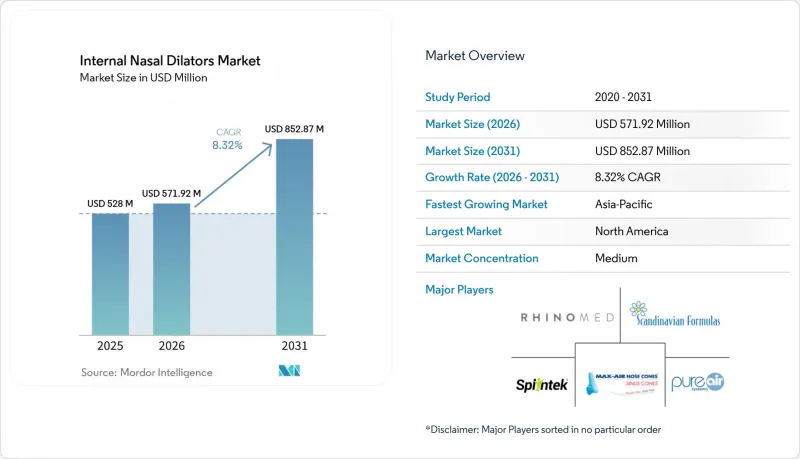

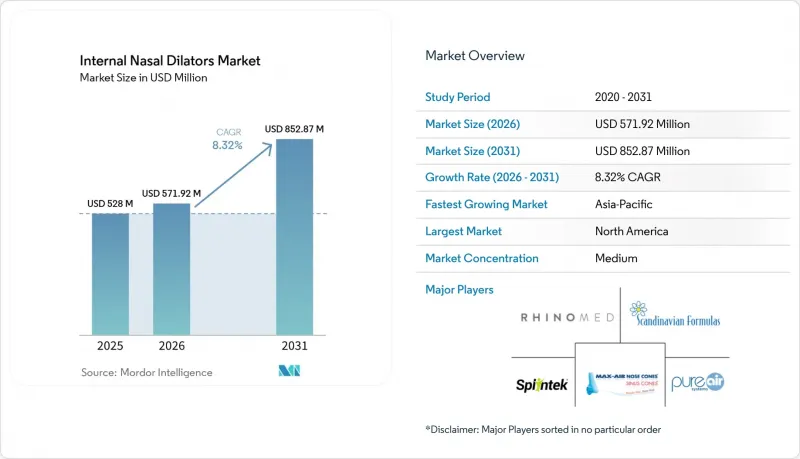

Mordor Intelligence에 의하면, 비강내 확장기 시장 규모는 2025년에 5억 2,800만 달러로 평가되었고 2026년 5억 7,192만 달러에서 2031년까지 8억 5,287만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 8.32%를 나타낼 전망입니다.

본 보고서는 제품 유형(폴리머, 폴리머 및 합금, 기타 제품 유형), 사용 편의성(재사용 가능, 일회용), 용도(코골이, 수면 무호흡증, 비강 중격 만곡증, 코막힘, 기타), 판매 채널(병원, 소매, 온라인 약국, 기타) 및 지역(북미, 유럽, 아시아태평양, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 비강내 확장기 시장 동향 및 인사이트

수면 관련 호흡 장애의 유병률 증가

비강내 확장기 시장은 수면 호흡 장애를 앓고 있음에도 불구하고 정식 진단 절차를 거치지 않은 많은 사람들이 존재한다는 점을 배경으로 성장세를 보이고 있습니다. 분석에 따르면, 폐쇄성 수면무호흡증 증례의 80-90%는 어느 시점에서도 진단받지 못한 채 남아 있으며, 이로 인해 일반 의료기기 부문에서 자가 치료 행위의 중요성이 여전히 유지되고 있습니다. 2025년 『Nature Communications』지에 게재된 연구는 주변 온도 상승이 상기도 폐쇄를 악화시켜, 시간이 지남에 따라 폐쇄성 수면 무호흡증의 중증도를 높일 가능성이 있음을 보여줌으로써 새로운 관점을 제시했습니다. 이 발견은 수요의 주요 요인을 고령화나 비만이라는 틀을 넘어 확장시키고, 야간 호흡 장애를 보다 광범위한 환경적 요인과 연관시킨다는 점에서 중요합니다. 중국과 인도는 확진자 수가 매우 많고, 전문의의 진료를 받기 전에 간편한 일반 의약품을 시도하는 경향이 강한 소비자가 많기 때문에 여전히 특히 중요한 시장으로 남아 있습니다. 따라서 비강내 확장기 시장은 진단을 받은 환자뿐만 아니라, 코막힘, 코골이, 호흡 시 불편함을 스스로 관리하고 있는 재구매 고객층과도 밀접하게 연결되어 있습니다.

약물을 사용하지 않는 비침습적 호흡 보조 기기에 대한 수요

비강내 확장기 시장은 장기간에 걸쳐 의약품에 의존하지 않고 기류 지원을 원하는 소비자들로부터 계속해서 혜택을 보고 있습니다. 기계적 확장은 비판막의 물리적 폐쇄를 해결하며, 리바운드 효과, 피부용 접착제 또는 일상적인 약물 사용에 따른 우려를 피할 수 있게 해줍니다. 21 CFR 874.3900에 따라, 비강내 확장기는 클래스 I 의료기기로 분류되며 시판 전 신고가 면제되므로, 약물 기반 비강 치료에 비해 상품화 장벽이 낮습니다. 2024년 미국정신의학회 보고서에 따르면, 미국인의 34%가 자신의 수면의 질을 “나쁘다” 또는 “그럭저럭”라고 평가하고 있으며, 5,000만 명 이상의 미국인이 만성 수면장애로 고통받고 있는 것으로 나타났습니다. 이는 비약물적 수면 지원 도구에 대한 소비자들의 폭넓은 관심을 뒷받침하는 것입니다. 또한, 체내에 삽입하는 형태의 제품은 접착 테이프로 인한 피부 자극 문제를 피할 수 있습니다. 이는 특히 재사용 가능한 제품을 선호하는 단골 고객들에게 있어, 치료 지속률 저하의 원인이 됩니다. 이러한 이유로, 체내에 삽입하는 비강내 확장기 시장에서는 일회성 구매의 편의성보다 착용감, 내구성, 매일 밤의 지속적인 사용을 중시하는 프리미엄 고객층이 형성되어 있습니다.

제품 착용 시 불편함과 착용감의 편차

비강내 확장기 시장은 여전히 보급에 있어 큰 장벽에 직면해 있습니다. 이는 기기의 착용감이 각 개인의 콧구멍 모양과 밀착도에 크게 좌우되기 때문입니다. 콧구멍의 구조에 미세한 차이만 있어도 수면 중 압력을 느끼는 방식이 달라지기 때문에 처음 사용 시 경험이 좋지 않았을 경우 다른 많은 시판 제품군보다 더 심각한 악영향을 미칩니다. EC 플랫폼에서 흔히 언급되는 구매 취소 사유로는 비강 내 압력, 밤중에 착용 위치가 어긋나는 것, 콧털과의 접촉으로 인한 자극 등이 있습니다. 다양한 사이즈 출시와 핏 조절 기능을 통해 각 브랜드는 이러한 문제들을 완화하고 있지만, 이 카테고리가 안고 있는 근본적인 핏 문제는 여전히 해결되지 않고 있습니다. 비강내 확장기 시장에서는 임상적 지도나 대면 피팅 없이 구매되는 경우가 많기 때문에 이 과제는 더욱 중요해집니다. 맞춤형 착용감을 실현하는 방식이 널리 보급되고 합리적인 가격대가 될 때까지는 착용감이 좋지 않다는 점이 재구매, 지인 추천, 그리고 장기적인 습관 형성을 계속해서 저해할 가능성이 있습니다.

부문별 분석

2025년에는 순수 폴리머 소재 장치가 해당 부문의 65.31%를 차지했으나, 2031년까지 연평균 성장률(CAGR) 9.38%를 기록하며 폴리머·합금 소재 장치가 가장 빠른 성장세를 보일 것으로 전망됩니다. 순수 폴리머는 대규모 생산이 용이하고, 일회용 제품이나 기본적인 재사용 가능 제품에서 저렴한 가격을 실현할 수 있기 때문에 여전히 광범위한 시장 점유율을 유지하고 있습니다. 이러한 가격의 접근성은 비강내 확장기 시장에서 중요한 요소입니다. 왜냐하면, 많은 첫 구매는 의료적 목적을 위한 확고한 의지에 따른 구매라기보다는 시험 사용 목적으로 이루어지기 때문입니다. 또한, 장기간 착용 시의 쾌적성이나 고급감보다는 단위당 비용이 저렴한 점이 더 중요시되는 단기 사용의 경우, 폴리머 제품도 여전히 널리 사용되고 있습니다. 따라서 2025년 비강내 확장기 시장에서 순수 폴리머 제품의 점유율이 높은 수준을 유지한 것은 대형 유통업체와 가성비를 중시하는 구매자들의 요구에 부합했기 때문입니다.

폴리머 및 합금 제품은 더 뛰어난 형상 기억성, 더 안정적인 신장력, 그리고 야간 사용 시의 쾌적성 향상을 강점으로 내세우고 있어 더욱 빠르게 성장하고 있습니다. 이러한 프리미엄 포지셔닝은 이미 기본 제품을 사용해 본 적이 있으며, 더 안정적인 사용감을 제공하는 재사용 가능한 제품에 대해 더 높은 가격을 지불할 의향이 있는 소비자에게 적합합니다. 또한, 이 부문은 일시적인 증상 완화가 아닌 매일 밤 지속적으로 사용할 수 있는 제품으로의 광범위한 전환 추세와도 부합합니다. 그 밖의 제품 유형은 판매량은 적지만, 임상용 콘이나 CPAP 보조용 제품은 평균 판매 가격을 끌어올릴 수 있기 때문에 중요한 위치를 차지하고 있습니다. 장기적으로, 비강내 확장기 시장에서 순수 폴리머 제품은 판매량 측면에서 기반을 유지하는 한편, 합금 혼합 제품은 업그레이드 수요를 통해 가치 측면에서 더 큰 점유율을 확보해 나갈 것으로 전망됩니다.

2025년에는 재사용 가능한 기기가 “사용 편의성” 부문의 59.24%를 차지하며, 2031년까지 연평균 성장률(CAGR) 10.52%로 성장할 것으로 전망됩니다. 이는 주류 포맷이 동시에 가장 빠르게 성장하는 포맷이기도 하다는 점에서 중요하며, 이는 좁은 프리미엄 틈새 시장이 아니라 폭넓은 수용을 시사합니다. 비강내 확장기 시장은 재사용 가능한 제품의 경제성 덕분에 호황을 누리고 있습니다. 12-25달러짜리 1개 단위로 수주에서 수개월간 사용할 수 있어, 일회용 제품을 반복해서 구매하는 경우에 비해 고객이 느끼는 가치가 높아지기 때문입니다. 이러한 가치 논리는 습관 형성을 뒷받침하며, 매일 밤 꾸준히 사용해야 하는 이 카테고리에서 습관 형성은 중요한 요소가 됩니다. 또한, 재사용이 가능한 기기는 피부에 접착제가 닿는 것을 피할 수 있어, 장기간 사용하는 사용자에게는 더욱 실용적으로 느껴진다는 점도 이 부문의 장점입니다.

일회용 제품은 병원에서의 사용, 코 성형술 후 관리, 그리고 재사용 가능한 제품으로 전환하기 전에 크기와 착용감을 확인해 보고자 하는 소비자들이 이용하는 첫 체험 팩에서 여전히 중요한 역할을 하고 있습니다. WoodyKnows사는 2024년, 첫 구매 단계에서 구매 포기를 줄이는 것을 목표로 여러 사이즈의 체험 팩을 제공함으로써 이 논리를 강조했습니다. 이러한 접근 방식은 비강내 확장기 시장의 전반적인 실태를 반영하고 있습니다. 왜냐하면 초기 착용감이 좋지 않은 것은 이 카테고리에서 이탈하게 되는 가장 큰 이유 중 하나이기 때문입니다. 또한, 재사용 가능한 제품은 구독 및 리필 생태계에도 적합합니다. 이러한 시스템에서는 액세서리, 교체 주기, 정기적인 내원이 고객 유지율 향상에 기여합니다. 그 결과, 일회용 제품이 도입 및 임상 용도를 뒷받침하고, 재사용 가능한 제품이 장기적인 수익 기반의 대부분을 차지하는 사용 편의성 측면에서의 균형이 이루어지고 있습니다.

지역별 분석

2025년, 북미는 비강내 확장기 시장의 45.22%를 차지하며 다른 지역을 크게 앞지르고 최대 지역 시장이 되었습니다. 이 지역은 수면장애에 대한 높은 인지도와 진단율, 그리고 체험 구매와 재구매를 뒷받침하는 성숙한 일반의약품 판매 네트워크의 혜택을 누리고 있습니다. Rhinomed사는 2024년, 자사의 ‘Mute Nasal Dilator”가 미국 내 4,500개 이상의 CVS 매장과 1,500개 이상의 월그린스 매장에서 진열 공간을 확보함으로써, 이 판매 경로의 강점을 입증했습니다. 이러한 체인점에 제품을 도입하는 것은 전문성이 높은 제품을 폭넓은 소비자에게 알리고, 일상적인 소매 환경에서 해당 카테고리를 정착시키는 데 중요합니다. 캐나다와 멕시코는 이 지역 내에서 여전히 시장 규모가 작지만, 디지털 약국에 대한 접근성이 개선되고 있으며, 실용적인 비약물적 호흡 지원에 대한 소비자의 선호도가 유사하다는 점에서 두 나라 모두 성장이 예상됩니다.

유럽은 비강내 확장기 시장에서 여전히 2위의 규모를 자랑하며, 독일, 영국, 프랑스가 주요 성장 동력으로 작용하고 있습니다. 이 국가들에서는 약물을 사용하지 않는 호흡 보조 장치에 대한 소비자의 인지도가 충분히 자리 잡았으며, 이것이 가성비 제품과 프리미엄 제품 모두에 대한 꾸준한 수요를 뒷받침하고 있습니다. 또한, 유럽의 온라인 약국 기반은 특히 매장 진열대 공간에 전적으로 의존하지 않는 전문 브랜드의 경우, 해당 카테고리의 성장을 가속화하는 요인이 되고 있습니다. 2025년 Redcare Pharmacy의 활성 고객 수 1,390만 명과 2026년의 성장 전망은 유럽 내 디지털 채널의 높은 보급률을 보여주고 있습니다. 이로 인해 유럽은 북미에서 볼 수 있는 대규모 소매점 진출 없이도 디지털 유통을 통해 시장 영향력을 확대할 수 있는 안정적인 지역이 되었습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 9.15%를 나타낼 것으로 예측되는 가장 빠르게 성장하는 지역이며, 이 지역의 비강내 확장기 시장 규모는 매우 큰 미충족 수요 기반에 힘입어 성장하고 있습니다. 중국은 폐쇄성 수면무호흡증 환자의 절대 수가 가장 많기 때문에 여전히 중심적인 위치를 차지하고 있으며, 2025년 『Nature Communications』지에 실린 연구에 따르면 기온 상승이 이 질환의 중증도를 악화시켜 향후 부담을 가중시킬 가능성이 있는 것으로 나타났습니다. 인도에서는 디지털 약국의 성장, 건강에 대한 인식 제고, 그리고 수면 관련 제품에 대한 지출 의향이 높은 도시 중산층의 부상으로 인해 도입이 급속히 확대될 전망입니다. 일본과 한국은 보다 꾸준한 성장세를 보이고 있지만, 이 시장의 소비자들은 의학적으로 입증된 제품이나 편의성을 중시하는 경향이 있어 프리미엄 기기에 대한 잠재적 수요가 더 높다고 할 수 있습니다. 남미 및 중동 및 아프리카(MEA) 지역은 여전히 시장 규모가 작은 편이지만, 남미에서는 브라질과 아르헨티나가 주도적인 역할을 하고 있으며, MEA 지역에서는 GCC 국가들이 가장 뚜렷한 수요를 보이고 있습니다. 이는 비만과 관련된 수면장애의 경향이 각 지역의 건강 통계에서 구조적인 호재로 작용하고 있기 때문입니다. 현재 비강내 확장기 시장 점유율은 여전히 북미에 집중되어 있지만, 중기적인 성장 동향은 아시아태평양과 주요 선진국 시장 이외의 특정 본인 부담형 도시권에 의해 점차 형성되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.07According to Mordor Intelligence, the internal nasal dilators market size was valued at USD 528 million in 2025 and is estimated to grow from USD 571.92 million in 2026 to reach USD 852.87 million by 2031, at a CAGR of 8.32% during the forecast period (2026-2031).

This report is Segmented by Product Type (Polymer, Polymer and Alloy, Other Product Types), Usability (Reusable, Single Use), Application (Snoring, Sleep Apnea, Deviated Septum, Nasal Congestion, Other), Distribution Channel (Hospital, Retail, Online Pharmacies, Other), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Internal Nasal Dilators Market Trends and Insights

Rising Prevalence Of Sleep-Related Breathing Disorders

The internal nasal dilators market is drawing strength from the large pool of people who live with sleep-disordered breathing but remain outside formal diagnosis pathways. The analysis notes that 80-90% of obstructive sleep apnea cases are undiagnosed at any given time, which keeps self-treatment behavior important for over-the-counter device categories. A 2025 Nature Communications study added a new layer by showing that rising ambient temperatures can worsen upper-airway collapsibility and increase obstructive sleep apnea severity over time. That finding matters because it extends demand drivers beyond aging and obesity and links nighttime breathing disruption to broader environmental conditions. China and India remain especially important because they carry a very large affected population and have many consumers who are more likely to try simple over-the-counter solutions before seeking specialist care. This keeps the internal nasal dilators market tied not only to diagnosed patients, but also to a recurring base of consumers managing congestion, snoring, and airflow discomfort on their own.

Preference For Drug-Free, Non-Invasive Breathing Aids

The internal nasal dilators market continues to benefit from consumers who want airflow support without depending on medicines for long periods. Mechanical dilation addresses physical restriction at the nasal valve and avoids concerns tied to rebound effects, skin adhesives, or routine pharmacological use. Under 21 CFR 874.3900, nasal dilators are classified as Class I devices that are exempt from premarket notification, which lowers commercialization barriers compared with drug-based nasal therapies. A 2024 American Psychiatric Association report showing that 34% of Americans rated their sleep quality as poor or fair and that more than 50 million Americans suffer from chronic sleep disorders, which supports broad consumer interest in non-drug sleep support tools. Internal devices also avoid the skin irritation issues that can reduce adherence to adhesive strips, especially for repeat users who want a reusable option. This supports a premium tier in the internal nasal dilators market where comfort, durability, and repeat nightly use matter more than single-purchase convenience.

Product Discomfort And Fit Variability

The internal nasal dilators market still faces a meaningful adoption barrier because device comfort depends heavily on individual nostril geometry and fit. Small differences in nasal valve structure can change how pressure is felt during sleep, which makes a poor first experience more damaging than in many other over-the-counter categories. Common abandonment reasons on e-commerce platforms include intranostril pressure, mid-night displacement, and irritation from contact with nasal hair. Multi-size offerings and adjustable geometries are helping brands reduce these issues, yet they have not removed the category's core fit challenge. That challenge matters even more in the internal nasal dilators market because purchases are often made without clinical guidance or in-person fitting. Until personalized-fit approaches become widely affordable, weak fit can continue to suppress repurchase, referral, and long-term habit formation.

Other drivers and restraints analyzed in the detailed report include:

- Growth Of Direct-To-Consumer And Online Pharmacy Channels

- Rising Clinical Interest In CPAP Adjunct And Nasal Airflow Support

- Reimbursement Gaps And Consumer Out-Of-Pocket Sensitivity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pure polymer devices held 65.31% of the segment in 2025, while polymer and alloy is projected to record the fastest growth at a 9.38% CAGR through 2031. Pure polymer keeps a large installed base because it is easy to manufacture at scale and it supports lower price points for single-use or basic reusable products. That price accessibility matters in the internal nasal dilators market because many first purchases are trial purchases rather than highly committed medical purchases. Polymer also remains acceptable for short-cycle use where low unit cost matters more than long wear comfort or premium feel. The internal nasal dilators market share for pure polymer therefore stayed high in 2025 because it matched the needs of mass retail and value-seeking buyers.

Polymer and alloy products are growing faster because they are positioned around better structural memory, more stable dilation force, and improved overnight comfort. That premium positioning fits consumers who have already tried basic products and are willing to pay more for a reusable option that feels more consistent. The segment also aligns with the broader shift toward products that can support repeat nightly use rather than occasional symptom relief. Other product types remain small in volume, but they matter because clinical-grade cones and CPAP-adjunct forms can support higher average selling prices. Over time, the internal nasal dilators market is likely to keep pure polymer as the volume anchor while alloy blends capture a larger share of value through upgrade behavior.

Reusable devices held 59.24% of the usability segment in 2025 and are projected to grow at a 10.52% CAGR through 2031. This is important because the dominant format is also the fastest-growing format, which signals broad acceptance rather than a narrow premium niche. The internal nasal dilators market is benefiting from reusable economics because one unit priced at USD 12 to USD 25 can cover weeks or months of use, which improves perceived value versus repeated disposable purchases. That value logic supports habit formation, and habit formation matters in a category that depends on repeat nightly use. The segment also benefits from the fact that reusable devices avoid adhesive contact with skin and can feel more practical for long-term users.

Single-use devices still hold a role in hospitals, post-rhinoplasty support, and first-time trial packs where consumers want to test size and fit before moving up to a reusable product. WoodyKnows highlighted this logic in 2024 through multi-size trial pack offerings designed to reduce abandonment during the first purchase stage. That approach reflects a broader truth in the internal nasal dilators market, because poor initial fit is one of the strongest reasons for category drop-off. Reusable formats are also better suited to subscription and replenishment ecosystems, where accessories, replacement cycles, and repeat site visits help improve retention. The result is a usability mix where disposables support entry and clinical use, while reusable devices capture more of the long-term revenue base.

Complete Report Scope:

- By Product Type

- Polymer

- Polymer and Alloy

- Other Product Types

- By Usability

- Reusable

- Single Use

- By Application

- Snoring

- Sleep Apnea

- Deviated Septum

- Nasal Congestion

- Other Applications

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Other Distribution Channels

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 45.22% of the internal nasal dilators market in 2025, making it the largest regional contributor by a clear margin. The region benefits from high awareness of sleep disorders, stronger diagnosis rates, and a mature over-the-counter pharmacy network that supports trial and repeat purchasing. Rhinomed showed the strength of this route in 2024 when its Mute Nasal Dilator secured shelf space in more than 4,500 CVS stores and 1,500 Walgreens stores in the United States. That kind of chain placement is important because it gives a specialist product broad consumer visibility and helps normalize the category in everyday retail settings. Canada and Mexico remain smaller within the region, but both are supported by improving digital pharmacy access and a similar consumer preference for practical drug-free respiratory support.

Europe remains the second-largest region in the internal nasal dilators market, with Germany, the United Kingdom, and France acting as the main anchors. Consumer familiarity with non-drug breathing support is well established across these countries, which supports steady demand for both value and premium product formats. The regional online pharmacy base also adds speed to category growth, especially for specialist brands that do not depend entirely on store shelf access. Redcare Pharmacy's 13.9 million active customers in 2025 and its 2026 growth outlook illustrate the depth of that digital channel in Europe. This leaves Europe as a stable region where digital distribution can widen reach without needing the same scale of mass retail penetration seen in North America.

Asia-Pacific is the fastest-growing region with a projected 9.15% CAGR through 2031, and this part of the internal nasal dilators market size is being supported by a very large untreated demand base. China remains central because it carries the largest absolute obstructive sleep apnea population, and the 2025 Nature Communications study suggests that rising temperatures can compound future burden by worsening disease severity. India presents a strong adoption runway through digital pharmacy growth, broader health awareness, and a rising urban middle class that is more willing to spend on consumer sleep products. Japan and South Korea grow more steadily, but they offer stronger premium-device potential because consumers in those markets place more weight on medically validated and comfort-focused formats. South America and the Middle East and Africa remain smaller, with Brazil and Argentina leading in South America and GCC countries showing the clearest demand in MEA because obesity-linked sleep disorder patterns remain a structural tailwind in regional health statistics. The internal nasal dilators market share is still concentrated in North America today, yet the medium-term growth story is increasingly shaped by Asia-Pacific and selected self-pay urban clusters outside the largest developed markets.

- Airware Labs

- ASO Medical

- Breathewave

- Consumer Sleep Solutions LLC.

- HealthRight Products, LLC

- Hivox Biotek Inc.

- Intake Breathing

- Medline Industries

- Nasaline

- Nasanita

- Quest Products, LLC

- RC Medical Devices

- RespiFacile

- Rhinomed Limited

- SANOSTEC CORP

- Scandinavian Formulas Inc.

- SnoreCare

- Splintek, Inc.

- WoodyKnows (M&M Pure Air Systems LLC)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Sleep-Related Breathing Disorders

- 4.2.2 Preference for Drug-Free, Non-Invasive Breathing Aids

- 4.2.3 Growth of Direct-to-Consumer and Online Pharmacy Channels

- 4.2.4 Wider Use in Sports Performance and Recovery

- 4.2.5 Rising Clinical Interest in CPAP Adjunct and Nasal Airflow Support

- 4.2.6 Under-Reported Demand From Travel, Shift Work, and Portable Sleep-Routine Use

- 4.3 Market Restraints

- 4.3.1 Product Discomfort and Fit Variability

- 4.3.2 Reimbursement Gaps and Consumer Out-of-Pocket Sensitivity

- 4.3.3 Strong Substitution From External Strips and Clinical Alternatives

- 4.3.4 Regulatory and Biocompatibility Burden on New Materials and Designs

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Polymer

- 5.1.2 Polymer and Alloy

- 5.1.3 Other Product Types

- 5.2 By Usability

- 5.2.1 Reusable

- 5.2.2 Single Use

- 5.3 By Application

- 5.3.1 Snoring

- 5.3.2 Sleep Apnea

- 5.3.3 Deviated Septum

- 5.3.4 Nasal Congestion

- 5.3.5 Other Applications

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.4.4 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Airware Labs

- 6.3.2 ASO Medical

- 6.3.3 Breathewave

- 6.3.4 Consumer Sleep Solutions LLC.

- 6.3.5 HealthRight Products, LLC

- 6.3.6 Hivox Biotek Inc.

- 6.3.7 Intake Breathing

- 6.3.8 Medline Industries, LP

- 6.3.9 Nasaline

- 6.3.10 Nasanita

- 6.3.11 Quest Products, LLC

- 6.3.12 RC Medical Devices

- 6.3.13 RespiFacile

- 6.3.14 Rhinomed Limited

- 6.3.15 SANOSTEC CORP

- 6.3.16 Scandinavian Formulas Inc.

- 6.3.17 SnoreCare

- 6.3.18 Splintek, Inc.

- 6.3.19 WoodyKnows (M&M Pure Air Systems LLC)

7 Market Opportunities & Future Outlook

- 7.1 White-Space and Unmet-Need Assessment