|

시장보고서

상품코드

2073264

인사 분야 생성형 AI 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Generative AI In HR - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

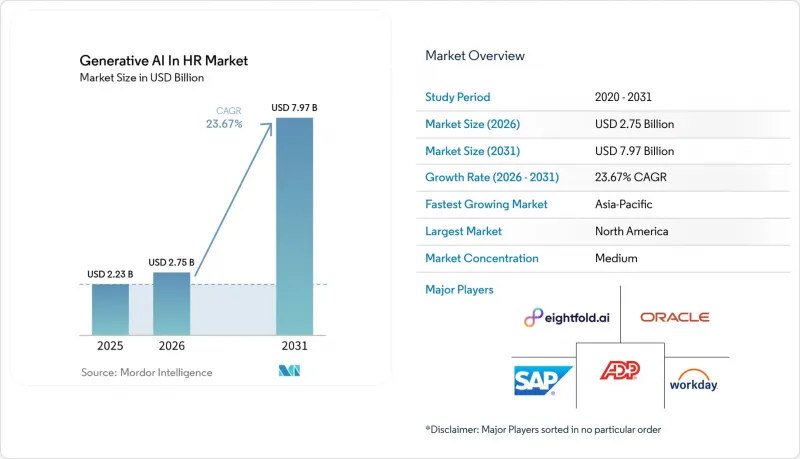

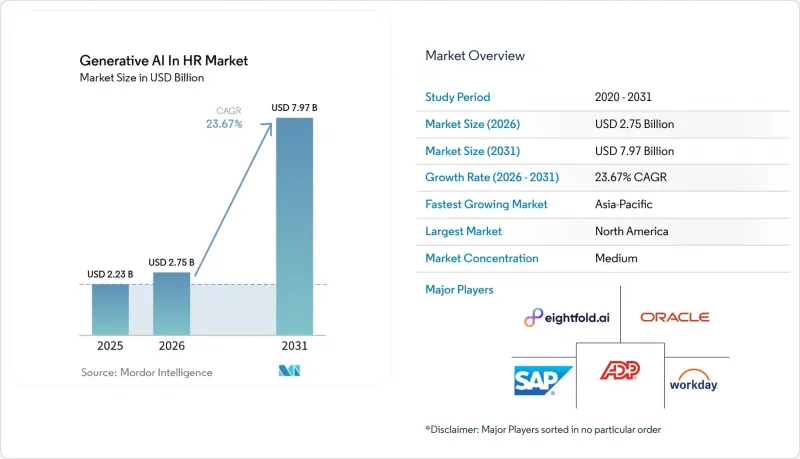

Mordor Intelligence에 의하면, 인사 분야 생성형 AI 시장 규모는 2025년 22억 3,000만 달러에서 2026년에는 27억 5,000만 달러로 확대되어 2031년까지 79억 7,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 23.67%로 성장할 전망입니다.

본 보고서는 배포 모델(클라우드, On-Premise, 하이브리드), 인사 기능(채용·인재 확보, 학습·역량 개발, 직원 참여도·경험, 성과 관리 등), 조직 규모(대기업 등), 최종 사용자 산업(IT 및 통신, BFSI 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인사 분야 생성형 AI에 대한 세계적 동향과 인사이트

엔터프라이즈 SaaS 분야의 대규모 언어 모델의 급속한 발전

고용주들이 설명 가능성, 감사 가능성, 그리고 도메인별 정확도를 요구함에 따라, 도메인 특화형 기반 모델이 범용 챗봇을 점차 대체하고 있습니다. Workday Illuminate는 8,000억 건 이상의 비즈니스 거래 데이터를 수집하여, 인사 및 재무 환경 전반에 걸친 프로세스의 맥락을 유지하면서 직무 설명서 작성, 인재 요약, 승계 계획의 자동화를 실현하고 있습니다. 마이크로소프트는 2026년 2월, IBM과 제휴하여 WatsonX의 거버넌스 제어 기능과 Copilot의 협업 계층을 결합함으로써, 개인 데이터를 공개 훈련 루프에 노출시키지 않고도 복리후생 관련 문의나 신입 사원 온보딩을 위한 HR 에이전트를 기밀성을 보장하며 도입할 수 있게 했습니다. Wisq와 같은 전문 벤더들은 EEOC 및 GDPR(EU 개인정보보호규정)의 틀에 부합하는 편향 검사 기능을 탑재한 독자적인 HR 언어 모델을 출시함으로써, 모델의 기능과 규제상의 기대치 간의 격차를 해소하고 있습니다. 이러한 모델들이 성숙해짐에 따라, 인사 분야 생성형 AI 시장은 그동안 시범 도입을 위험이 낮은 업무로만 제한해 왔던 위험 회피적인 업계에서도 신뢰도를 높여가고 있습니다.

대규모 인재 채용 업무의 자동화에 대한 압박이 커지고 있습니다.

현장 직원이나 시급제 직원의 채용은 전 세계 인력의 대부분을 차지하고 있음에도 불구하고, 여전히 디지털화가 진전되지 않고 있습니다. ICIMS의 “Frontline AI”는 SMS, WhatsApp, 웹 채팅을 통해 24시간 지원자와 소통하며, 채용까지 걸리는 시간을 최대 75% 단축하고, 채용 담당자 1인당 채용 건수를 10배로 늘리고 있습니다. Paradox사의 “Olivia”어시스턴트는 면접 일정 조율 및 사전 심사를 대규모로 진행합니다. 한편, Eightfold AI사의 구조화된 영상 면접 시스템은 문서 작성 시간을 90% 단축하며, 뉴욕시 지방법 제144호에 따른 새로운 감사 요건을 충족합니다. 이러한 효율화의 진전은 고용주의 투자 의지를 북돋아, 과거 수작업이 주를 이루던 채용 워크플로우의 핵심으로 인사 분야 생성형 AI 시장을 밀어붙이고 있습니다.

노동력 관련 AI 모델에서 제기되는 데이터 개인정보 보호 및 편향에 대한 우려

알고리즘의 편향, 개인정보 유출, 불투명한 의사결정 논리는 고용주에게 막대한 벌금이 부과될 위험을 초래합니다. EU AI법에 따르면, 금지된 시스템을 도입할 경우 최대 3,500만 유로(3,960만 달러) 또는 전 세계 매출액의 7%에 해당하는 벌금이 부과되지만, 2026년 8월 마감 시한을 앞두고 “충분히 준비가 되어 있다”라고 느끼는 조직은 고작 18%에 불과합니다. 뉴욕시 지방법 제144호에 따르면, 이미 자동화된 채용 도구에 대한 편향성 감사가 의무화되어 있으며, 공급업체는 감사 결과를 공개하고 지원자에게 이를 통지해야 합니다. 한편, ISO 42001은 선택적인 거버넌스 모델을 제시하고 있습니다. 컴플라이언스의 복잡성으로 인해, 인사 분야 생성형 AI 시장에서 고위험 이용 사례, 특히 성과 평가나 승진 심사에서의 도입이 지연되고 있습니다.

부문별 분석

고용주들이 클라우드 추론의 민첩성과 On-Premise 환경에서의 개인 데이터 관리를 결합한 유연성을 추구하는 가운데, 하이브리드 도입은 연평균 성장률(CAGR) 26.77%로 확대될 것으로 전망됩니다. 그렇긴 하지만, 구독형 가격 정책, 신속한 출시 주기, 공급업체 관리에 의한 보안이 중견 기업 구매자들에게 호응을 얻고 있어, 2025년 인사 분야 생성형 AI 시장 점유율의 64.29%는 클라우드 서비스가 계속해서 차지했습니다. 중국이나 중동 등 엄격한 현지화 요건이 적용되는 지역에서 사업을 전개하는 다국적 기업들은 현재, 데이터 본국 송환의 위험을 피하기 위해 소버린 클라우드 지역이나 기밀 컴퓨팅 엔클레이브를 시범 도입하고 있으며, 기밀성이 높은 기록은 On-Premise에 보관하는 한편, 익명화된 메타데이터를 클라우드 엔진으로 전송하고 있습니다. 주요 하이퍼스케일러 기업들은 Workday, SAP SuccessFactors, Oracle HCM용 전용 HR 커넥터를 제공함으로써 이에 대응하고 있으며, 고객은 핵심 데이터를 이동시키지 않고도 생성형 AI 기능을 활용할 수 있게 되었습니다. 이 공존 모델은 기존의 감사 관리 체계를 유지하면서, 규정 준수 요건이 엄격한 업계의 인사 분야에서 생성형 AI 시장의 확산을 가속화하고 있습니다.

방위, 정보 기관, 중요 인프라 분야에서는 여전히 On-Premise 도입이 이어지고 있습니다. 그러나 각 벤더들이 소버린 클라우드 인증과 기존 에어갭 방식과의 동등성을 입증해 나가면서, On-Premise의 전체 시장 점유율은 계속해서 하락하고 있습니다. ADP와 SAP의 세계 급여 계산 통합은 이러한 변화를 상징합니다. 기업은 현재 기존 인사 시스템을 근본적으로 변경하지 않고도 140개국에 걸쳐 급여 계산 오류 감지, 보고서 작성, 직원용 셀프 서비스를 통합적으로 운영할 수 있게 되었습니다. 이러한 API 우선 확장 기능은 전환 위험을 줄여주며, 인사 분야 생성형 AI 시장에서 하이브리드형을 기본 운영 모델로 자리매김하고 있습니다.

HR 애널리틱스와 인재 계획 분야는 연평균 성장률(CAGR) 25.85%라는 가장 높은 성장세가 예상되며, 이는 채용과 관련된 거래형 지표에서 예측적 역량 예측, 시나리오 모델링, 조직 설계로의 전환을 시사합니다. 2025년 인사 분야 생성형 AI 시장 규모에서 채용 관련 분야는 여전히 28.45%를 차지하고 있지만, 챗봇이나 스케줄링 도구의 기능적 동등화가 진행됨에 따라 구매자들은 더 큰 부가가치를 찾아 하류 분야로 눈을 돌리고 있습니다. Workday Illuminate와 같은 플랫폼은 기업 고유의 프로세스 데이터를 통합하여 온보딩 병목 현상에 대한 보고서, 후임자 후보 목록, 보상 관련 인사이트를 생성합니다. 한편, 학습 시스템은 생성형 엔진을 활용해 맞춤형 마이크로 레슨을 생성함으로써 외부 컨텐츠 라이브러리에 대한 지출을 줄이고 있습니다.

직원 참여도 관리 솔루션에는 감정 분석 및 AI가 생성한 실행 계획이 통합되어 있어, 관리자가 번아웃 징후에 실시간으로 대응할 수 있기 때문에 인적 자본 전략의 인사 분야에서 생성형 AI 시장의 입지가 공고해지고 있습니다. 성과 관리는 법적 책임에 대한 우려로 인해 여전히 신중한 접근이 요구되고 있지만, 설명 가능한 AI 대시보드나 ‘휴먼 인 더 루프” 방식에 따른 승인 절차가 점차 경영진의 지지를 얻고 있습니다.

지역별 분석

북미는 벤처 캐피털의 확충, HR 테크 벤더의 집중, 그리고 역사적으로 관대한 규제 환경의 뒷받침을 받아 2025년 인사 분야 생성형 AI 시장 점유율을 35.27%로 유지했습니다. 제각각인 규제 증가, 캘리포니아주의 CCPA, 뉴욕주의 로컬 법 144, 그리고 향후 제정될 연방 지침에 따라, 선정 기준은 규정 준수 대응을 위한 대시보드를 즉시 이용할 수 있는 플랫폼으로 전환되고 있습니다. 대서양 양쪽에서 사업을 전개하는 고용주들은 현재 기능의 범위뿐만 아니라 규제 대응의 유연성을 중요시하고 있으며, 이는 감사 보고서 기능이 내장된 공급업체에게 경쟁 우위를 제공합니다.

아시아태평양은 2031년까지 26.20%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 중국의 국가 AI 전략에서는 대규모 기술 재교육과 노동력 분석이 의무화되어 있으며, 국영 기업 전반에 걸쳐 확장 가능한 중국어 지원 모델의 도입을 장려하고 있습니다. 인도의 주요 IT 서비스 기업들은 생성형 에이전트를 활용해 해외 채용 워크플로우를 자동화하고, 이직률을 낮추며, 학습 경로를 개인화하고 있는 반면, 일본에서는 인구 고령화에 대응하기 위해 AI를 활용한 후계자 육성 계획의 시범 운영이 진행되고 있습니다. 호주 및 뉴질랜드는 EU식 투명성 규정을 모델로 삼고 있으며, 이 지역에서는 공급업체가 유럽 진출에 앞서 규정 준수 준비가 완료되었음을 입증하는 ‘샌드박스”라고 되어 있습니다.

유럽, 중동 및 아프리카에서는 그 성장세에 차이가 나타나고 있습니다. 유럽의 고용주들은 EU AI법에 따른 복잡한 절차에 직면해 있으며, 근로자 대표 위원회와의 협의 의무 및 적합성 평가로 인해 구매 주기가 길어지면서 인사 분야 생성형 AI 시장 확대가 일시적으로 주춤하고 있습니다. 리틀러사의 2025년 조사에 따르면, 2026년 8월 마감 기한을 앞두고 준비를 마친 기업은 고작 18%에 불과해, 단기적인 병목 현상이 두드러지게 나타나고 있습니다. 중동, 특히 아랍에미리트(UAE)와 사우디아라비아에서는 정부계 펀드의 자금을 AI를 활용한 인재 국내 유치 프로그램에 투입하고 있습니다. 한편, 아프리카 수요는 저대역폭 환경에 최적화된 모바일 우선 챗봇에 집중되어 있습니다. 브라질과 아르헨티나를 비롯한 남미 지역에서는 대화형 AI를 대거 도입하고 있는 소매업 및 농업 분야의 채용 활동에 이를 활용하고 있지만, 거시경제의 변동으로 인해 수년에 걸친 혁신 예산은 여전히 제한되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the generative AI in HR market size is expected to increase from USD 2.23 billion in 2025 to USD 2.75 billion in 2026 and reach USD 7.97 billion by 2031, growing at a CAGR of 23.67% over 2026-2031.

This report is Segmented by Deployment Model (Cloud, On-Premises, and Hybrid), HR Function (Recruitment and Talent Acquisition, Learning and Development, Employee Engagement and Experience, Performance Management, and More), Organization Size (Large Enterprises, and More), End-Use Industry (IT and Telecom, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Generative AI In HR Market Trends and Insights

Rapid Advancement of Large Language Models in Enterprise SaaS

Domain-tuned foundation models are overtaking generic chatbots as employers require explainability, auditability and domain-specific accuracy. Workday Illuminate ingests more than 800 billion business transactions to automate job description creation, talent summarization and succession planning, while preserving process context across HR and finance environments. Microsoft joined forces with IBM in February 2026 to pair watsonx governance controls with the Copilot collaboration layer, enabling confidential deployment of HR agents for benefits queries and onboarding without exposing personal data to public training loops. Specialist vendors such as Wisq are launching proprietary HR language models that embed bias checks aligned to EEOC and GDPR frameworks, closing the gap between model capability and regulatory expectation. As these models mature, the generative AI in HR market gains credibility among risk-averse sectors that previously limited pilots to low-stakes tasks.

Rising Pressure to Automate High-Volume Talent Acquisition Tasks

Frontline and hourly hiring remains largely undigitized even though it represents a majority of global headcount. ICIMS Frontline AI now engages applicants around the clock across SMS, WhatsApp and web chat, reducing time-to-fill by up to 75% and allowing tenfold more hires per recruiter.Paradox's Olivia assistant schedules interviews and conducts pre-screens at scale, while Eightfold AI's structured video interviewer compresses documentation time by 90% to satisfy emerging audit mandates under NYC Local Law 144. These efficiency gains fuel employer willingness to invest, propelling the generative AI in HR market into core hiring workflows once dominated by manual labor.

Data Privacy and Bias Concerns in Workforce-Related AI Models

Algorithmic bias, privacy lapses and opaque decision logic expose employers to hefty penalties. The EU AI Act imposes fines of up to EUR 35 million (USD 39.6 million) or 7% of global turnover for deploying prohibited systems, yet only 18% of organizations feel very prepared for the August 2026 deadline. NYC Local Law 144 already requires bias audits for automated hiring tools, forcing vendors to publish audit results and notify candidates, while ISO 42001 offers an optional governance blueprint. Compliance complexity is delaying high-risk use cases in the generative AI in HR market, particularly performance evaluation and promotion selection.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Conversational AI for Employee Self-Service

- Mainstreaming of Skills-Based Workforce Planning Frameworks

- Limited Availability of HR-Specific High-Quality Training Data

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid deployments are forecast to expand at a 26.77% CAGR as employers seek the agility of cloud inference paired with on-premises control of personal data. Cloud services nonetheless retained 64.29% of the 2025 generative AI in HR market share because subscription pricing, rapid release cycles and vendor-managed security appeal to mid-market buyers. Multinationals operating under strict localization mandates in China or the Middle East now pilot sovereign-cloud regions and confidential-computing enclaves to avoid repatriation risk, keeping sensitive records on-premises while sending de-identified metadata to cloud engines. Major hyperscalers have responded with dedicated HR connectors for Workday, SAP SuccessFactors and Oracle HCM that let customers unlock generative features without moving core data. This coexistence model preserves existing audit controls yet accelerates the generative AI in HR market penetration among compliance-heavy industries.

On-premises installations persist in defense, intelligence and critical-infrastructure environments, but their overall share continues to slide as vendors document equivalence between sovereign-cloud certifications and traditional air-gaps. ADP's global payroll integration with SAP exemplifies the shift: firms can now orchestrate payroll anomaly detection, reporting and employee self-service across 140 countries without uprooting incumbent HR stacks.Such API-first extensions lower migration risk and reinforce hybrid as the default operating model within the generative AI in HR market.

HR analytics and workforce planning is projected to grow at the fastest 25.85% CAGR, signaling a pivot from transactional hiring metrics toward predictive skills forecasting, scenario modeling and organizational design. Recruitment still commanded 28.45% of the 2025 generative AI in HR market size, but feature parity in chatbots and scheduling tools is pushing buyers to look further downstream for incremental value. Platforms such as Workday Illuminate generate onboarding bottleneck reports, succession shortlists and compensation insights by ingesting enterprise-specific process data. Meanwhile learning systems leverage generative engines to produce customized micro-lessons, reducing spend on external content libraries.

Employee engagement suites embed sentiment analysis and AI-generated action plans so managers can respond to burnout signals in real time, raising stickiness of the generative AI in HR market within human capital strategies. Performance management remains a cautious frontier due to liability worries, but explainable AI dashboards and human-in-the-loop approvals are gradually winning executive sponsorship.

Complete Report Scope:

- By Deployment Model

- Cloud

- On-premises

- Hybrid

- By HR Function

- Recruitment and Talent Acquisition

- Learning and Development

- Employee Engagement and Experience

- Performance Management

- HR Analytics and Workforce Planning

- Other HR Functions

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By End-use Industry

- IT and Telecom

- BFSI

- Healthcare and Life Sciences

- Manufacturing

- Retail and E-commerce

- Other End-use Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Geography Analysis

North America maintained 35.27% share of the generative AI in HR market in 2025, buoyed by venture capital depth, concentration of HR tech vendors and a historically permissive regulatory climate. Rising patchwork rules, California CCPA, New York Local Law 144 and forthcoming federal guidelines, are shifting selection criteria toward platforms with turnkey compliance dashboards. Employers operating on both sides of the Atlantic now rate regulatory agility as high as feature scope, giving advantage to vendors with embedded audit reporting.

Asia-Pacific is anticipated to post the fastest 26.20% CAGR through 2031. China's national AI strategy mandates large-scale reskilling and workforce analytics, driving adoption of Mandarin-trained models that can scale across state-owned enterprises. India's IT services giants use generative agents to automate offshore recruitment workflows, cut attrition and personalize learning paths, while Japan pilots AI-driven succession planning to hedge against population aging. Australia and New Zealand model EU-style transparency rules, turning the region into a sandbox where vendors prove compliance readiness before European rollouts.

Europe, the Middle East and Africa display uneven momentum. European employers face procedural complexity under the EU AI Act, mandatory works-council consultation and conformity assessments lengthen buying cycles, temporarily tempering the generative AI in HR market expansion. Littler's 2025 survey revealed only 18% readiness for the August 2026 deadline, spotlighting a short-term bottleneck.The Middle East channels sovereign wealth into AI workforce nationalization programs, particularly in the UAE and Saudi Arabia, while African demand centers on mobile-first chatbots optimised for low bandwidth. South America, led by Brazil and Argentina, applies conversational AI to high-volume retail and agriculture hiring, though macroeconomic volatility still limits multi-year transformation budgets.

- ADP, Inc.

- Workday, Inc.

- Oracle Corporation

- SAP SE

- International Business Machines Corporation

- Microsoft Corporation

- Google LLC

- Eightfold AI, Inc.

- Phenom People, Inc.

- Paradox.ai, Inc.

- Beamery Ltd.

- HireVue, Inc.

- iCIMS, Inc.

- Greenhouse Software, Inc.

- Lever, Inc.

- Textio, Inc.

- Gloat, Inc.

- Retrain.ai Ltd.

- SeekOut Inc.

- Lattice, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Advancement of Large Language Models in Enterprise SaaS

- 4.2.2 Rising Pressure to Automate High-Volume Talent Acquisition Tasks

- 4.2.3 Growing Adoption of Conversational AI for Employee Self-Service

- 4.2.4 Mainstreaming of Skills-Based Workforce Planning Frameworks

- 4.2.5 Integration of GenAI with Low-Code HR Tech Stacks

- 4.2.6 Increasing Employer Demand for Hyper-Personalized Learning Content

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Bias Concerns in Workforce-Related AI Models

- 4.3.2 Limited Availability of HR-Specific High-Quality Training Data

- 4.3.3 Rising Total Cost of Ownership for GenAI Model Fine-Tuning

- 4.3.4 Uncertain Intellectual Property Rights Around AI-Generated Content

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products or Services

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-premises

- 5.1.3 Hybrid

- 5.2 By HR Function

- 5.2.1 Recruitment and Talent Acquisition

- 5.2.2 Learning and Development

- 5.2.3 Employee Engagement and Experience

- 5.2.4 Performance Management

- 5.2.5 HR Analytics and Workforce Planning

- 5.2.6 Other HR Functions

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-use Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Manufacturing

- 5.4.5 Retail and E-commerce

- 5.4.6 Other End-use Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ADP, Inc.

- 6.4.2 Workday, Inc.

- 6.4.3 Oracle Corporation

- 6.4.4 SAP SE

- 6.4.5 International Business Machines Corporation

- 6.4.6 Microsoft Corporation

- 6.4.7 Google LLC

- 6.4.8 Eightfold AI, Inc.

- 6.4.9 Phenom People, Inc.

- 6.4.10 Paradox.ai, Inc.

- 6.4.11 Beamery Ltd.

- 6.4.12 HireVue, Inc.

- 6.4.13 iCIMS, Inc.

- 6.4.14 Greenhouse Software, Inc.

- 6.4.15 Lever, Inc.

- 6.4.16 Textio, Inc.

- 6.4.17 Gloat, Inc.

- 6.4.18 Retrain.ai Ltd.

- 6.4.19 SeekOut Inc.

- 6.4.20 Lattice, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment