|

시장보고서

상품코드

2073275

미디어 구매 서비스 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Media Buying Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

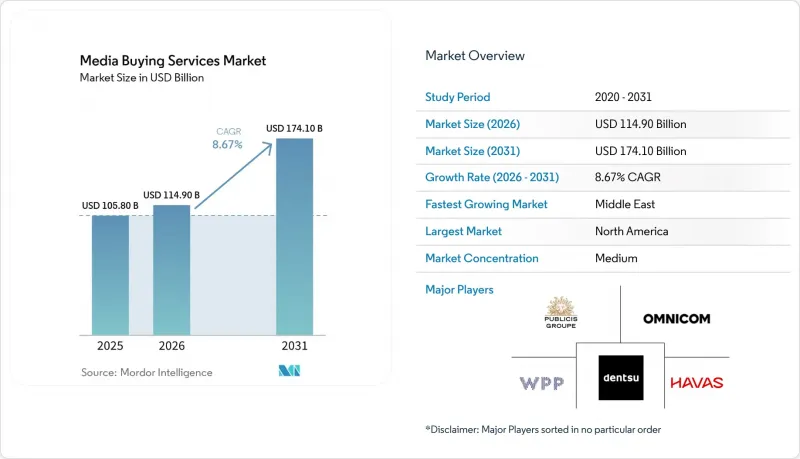

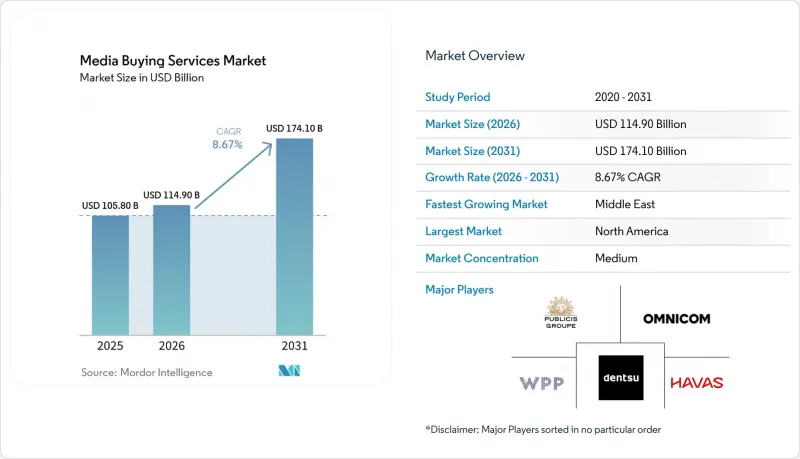

Mordor Intelligence에 의하면, 미디어 구매 서비스 시장 규모는 2025년 1,058억 달러, 2026년 1,149억 달러에서 2031년까지 1,741억 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 8.67%를 나타낼 전망입니다.

본 보고서는 서비스 유형별(미디어 전략·기획, 미디어 구매·협상, 프로그래매틱 및 성과형 구매 등), 미디어 채널별(소셜 미디어 광고, 디스플레이 광고 등), 조직 규모별(대기업 등), 최종 사용자 산업별(소매 및 전자상거래, IT 및 통신 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 미디어 구매 서비스 시장 동향과 인사이트

프로그래매틱 및 AI 기반 광고 구매가 광고 대행사의 핵심 워크플로우가 될 것

프로그래매틱 광고는 전문적인 기능에서 디지털 미디어 전반에 걸친 표준적인 실행 계층으로 전환되었습니다. 독일에서는 BVDW의 예측에 따르면, 2026년에는 독일의 온라인 디스플레이 및 동영상 시장의 80%를 프로그래매틱 구매이 차지하며, 65억 유로에 달할 것으로 전망됩니다. 이는 2025년 IRS 평균 환율 기준으로 70억 달러에 해당합니다. 이러한 변화로 인해 광고 대행사의 선정 기준도 변화하고 있습니다. 대부분의 구매자가 동일한 유통 경로에 접근할 수 있게 되면, 인벤토리에 대한 접근 권한의 중요성은 낮아지고, 최적화 로직의 중요성은 더욱 커지기 때문입니다. 따라서 미디어 구매 서비스 시장에서는 단순히 수동으로 실행하는 것보다 아이덴티티 인프라, 데이터 모델, 워크플로우의 자동화가 더욱 중요시되고 있습니다. 표준 플랫폼에 대한 접근 외에도, 차별화된 AI 레이어를 제공하지 못하는 광고 대행사는 가격 책정 및 고객 유지 측면에서 더 큰 압박에 직면하고 있습니다.

커넥티드 TV, 리테일 미디어, 디지털 동영상으로의 예산 전환

커넥티드 TV와 리테일 미디어가 신규 광고 예산에서 차지하는 비중이 점점 커지면서, 이에 따라 광고 대행사가 가치를 창출하는 영역도 변화하고 있습니다. 덴츠는 2026년 전 세계 커넥티드 TV 시장이 11.5%, 같은 해 리테일 미디어 시장이 12.3% 성장할 것으로 전망하고 있으며, 이는 두 채널이 광고 시장 전체에 비해 훨씬 더 많은 투자를 유치하고 있음을 뒷받침합니다. 리테일 미디어가 주목받고 있는 이유는 구매 의향 데이터를 캠페인 계획을 위한 타겟팅이 가능하면서도 개인정보 보호를 고려한 입력 자료로 변환할 수 있기 때문입니다. 리테일 미디어의 신호와 커넥티드 TV의 활성화 기능을 결합할 수 있는 광고 대행사는 광고 노출과 구매 사이의 연결 고리를 더욱 긴밀하게 구축하고 있습니다. 이러한 융합은 이미 인프라 선택에 영향을 미치고 있으며, 2026년 4월 Stagwell이 FreeWheel과 통합하여 통합된 커넥티드 TV 활성화 계층을 구축한 것이 그 한 예입니다.

개인정보 보호 규제와 신호 손실이 타겟팅 정확도를 떨어뜨립니다.

개인정보 보호 규제는 단순한 규정 준수 문제에 그치지 않고, 주소 지정 가능한 미디어에 대한 구조적인 제약으로 작용하고 있습니다. 주요 브라우저에서의 쿠키 폐지 및 Apple의 ‘앱 추적 투명성(App Tracking Transparency)”프레임워크 덕분에 계획 및 최적화에 활용할 수 있는 결정론적 식별자의 양이 감소했습니다. 이러한 신호의 상실로 인해, 오픈 웹 전반에 걸친 잠재 고객 도달 계획의 효율성이 저하되고, ID 시스템 간 분절화가 심화되고 있습니다. 미디어 구매 서비스 시장에서 이러한 부담은 운영 모델에 법무, 데이터, 엔지니어링 지원이 포함되지 않은 소규모 대행사에 특히 크게 짓누르고 있습니다. 그 결과, 몇년전과 비교해 캠페인의 정확도가 자사 자산이나 퍼블리셔와의 관계에 더 크게 좌우되게 되었으며, 계획 수립 환경은 더욱 까다로워졌습니다.

부문별 분석

2025년, 미디어 구매 및 협상 업무는 서비스 매출의 35.76%를 차지하며, 이 부문은 미디어 구매 서비스 시장에서 계속해서 핵심적인 위치를 차지했습니다. 커넥티드 TV, 스포츠, 실시간 뉴스 및 기타 고부가가치 환경에서의 프리미엄 인벤토리는 여전히 직접 거래 구조에 크게 의존하고 있기 때문에 이러한 입지는 견고하게 유지되었습니다. 구매 담당자들은 이러한 환경에서 협상을 통한 접근권, 가격 규율, 그리고 인접 광고 관리를 계속해서 중요하게 여기고 있습니다. 이러한 상황으로 인해, 실제 업무의 상당 부분이 소프트웨어로 전환되고 있는 와중에도, 인간 중개인과의 관계는 여전히 중요하게 여겨지고 있습니다. 클라이언트들은 프리미엄 광고 공간과 상업적 조건에 대한 확실성을 원하고 있기 때문에 미디어 구매 서비스 시장의 이 분야는 견조한 성장세를 유지하고 있습니다.

프로그래매틱 및 퍼포먼스형 광고 구매는 2026년부터 2031년까지 연평균 성장률(CAGR) 9.46%를 나타낼 것으로 예측되며, 미디어 구매 서비스 시장에서 가장 빠르게 성장하는 서비스 카테고리가 될 것입니다. 이러한 성장은 오픈 웹의 프로그래매틱, 프라이빗 마켓플레이스, 큐레이션된 거래, 그리고 실시간 최적화 모델로 예산이 이동한 것과 밀접한 관련이 있습니다. PubMatic에 따르면, 이 회사의 AgenticOS 플랫폼은 2026년 1분기까지 30건 이상의 완전 자율형 엔드투엔드 캠페인을 실행했으며, 이는 워크플로우 자동화가 실제 구매 업무에 얼마나 빠르게 확산되고 있는지를 보여줍니다. 트랜잭션 기반 구매의 자동화가 진행됨에 따라, 대행사들은 미디어 구매 서비스 시장에서의 수익원으로 전략, 분석 및 상거래 활성화에 점점 더 중점을 두고 있습니다.

2025년, 검색 광고는 채널 매출의 31.44%를 차지하며 미디어 구매 서비스 시장에서 1위 자리를 지켰습니다. 검색 광고가 그 위상을 유지할 수 있는 이유는 명확한 하류 퍼널의 의도를 파악하고, 다양한 업종에서 브랜드에서 성과로 이어지는 직접적인 기여도 측정을 지원하기 때문입니다. 광고주는 특히 광범위한 인지도보다 투자 대비 효과의 가시성이 더 중요하게 여겨지는 경우, 여전히 검색 광고를 성과 기반 예산의 핵심으로 삼고 있습니다. 이러한 안정성 덕분에 입찰, 키워드, 예산 배분 및 크로스 채널 배분을 관리할 수 있는 광고 대행사에 대한 수요가 지속적으로 발생하고 있습니다. 미디어 구매 서비스 시장이 여전히 검색 광고에 의존하고 있는 이유는 지출 관리와 측정 가능한 성과를 동시에 달성하고 있기 때문입니다.

커넥티드 TV 및 OTT 동영상은 2031년까지 연평균 성장률(CAGR) 10.14%를 나타낼 것으로 예측되며, 미디어 구매 서비스 시장에서 가장 빠르게 성장하고 있는 미디어 채널로 자리매김하고 있습니다. 이러한 성장은 광고 수익형 스트리밍, 시청 습관의 변화, 그리고 동영상 기획에 상거래 데이터를 접목한 데 힘입어 이루어지고 있습니다. 일본에서는 2025년 인터넷 광고 매체 지출이 11.8% 증가했습니다. 이는 주로 SNS의 세로형 동영상에서 비롯된 것으로, 동영상 중심의 컨텐츠 발견과 활성화를 향한 광범위한 흐름과 일치합니다. 디스플레이 광고, 디지털 동영상, 디지털 오디오, 디지털 옥외 광고, 소매 미디어 네트워크 역시 여전히 중요하지만, 가장 극적인 변화는 동영상 인벤토리, 오디언스 데이터, 품질 관리가 융합되는 분야에서 일어나고 있습니다.

지역별 분석

2025년, 북미는 미디어 구매 서비스 시장에서 여전히 최대의 지역 거점으로서 전 세계 시장 매출의 약 41.48%를 차지했습니다. 미국은 광고주의 지출이 집중되어 있을 뿐만 아니라, 성숙한 프로그래매틱 인프라를 갖추고 있어 해당 지역의 수익 대부분을 차지하고 있습니다. 또한, 이 지역에는 대형 지주 기업의 네트워크와 많은 구매 기술 파트너들이 거점을 두고 있어, 높은 규모의 경제 효과를 유지하고 있습니다. 캐나다는 디지털화가 급속히 진행되고 있는 견실한 제2 시장으로 자리매김하고 있는 반면, 멕시코는 아직 성숙도가 낮은 단계에 있지만 ‘모바일 우선’ 구매 패턴을 통해 성장하고 있습니다. 이러한 집중 현상으로 인해 데이터 활용, 운영 및 플랫폼에 대한 의존도가 점점 더 주목받고 있는 가운데, 북미 미디어 구매 서비스 시장은 여전히 치열한 경쟁 국면을 보이고 있습니다.

유럽은 미디어 구매 서비스 시장에서 2위를 차지하고 있습니다. 독일의 온라인 디스플레이 및 동영상 광고 시장은 2026년에 82억 유로(89억 달러 상당)에 달할 것으로 예상되며, 거래의 80%를 프로그래매틱 광고가 차지할 것으로 전망됩니다. 프랑스의 광고 시장은 2025년에 198억 유로(214억 달러 상당)에 달했습니다. 같은 해 디지털 광고 시장은 11% 성장했으며, 2026년에는 7.5%의 추가 성장이 예상됩니다. 동의에 기반한 데이터 규제와 프리미엄 퍼블리셔 기반의 강화로 인해, 유럽의 구매자들은 오픈 옥션을 통한 구매보다 프로그래매틱 게런티드나 큐레이션된 프라이빗 마켓플레이스에서의 거래를 선호하는 경향이 더욱 강해지고 있습니다. 아시아태평양은 미디어 구매 서비스 시장에서 가장 빠르게 성장하고 있는 대규모 지역 클러스터입니다. 2025년, 일본의 총 광고비는 8조 623억 엔(534억 달러 상당)을 넘어섰으며, 인터넷 광고가 총 광고비의 50%를 처음으로 상회했습니다. 하쿠호도 DY ONE은 2025년 7월, 니혼 TV의 AdRM-Exchange를 통해 TV 프로그래매틱 구매를 시작했으며, 2025년 10월에는 고유 도달 범위 극대화 입찰 기능을 추가했습니다. 이는 이 지역 전체에서 방송 광고 재고가 프로그래매틱 워크플로우에 어떻게 통합되고 있는지를 보여줍니다.

남미는 북미나 유럽에 비해 규모는 작지만, 모바일 중심의 광고 활동을 통해 디지털 구매의 기반은 여전히 확대되고 있습니다. 중동 및 아프리카도 절대적인 규모로는 여전히 작지만, 중동은 2026년부터 2031년까지 연평균 성장률(CAGR) 8.86%를 기록하며, 지역별로는 가장 빠르게 성장하는 부문이 될 것으로 전망됩니다. 이러한 성장은 디지털 광고 투자 증가, 커넥티드 TV의 급속한 보급, 리테일 미디어 생태계의 확대, 그리고 사우디아라비아와 아랍에미리트(UAE) 등 여러 국가에서 진행되고 있는 정부 주도의 디지털 전환(DX) 이니셔티브에 힘입어 이루어지고 있습니다. 미디어 구매 서비스 시장은 현지 운영 노하우를 바탕으로 전 세계적인 도구와 각국 고유의 미디어 시스템을 연동할 수 있는 지역에서 가장 빠르게 성장하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.07According to Mordor Intelligence, the media buying services market size is projected to expand from USD 105.8 billion in 2025 and USD 114.9 billion in 2026 to USD 174.1 billion by 2031, registering a CAGR of 8.67% between 2026 to 2031.

This report is Segmented by Service Type (Media Strategy and Planning, Media Buying and Negotiation, Programmatic and Performance Buying, and More), Media Channel (Social Media Advertising, Display Advertising, and More), Organization Size (Large Enterprises, and More), End-User Industry (Retail and E-Commerce, IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Media Buying Services Market Trends and Insights

Programmatic And AI-Driven Buying Becomes Core Agency Workflow

Programmatic advertising has moved from a specialist capability to a default execution layer across digital media. In Germany, BVDW projected that programmatic buying would account for 80% of the country's online display and video market in 2026, reaching EUR 6.5 billion, which equals USD 7.0 billion at the 2025 IRS average exchange rate. That shift changes agency selection criteria, because inventory access matters less when most buyers can reach the same pipes, and optimization logic matters more. The media buying services market is therefore placing more value on identity infrastructure, data models, and workflow automation than on manual execution alone. Agencies that cannot show a differentiated AI layer on top of standard platform access are facing stronger pressure on pricing and retention.

Budget Migration Toward Connected TV, Retail Media, And Digital Video

Connected TV and retail media are taking a larger share of new ad budgets, and that is changing where agencies create value. Dentsu projected global connected TV growth of 11.5% in 2026 and global retail media growth of 12.3% in the same year, which confirms that both channels are attracting outsized investment compared with the wider ad market. Retail media is gaining traction because it turns purchase intent data into an addressable and privacy-safe input for campaign planning. Agencies that can combine retail media signals with connected TV activation are building a tighter loop between exposure and purchase. That convergence is already shaping infrastructure choices, as shown by Stagwell's April 2026 integration with FreeWheel to create a unified connected TV activation layer.

Privacy Regulation And Signal Loss Reduce Targeting Precision

Privacy regulation has become a structural limit on addressable media rather than a narrow compliance issue. Cookie deprecation in major browsers and Apple's App Tracking Transparency framework have reduced the volume of deterministic identifiers available for planning and optimization. That loss of signal has made audience reach planning less efficient across the open web and more fragmented across identity systems. In the media buying services market, the burden falls harder on smaller agencies that do not have legal, data, and engineering support built into their operating model. The result is a tougher planning environment where campaign precision depends more on first-party assets and publisher relationships than it did a few years ago.

Other drivers and restraints analyzed in the detailed report include:

- Demand For Omnichannel Measurement And ROAS Accountability

- First-Party Data Activation And Privacy-Safe Audience Planning

- Ad Fraud, Brand Safety, And Viewability Risks Persist

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Media buying and negotiation retained 35.76% of service revenue in 2025, which kept this function at the center of the media buying services market size. That position remained durable because premium inventory in connected TV, sports, live news, and other high-value environments still relies heavily on direct deal structures. Buyers continue to value negotiated access, pricing discipline, and adjacency control in these environments. Those conditions keep human broker relationships relevant even as more execution shifts into software. This part of the media buying services market stayed resilient because clients still need certainty around premium placements and commercial terms.

Programmatic and performance buying is projected to record a 9.46% CAGR from 2026 to 2031, which makes it the fastest-growing service category in the media buying services market. Growth is tied to budget movement into open-web programmatic, private marketplaces, curated deals, and real-time optimization models. PubMatic said its AgenticOS platform had executed more than 30 fully autonomous end-to-end campaigns by Q1 2026, which showed how quickly workflow automation is moving into live buying operations. As transactional buying becomes more automated, agencies are placing more emphasis on strategy, analytics, and commerce activation as the fee-bearing layers of the media buying services market.

Search advertising held 31.44% of channel revenue in 2025, which preserved its lead within the media buying services market. Search keeps that position because it captures clear lower-funnel intent and supports direct brand-to-outcome attribution across many verticals. Advertisers still rely on search to anchor performance budgets, especially when return visibility matters more than broad awareness. That stability creates consistent demand for agencies that can manage bidding, keywords, budget pacing, and cross-channel allocation. The media buying services market still leans on search because it combines spend discipline with measurable outcomes.

Connected TV and OTT video are projected to expand at a 10.14% CAGR through 2031, which makes it the fastest-growing media channel in the media buying services market. Growth is being pushed by ad-supported streaming, changing viewing habits, and the addition of commerce data into video planning. In Japan, internet advertising media expenditure grew 11.8% in 2025, driven mainly by SNS vertical video, which aligned with the broader move toward video-led discovery and activation. Display, digital video, digital audio, digital out-of-home, and retail media networks remain important, but the sharpest change is happening where video inventory, audience data, and quality controls now meet.

Complete Report Scope:

- By Service Type

- Media Strategy and Planning

- Media Buying and Negotiation

- Programmatic and Performance Buying

- Campaign Management and Optimization

- Measurement and Analytics

- Others (Retail Media and Commerce Activation, Influencer and Creator Media Amplification, Media Consulting and In-Housing Support)

- By Media Channel

- Search Advertising

- Social Media Advertising

- Display Advertising

- Digital Video

- Connected TV and Over-the-Top Video

- Others (Retail Media Networks, Digital Audio and Podcasts, Radio, Print, OOH and DOOH)

- By Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By End-User Industry

- Retail and E-commerce

- Media and Entertainment

- BFSI

- IT and Telecom

- Travel and Hospitality

- Healthcare

- Others (Automotive, Education, and Public sector)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Qatar

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America remained the largest regional base in the media buying services market in 2025, accounting for approximately 41.48% of global market revenue. The United States drives most regional revenue because it combines concentrated advertiser spending with mature programmatic infrastructure. The region also hosts many of the largest holding company networks and buying technology partners, which keeps scale advantages high. Canada remains a solid secondary market with strong digital adoption, while Mexico is still earlier in maturity but is moving forward through mobile-first buying patterns. This concentration keeps the media buying services market highly competitive in North America, even as data use, conduct, and platform dependence draw more attention.

Europe represented the second-largest geography in the media buying services market. Germany's online display and video advertising market is forecast to reach EUR 8.2 billion, which equals USD 8.9 billion in 2026, and programmatic is expected to account for 80% of transactions. France's advertising market reached EUR 19.8 billion, which equals USD 21.4 billion in 2025. Digital grew 11% in that year, and digital is forecast to grow another 7.5% in 2026. Consent-driven data rules and a stronger premium publisher base continue to push European buyers toward programmatic guaranteed and curated private marketplace deals over open-auction buying. Asia-Pacific is the fastest-growing large regional cluster in the media buying services market. Japan's total advertising spend crossed JPY 8,062.3 billion, which equals USD 53.4 billion in 2025, and internet advertising surpassed 50% of total ad investment for the first time. Hakuhodo DY ONE began programmatic TV buying through NTV's AdRM-Exchange in July 2025 and added a unique-reach maximization bidding function in October 2025, demonstrating how broadcast inventory is being integrated into programmatic workflows across the region.

South America remains smaller than North America and Europe, but its digital buying base is still expanding through mobile-led advertising activity. The Middle East and Africa also remain smaller in absolute scale; however, the Middle East is projected to be the fastest-growing regional segment during 2026-2031, registering a CAGR of 8.86%. Growth is being supported by increasing digital advertising investments, rapid connected TV adoption, expanding retail media ecosystems, and government-backed digital transformation initiatives in countries such as Saudi Arabia and the United Arab Emirates. The media buying services market is widening fastest where local execution expertise can connect global tools with country-specific media systems.

- WPP plc

- Omnicom Group Inc.

- Publicis Groupe S.A.

- Dentsu Group Inc.

- The Interpublic Group of Companies, Inc.

- Havas Group

- Hakuhodo DY Holdings Inc.

- Stagwell Inc.

- S4 Capital plc

- Accenture plc

- MiQ Digital Ltd.

- Horizon Media, Inc.

- PMG Worldwide LLC

- Tinuiti, Inc.

- The Trade Desk, Inc.

- Brandtech Group

- MiQ Digital

- Assembly Global

- Microsoft Corporation

- Criteo S.A.

- Adform A/S

- Viant Technology Inc.

- LiveRamp Holdings

- FreeWheel

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Programmatic and AI-Driven Buying Becomes Core Agency Workflow

- 4.2.2 Budget Migration Toward Connected TV, Retail Media, and Digital Video

- 4.2.3 Demand for Omnichannel Measurement and ROAS Accountability

- 4.2.4 First-Party Data Activation and Privacy-Safe Audience Planning

- 4.2.5 Curated Marketplaces and Supply Path Optimization Favor Specialist Buying Partners

- 4.2.6 Agentic AI Expands Outsourced Buying Among Mid-Market Brands

- 4.3 Market Restraints

- 4.3.1 Privacy Regulation and Signal Loss Reduce Targeting Precision

- 4.3.2 Ad Fraud, Brand Safety, and Viewability Risks Persist

- 4.3.3 Walled-Garden Measurement Gaps Limit Cross-Platform Optimization

- 4.3.4 Margin Compression from In-Housing and Platform Automation

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Media Strategy and Planning

- 5.1.2 Media Buying and Negotiation

- 5.1.3 Programmatic and Performance Buying

- 5.1.4 Campaign Management and Optimization

- 5.1.5 Measurement and Analytics

- 5.1.6 Others (Retail Media and Commerce Activation, Influencer and Creator Media Amplification, Media Consulting and In-Housing Support)

- 5.2 By Media Channel

- 5.2.1 Search Advertising

- 5.2.2 Social Media Advertising

- 5.2.3 Display Advertising

- 5.2.4 Digital Video

- 5.2.5 Connected TV and Over-the-Top Video

- 5.2.6 Others (Retail Media Networks, Digital Audio and Podcasts, Radio, Print, OOH and DOOH)

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By End-User Industry

- 5.4.1 Retail and E-commerce

- 5.4.2 Media and Entertainment

- 5.4.3 BFSI

- 5.4.4 IT and Telecom

- 5.4.5 Travel and Hospitality

- 5.4.6 Healthcare

- 5.4.7 Others (Automotive, Education, and Public sector)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Qatar

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 WPP plc

- 6.4.2 Omnicom Group Inc.

- 6.4.3 Publicis Groupe S.A.

- 6.4.4 Dentsu Group Inc.

- 6.4.5 The Interpublic Group of Companies, Inc.

- 6.4.6 Havas Group

- 6.4.7 Hakuhodo DY Holdings Inc.

- 6.4.8 Stagwell Inc.

- 6.4.9 S4 Capital plc

- 6.4.10 Accenture plc

- 6.4.11 MiQ Digital Ltd.

- 6.4.12 Horizon Media, Inc.

- 6.4.13 PMG Worldwide LLC

- 6.4.14 Tinuiti, Inc.

- 6.4.15 The Trade Desk, Inc.

- 6.4.16 Brandtech Group

- 6.4.17 MiQ Digital

- 6.4.18 Assembly Global

- 6.4.19 Microsoft Corporation

- 6.4.20 Criteo S.A.

- 6.4.21 Adform A/S

- 6.4.22 Viant Technology Inc.

- 6.4.23 LiveRamp Holdings

- 6.4.24 FreeWheel

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment