|

시장보고서

상품코드

2073285

북미의 AI 기반 에너지 관리 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America AI-Powered Energy Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

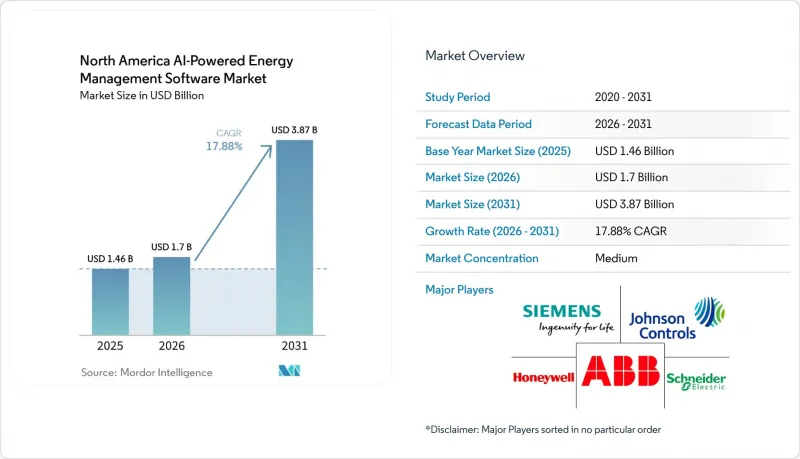

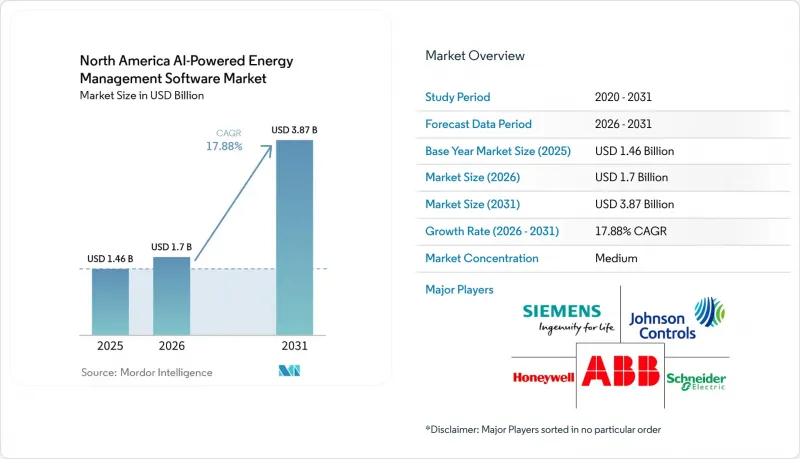

Mordor Intelligence에 의하면, 북미의 AI 기반 에너지 관리 소프트웨어 시장 규모는 2025년 14억 6,000만 달러로 평가되었습니다. 2026년 17억 달러에서 2031년까지 38억 7,000만 달러로 확대될 것으로 예측되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 17.88%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 배포 방식(클라우드 기반, On-Premise형, 하이브리드형), 용도(에너지 소비 및 수요 최적화, 자산 성능 및 예측 유지보수 등), 최종 사용자(상업용 건물, 산업 시설 등) 및 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

북미의 AI 기반 에너지 관리 소프트웨어 시장 동향 및 인사이트

상업시설에서의 스마트 계량기 및 IoT 센서의 급속한 보급

계량기 및 센서의 급속한 도입으로 인해, 건물 및 시설용 소프트웨어가 일반적인 가동 패턴을 학습하는 데 활용할 수 있는 데이터베이스가 확대되고 있습니다. 북미의 AI 기반 에너지 관리 소프트웨어 시장에서 이는 중요한 의미를 지닙니다. 왜냐하면, 더 높은 품질의 간격 데이터가 있다면 플랫폼은 단순한 모니터링에서 능동적인 예측 및 자동 대응으로 전환하기가 더 쉬워지기 때문입니다. 또한, 상업시설에서는 HVAC 제어, 인버터를 통한 전력 공급, 재실 신호 등을 공유 디지털 레이어에 통합하고 있으며, 이를 통해 여러 거점 간의 벤치마킹이 더욱 실용적으로 이루어지고 있습니다. 이러한 변화로 인해 각 거점에서의 전용 하드웨어 필요성이 줄어들고, 포트폴리오 전반에 걸친 소프트웨어 주도형 도입의 타당성이 높아지고 있습니다. 또한, 제2차 단계에 해당하는 계측 기기 및 센서의 업그레이드를 통해 암호화, 엣지 처리, 기기의 신뢰성이 향상되어, 운영 환경에서 보다 안전한 분석 활용을 뒷받침하고 있습니다. 도입 기반의 일관성이 높아짐에 따라, 북미의 AI 기반 에너지 관리 소프트웨어 시장 공급업체들은 기존 고객 기반 전반에 걸쳐 지속적인 소프트웨어 계약을 확대하는 데 있어 더욱 유리한 입지를 확보하고 있습니다.

피크 부하 고객에 대한 전기 요금 및 수요 요금 인상

전기 요금 상승에 따라, 대규모 시설에서 에너지 최적화는 단순한 비용 관리 수단에서 영업 이익률을 직접적으로 향상시키는 수단으로 변화하고 있습니다. 수요 요금의 중요성은 여전히 특히 크며, 단시간의 피크 수요가 발생하는 것만으로도 상업 및 산업 사용자의 월간 청구액 전체에 영향을 미칠 수 있기 때문입니다. ERCOT(텍사스주 전력거래소)의 전력 수요는 2025년 10월부터 2026년 3월까지 전년 대비 9% 이상 증가했습니다. 이는 데이터센터 건설, 산업의 전기화, 그리고 전기차 충전 수요의 확대를 반영한 것입니다. 이러한 증가로 인해 송전망 상황이압박을 받게 되면서, 부하를 분산시키고, 대응을 자동화하며, 배터리 가동 시점을 보다 정확하게 조정할 수 있는 소프트웨어의 가치가 높아졌습니다. 이러한 도구를 도입하지 않은 시설은 전기 요금 급등에 직면할 뿐만 아니라, 송전망 운영자가 보다 동적인 요금 체계를 채택함에 따라 단기적인 가격 변동의 영향을 더 크게 받게 됩니다. 따라서 북미의 AI 기반 에너지 관리 소프트웨어 시장은 부하가 높은 주에서 발생하는 요금 압박과 밀접한 관련이 있습니다.

기존 빌딩 관리 시스템과의 통합에 따른 복잡성

많은 건물이 여전히 여러 프로토콜이나 구형 컨트롤러를 병행하여 운영되고 있기 때문에 레거시 시스템의 복잡성은 여전히 큰 장벽으로 남아 있습니다. 북미의 AI 기반 에너지 관리 소프트웨어 시장에서 빌딩 자동화의 각 계층이 공통된 데이터 구조나 사용하기 쉬운 용도 인터페이스를 공유하지 않을 경우, 도입이 지연되는 요인이 됩니다. 많은 시설에서는 단일 통합 아키텍처로 설계된 것이 아니라, 단계적으로 도입된 BACnet, Modbus 및 독자적인 사양의 제어 시스템이 오랫동안 사용되어 왔습니다. 따라서 소프트웨어 공급업체는 초기 분석 모델이 실질적인 가치를 제공할 수 있게 될 때까지 미들웨어, 맞춤형 매핑 및 검증에 많은 시간을 할애할 수밖에 없습니다. 중규모 상업시설은 소프트웨어 투자를 정당화할 수 있을 만큼 충분한 규모를 갖추고 있음에도 불구하고, 전문적인 통합 기술이나 인력이 부족한 경우가 많아 가장 큰 영향을 받고 있습니다. 이로 인해 도입 비용이 높은 수준을 유지하고 있으며, 북미

부문별 분석

2025년, 북미의 AI 기반 에너지 관리 소프트웨어 시장에서 소프트웨어가 74.12%의 점유율을 차지했으며, 공급업체의 수익은 하드웨어 중심의 프로젝트 이익률이 아닌 지속적인 구독료 및 라이선스 수수료에 중점을 두고 있습니다. 북미의 AI 기반 에너지 관리 소프트웨어 시장에서는 고객들이 일반적으로 새로운 현장 하드웨어를 대폭 추가하지 않고도 신속한 시각화, 최적화 로직 및 보고 기능을 원하기 때문에 해당 소프트웨어가 계속해서 선호되고 있습니다. 또한, 이러한 수익 구조를 통해 벤더는 시간이 지남에 따라 분석 기능 업그레이드, 대시보드, 예측 도구, 규정 준수 대응 모듈 등으로 사업을 확장할 여지도 넓어집니다. 이튼사는 2026년 3월, 의료, 교육, 소매 분야의 상업용 빌딩을 대상으로 ‘Brightlayer Energy"를 발매했습니다. 이 제품에는 실시간 분석, 예측, 자동 제어, 분산형 에너지 최적화 기능이 탑재되어 있습니다. 이러한 제품의 출시는 소프트웨어 공급업체들이 에너지 최적화를 운영 관리 및 현지 규정 준수 대응과 더욱 밀접하게 연계하고 있음을 보여줍니다.

서비스 부문은 절대적인 규모로는 작지만, 2026년부터 2031년까지 연평균 성장률(CAGR) 17.93%를 나타낼 것으로 예측되며, 이는 시장 전체의 성장 속도를 소폭 상회하는 수준입니다. 북미의 AI 기반 에너지 관리 소프트웨어 시장에서는 고객 기반 측면에서 초기 도입 후의 통합 지원, 관리형 분석, 모델 튜닝에 대한 수요가 증가하고 있습니다. 많은 조직에서는 복잡한 사내 최적화 도구를 유지 관리할 수 있는 충분한 에너지 분석 및 데이터 사이언스 전문 인력이 부족합니다. 따라서 각 인터넷 서비스 제공업체들은 소프트웨어의 기능뿐만 아니라 서비스의 충실도, 도입 지원의 질, 지속적인 성능 지원 측면에서도 경쟁을 벌여야 하는 상황에 놓여 있습니다.

2025년에는 클라우드 기반 솔루션의 도입이 시장의 63.14%를 차지했으며, 이는 많은 건물 및 기업 사용자에게 도입이 간편하고 인프라 관리 부담이 줄어든다는 장점이 반영된 결과입니다. 북미의 AI 기반 에너지 관리 소프트웨어 시장은 클라우드로 전환되고 있습니다. 이는 여러 거점을 보유한 사용자가 포트폴리오 전반에 걸친 통합 보고서를 작성하거나, 보다 신속한 소프트웨어 업데이트를 필요로 하는 경우가 많기 때문입니다. 하이브리드 방식은 여전히 가장 빠르게 성장하고 있는 형태이며, 2026년부터 2031년까지 연평균 성장률(CAGR) 18.02%를 나타낼 것으로 전망됩니다. 이는 규제 대상이나 기밀성이 높은 환경의 상당수가, 제어 플레인의 데이터를 로컬 보안 경계 밖으로 완전히 이동시키지 않으면서도 분석의 규모를 확보하고자 하기 때문입니다. 따라서 하이브리드 아키텍처는 운영 시스템을 보다 엄격하게 관리해야 하는 유틸리티체 및 산업 사업자에게 실용적인 대안이 되고 있습니다. 또한, 벤더 입장에서는 보다 광범위한 분석 및 모니터링을 위해 클라우드 계층을 활용하면서도, 현장에서의 실시간 엣지 의사결정을 원하는 고객의 요구에 대응하는 데에도 도움이 됩니다.

NERC의 요건은 소프트웨어가 전력 시스템과 연동될 때 신중한 사이버 보안 설계가 필요함을 강조하고 있습니다. AWS와 지멘스 에너지는 2026년 4월, 디지털 전환 및 에너지 인프라 솔루션을 지원하기 위해 제휴를 확대했습니다. 이는 주요 기술 제공업체들이 클라우드 기능을 에너지 부문의 운영 요구 사항에 맞추고 있음을 반영합니다. 북미의 AI 기반 에너지 관리 소프트웨어 시장에서 이는 유틸리티체와 대기업들이 규모, 지연 시간, 규정 준수의 균형을 맞추는 과정에서 하이브리드 프레임워크가 계속해서 핵심적인 역할을 수행할 것이라는 전망을 뒷받침하는 것입니다. 순수한 On-Premise 모델은 보다 엄격한 환경에서는 여전히 그 중요성을 유지할 것이지만, 예측 기간 동안에는 보다 유연한 아키텍처에 비해 성장률이 뒤처질 가능성이 높을 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the north america AI-Powered energy management software market size is projected to expand from USD 1.46 billion in 2025 and USD 1.70 billion in 2026 to USD 3.87 billion by 2031, registering a CAGR of 17.88% between 2026 and 2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, and More), End User (Commercial Buildings, Industrial Facilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America AI-Powered Energy Management Software Market Trends and Insights

Rapid Smart Meter and IoT Sensor Penetration Across Commercial Sites

Rapid meter and sensor adoption is expanding the database that building and facility software can use to learn normal operating patterns. In the North America AI-Powered Energy Management Software Market, this matters because better interval data helps platforms move from simple monitoring to active prediction and automated response. Commercial sites are also bringing HVAC controls, inverter feeds, and occupancy signals onto shared digital layers, which makes multi-site benchmarking more practical. That shift reduces the need for proprietary hardware in every location and improves the case for software-led rollouts across portfolios. Second-wave metering and sensor upgrades are also improving encryption, edge processing, and device reliability, which supports more secure analytics use in operating environments. As that installed base becomes more consistent, vendors in the North America AI-Powered Energy Management Software Market are better positioned to scale recurring software contracts across existing customer sites.

Rising Utility Tariffs and Demand Charges for Peak Load Customers

Rising electricity tariffs are turning energy optimization from a cost-control tool into a direct operating-margin tool for large facilities. Demand charges remain especially important because a short peak event can shape the full monthly bill for commercial and industrial users. Electricity demand in ERCOT grew by more than 9% year over year from October 2025 through March 2026, reflecting data center construction, industrial electrification, and growth in electric vehicle charging. That increase tightened grid conditions and strengthened the value of software that can shift load, automate response, and time battery dispatch more accurately. Facilities without these tools are facing not only higher bills but also greater exposure to short-term price swings as grid operators use more dynamic pricing structures. This is keeping the North America AI-Powered Energy Management Software Market closely tied to tariff pressure in high-load states.

Integration Complexity with Legacy Building Management Systems

Legacy system complexity remains a major barrier because many buildings still operate with mixed protocols and older controllers. In the North America AI-Powered Energy Management Software Market, this slows deployment when building automation layers do not share a common data structure or an easy application interface. Many sites carry years of BACnet, Modbus, and proprietary controls that were installed in stages rather than designed as one connected architecture. That forces software vendors to spend more time on middleware, custom mapping, and validation before the first analytic model can deliver value. Mid-sized commercial properties are affected the most because they are large enough to justify software investment but often lack specialist integration and staff. This keeps deployment costs elevated and makes the North

Other drivers and restraints analyzed in the detailed report include:

- Portfolio Decarbonization Commitments from Enterprises and Campuses

- Integration With Distributed Energy Resources and Battery Storage

- Cybersecurity and Data Governance Concerns for Connected Energy Data

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 74.12% of the North America AI-Powered Energy Management Software market share in 2025, keeping vendor revenue centered on recurring subscriptions and licensing rather than hardware-led project margins. The North America AI-Powered Energy Management Software Market continues to favor software because customers typically want fast visibility, optimization logic, and reporting without adding significant new field hardware. That revenue profile also gives vendors more room to expand into analytics upgrades, dashboards, forecasting tools, and compliance modules over time. Eaton launched Brightlayer Energy in March 2026 for commercial buildings in healthcare, education, and retail, with functions for real-time analysis, forecasting, automated control, and distributed energy optimization. Product launches like this show how software vendors are tying energy optimization more closely to operational management and local compliance support

Services are smaller in absolute terms, but they are projected to grow at a 17.93% CAGR from 2026 to 2031, slightly ahead of the overall market pace. In the North America AI-Powered Energy Management Software Market, the customer base increasingly needs integration support, managed analytics, and model tuning after initial deployment. Many organizations lack sufficient internal energy analytics or data science staff to maintain complex in-house optimization tools. This is pushing providers to compete on service depth, onboarding quality, and ongoing performance support as much as on software features.

Cloud-based deployment accounted for 63.14% of the market in 2025, reflecting the appeal of simpler rollout and lower infrastructure management for many building and enterprise users. The North America AI-Powered Energy Management Software Market has shifted toward the cloud because multi-site users often need centralized reporting and faster software updates across portfolios. Hybrid deployment is still the fastest-growing mode with an 18.02% CAGR from 2026 to 2031, because many regulated or sensitive environments want analytics scale without fully moving control-plane data outside the local security boundary. That makes hybrid architecture a practical fit for utilities and industrial operators that must keep tighter control over operational systems. It also helps vendors serve customers who want real-time edge decisions on-site while still using cloud layers for broader analytics and oversight.

NERC requirements reinforce the need for careful cyber design when software interfaces with the bulk electric system. AWS and Siemens Energy expanded their collaboration in April 2026 to support digital transformation and energy infrastructure solutions, reflecting how major technology providers are aligning cloud capabilities with the energy sector's operating needs. In the North America AI-Powered Energy Management Software Market, this supports the view that hybrid frameworks will remain central while utilities and large enterprises balance scale, latency, and compliance. Pure on-premises models will remain relevant in more stringent environments, but their relative growth is likely to lag that of more flexible architectures over the forecast period.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

- By Application

- Energy Consumption and Demand Optimization

- Asset Performance and Predictive Maintenance

- Smart Grid and Distributed Energy Resource (DER) Management

- Renewable Energy Forecasting and Integration

- Energy Trading, Pricing and Market Intelligence

- By End User

- Utilities

- Commercial Buildings

- Industrial Facilities

- Residential Buildings

- By Geography

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- Schneider Electric SE

- Siemens AG

- Johnson Controls International plc

- Honeywell International Inc.

- ABB Ltd.

- IBM Corporation

- Oracle Corporation

- Cisco Systems, Inc.

- Enel X North America, Inc.

- Delta Electronics, Inc.

- SAP SE

- Eaton Corporation plc

- Carrier Global Corporation

- Trane Technologies plc

- GridPoint, Inc.

- AutoGrid Systems, Inc

- EnergyHub

- Acuity Brands, Inc.

- AutoGrid Systems, Inc.

- Amperon

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Smart Meter And IoT Sensor Penetration Across Commercial Sites

- 4.2.2 Rising Utility Tariffs And Demand Charges For Peak Load Customers

- 4.2.3 Portfolio Decarbonization Commitments From Enterprises And Campuses

- 4.2.4 Integration With Distributed Energy Resources And Battery Storage

- 4.2.5 AI-Enabled Fault Detection Reducing Energy Waste From Hidden Equipment Drift

- 4.2.6 New Utility Incentives For Automated Demand Response Participation

- 4.3 Market Restraints

- 4.3.1 Integration Complexity With Legacy Building Management Systems

- 4.3.2 Cybersecurity And Data Governance Concerns For Connected Energy Data

- 4.3.3 Long Enterprise Sales Cycles And Solution Validation Requirements

- 4.3.4 Skilled Facility-Analytics Talent Shortage At Mid-Market End Users

- 4.4 Impact of Macroeconomic Factors on The Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Energy Consumption and Demand Optimization

- 5.3.2 Asset Performance and Predictive Maintenance

- 5.3.3 Smart Grid and Distributed Energy Resource (DER) Management

- 5.3.4 Renewable Energy Forecasting and Integration

- 5.3.5 Energy Trading, Pricing and Market Intelligence

- 5.4 By End User

- 5.4.1 Utilities

- 5.4.2 Commercial Buildings

- 5.4.3 Industrial Facilities

- 5.4.4 Residential Buildings

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 Siemens AG

- 6.4.3 Johnson Controls International plc

- 6.4.4 Honeywell International Inc.

- 6.4.5 ABB Ltd.

- 6.4.6 IBM Corporation

- 6.4.7 Oracle Corporation

- 6.4.8 Cisco Systems, Inc.

- 6.4.9 Enel X North America, Inc.

- 6.4.10 Delta Electronics, Inc.

- 6.4.11 SAP SE

- 6.4.12 Eaton Corporation plc

- 6.4.13 Carrier Global Corporation

- 6.4.14 Trane Technologies plc

- 6.4.15 GridPoint, Inc.

- 6.4.16 AutoGrid Systems, Inc

- 6.4.17 EnergyHub

- 6.4.18 Acuity Brands, Inc.

- 6.4.19 AutoGrid Systems, Inc.

- 6.4.20 Amperon

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment