|

시장보고서

상품코드

2073291

유럽의 AI 기반 에너지 관리 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe AI-Powered Energy Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

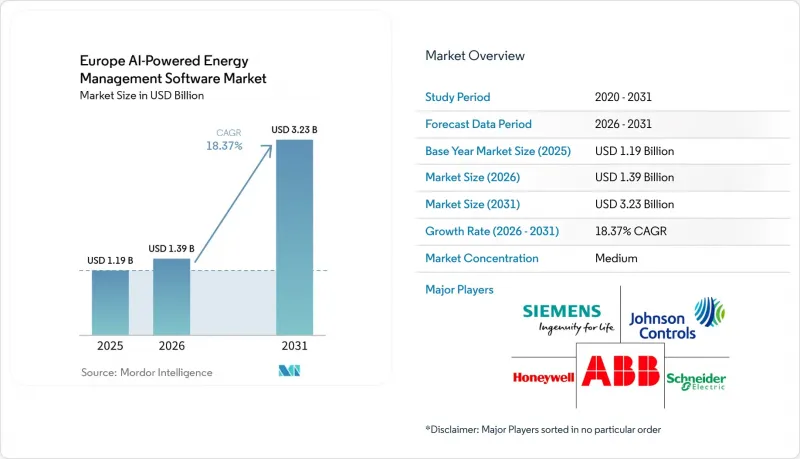

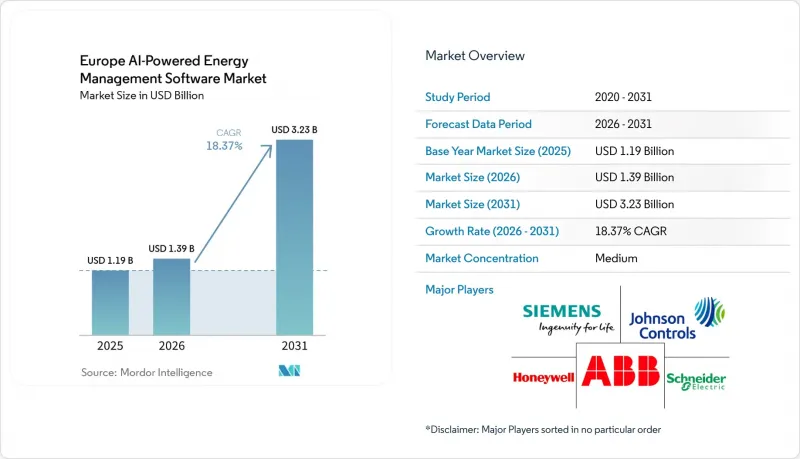

Mordor Intelligence에 의하면, 유럽의 AI 기반 에너지 관리 소프트웨어 시장 규모는 2025년에 11억 9,000만 달러로 평가되었고 2031년까지 32억 3,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 18.37%로 성장할 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 배포 방식(클라우드 기반, On-Premise형, 하이브리드형), 용도(에너지 소비 및 수요 최적화, 자산 성능 및 예측 유지보수 등), 최종 사용자(상업용 건물, 산업 시설 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 AI 기반 에너지 관리 소프트웨어 시장 동향 및 인사이트

유럽 전역의 전력 비용 상승과 부하 변동

급등하고 불안정한 전력 가격으로 인해, 유럽의 AI 기반 에너지 관리 소프트웨어 시장에서 얻을 수 있는 비즈니스상의 이점이 더욱 커지고 있습니다. 2025년 유럽의 도매 다음 날 전력 가격은 평균 88유로/MWh(95달러/MWh)를 기록했으며, 거래 시간의 9.3% 동안 가격이 150유로/MWh(162달러/MWh)를 초과했기 때문에 대규모 포트폴리오에서 수동 스케줄링의 타당성을 유지하기가 어려워지고 있습니다. 구매자들은 더 이상 단순히 에너지 비용 절감만을 바라는 것이 아닙니다. 수동으로 운영하는 팀으로는 달성할 수 없는 수준의 엄격함을 바탕으로, 급격한 가격 변동에 대응할 수 있는 도구도 필요합니다. 이러한 변화가 중요한 이유는 가격 변동이 예측, 자동 배분, 피크 수요 회피 등 유럽의 AI 기반 에너지 관리 소프트웨어 시장의 모든 핵심 기능에서 가치를 창출하기 때문입니다. 의사결정 주기를 단축하고 보다 빈번한 제어 조치를 지원할 수 있는 공급업체는 단순한 보고 업무에 그치지 않고, 운영 워크플로우에 밀접하게 관여하고 있습니다. 그 결과, 에너지 최적화 소프트웨어는 단순한 선택적 분석 계층이라기보다는 운영 인프라로 간주되고 있습니다.

스마트 계량기의 보급률과 상세한 소비 데이터의 입수 가능성

유럽의 AI 기반 에너지 관리 소프트웨어 시장은 상세한 소비 데이터에 대한 접근성이 확대되고 있는 점에서도 혜택을 보고 있습니다. EU 27+3 지역의 스마트 계량기 보급률은 2024년 말까지 58%에 달했으며, EU가 제시한 80%라는 목표를 향해 꾸준히 증가하고 있습니다. 이에 따라 AI 모델에 상세한 사용 현황 신호를 제공할 수 있는 도입 기반이 착실히 확대되고 있습니다. 또한 유럽집행위원회는 스마트 계량기를 활용한 에너지 관리를 통해 계량 지점당 평균 270유로(292달러)의 전력 비용을 절감할 수 있다고 밝혔으며, 이는 소프트웨어의 보다 광범위한 도입에 대한 경제적 타당성을 뒷받침하고 있습니다. 이탈리아나 프랑스 등 1세대 도입률이 이미 높은 수준에 도달한 시장에서는 병목 현상이 데이터 수집 단계에서 데이터 분석 및 제어 로직 단계로 이동하고 있습니다. 독일에서는 2025년 1분기 스마트 계량기 보급률이 고작 2.8%에 그쳤는데, 이는 신규 설치가 이루어질 때마다 장기적으로 볼 때 유럽의 AI 기반 에너지 관리 소프트웨어 시장의 잠재 고객 기반이 확대된다는 것을 의미합니다. 이러한 추세는 성숙한 계량기 시장의 단기적인 도입과 도입이 지연되고 있는 국가들의 장기적인 성장을 모두 뒷받침하고 있습니다.

기존 빌딩 및 산업용 제어 시스템과의 통합에 따른 복잡성

통합의 복잡성은 유럽의 AI 기반 에너지 관리 소프트웨어 시장이 대규모 포트폴리오 전반에 걸쳐 어느 정도의 속도로 성장할 수 있는지에 있어 여전히 가장 뚜렷한 제약 요인 중 하나로 남아 있습니다. 많은 상업시설과 산업 시설에서는 여전히 구식 건물 제어 시스템, 공정 시스템, 그리고 데이터 교환이 원활하게 이루어지지 않는 단편화된 센서 네트워크에 의존하고 있습니다. 이로 인해 도입에 소요되는 시간이 길어지고 테스트의 필요성이 높아질 뿐만 아니라, 입력 데이터가 불완전하거나 불일치할 경우 모델의 품질이 저하될 우려가 있습니다. 또한, 사이트 차원에서 그 가치를 실감하기 전에 구매자는 설정, 미들웨어, 지원에 추가 비용을 지출해야만 합니다. 일부 벤더들은 협업 제어와 엣지 처리 및 클라우드 처리를 결합한 모듈식 플랫폼을 제안하고 있으며, 이를 통해 보다 유연한 시스템 설계를 통해 이 문제를 완화하고자 하고 있음을 보여주고 있습니다. 그럼에도 불구하고, 특히 포트폴리오 소유자가 단일 플랫폼에서 여러 유형의 시설을 포괄하고자 하는 경우, 통합 작업은 도입 속도를 크게 저해하는 요인이 되고 있습니다.

부문별 분석

2025년 유럽의 AI 기반 에너지 관리 소프트웨어 시장에서 소프트웨어가 69.21%를 차지한 것으로 나타났으며, 구매자들이 여전히 하드웨어 기반 도입보다 확장성이 뛰어난 소프트웨어 구독 방식을 선호하는 것으로 확인되었습니다. 이러한 우위는 소프트웨어가 업데이트 빈도가 더 높고, 여러 거점에 배포할 수 있으며, 새로운 설비 도입 주기를 거치지 않고도 새로운 보고서 작성이나 최적화 작업에 대응할 수 있다는 사실을 반영하고 있습니다. 소프트웨어 계층은 예측, 이상 감지, 부하 조정, 배출량 보고가 통합되는 영역이기 때문에 유럽의 AI 기반 에너지 관리 소프트웨어 시장에서 여전히 구매 결정의 핵심 요소로 자리 잡고 있습니다. 또한, 유틸리티, 상업용 빌딩, 산업 시설 등 어느 분야든 서로 다른 제어 로직과 보고서 표시 방식을 채택하면서도 동일한 핵심 플랫폼을 도입할 수 있기 때문에 소프트웨어 부문은 더욱 폭넓은 구매자층으로부터 지지를 받고 있습니다. 많은 고객에게 매력적인 점은 비용 관리뿐만 아니라, 지리적으로 분산된 자산 전반에 걸쳐 에너지 가시화를 표준화할 수 있다는 점에도 있습니다.

서비스 분야는 2031년까지 연평균 성장률(CAGR) 18.44%로 확대될 것으로 예측되며, 이는 유럽의 AI 기반 에너지 관리 소프트웨어 업계가 소프트웨어 자체에서 벗어나는 것이 아니라, 그 주변에 도입 및 최적화 업무를 더욱 추가하고 있음을 보여줍니다. 대규모 고객의 경우, 사내 팀이 플랫폼을 대규모로 효과적으로 활용할 수 있도록 하기 위해서는 시스템 통합, 모델 튜닝, 교육 및 관리형 분석이 필요한 경우가 많습니다. 이는 특히, 운영 조건이 거점마다 달라 에너지 워크플로우를 별다른 조정 없이 그대로 적용할 수 없는 산업 시설이나 여러 거점으로 구성된 빌딩 포트폴리오에서 두드러지게 나타납니다. 각 벤더사는 이에 대응하여, 구독 모델에 도입 지원 및 장기적인 성과 관리를 지원하는 고부가가치 서비스 계층을 결합하는 방식으로 대응하고 있습니다. 그 결과, 유럽의 AI 기반 에너지 관리 소프트웨어 시장에서는 소프트웨어가 수익을 주도하고, 서비스가 고객 유지율, 지속 이용률 및 실현되는 고객 가치를 높이는 구조가 형성되어 있습니다.

2025년, 유럽의 AI 기반 에너지 관리 소프트웨어 시장에서 클라우드 기반 도입은 60.17%의 점유율을 차지하며, 건물 및 유틸리티 분야 전반에 걸쳐 지배적인 도입 모델이 되었습니다. 통합된 데이터 액세스, 간편한 원격 업데이트, 그리고 여러 시설에 걸친 신속한 확장성 덕분에 클라우드 모델은 중간 수준의 실시간 제어 요구 사항이 있는 이용 사례에서 기본적인 선택지가 되고 있습니다. 많은 조직이 초기 단계에서 IT의 복잡성을 줄이고, 지점 간 보고 통합을 용이하게 하기를 원하고 있기 때문에 이러한 추세는 기업의 구매 패턴과도 일치합니다. 유럽의 AI 기반 에너지 관리 소프트웨어 시장에서 클라우드 도입은 광범위한 포트폴리오 파악이 필요한 지속가능성 보고, 비용 벤치마킹 및 소비 분석 분야에서 특히 매력적입니다. 또한, 구독형 가격 책정이나 더 빈번한 기능 출시 추진과도 부합합니다.

하이브리드 도입은 2031년까지 연평균 성장률(CAGR) 18.53%로 확대될 것으로 예상되며, 이는 시장이 클라우드의 경제성과 현장 수준의 운영 실태 사이에서 균형을 맞추고 있음을 보여줍니다. 중요 인프라 운영자나 에너지 집약적 제조업자는 일부 제어 스택을 자산 근처에 배치해야 하는 경우가 많습니다. 이는 일부 작업을 낮은 지연 시간으로 실행하고, 보다 엄격한 시스템 분리를 보장해야 하기 때문입니다. 하이브리드 모델을 통해 예측, 벤치마킹, 포트폴리오 분석을 보다 광범위한 클라우드 환경으로 이전하는 동시에, 현장에 결정론적 제어 루프를 유지할 수 있게 됩니다. 이에 따라 유럽의 AI 기반 에너지 관리 소프트웨어 시장에서 하이브리드 아키텍처는 기존의 현장 환경과 새로운 기업 소프트웨어 전략을 연결하는 실용적인 가교 역할을 하고 있습니다. 에지 처리 계층과 클라우드 처리 계층을 모두 갖춘 모듈형 플랫폼은 이러한 하이브리드 도입 로직을 직접 지원합니다. 규제가 엄격한 현장이나 연결성에 제약이 있는 현장에서는 On-Premise형 시스템이 여전히 중요하지만, 더 복잡한 프로젝트에서 하이브리드 구성이 바람직한 타협안이 되면서 그 상대적인 역할은 점차 축소되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the europe AI-powered energy management software market size was valued at USD 1.19 billion in 2025 and is projected to reach USD 3.23 billion by 2031, growing at a CAGR of 18.37% during 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, and More), End User (Commercial Buildings, Industrial Facilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe AI-Powered Energy Management Software Market Trends and Insights

Rising Electricity Costs and Load Volatility Across Europe

High and unstable electricity prices have strengthened the commercial case for the Europe AI-powered energy management software market. European wholesale day-ahead electricity averaged EUR 88/MWh (USD 95/MWh) in 2025, and prices exceeded EUR 150/MWh (USD 162/MWh) in 9.3% of trading hours, making manual scheduling harder to justify for large portfolios. Buyers are no longer looking only for lower energy bills; they also need tools that can respond to rapid price swings with the discipline manual teams cannot. This shift matters because volatility creates value for forecasting, automated dispatch, and peak avoidance, which are all core functions of the Europe AI-powered energy management software market. Vendors that can support shorter decision cycles and more frequent control actions are moving closer to operational workflows rather than staying in reporting-only roles. The result is that energy optimization software is being treated more like operating infrastructure than an optional analytics layer.

Smart Meter Penetration and Granular Consumption Data Availability

The Europe AI-powered energy management software market is also benefiting from broader access to granular consumption data. Smart meter penetration across the EU27+3 region reached 58% by the end of 2024 and continued to move toward the EU target of 80%, which is steadily enlarging the installed base that can feed AI models with detailed usage signals. The European Commission has also stated that smart meter-enabled energy management can deliver average electricity savings of EUR 270 (USD 292) per metering point, which supports the financial case for wider software adoption. In markets such as Italy and France, where first-generation rollout has already reached high penetration, the bottleneck has shifted from data collection to data interpretation and control logic. In Germany, smart meter penetration was only 2.8% in Q1 2025, meaning each new installation expands the addressable base for the Europe AI-powered energy management software market over the long term. This pattern supports both near-term adoption in mature meter markets and longer runway growth in late-moving countries.

Integration Complexity With Legacy Building and Industrial Control Systems

Integration complexity remains one of the clearest limits on how fast the Europe AI-powered energy management software market can scale across large portfolios. Many commercial and industrial sites still rely on older building controls, process systems, and fragmented sensor networks that do not exchange data smoothly. This raises implementation time, increases testing needs, and can weaken model quality if the incoming data is incomplete or inconsistent. It also pushes buyers to spend more on configuration, middleware, and support before they see value at the site level. Some vendors are positioning modular platforms that combine coordinated control with both edge and cloud processing, demonstrating how they aim to reduce this problem through more flexible system design. Even so, integration work remains a significant drag on rollout speed, especially when portfolio owners want a single platform to cover multiple facility types.

Other drivers and restraints analyzed in the detailed report include:

- EU Building Efficiency Compliance Pressure on Commercial Portfolios

- AI-Enabled Forecasting for Demand Response and Peak Shaving

- Data Privacy, Cybersecurity, and AI Governance Compliance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 69.21% of the Europe AI-powered energy management software market in 2025, confirming that buyers still prefer scalable software subscriptions over hardware-based deployments. This lead reflects the fact that software can be updated more often, rolled out across multiple sites, and adapted to new reporting or optimization tasks without a new equipment cycle. The software layer is where forecasting, anomaly detection, load shaping, and emissions reporting come together, so it remains the center of the buying decision in the Europe AI-powered energy management software market. The software segment also benefits from a broader buyer base, as utilities, commercial buildings, and industrial facilities can all deploy the same core platform with different control logic and reporting views. For many customers, the appeal is not only cost control, but also the ability to standardize energy visibility across geographically dispersed assets.

Services are projected to expand at a 18.44% CAGR through 2031, indicating that the Europe AI-powered energy management software industry is not moving away from software but is adding more implementation and optimization work around it. Large accounts often need system integration, model tuning, training, and managed analytics before internal teams can use the platform effectively at scale. This is especially true in industrial and multi-site building portfolios where operating conditions differ by site, and energy workflows cannot be copied without adjustment. Vendors are responding by combining subscription models with higher-value service layers that support onboarding and long-term performance management. The result is a component mix where software leads revenue and services deepen stickiness, retention, and realized customer value within the Europe AI-powered energy management software market.

Cloud-based deployment held a 60.17% share of the European AI-powered energy management software market in 2025, making it the dominant deployment model across buildings and utility analytics use cases. Centralized data access, easier remote updates, and faster scaling across multiple facilities have made cloud models the default choice for moderate real-time control requirements. This preference also aligns with enterprise buying patterns, as many organizations seek lower upfront IT complexity and easier reporting consolidation across sites. In the European AI-powered energy management software market, cloud deployment is particularly attractive for sustainability reporting, cost benchmarking, and consumption analytics that need a broad portfolio view. It also aligns with the push toward subscription pricing and more frequent feature releases.

Hybrid deployment is expected to expand at a 18.53% CAGR through 2031, indicating that the market is balancing cloud economics with site-level operational realities. Critical infrastructure operators and energy-intensive manufacturers often need parts of the control stack to stay closer to the asset because some actions must occur with low latency and with tighter system separation. Hybrid models let them keep deterministic control loops on site while moving forecasting, benchmarking, and portfolio analytics into broader cloud environments. This makes hybrid architecture a practical bridge between legacy site conditions and newer enterprise software strategies in the Europe AI-powered energy management software market. Modular platforms with both edge and cloud processing layers directly support this blended deployment logic. On-premises systems still matter in regulated or connectivity-constrained sites, but their relative role is narrowing as hybrid setups become the preferred compromise for more complex accounts.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

- By Application

- Energy Consumption and Demand Optimization

- Asset Performance and Predictive Maintenance

- Smart Grid and Distributed Energy Resource (DER) Management

- Renewable Energy Forecasting and Integration

- Energy Trading, Pricing and Market Intelligence

- By End User

- Utilities

- Commercial Buildings

- Industrial Facilities

- Residential Buildings

- By Geography

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

List of Companies Covered in this Report:

- ABB Ltd.

- Schneider Electric SE

- Siemens AG

- Honeywell International Inc.

- Johnson Controls International plc

- IBM Corporation

- SAP SE

- Schneider Electric S.E.

- Cisco Systems, Inc.

- Carrier Global Corporation

- Emerson Electric Co.

- GridPoint, Inc.

- EnergyCAP, LLC

- Enel X S.r.l.

- Dexma Sensors, S.L.U.

- C3.ai, Inc.

- METRON

- enercast GmbH

- Spacewell International N.V.

- Kaluza Limited

- BrainBox AI Inc.

- GridBeyond Limited

- Energyworx B.V.

- Power Factors, LLC

- Verdigris Technologies, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Electricity Costs and Load Volatility Across Europe

- 4.2.2 Smart Meter Penetration and Granular Consumption Data Availability

- 4.2.3 EU Building Efficiency Compliance Pressure on Commercial Portfolios

- 4.2.4 AI Enabled Forecasting for Demand Response and Peak Shaving

- 4.2.5 Faster Return on Investment from Cloud Native Energy Optimization

- 4.2.6 Carbon Reporting and Decarbonization Commitments from Large Enterprises

- 4.3 Market Restraints

- 4.3.1 Integration Complexity With Legacy Building and Industrial Control Systems

- 4.3.2 Data Privacy, Cybersecurity, and AI Governance Compliance Burden

- 4.3.3 Fragmented Facility Ownership Slowing Portfolio Scale-Up

- 4.3.4 Skilled Implementation Shortage for Energy AI Deployment and Tuning

- 4.4 Impact of Macroeconomic Factors on The Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Energy Consumption and Demand Optimization

- 5.3.2 Asset Performance and Predictive Maintenance

- 5.3.3 Smart Grid and Distributed Energy Resource (DER) Management

- 5.3.4 Renewable Energy Forecasting and Integration

- 5.3.5 Energy Trading, Pricing and Market Intelligence

- 5.4 By End User

- 5.4.1 Utilities

- 5.4.2 Commercial Buildings

- 5.4.3 Industrial Facilities

- 5.4.4 Residential Buildings

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Russia

- 5.5.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Schneider Electric SE

- 6.4.3 Siemens AG

- 6.4.4 Honeywell International Inc.

- 6.4.5 Johnson Controls International plc

- 6.4.6 IBM Corporation

- 6.4.7 SAP SE

- 6.4.8 Schneider Electric S.E.

- 6.4.9 Cisco Systems, Inc.

- 6.4.10 Carrier Global Corporation

- 6.4.11 Emerson Electric Co.

- 6.4.12 GridPoint, Inc.

- 6.4.13 EnergyCAP, LLC

- 6.4.14 Enel X S.r.l.

- 6.4.15 Dexma Sensors, S.L.U.

- 6.4.16 C3.ai, Inc.

- 6.4.17 METRON

- 6.4.18 enercast GmbH

- 6.4.19 Spacewell International N.V.

- 6.4.20 Kaluza Limited

- 6.4.21 BrainBox AI Inc.

- 6.4.22 GridBeyond Limited

- 6.4.23 Energyworx B.V.

- 6.4.24 Power Factors, LLC

- 6.4.25 Verdigris Technologies, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment