|

시장보고서

상품코드

2073289

유럽의 복리후생 관리 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Benefits Administration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

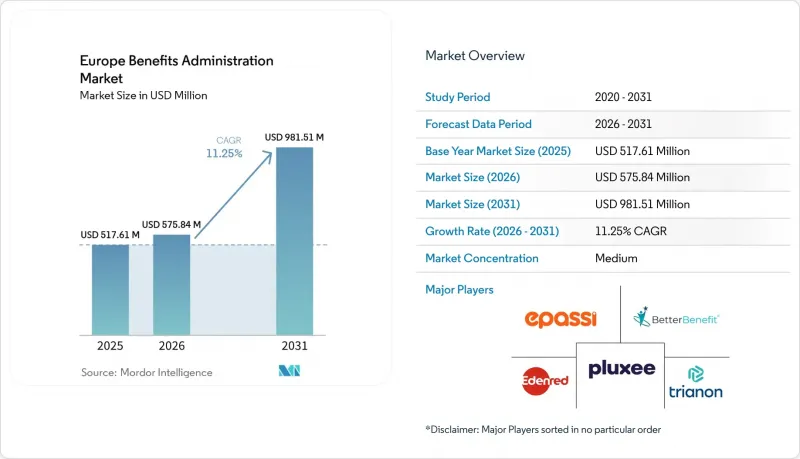

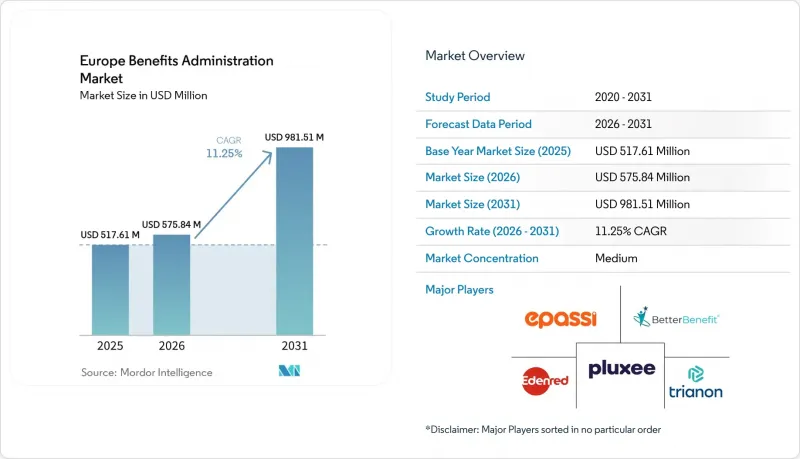

Mordor Intelligence에 의하면, 유럽의 복리후생 관리 시장 규모는 2025년에 5억 1,761만 달러로 평가되었습니다. 2026년에 5억 7,584만 달러에 달하고, 2031년까지 9억 8,151만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 11.25%로 성장할 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 솔루션 유형(퇴직·연금 관리 등), 도입 형태(클라우드 기반, On-Premise형, 하이브리드형), 조직 규모(대기업 및 중소기업), 최종 사용자 산업 분야(헬스케어 및 생명과학 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 복리후생 관리 시장 동향 및 인사이트

EU의 급여 투명성 지침에 따라 총보상(Total Reward)에 관한 데이터 요건이 강화됩니다.

EU의 임금 투명성 지침은 복리후생 데이터를 단순한 인사 기록의 보충 정보에서 공식적인 규정 준수 요건으로 격상시키는 것이므로, 유럽의 복리후생 관리 시장에 있어 단기적으로 가장 명확한 촉진요인이 되고 있습니다. 회원국은 2026년 6월 7일까지 해당 지침을 적용했으며, 이에 따라 고용주는 첫 번째 완전한 보고 주기가 시작되기 전에 보고 체계를 마련해야 합니다. EU 역내에서 250명 이상의 직원을 고용하는 고용주는 2026년 이후부터 변동 보수 및 복리후생 요소를 포함한 남녀 간 임금 격차 보고서를 제출해야 하며, 보고는 2027년부터 시작됩니다. 이로 인해 조직은 급여, 복리후생, 인사 시스템 전반에 걸친 보상 데이터의 평가 및 분류 방식을 표준화할 수밖에 없게 되었으며, 통합 관리 플랫폼의 매력이 더욱 커지고 있습니다. 또한, 이 지침은 지속적인 규정 준수 사이클을 만들어내고 있습니다. 이는 5%를 초과하는 정당한 사유 없는 임금 격차가 있는 고용주는 근로자 대표와 공동으로 임금 평가를 실시해야 하기 때문입니다. 이로 인해 일회성 감사가 아닌, 상시 이용 가능한 분석 기능의 필요성이 강조되고 있습니다. 각국 정부가 독자적인 요건과 일정을 추가하는 가운데, 유럽의 복리후생 관리 시장에서는 개별적인 현지 대응 없이도 각국의 차이점을 수용할 수 있는 시스템에 대한 수요가 높아지고 있습니다.

다자간 규정 준수 자동화에 대한 수요 증가

유럽의 복리후생 관리 시장은 세제, 급여 계산, 연금, 보고 규정이 서로 다른 여러 유럽 관할 구역에 걸쳐 복리후생 프로그램을 운영해야 하는 복잡성이 커지고 있는 점도 긍정적인 요인으로 작용하고 있습니다. 이 지역 전체에서 사업을 운영하는 고용주들은 현지 급여 계산 팀, 중개인, 관리자 간의 수작업 조정이 인사 부서의 시간을 지나치게 소모하고, 피할 수 있는 실수를 초래하고 있다는 사실을 깨닫기 시작했습니다. 인사 시스템 도입 전문가들은 2026년, 자동화가 제한적인 다국적 환경에서 관리 업무가 인사 부서의 근무 시간 중 최대 57%를 차지할 가능성이 있다고 보고하고 있으며, 이로 인해 플랫폼에 대한 투자 대비 효과를 정당화하기가 쉬워지고 있습니다. 이러한 수요로 인해, 단순한 가입 절차의 프런트엔드를 제공하는 데 그치지 않고, 복리후생 워크플로우와 급여 계산 시스템 간의 연동, 그리고 현지 규정 준수 로직을 결합할 수 있는 제공업체의 입지가 더욱 공고해지고 있습니다. SD Worx가 유럽 27개국에 진출해 있는 규모와 2025년 매출 13억 700만 유로(14억 1,000만 달러)라는 실적은 국경을 초월한 규정 준수 대응을 표준 기능으로 해결하는 것의 상업적 가치를 보여줍니다. 보고 의무가 확대됨에 따라 조달 기준은 통합의 품질, 감사 가능성 및 현지 규정 준수로 전환되고 있으며, 이는 유럽의 복리후생 관리 시장의 기술 기준을 높이고 있습니다.

데이터 개인정보 보호와 국경을 넘는 데이터 전송의 부담

복리후생 플랫폼은 여러 관할 구역에 걸쳐 기밀성이 높은 개인정보, 급여 정보, 건강 관련 데이터를 처리하기 때문에 데이터 개인정보 보호는 여전히 유럽의 복리후생 관리 시장에서 가장 큰 제약 요인 중 하나입니다. GDPR(EU 개인정보보호규정)(일반 데이터 보호 규정)은 지속적인 문서화, 거버넌스, 위험 평가에 대한 요건을 부과하고 있으며, 대규모 사내 규정 준수 팀을 갖추지 못한 중견 기업에게 이러한 의무는 더 큰 부담이 되고 있습니다. “슈렘스 II 판결”이후, 인사 데이터를 미국 기반 클라우드 환경으로 전송하는 고용주는 전송 영향 평가를 완료하고, EU가 관리하는 키를 사용한 암호화 등의 기술적 보호 조치를 시행해야 합니다. EU·미국 데이터 개인정보 보호 프레임워크 덕분에 인증된 데이터 전송 과정에서 발생하는 마찰은 일부 완화되었지만, 향후 법적 분쟁의 가능성은 여전히 많은 고용주들에게 우려 사항으로 남아 있어, EU 역외에서의 장기적인 아키텍처 선택에 있어 신중한 태도를 취하게 하고 있습니다. 독일의 고용법은 또 다른 과제를 안겨주고 있습니다. 인사 데이터의 일원화 처리에는 엄격한 '필요성 심사'를 충족해야 하며, 이로 인해 다국적 기업이 업무 효율화만을 목적으로 복리후생 데이터를 일원화하는 것이 제한되기 때문입니다. 따라서 유럽의 복리후생 관리 시장에서는 EU 내에 호스팅된 인프라가 확실히 선호되고 있습니다. 그러나 이러한 경향은 공급업체 비용의 상승, 조달 절차의 지연, 도입 일정의 장기화를 초래할 가능성이 있습니다.

부문별 분석

2025년, 소프트웨어는 유럽의 복리후생 관리 시장의 68.12%를 차지하며, 이 부문에서 확실한 수익 기반으로서의 입지를 유지했습니다. 고용주는 수급 자격 심사, 가입 절차, 직원용 셀프 서비스 및 보고서 작성을 위한 핵심 엔진을 지속적으로 우선시해 왔습니다. 이러한 기능들은 수작업에 의존하는 관리 방식에서 벗어나기 위한 첫걸음이 되기 때문입니다. 또한, 이 소프트웨어는 모든 프로세스를 즉시 외부에 위탁하지 않고 각국에 공통된 운영 계층을 구축하고자 하는 조직의 예산상 우선순위와도 부합합니다. 그렇긴 하지만, 서비스 부문은 2031년까지 연평균 성장률(CAGR) 14.02%를 나타낼 것으로 예측되며, 이는 유럽의 복리후생 관리 시장 전체의 성장률을 상회하는 수치이므로 수익 구성은 변화하고 있습니다.

이 서비스 부문의 급속한 성장은 직원 대표 위원회, GDPR(EU 개인정보보호규정)(일반 데이터 보호 규정) 규제, 급여 계산 매핑, 보험사와의 조정 등이 특징인 지역에서 소프트웨어만으로는 도입의 복잡성을 해결할 수 없습니다는 사실을 반영하고 있습니다. 여러 EU 국가로 사업을 확장하는 고용주는 도입, 규칙 수립, 규정 준수 해석 및 변경 관리에 있어 여전히 외부 지원이 필요합니다. Benifex는 2026년 1월, 전 세계 고용주의 32%가 이미 단일 통합 복리후생 관리 플랫폼을 이용하고 있으며, 14%는 지역별로 여러 플랫폼을 이용하고 있다고 보고했습니다. 이는 플랫폼 도입이 진행되고 있음에도 불구하고, 여전히 자문 지원이 필요한 경우가 많다는 것을 보여줍니다. 이 조사에 따르면, 전 세계 고용주의 51%가 HR 시스템과 복리후생 플랫폼의 통합을 최우선 과제로 삼고 있는 것으로 나타났으며, 이에 따라 당연히 서비스 중심의 제공에 대한 수요가 증가하고 있습니다. 유럽의 복리후생 관리 업계에서는 소프트웨어가 여전히 주요 지출 항목인 반면, 예측 기간 동안에는 서비스가 더 강력한 성장 동력이 되고 있습니다.

2025년 기준으로, 핵심 관리 플랫폼은 유럽 복리후생 관리 시장의 41.16%를 차지했으며, 이는 가입 절차, 수급 자격 및 청구 대조 분야에서 주요 기록 시스템으로서의 역할을 반영한 것입니다. 이러한 도구들은 스프레드시트나 분산된 로컬 워크플로우에서 전환을 모색하는 고용주들에게 여전히 일반적인 출발점이 되고 있습니다. 또한, 이러한 주도적인 위상은 많은 조직이 우선적으로 고도의 사용자 경험 기반을 구축하기보다는 여전히 레거시 관리 시스템의 교체를 중점적으로 추진하고 있음을 보여줍니다. 한편, 직장 복리후생 관리 시장은 2031년까지 연평균 성장률(CAGR) 13.14%를 기록하며 성장할 것으로 예상되며, 유럽의 복리후생 관리 시장에서 가장 빠르게 확대될 솔루션 분야가 될 전망입니다.

이러한 성장은 모빌리티, 웰빙, 바우처, 유연한 라이프스타일 예산 등 고용주가 자금을 지원하며 직원이 자유롭게 사용할 수 있는 지출 항목으로의 명확한 전환을 반영하고 있습니다. 고용주들이 단일 디지털 경험을 통해 개인 맞춤화 및 소통이 용이한 복리후생 프로그램을 요구함에 따라, 업무용 도구의 중요성이 커지고 있습니다. 또한, 단일 카드 및 앱 기반 시스템을 통해 여러 가지 재량형 복리후생 제도를 하나의 인터페이스로 통합함으로써 관리 업무의 부담을 줄이고 있습니다. 퇴직 및 연금 관리는 여전히 중요한 관련 분야이며, 특히 영국에서는 대시보드 지원 및 데이터 정제 기술의 발전에 힘입어 최신 관리 계층의 가치가 높아지고 있습니다. 따라서 유럽의 복리후생 관리 업계는 기본적인 복리후생 처리에서 벗어나, 법정 관리와 직원 대상 선택권을 모두 지원하는 보다 광범위한 플랫폼 모델로 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.07According to Mordor Intelligence, the europe benefits administration market size is projected to be USD 517.61 million in 2025, USD 575.84 million in 2026, and reach USD 981.51 million by 2031, growing at a CAGR of 11.25% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Solution Type (Retirement and Pension Administration, and More), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe Benefits Administration Market Trends and Insights

EU Pay Transparency Directive Elevates Total Reward Data Requirements

The EU Pay Transparency Directive is the clearest near-term driver for the Europe benefits administration market because it moves benefits data from a supporting HR record into a formal compliance requirement. Member states must apply the directive by June 7, 2026, which is forcing employers to prepare their reporting structures before the first full reporting cycle begins. Employers with 250 or more employees in the EU must file gender pay gap reports that include variable pay and benefits components from the 2026 calendar year onward, with reporting beginning in 2027. This pushes organizations to standardize how they value and classify rewards data across payroll, benefits, and HR systems, which increases the appeal of unified administration platforms. The directive also creates an ongoing compliance loop, as employers with an unjustified pay gap above 5% must complete a joint pay assessment with employee representatives, underscoring the need for always-available analytics rather than one-time audits. As national governments add their own requirements and timelines, the Europe benefits administration market is benefiting from demand for systems that can handle country variation without separate local builds.

Rising Need for Multi-Country Compliance Automation

The Europe benefits administration market is also being boosted by the growing complexity of running benefit programs across multiple European jurisdictions with different tax, payroll, pension, and reporting rules. Employers operating across the region are finding that manual coordination among local payroll teams, brokers, and administrators consumes too much HR time and leads to avoidable errors. HR implementation specialists reported in 2026 that administration can take up to 57% of HR working time in multi-country environments when automation is limited, which makes the return on platform investment easier to justify. This demand is strengthening providers that can combine benefits workflows with payroll connectivity and local compliance logic, rather than offering a simple enrollment front end. SD Worx's scale across 27 European countries and its 2025 revenue base of EUR 1.307 billion (USD 1.41 billion) show the commercial value of solving compliance across borders as a built-in capability. As reporting obligations expand, procurement criteria are shifting toward integration quality, auditability, and support for local rules, raising the technical standard for the Europe benefits administration market.

Data Privacy and Cross-Border Data Transfer Burdens

Data privacy remains one of the strongest brakes on the Europe benefits administration market because benefit platforms process sensitive personal, salary, and health-related data across multiple legal jurisdictions. GDPR creates ongoing documentation, governance, and risk assessment requirements, and those obligations fall more heavily on mid-sized employers that lack large internal compliance teams. Post-Schrems II, employers transferring HR data to U.S.-based cloud environments have had to complete transfer impact assessments and implement technical safeguards, such as encryption using EU-controlled keys. The EU-U.S. Data Privacy Framework reduced some friction for certified transfers, but the possibility of future legal challenges remains a concern for many employers, making them cautious about long-term architecture choices outside the EU. German employment law adds another layer because centralized HR data processing must meet a strict necessity test, which limits how easily multinational groups can centralize benefits data for operational efficiency alone. This leaves the Europe benefits administration market with a clear preference for EU-hosted infrastructure, but that preference can raise vendor costs, slow procurement, and stretch implementation timelines.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Migration Across European HR Stacks

- Cross-Border Remote Work Expands A1 and Social Security Administration Complexity

- Integration Complexity with Legacy Payroll, Carrier, and Pension Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 68.12% of the Europe benefits administration market in 2025, which kept it as the clear revenue base for the category. Employers continued to prioritize core engines for eligibility, enrollment, employee self-service, and reporting because those functions are the first step away from manual administration. Software also fits the budget priorities of organizations that want a common operating layer across countries without immediately outsourcing every process. Even so, the revenue mix is changing because services are projected to grow at a 14.02% CAGR through 2031, which is faster than the overall Europe benefits administration market.

That faster services growth reflects the fact that software alone does not solve deployment complexity in a region shaped by works councils, GDPR controls, payroll mapping, and carrier coordination. Employers expanding across several EU countries still need outside support for implementation, rule configuration, compliance interpretation, and change management. Benifex reported in January 2026 that 32% of employers globally already use a single, unified benefits management platform, while 14% use multiple platforms across regions, indicating that platform adoption is advancing but still often requires advisory support. The same research found that 51% of global employers prioritize integrating HR systems with benefits platforms, which naturally increases the demand for services-led delivery. In the Europe benefits administration industry, software remains the core spend category, while services are the stronger growth lever over the forecast period.

Core administration platforms accounted for 41.16% of the Europe benefits administration market in 2025, reflecting their role as the main system of record for enrollment, eligibility, and billing reconciliation. These tools remain the usual starting point for employers moving away from spreadsheets or fragmented local workflows. Their lead position also shows that many organizations are still focused on replacing legacy administration rather than building advanced experience layers first. At the same time, worksite benefits administration is expected to grow at a 13.14% CAGR through 2031, making it the fastest-moving solution area in the Europe benefits administration market.

This growth reflects a clear shift toward employer-funded but employee-directed spending categories such as mobility, wellbeing, vouchers, and flexible lifestyle budgets. Worksite tools are becoming more relevant as employers seek benefit programs that are easier to personalize and communicate through a single digital experience. Single-card and app-based structures also reduce administrative effort by consolidating several discretionary benefits into a single interface. Retirement and pension administration remains an important adjacent category, especially in the United Kingdom, where dashboard readiness and data cleanup are raising the value of modern administration layers. The Europe benefits administration industry is therefore broadening from basic benefit processing into a wider platform model that supports both statutory administration and employee-facing choice.

Complete Report Scope:

- By Component

- Software

- Services

- By Solution Type

- Core Administration Platforms

- Voluntary Benefits Administration

- Retirement and Pension Administration

- Worksite Benefits Administration

- Employee Decision Support and Self-Service

- Other Solution Types

- By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By End-user Industry

- Information Technology and Telecommunications

- Banking, Financial Services, and Insurance

- Healthcare and Life Sciences

- Manufacturing

- Retail and E-Commerce

- Other End-user Industries

- By Geography

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Nordics

- Poland

- Rest of Europe

List of Companies Covered in this Report:

- Benefex Limited

- EDENRED SE

- Pluxee N.V.

- Epassi Group Oy

- Reward Gateway (UK) Ltd

- SME HCI Limited

- Universal Cover, SA

- SPENDIT AG

- Thanks Ben Ltd

- Yonder Technology Limited

- Zest Technology Ltd.

- BetterBenefit GmbH

- Swile, societe par actions simplifiee

- Trianon SA

- Aptia UK Limited

- PlanSource Benefits Administration, Inc.

- Benefitfocus.com, Inc.

- Businessolver.com Inc.

- bswift LLC

- Empower Benefits, Inc. dba Corestream

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud Migration across European HR Stacks

- 4.2.2 Rising Need for Multi-Country Compliance Automation

- 4.2.3 Growing SME Adoption of Configurable SaaS Platforms

- 4.2.4 Demand for Personalized and Mobile-First Benefits Experiences

- 4.2.5 EU Pay Transparency Directive Elevates Total Reward Data Requirements

- 4.2.6 Cross-Border Remote Work Expands A1 and Social Security Administration Complexity

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cross-Border Data Transfer Burdens

- 4.3.2 Integration Complexity with Legacy Payroll, Carrier, and Pension Systems

- 4.3.3 Works Council and Co-Determination Delays in DACH Rollouts

- 4.3.4 Carrier and Benefits Provider Connectivity Fragmentation across Europe

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Solution Type

- 5.2.1 Core Administration Platforms

- 5.2.2 Voluntary Benefits Administration

- 5.2.3 Retirement and Pension Administration

- 5.2.4 Worksite Benefits Administration

- 5.2.5 Employee Decision Support and Self-Service

- 5.2.6 Other Solution Types

- 5.3 By Deployment Mode

- 5.3.1 Cloud-Based

- 5.3.2 On-Premises

- 5.3.3 Hybrid

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-Sized Enterprises

- 5.5 By End-user Industry

- 5.5.1 Information Technology and Telecommunications

- 5.5.2 Banking, Financial Services, and Insurance

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 Manufacturing

- 5.5.5 Retail and E-Commerce

- 5.5.6 Other End-user Industries

- 5.6 By Geography

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Netherlands

- 5.6.7 Nordics

- 5.6.8 Poland

- 5.6.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Benefex Limited

- 6.4.2 EDENRED SE

- 6.4.3 Pluxee N.V.

- 6.4.4 Epassi Group Oy

- 6.4.5 Reward Gateway (UK) Ltd

- 6.4.6 SME HCI Limited

- 6.4.7 Universal Cover, SA

- 6.4.8 SPENDIT AG

- 6.4.9 Thanks Ben Ltd

- 6.4.10 Yonder Technology Limited

- 6.4.11 Zest Technology Ltd.

- 6.4.12 BetterBenefit GmbH

- 6.4.13 Swile, societe par actions simplifiee

- 6.4.14 Trianon SA

- 6.4.15 Aptia UK Limited

- 6.4.16 PlanSource Benefits Administration, Inc.

- 6.4.17 Benefitfocus.com, Inc.

- 6.4.18 Businessolver.com Inc.

- 6.4.19 bswift LLC

- 6.4.20 Empower Benefits, Inc. dba Corestream

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment