|

시장보고서

상품코드

2073300

직원 복리후생 기술 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Employee Benefits Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

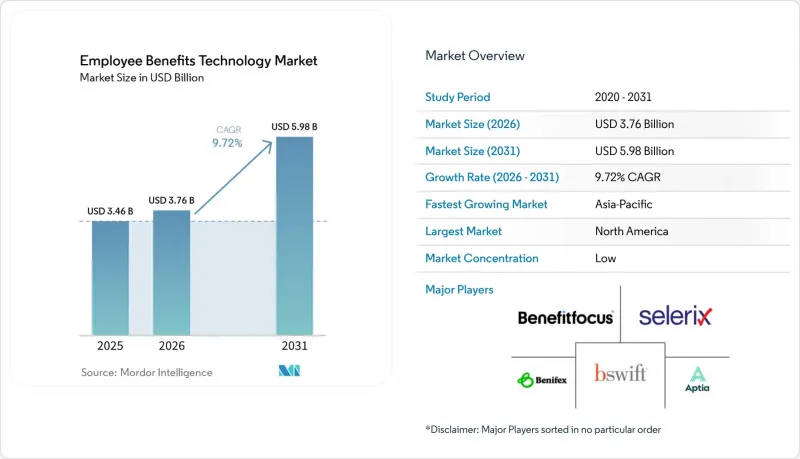

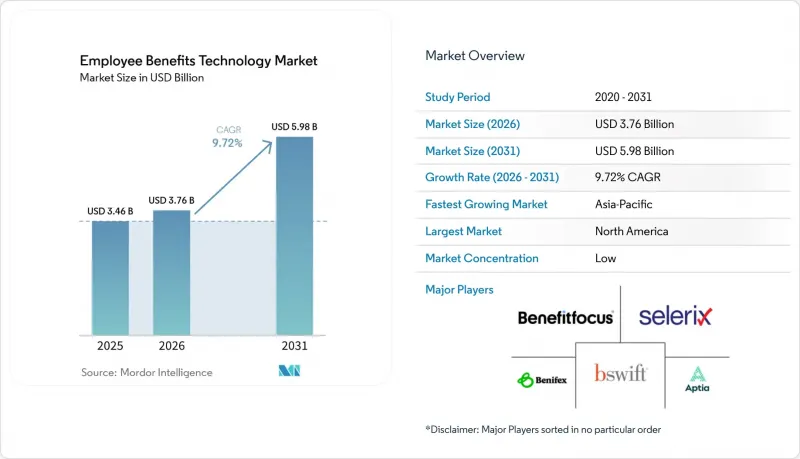

Mordor Intelligence에 의하면, 직원 복리후생 기술 시장 규모는 2025년에 34억 6,000만 달러로 평가되었습니다. 2026년에는 37억 6,000만 달러, 2031년까지 59억 8,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 9.72%로 성장할 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 배포 모델(클라우드 기반 및 On-Premise형), 조직 규모(대기업 및 중소기업), 기능(가입·자격 관리, 핵심 복리후생 관리 등), 최종 사용자 산업 분야(은행, 금융서비스 및 보험(BFSI), IT 및 통신 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 직원 복리후생 기술 시장 동향 및 인사이트

복리후생 제도의 복잡화와 규정 준수 자동화에 대한 수요 증가

직원 복리후생 기술 시장은 국가 및 지방 자치단체 차원의 복리후생 규정이 복잡해지는 것을 배경으로 지지를 넓혀가고 있습니다. 미국에서는 2026년에 ACA(환자 보호 및 의료비 부담 적정화법)의 “고용주 공동책임 벌칙 B"는 규정 준수 요건을 충족하지 않는 보험 제공에 대해 직원 1인당 4,350달러로 설정되어 있어, 여전히 수작업에 의존해 추적하고 있는 고용주들에게는 규정 위반 위험이 여전히 높은 수준을 유지하고 있습니다. 또한, 고용주는 ACA 보고, 휴가 관리, COBRA 관리, ERISA 절차, HIPAA 관련 데이터 처리 등 보다 광범위한 규정 준수 업무를 관리해야 하므로, 이에 따라 통합형 자동화 도구의 가치가 높아지고 있습니다. AI를 활용한 컴플라이언스 엔진이 ACA 1095-C 양식의 자동 생성, FMLA(가족 의료 휴가법) 적용 자격 추적, 그리고 제재 위험의 실시간 모니터링에 점점 더 많이 활용되고 있으며, 도입 사례를 통해 수동 모니터링 시간을 70-80% 단축할 수 있었던 것으로 확인되었습니다. 이러한 변화로 인해 직원 복리후생 기술 시장은 백오피스용 소프트웨어 부문에서 고용주의 리스크 관리를 담당하는 제어 계층으로 전환되고 있습니다.

인사 및 복리후생 시스템 전체의 클라우드 전환

또한, 고용주들이 분산된 도구를 통합 플랫폼으로 대체함에 따라, 인사 및 복리후생 시스템 전반에 걸친 클라우드 전환 역시 직원 복리후생 기술 시장의 성장을 뒷받침하고 있습니다. Alight Solutions사는 2025년 2월에 AWS로의 이전을 완료했으며, 이를 통해 연간 7,500만 달러의 비용 절감, 서버 설치 공간 40% 축소, 가입 절차 응답 시간 43% 단축을 달성했습니다. 이러한 성과가 중요하게 여겨지는 이유는 클라우드 전환이 더 이상 인프라 비용 절감에 그치지 않고, 그동안 수작업에 의한 대조를 통해 유지되어 온 보험사와의 연계, 수급 자격 규칙, 데이터 정의 정리를 고용주가 직접 수행하도록 유도하게 되었기 때문입니다. 이러한 정리 단계에서는 도입, 통합 및 지속적인 계획 수립에 대한 서비스 수요가 증가하는 경우가 많으며, 이는 직원 복리후생 기술 시장에서 더 큰 서비스 기회를 뒷받침하고 있습니다. 또한, 규제가 엄격한 환경에서도 하이브리드 도입 모델의 중요성이 커지고 있습니다. 이러한 환경에서는 고용주가 클라우드의 경제성을 추구하는 한편, 여전히 로컬에서의 데이터 처리나 인사 정보의 흐름에 대한 보다 엄격한 법적 감독을 필요로 하고 있기 때문입니다.

기존 HRIS와 급여 계산 시스템 통합의 복잡성

직원 복리후생 기술 시장은 여전히 HRIS와 급여 계산 시스템의 통합이 복잡하다는 점이라는 가장 큰 운영상의 장벽에 직면해 있습니다. Align HCM은 2026년 4월, 복리후생 시스템과 급여 계산 시스템이 연동되지 않은 조직에서는 매월 40시간을 수동으로 데이터를 재입력하는 데 소비하고 있을 가능성이 있으며, 데이터 품질 저하로 인해 생산성 저하 및 오류 시정에 연간 평균 1,290만 달러의 비용이 발생하고 있는 것으로 밝혀졌습니다. 많은 레거시 시스템은 현대의 API 표준이 보급되기 전에 구축되었기 때문에 복리후생 플랫폼은 여전히 배치 파일 전송에 의존하고 있으며, 이로 인해 수급 자격 반영 지연이나 청구 불일치가 발생하고 있습니다. 또한, Align HCM은 2025년 12월 보고서를 통해 프로젝트 실패의 37%가 불명확한 요구사항에서 기인하며, 29%의 기업이 전환 후 심각한 급여 계산 불일치를 경험했다고 밝혔습니다. 고용주들은 제품의 기능 자체뿐만 아니라 도입 결과를 통해 플랫폼의 가치를 판단하는 경우가 많기 때문에 이로 인해 직원 복리후생 기술 시장의 성장세가 둔화되고 있습니다.

부문별 분석

2025년 직원 복리후생 기술 시장 규모 중 소프트웨어가 74.14%를 차지했으며, 이러한 우위는 고용주의 도입 과정에서 가입 절차 엔진, 자격 관리, AI를 활용한 의사결정 지원이 핵심적인 역할을 수행하고 있음을 반영합니다. 고용주들은 서비스 관계를 더욱 심화시키기 전에 여전히 플랫폼 구매를 통해 현대화를 시작하고 있기 때문에 소프트웨어 계층은 계속해서 직원 복리후생 기술 시장의 기반을 이루고 있습니다. 그렇긴 하지만, 서비스 분야는 2031년까지 연평균 성장률(CAGR) 10.06%를 나타낼 것으로 예측되며, 이는 시장 전체를 웃도는 속도입니다. 이는 소프트웨어 도입이 구매 주기를 마무리하는 것이 아니라, 제2 수요 물결을 만들어내고 있음을 보여줍니다. 복리후생 체계가 점점 더 전문화됨에 따라, 도입 지원, 보험사와의 연계, 플랜 수립 및 지속적인 규정 준수 유지 관리를 사내에서 처리하기가 어려워지고 있습니다.

이러한 변화가 중요한 이유는 직원 복리후생 기술 업계 전반에서 제품 및 서비스의 경계가 모호해지기 시작했기 때문입니다. Businessolver사가 2025년 7월 ProView Global의 자산을 인수함에 따라 백엔드 관리 역량이 강화되었으며, AI 기반 도구는 물론, 인적 지원을 원하는 고객의 직접적인 요구 사항도 반영되었습니다. 도입 관리나 일상적인 예외 상황 처리를 벤더에 의뢰하는 고용주가 늘어남에 따라, 서비스는 단순한 부수적인 수익원이 아니라 고객 유지율을 높이는 요인이 되어가고 있습니다. 따라서 직원 복리후생 기술 시장에서는 강력한 핵심 소프트웨어와 신뢰할 수 있는 운영 서비스를 결합할 수 있는 공급업체가 앞으로도 계속해서 높은 평가를 받을 것으로 보입니다.

2025년 기준으로 클라우드 기반 솔루션의 도입 비중은 직원 복리후생 기술 시장의 71.62%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 9.88%로 성장할 것으로 전망됩니다. 클라우드 시스템이 주류를 이루게 된 배경에는 고용주들이 시스템 업그레이드의 신속화, 인프라 부담 경감, 그리고 급여 계산 시스템, 인사 정보 시스템(HRIS), 보험사 시스템 간의 연동 용이화를 요구하고 있기 때문입니다. 직원 복리후생 기술 시장은 단순한 호스팅 변경 단계를 이미 넘어섰으며, 현재 진행 중인 프로젝트에서는 기존 로직을 새로운 서버로 이전하는 대신, API 우선 설계에 기반하여 가입 절차, 자격 심사, 보고서 작성 등 각 계층을 재구축하는 사례가 늘고 있습니다. On-Premise 구축은 여전히 외부 호스팅이 어려운 정부 기관이나 규제가 엄격한 환경에서 그 중요성을 유지하고 있지만, 이 부문은 지속적인 구조적 축소에 직면해 있습니다.

클라우드에 대한 강력한 수요는 측정 가능한 성능 향상에도 기인하고 있습니다. Alight사의 AWS 전환을 통해 가입 절차의 응답 시간이 43% 단축되었으며, 연간 7,500만 달러의 비용 절감을 달성했습니다. 이는 대규모 재투자 없이는 기존의 On-Premise 환경으로는 따라잡기 어려운 벤치마크입니다. 유럽에서는 직원 데이터의 보관 장소에 대한 법적 감독도 도입 방식 선택에 영향을 미치고 있으며, 이로 인해 대규모 고용주들 사이에서는 프라이빗 클라우드나 지역 호스팅 모델이 여전히 중요한 위치를 차지하고 있습니다. 비용, 성능, 법적 관리 등 이러한 요소들이 결합되어, 최종 아키텍처가 완전한 퍼블릭 클라우드가 아니더라도 클라우드는 직원 복리후생 기술 시장의 중심적인 위치를 계속 차지하고 있습니다.

지역별 분석

2025년, 북미는 직원 복리후생 기술 시장 규모의 40.36%를 차지하며 최대 지역 시장이 되었습니다. 이 지역은 ACA, COBRA, ERISA, HIPAA, 그리고 계속 늘어나는 주 차원의 복리후생 의무 등 엄격한 규정 준수 환경의 혜택을 누리고 있습니다. 자가보험을 도입하는 고용주들은 보다 강력한 수급 자격 관리, 비용 추적, 그리고 보험사 및 스톱로스 구조 간의 연계가 필요하기 때문에 미국은 여전히 수요의 핵심 시장으로 남아 있습니다. 캐나다와 멕시코에서도 고용주가 관리 업무의 표준화를 추진하고, 현지 복리후생 의무를 보다 광범위한 인사 시스템과 연계함에 따라 그 역할이 확대되고 있습니다. 이 지역에서는 단순한 디지털화뿐만 아니라 플랫폼의 심도도 중요하게 여겨지기 때문에 북미는 직원 복리후생 기술 시장의 중심지로 자리매김하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 11.92%를 나타낼 것으로 예측되며, 이는 직원 복리후생 기술 시장에서 지역별 가장 높은 성장률입니다. 해당 지역은 각각 다른 경로를 통해 성장하고 있으며, 인도에서는 비용 효율이 높은 국내 인사 기술 솔루션이 선호되고, 동남아시아에서는 모바일 우선 접근 방식이 중시되며, 중국에서는 기업의 커뮤니케이션 생태계와 연계된 현지 플랫폼에 대한 지지가 높아지고 있습니다. 이 지역에서는 많은 고용주들이 복리후생 관리의 디지털화에 아직 여지가 있다고 판단하여, 관련 시스템 도입이 활발히 진행되고 있습니다. 이를 통해 공급업체는 단순한 시스템 교체에 그치지 않고, 접근성, 사용 편의성, 그리고 현지 상황에 최적화된 규정 준수 워크플로를 통해 성장을 도모할 수 있습니다. 한편, 일본과 한국에서는 고용주와 근로자가 복리후생 결정에 있어 여전히 사람의 중재를 중시하고 있기 때문에 도입 속도는 비교적 완만합니다. 그 결과, 지역 전체적으로는 견실한 성장이 나타나고 있지만, 단일한 지역 운영 모델은 존재하지 않습니다.

유럽에서는 국가에 따라 촉진요인이 다르지만, 직원 복리후생 기술 시장 전반에 걸쳐 규정 준수를 중심으로 한 업그레이드 주기가 진행되고 있습니다. EU의 임금 투명성 지침과 규제 당국의 광범위한 감독으로 인해, 고용주들은 미비한 점이 업무상의 문제로 이어지기 전에 보상, 보고 및 복리후생 데이터 시스템을 재검토해야 하는 상황에 직면해 있습니다. SD Worx는 2026년 4월, 독일, 룩셈부르크, 스페인, 스웨덴, 네덜란드에서 이루어지는 법 개정을 추적하는 “Legal Watch"를 개설했습니다. 이는 공급업체가 규제와 관련된 정보를 핵심 제품 기능으로 전환하고 있음을 보여줍니다. 유럽 이외의 지역에서는 남미, 중동 및 아프리카가 여전히 초기 단계 시장이며, 사업 단위 전체에 걸친 관리의 표준화를 추구하는 대규모 다국적 기업들이 도입을 주도하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the employee benefits technology market size was valued at USD 3.46 billion in 2025 and is expected to reach USD 3.76 billion in 2026 and USD 5.98 billion by 2031, growing at a CAGR of 9.72% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Deployment Model (Cloud-Based, and On-Premises), Organization Size (Large Enterprises, and SMEs), Functionality (Enrollment and Eligibility Management, Core Benefits Administration, and More), End-User Industry (BFSI, IT and Telecommunications, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Employee Benefits Technology Market Trends and Insights

Rising Benefits Complexity And Compliance Automation Demand

The employee benefits technology market is gaining support from the rising complexity of benefit rules across national and sub-national jurisdictions. In the United States, the ACA Employer Shared Responsibility Penalty B stood at USD 4,350 per employee for non-compliant coverage offerings in 2026, which keeps compliance exposure high for employers that still rely on manual tracking. Employers also have to manage a wider compliance stack that includes ACA reporting, leave tracking, COBRA administration, ERISA processes, and HIPAA-linked data handling, which increases the value of unified automation tools. AI-enabled compliance engines are increasingly being used to automate ACA 1095-C generation, FMLA eligibility tracking, and live penalty-risk monitoring, and documented deployments have reduced manual monitoring time by 70-80%. That shift is helping the employee benefits technology market move from a back-office software category toward a control layer for employer risk management.

Cloud Migration Across HR And Benefits Stacks

The employee benefits technology market is also being lifted by cloud migration across HR and benefits systems as employers replace fragmented tools with unified platforms. Alight Solutions completed its AWS migration in February 2025, and the move resulted in USD 75 million in annual savings, a 40% reduction in server footprint, and 43% faster enrollment response times. These results matter because cloud migration is no longer limited to infrastructure cost savings, and it now pushes employers to clean up carrier links, eligibility rules, and data definitions that had been sustained through manual reconciliation. That cleanup phase often increases service demand for implementation, integration, and ongoing plan configuration, which supports a larger services opportunity inside the employee benefits technology market. Hybrid deployment models are also becoming more relevant in regulated settings where employers want cloud economics but still need local data handling and tighter legal oversight of HR information flows.

Legacy HRIS And Payroll Integration Complexity

The employee benefits technology market still faces its largest operational barrier in HRIS and payroll integration complexity. Align HCM stated in April 2026 that organizations with disconnected benefits and payroll systems can spend 40 hours per month on manual data re-entry, and poor data quality has been shown to cost organizations an average of USD 12.9 million annually in productivity loss and error remediation. Many legacy systems were built before modern API standards became common, so benefits platforms still depend on batch file transfers that create eligibility lags and billing mismatches. Align HCM also reported in December 2025 that 37% of project failures were tied to unclear requirements, and 29% of firms experienced critical payroll discrepancies after migration. This is slowing the employee benefits technology market because employers often judge the value of a platform through implementation outcomes rather than through product features alone.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand For Employee Self-service And Personalized Guidance

- Small And Medium Enterprise Adoption Through SaaS Pricing

- Data Privacy And Cybersecurity Exposure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 74.14% of the employee benefits technology market size in 2025, and this lead reflected the central role of enrollment engines, eligibility management, and AI-guided decision support in employer deployments. The software layer remains the foundation of the employee benefits technology market because employers still begin modernization through a platform purchase before they expand into deeper service relationships. That said, services is projected to grow at a 10.06% CAGR through 2031, which is faster than the overall market and shows that software adoption is creating a second demand wave rather than closing the buying cycle. Implementation support, carrier connectivity, plan configuration, and ongoing compliance maintenance are becoming harder to manage internally as benefit structures become more specialized.

This shift matters because the boundary between product and service is starting to blur across the employee benefits technology industry. Businessolver's July 2025 acquisition of ProView Global assets added back-end administration capacity and reflected direct client demand for human support alongside AI-driven tools. As more employers ask vendors to manage implementation and daily exceptions, services is becoming a source of stickiness rather than a peripheral revenue stream. This is why the employee benefits technology market is likely to keep rewarding vendors that can combine strong core software with reliable operational delivery.

Cloud-based deployment held 71.62% of the employee benefits technology market share in 2025, and it is forecast to grow at a 9.88% CAGR through 2031. Cloud systems are leading because employers want faster upgrades, lower infrastructure burden, and easier connectivity across payroll, HRIS, and carrier systems. The employee benefits technology market has moved beyond simple hosting changes, and current projects increasingly rebuild enrollment, eligibility, and reporting layers around API-first designs instead of moving old logic into new servers. On-premises deployments still hold relevance in government and heavily regulated settings where external hosting remains difficult, but this segment faces ongoing structural compression.

The stronger pull toward the cloud also comes from measurable performance gains. Alight's AWS migration delivered 43% faster enrollment response times and USD 75 million in annual savings, which set a benchmark that traditional on-premises environments struggle to match without major reinvestment. In Europe, deployment choice is also shaped by legal scrutiny of where employee data resides, which is helping private-cloud and regional-hosting models stay relevant for larger employers. That mix of cost, performance, and legal control keeps the cloud at the center of the employee benefits technology market even when the final architecture is not fully public cloud.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Model

- Cloud-based

- On-premises

- By Organization Size

- Large Enterprises

- SMEs

- By Functionality

- Enrollment and Eligibility Management

- Core Benefits Administration

- Employee Self-service and Decision Support

- Compliance and Audit Management

- Analytics and Reporting

- Other Functionalities

- By End-user Industry

- BFSI

- IT and Telecommunications

- Healthcare and Lifesciences

- Retail and E-commerce

- Industrial Manufacturing

- Government and Public Sector

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 40.36% of the employee benefits technology market size in 2025, which made it the largest regional market. The region benefits from a dense compliance environment that includes ACA, COBRA, ERISA, HIPAA, and a growing list of state benefit mandates. The United States remains the core demand center because self-insured employers need stronger eligibility management, cost tracking, and coordination across carriers and stop-loss structures. Canada and Mexico are also expanding their role as employers standardize administration and connecting local benefit obligations to broader HR systems. This keeps North America central to the employee benefits technology market because platform depth matters more here than basic digitization alone.

Asia-Pacific is forecast to grow at an 11.92% CAGR through 2031, which is the fastest regional rate in the employee benefits technology market. The region is expanding through different paths, with India favoring cost-efficient domestic HR technology, Southeast Asia leaning toward mobile-first access, and China showing stronger traction for local platforms tied to enterprise communication ecosystems. Adoption is rising because many employers in the region still have room to digitize benefits administration, enabling vendors to grow through access, usability, and localized compliance workflows rather than through replacement alone. At the same time, Japan and South Korea show a more measured pace because employers and employees still place a higher value on human intermediation in benefits decisions. The result is strong regional growth, but not a single regional operating model.

Europe is seeing a compliance-led upgrade cycle across the employee benefits technology market, even though the drivers differ by country. The EU Pay Transparency Directive and wider regulatory scrutiny are pushing employers to revisit compensation, reporting, and benefit data systems before gaps become operational problems. SD Worx launched Legal Watch in April 2026 to track legal changes across Germany, Luxembourg, Spain, Sweden, and the Netherlands, which shows how vendors are turning regulatory intelligence into a core product feature. Outside Europe, South America, the Middle East, and Africa remain earlier-stage opportunities where adoption is led mainly by large multinational employers that want standardized administration across operating units.

- Aptia Group Limited

- Benefex Limited

- bswift LLC

- Benefitfocus.com, Inc.

- Businessolver.com Inc.

- PlanSource Benefits Administration, Inc.

- Employee Navigator LLC

- Selerix Systems, Inc.

- HealthJoy, LLC

- The Jellyvision Lab, Inc.

- Nayya Health, Inc.

- ThrivePass, Inc.

- Forma Inc.

- Benepass, Inc.

- PeopleKeep, Inc.

- Benefitfirst

- Alegeus Technologies, LLC

- Reward Gateway (UK) Limited

- Universal Cover, SA

- Thanks Ben LTD

- Compt Inc.

- Level Benefits, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Benefits Complexity and Compliance Automation Demand

- 4.2.2 Cloud Migration Across HR and Benefits Stacks

- 4.2.3 Growing Demand for Employee Self-service and Personalized Guidance

- 4.2.4 Small and Medium Enterprise Adoption Through SaaS Pricing

- 4.2.5 Embedded Benefits APIs Inside Payroll and HCM Ecosystems

- 4.2.6 Expansion of Wallet-based and Lifestyle Benefit Programs

- 4.3 Market Restraints

- 4.3.1 Legacy HRIS and Payroll Integration Complexity

- 4.3.2 Data Privacy and Cybersecurity Exposure

- 4.3.3 Multi-country Carrier Data Fragmentation

- 4.3.4 Shortage of Benefits Configuration and Implementation Talent

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 Cloud-based

- 5.2.2 On-premises

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 SMEs

- 5.4 By Functionality

- 5.4.1 Enrollment and Eligibility Management

- 5.4.2 Core Benefits Administration

- 5.4.3 Employee Self-service and Decision Support

- 5.4.4 Compliance and Audit Management

- 5.4.5 Analytics and Reporting

- 5.4.6 Other Functionalities

- 5.5 By End-user Industry

- 5.5.1 BFSI

- 5.5.2 IT and Telecommunications

- 5.5.3 Healthcare and Lifesciences

- 5.5.4 Retail and E-commerce

- 5.5.5 Industrial Manufacturing

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Nigeria

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Aptia Group Limited

- 6.4.2 Benefex Limited

- 6.4.3 bswift LLC

- 6.4.4 Benefitfocus.com, Inc.

- 6.4.5 Businessolver.com Inc.

- 6.4.6 PlanSource Benefits Administration, Inc.

- 6.4.7 Employee Navigator LLC

- 6.4.8 Selerix Systems, Inc.

- 6.4.9 HealthJoy, LLC

- 6.4.10 The Jellyvision Lab, Inc.

- 6.4.11 Nayya Health, Inc.

- 6.4.12 ThrivePass, Inc.

- 6.4.13 Forma Inc.

- 6.4.14 Benepass, Inc.

- 6.4.15 PeopleKeep, Inc.

- 6.4.16 Benefitfirst

- 6.4.17 Alegeus Technologies, LLC

- 6.4.18 Reward Gateway (UK) Limited

- 6.4.19 Universal Cover, SA

- 6.4.20 Thanks Ben LTD

- 6.4.21 Compt Inc.

- 6.4.22 Level Benefits, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment