|

시장보고서

상품코드

2073337

목재 플라스틱 복합 바닥재 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Wood Plastic Composite Flooring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

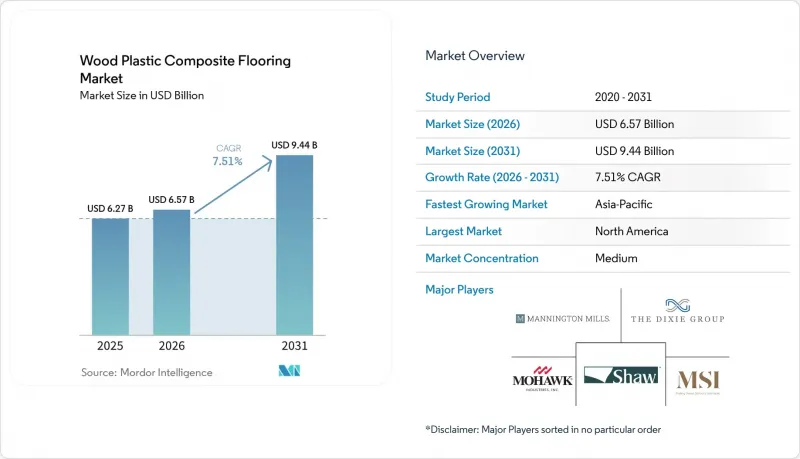

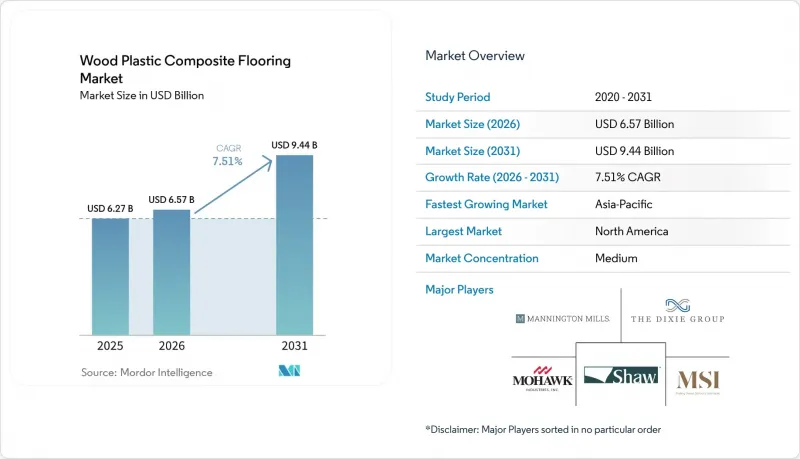

Mordor Intelligence에 의하면, 목재 플라스틱 복합 바닥재 시장 규모는 2025년 62억 7,000만 달러로 평가되었습니다. 2026년에는 65억 7,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 7.51%로 성장을 지속하여, 2031년에는 94억 4,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(폴리에틸렌, PVC, 폴리프로필렌, 기타), 두께(3.5-4 mm, 5-6 mm, 6.5-8 mm, 8 mm 이상), 시공 방법(클릭 잠금, 접착 시공, 기타), 최종 사용자, 유통 채널(B2C, B2B), 지역(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 목재 플라스틱 복합 바닥재 시장 동향 및 인사이트

DIY에 적합한 클릭 잠금 방식의 경질 비닐 바닥재가 주택 리모델링을 가속화하고 있습니다.

클릭 잠금 구조는 시공 기간 단축, 시공 교육 간소화, 거주 중인 주택에서의 수리 위험 감소로 이어지기 때문에 목재 플라스틱 복합 마루 시장에서 가치 제안을 위한 핵심 요소로 자리 잡고 있습니다. 각 대형 브랜드 업체들은 프로파일의 형상과 모서리의 안정성을 지속적으로 개선하여 시공 시간을 단축하는 한편, 마감된 바닥면의 평탄성을 일정하게 유지함으로써, 까다로운 리모델링 공사 기간 내 일정 관리를 용이하게 하고 있습니다. 소매 현장에서는 락 시스템에 어울리는 트림과 기초 키트를 세트로 구성한 컬렉션을 통해, 주택 소유자와 전문가들이 샘플 선택부터 완성까지 의사결정 단계를 최소화하며 진행할 수 있도록 지원하고 있으며, 이는 계약 성사율과 만족도 향상으로 이어지고 있습니다. ‘단일 가격’이라는 간단한 방식을 통해 설치 준비가 완료된 시스템을 제공하는 제조업체는 최근의 제품 주기에서 높은 평가를 받고 있으며, 이는 시공의 확실성이 리모델링 시 중요한 구매 동기가 됨을 보여줍니다. 또한, 짧은 리드타임과 지역별 재고를 보장하는 유통 프로그램 역시 DIY 및 전문가에 의한 리모델링을 지원하고 있습니다. 이를 통해 시공사는 자신 있게 납기를 약속할 수 있으며, 해외 운송으로 인한 지연을 피할 수 있기 때문입니다.

다층 주택의 방수 및 방음 성능의 장점

다층 주택 프로젝트에서는 소리의 전달을 억제하고 발밑에 따뜻한 감촉을 주는 제품이 선호됩니다. 그 때문에 침실, 로프트, 메자닌에서 WPC에 대한 수요가 계속되고 있습니다. 두께감이 있는 코어와 특수 가공된 패드를 조합한 이 컬렉션은 균형 잡힌 구조 덕분에 바닥의 요철을 보정하는 동시에 발소리 특성도 개선합니다. 이는 개축이나 지하실 공사에서 중요한 요소가 됩니다. 프리미엄 WPC 시리즈는 내마모성이 뛰어난 표면과 발포재를 일체화함으로써 쾌적성과 내흠집성을 동시에 확보하여, 거주자들이 조용한 바닥을 중요시하는 가족실이나 미디어룸 등으로의 적용 범위를 넓히고 있습니다. 상업시설이나 복합 용도 건물에서도 특정 구역에는 동일한 기준이 적용됩니다. 특히, 최대 정하중 내구성보다 부드러운 밟는 느낌이나 유지보수가 간편한 청결성이 중시되는 장소에서는 WPC가 계속해서 사양 후보로 선정되고 있습니다. 내습성은 물론 단열 성능과 방음 성능을 강조한 제품 데이터 시트는 음향적 쾌적성이 중요한 프로젝트에서 목재 플라스틱 복합 바닥재 시장 내 명확한 포지셔닝을 뒷받침하고 있습니다.

SPC의 저렴한 가격과 뛰어난 내충격성이 WPC 시장 점유율을 빼앗을 전망입니다.

구름 하중이나 쌓인 가구로 인한 찌그러짐 저항성을 우선시하는 프로젝트에서는 광물 코어가 적용된 경질 제품이나 상업용 등급의 LVT가 지정되는 경우가 많으며, 이로 인해 복도나 카페테리아에서 WPC와의 경쟁이 발생하고 있습니다. 의료 및 교육 분야의 시설 관리자들은 장기간 사용에도 외관을 유지할 수 있는 경질 바닥재의 보증 및 표면 경도 솔루션을 원하고 있으며, 그 결과 일반적으로 검증된 리지드 LVT 제품군으로 선택의 폭이 좁혀집니다. 총 예산이 고정된 저가형 주택 프로젝트의 경우, 구매자들은 입주 일정을 맞추기 위해 당장의 쾌적성을 희생하면서 자재비를 절감하거나 정하중 정격을 높이는 경우가 적지 않습니다. 이러한 추세로 인해, 쾌적성 및 충격음 제어 측면에서 강점을 가지고 있음에도 불구하고, 특정 하위 부문에서는 WPC의 채택이 주춤할 가능성이 있습니다. 제품 라인이 진화하는 가운데, 거주자들이 아늑함과 소음 저감을 중요시하는 공간에서는 WPC가 여전히 시장 점유율을 유지하고 있습니다. 한편, 유동 인구가 많은 지역에서는 경질 LVT나 광물 코어 소재를 사용한 제품이 여전히 일반적이며, 이로 인해 목재 플라스틱 복합 바닥재 시장에서는 이용 사례에 따른 실용적인 양분된 양상이 유지되고 있습니다.

부문별 분석

2025년에는 폴리에틸렌계 WPC가 제품 구성의 40%를 차지하며 1위를 차지했으나, 폴리프로필렌은 2031년까지 연평균 성장률(CAGR) 8.15%를 나타낼 것으로 예측됩니다. 2031년까지의 범용 폴리머 중에서는 이 두 제품이 목재 플라스틱 복합 바닥재 시장의 엔트리, 미들, 프리미엄 각 가격대를 아우르는 가격 체계의 핵심으로 자리 잡고 있습니다. 실제로 폴리에틸렌 계열 제품은 밀도와 탄력성의 균형이 잘 잡혀 있어 선택되고 있습니다. 이를 통해 쾌적한 발소리 성능이 실현되어, 2층 방이나 거주자들의 보행 빈도가 제각각인 주거 지역에 적합합니다. 계절적 변동에 따른 치수 안정성을 중시한 제품 라인은 틈새나 가장자리의 들뜸으로 인한 재시공을 피하고자 하는 시공업체들로부터 지지를 받고 있으며, 이는 폴리에틸렌계 제품 시장 점유율 유지에 기여하고 있습니다. 폴리프로필렌은 특히 햇볕이 잘 드는 방이나 온난한 지역 등 더 높은 열변형 온도가 요구되는 상황에서 주목을 받고 있으며, 이러한 특성 덕분에 새로운 적용 분야를 개척하며 전반적인 목표 시장을 확대되고 있습니다. 고성능 코어와 내구성이 뛰어난 마모층을 결합한 이 브랜드는 이러한 컬렉션을 압흔 저항성이 가장 뛰어난 제품보다는 부드러운 촉감을 선호하는 주택 소유자를 타겟으로 삼고 있으며, 두 폴리머에 걸쳐 제품 포트폴리오의 일관성을 유지하고 있습니다.

이러한 규제 환경은 제조업체들이 복합 코어 기반 탄성 바닥재에 대한 가소제 선택지 및 인증 목표를 평가하는 과정에서 재료 선정의 추세를 뒷받침하고 있습니다. 각사의 공개 정보에 따르면, 브랜드 소유주들이 관련 제품군 전반에 걸쳐 저탄소형 탄성 바닥재를 구현할 방안을 모색하는 가운데, 재활용 소재의 함유율 및 대체 전략 측면에서 꾸준한 진전이 나타나고 있습니다. 목재 플라스틱 복합 마루 시장에서도 제품 매니저는 명확한 이용 사례 스토리를 바탕으로 방의 용도나 통행량에 따른 제품 선택을 유도할 수 있도록 제품 라인업을 구성함으로써, 보증 청구로 이어질 수 있는 잘못된 사용을 억제하고 있습니다. 제품 라인업에서 마모층의 내구성과 코어층의 안정성, 그리고 패드의 통합이 조화를 이룰 경우, 이러한 조합은 사용자의 기대와 실제 성능을 일치시켜 소매업체의 재구매 촉진 및 NPS 점수 상승으로 이어집니다. 이러한 폴리머의 포지셔닝, 인증의 일관성, 그리고 방별 사양 설정이라는 패턴은 가격대가 겹치는 광물 코어 제품이라는 대체품에 맞서 브랜드가 시장 점유율을 지켜내는 방식을 계속해서 결정짓고 있습니다.

2025년에는 5-6mm 두께 대가 시장 점유율의 56.72%를 차지했습니다. 이는 비용을 중시하는 프로젝트에서 구매자가 총 설치 비용을 예산 범위 내로 맞추면서도, 찌그러짐 저항성과 쾌적성에 대한 기대를 충족시키는 대안을 선택했기 때문입니다. 또한, 이 두께 범위는 단기간에 완료할 수 있는 리모델링에 적합하기 때문에 목재 플라스틱 복합 마루 시장에서 계속해서 중요한 위치를 차지하고 있습니다. 이 두께의 제품 라인에는 일반적으로 패드가 일체형으로 되어 있으며, 클릭 프로파일도 통일되어 있어 사전 준비 작업을 최소화하고 방별로 효율적인 시공이 가능합니다. 또한, 이 규격은 중형 주택에 널리 설치된 문턱 및 트림과도 호환되므로, 목공 공사의 변경을 최소화하고 시공 업체가 하루에 더 많은 방을 마감할 수 있도록 지원합니다. 두께별로 색상 구성과 질감이 통일된 제품 라인업을 통해 소매업체는 고객이 선호하는 외관을 유지한 채 더 상위 제품으로의 업그레이드를 제안할 수 있는 유연성을 확보하게 되며, 이를 통해 상품 구성 관리가 강화됩니다. 이러한 특징들이 결합되어, 예측 가능한 비용과 신뢰할 수 있는 성능을 추구하는 건설업체 및 부동산 관리자들에게 5-6mm 두께의 제품이 여전히 핵심적인 위치를 차지하고 있습니다.

6.5-8mm 카테고리는 더 높은 쾌적성과 정숙성을 추구하는 주택 소유자, 그리고 셀프 레벨링이 필요 없고 하층면의 미세한 요철을 허용하는 패드 일체형 구조를 중시하는 전문가들의 지지를 받아, 2031년까지 연평균 8.31%의 성장이 예상됩니다. 이 범주의 프리미엄 라인은 가족이 많은 시간을 보내는 공간에서 가격 인상을 정당화할 수 있도록, 더 두꺼운 코어, 고성능 마모층, 그리고 더욱 인상적인 외관을 특징으로 합니다. 구조와 내마모 성능을 상세하게 설명한 제품 페이지는 시공업체와 고객 모두가 열적 쾌적성과 흡음성이 중요한 거실, 홈 오피스, 서재 등에 해당 SKU를 적절히 배치하는 데 도움이 됩니다. 이러한 경향은 개인 사무실이나 회의실과 같은 소규모 상업시설에서도 마찬가지이며, 이러한 공간에서는 최대 하중보다 부드러운 발 밑 감촉과 고급스러운 외관이 더 중요하게 여겨집니다. 이 성장 전략은 엔트리 레벨 제품보다 두께가 6.5-8mm 더 두꺼운 제품을 포지셔닝하면서도, 비용과 시공 복잡성 면에서는 하드우드 마루보다 낮은 수준을 유지한다는 제품 포트폴리오 논리에 기반을 두고 있습니다.

지역별 분석

2025년에는 북미가 전체 시장의 33%를 차지했습니다. 이는 리모델링이나 바닥재 교체에 따른 견조한 수요가, 따뜻함과 방음성이 중시되는 침실이나 거실 공간에서 WPC의 꾸준한 도입을 뒷받침했기 때문입니다. 의료 및 교육 분야의 시설 소유주들은 여전히 구역별로 사양을 달리하고 있으며, 특정 구역에는 부드러운 촉감의 제품을 채택하는 한편, 하중이 큰 장소에서는 경질 LVT나 광물 코어 소재의 솔루션을 사용하고 있습니다. 강제 노동 위험과 관련된 무역 규제 역시 조달 동향에 영향을 미치고 있어, 수입업체들은 화물의 압류나 지연을 피하기 위해 원산지 전략과 서류 작성 관행을 조정해야 하는 상황에 놓여 있습니다. 관련 탄성 바닥재 제품군에 대한 국내 및 근해 지역 투자는 해당 카테고리 전체의 리드타임 안정성을 높이고, 가동률이 높은 시설의 일정 관리를 개선하고 있습니다. WPC 바닥재 시장 전반에서 각 브랜드가 제품 교육과 규정 준수 조치를 조화롭게 추진해 나가는 가운데, 제품 포트폴리오의 다양성과 명확한 시공 지침은 소매 시장에서 여전히 차별화의 핵심 요소로 자리 잡고 있습니다.

아시아태평양은 도시화, 중가 주택 시장의 확대, 그리고 유통 인프라의 지속적인 개선을 반영하여 2031년까지 8.60%라는 이 지역에서 가장 높은 성장률을 나타낼 것으로 전망됩니다. 각 제조업체들은 회복탄력성을 높이고 주요 수출처로의 운송 시간을 단축하기 위해 지역 전체에서 생산 능력의 다각화를 추진하고 있으며, 이를 통해 지정학적 위험과 정책적 위험을 완화하고 있습니다. 지역별 공급망에서는 규제 대상 시장에 대한 접근성을 유지하기 위해 자재 문서화 및 저배출 마감 처리가 점점 더 중요시되고 있으며, 이러한 노력은 보다 원활한 통관 절차와 고객 신뢰도 향상에 기여하고 있습니다. 코어 층의 두께나 패드 포함이 보편화된 것은 인구 밀도가 높은 주거 환경에서 쾌적성과 소음 대책이라는 구매자의 우선 순위에 부합하기 때문입니다. 주요 도시에서 온라인 및 오프라인 판매 채널이 성숙해짐에 따라, 인기 있는 인테리어 스타일에 부합하고 확실한 납기를 보장하는 상품 라인업이 지역 전체의 탄성 바닥재 계약 성사율 향상으로 이어지고 있습니다.

유럽에서는 주택 재고의 장기적인 현대화와 저배출 제품 및 더 안전한 표면 화학 물질을 우선시하는 규제 체계에 힘입어 여전히 큰 시장 점유율을 유지하고 있습니다. 이러한 요소들은 탄성 바닥재의 사양 기준에 영향을 미치고 있습니다. 2층의 방이나 특정 상업시설에서 WPC의 매력은 여전히 높은 반면, 특정 화학 물질 군에 대한 규제가 강화됨에 따라 마감재와 접착제의 배합 재검토가 진행되고 있습니다. 해당 지역에서 제품을 판매하는 브랜드들은 원자재 선정 과정을 보다 엄격하게 문서화하고, 제3자 기관의 시험 결과를 활용함으로써 기관 투자자를 대상으로 한 규정 준수 절차를 효율화하고 있습니다. 성능, 인증 및 디자인 다양성을 중시한 제품 라인업은 전문 소매점 및 건설업체 대상 유통 채널에서 진열 공간을 확보하는 데 유리한 입장에 있습니다. 규제 해석과 제품 표기의 일관성은 목재 플라스틱 복합 바닥재 시장에서 예측 가능한 계획을 뒷받침하고 있으며, 이는 국경을 초월한 사업 전개에 있어 중요한 요소가 됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the wood plastic composite flooring market size is expected to grow from USD 6.27 billion in 2025 to USD 6.57 billion in 2026 and is forecast to reach USD 9.44 billion by 2031 at 7.51% CAGR over 2026-2031.

This report is Segmented by Product Type (Polyethylene, PVC, Polypropylene, Others), Thickness (3. 5-4 Mm, 5-6 Mm, 6. 5-8 Mm, Above 8 Mm), Installation Method (Click-Lock, Glue-Down, Others), End User, Distribution Channel (B2C, B2B), and Geography (North America, South America, Europe, Asia-Pacific, Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Wood Plastic Composite Flooring Market Trends and Insights

DIY-Friendly Click-Lock Rigid Vinyl Accelerates Residential Remodels

Click-lock construction remains central to the value proposition in the wood plastic composite flooring market because it reduces job duration, simplifies training, and lowers rework risk in occupied homes. Large brands continue to refine profile geometry and edge stability to support faster installs with consistent finished-floor flatness, which eases scheduling in tight remodel windows. At retail, collections that package locking systems with matched trims and underlayment kits help homeowners and pros move from sample to completion with fewer decision points, which benefits conversion and satisfaction. Manufacturers that offer installation-ready systems with one-price simplicity have seen strong reception in recent product cycles, indicating that execution certainty is a critical purchase driver for remodels. Distribution programs that guarantee short lead times and regional stock also support DIY and pro remodels, as contractors can commit to dates with confidence and avoid delays tied to transoceanic shipments.

Waterproof and Acoustic Comfort Advantages in Multi-Level Housing

Multi-level housing projects favor products that control sound transmission and deliver a warmer underfoot experience, which sustains demand for WPC in bedrooms, lofts, and mezzanines. Collections that integrate thicker cores with engineered pads offer a balanced footprint that helps manage subfloor variation while improving step-sound characteristics, which matters in conversions and basements. Premium WPC lines also bundle high-wear surfaces with attached foam to deliver comfort and scratch resistance, which broadens their use into family rooms and media rooms where occupants prioritize quiet floors. Commercial and mixed-use properties apply similar criteria for select zones, especially where a softer feel and low-maintenance cleaning profile are preferred over maximum static load resistance, which keeps WPC in the specification mix. Product data sheets that highlight thermal and acoustic performance, alongside moisture tolerance, support clear positioning in the wood-plastic composite flooring market for projects where acoustic comfort is critical.

SPC's Lower Cost and Higher Dent Resistance Cannibalize WPC

Projects that prioritize dent resistance under rolling loads and stacked furniture often specify mineral-core rigid products or commercial-grade LVT, which creates competition for WPC in corridors and cafeterias. Facility managers in healthcare and education seek hard-surface warranties and surface-hardness solutions that maintain appearance over long service intervals, which typically narrow the field to rigid LVT families with proven track records. In entry-price residential projects where the total budget is fixed, buyers often trade underfoot comfort for lower material cost and higher static-load ratings to satisfy move-in schedules. That dynamic can slow WPC adoption in specific sub-segments, despite its strengths in comfort and impact sound control. As product lines evolve, WPC continues to retain share in rooms where dwellers prioritize warmth and noise control. At the same time, rigid LVT and mineral-core options remain common in heavy-traffic zones, which sustains a pragmatic split of use cases in the wood plastic composite flooring market.

Other drivers and restraints analyzed in the detailed report include:

- Premium WPC Rebound Amid Quality Issues in Entry-Level SPC Tiers

- Omnichannel Discovery and Visualization Improve Conversion

- Tightening PVC Chemical Policies and Trade Barriers Raise Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyethylene-based WPC led the product mix with 40% in 2025, while polypropylene is projected to grow at an 8.15% CAGR to 2031. Among commodity polymers through 2031, positioning both as anchors for pricing ladders that cover entry, mid, and premium tiers in the wood plastic composite flooring market. In practice, polyethylene variants are selected for their balanced density and resilience, which support comfortable step-sound performance and make them a fit for upstairs rooms and mixed-traffic residential zones. Product lines that emphasize dimensional stability across seasonal swings gain favor with installers who want to avoid callbacks related to gapping and edge telegraphing, which helps polyethylene families maintain mindshare. Polypropylene draws attention where higher heat-deflection tolerance is desired, particularly in sun-exposed rooms or warmer geographies, and that characteristic opens new placements, widening the overall addressable set. Brands that blend higher-spec cores with durable wear layers direct these collections toward homeowners who prefer a softer feel over maximum indentation resistance, keeping the portfolio logic consistent across both polymers.

The regulatory context reinforces material selection patterns as manufacturers evaluate plasticizer choices and certification targets for resilient surfaces above composite cores. Company disclosures suggest steady progress on recycled content and substitution strategies as brand owners seek routes to lower-carbon resilience across adjacent product families. In the wood-plastic composite flooring market, product managers are also shaping assortments so that clear use-case narratives guide selection by room and traffic level, limiting misapplications that can trigger warranty events. Where portfolios connect wear-layer durability to core stability and pad integration, the combination aligns user expectations with delivered performance, which supports repeat business and higher NPS scores for retailers. This pattern of polymer positioning, certification alignment, and room-by-room specification continues to define how brands defend share against mineral-core alternatives in overlapping price bands.

The 5-6mm band accounted for 56.72% in 2025, as buyers in cost-sensitive projects selected options that meet indentation and comfort expectations without pushing total installed cost above budget, and the tier's fit with quick-turn remodels keeps it prominent in the wood-plastic composite flooring market. Lines at this thickness typically integrate attached pads and consistent click profiles, which minimize prep and enable efficient room-by-room installs. The format also aligns with a large installed base of thresholds and trims in mid-market homes, limiting carpentry changes and helping installers finish more rooms per day. Portfolios that match colorways and textures across thicknesses give retailers flexibility to step customers up without changing the visual they fell in love with, which strengthens mix management. These features combine to keep the 5-6mm category central for builders and property managers who require predictable cost and reliable performance.

The 6.5-8mm tier is projected to grow at 8.31% through 2031, supported by homeowners who want more comfort and a quieter floor, and by pros who value pad integration that tolerates small subfloor variances without self-leveling. Premium lines in this range highlight thicker cores, higher-spec wear layers, and stronger visuals to justify a step-up ticket for rooms where families spend more time. Product pages that detail construction and wear performance help both installers and customers place these SKUs correctly in living rooms, home offices, and dens where thermal comfort and sound absorption are valued. The narrative also holds in light-commercial pockets, such as private offices and conference rooms, where a softer step and a premium look win out over maximum load capacity. This growth thesis is sustained by a portfolio logic that slots 6.5-8mm above entry tiers while staying under hardwood in cost and complexity.

Complete Report Scope:

- By Product Type

- Polyethylene

- High-Density Polyethylene (HDPE)

- Low-Density Polyethylene (LDPE)

- Polyvinylchloride

- Rigid PVC

- Flexible PVC

- Polypropylene

- Homopolymer Polypropylene

- Copolymer Polypropylene

- Other Product Types

- Polyethylene

- By Thickness

- 3.5-4 mm

- 5-6 mm

- 6.5-8 mm

- Above 8 mm

- By Installation Method

- Joist-and-Clip System

- Glue-Down

- Interlocking/Click-lock

- Others

- By End User

- Residential

- Commercial

- By Distribution Channel

- B2C / Retail Consumers

- Home Centers

- Specialty Flooring Stores

- Online

- Local Hardware Shops (unorganized market)

- Other Distribution Channels

- B2B / Contractors / Builders

- B2C / Retail Consumers

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South-East Asia

- Rest of Asia-Pacific

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Geography Analysis

North America accounted for 33% in 2025 as resilient demand from remodeling and replacement sustained steady placements for WPC in bedrooms and living spaces where warmth and sound control matter. Owners in healthcare and education continue to split specifications by zone, reserving softer-feel formats for select areas while using rigid LVT or mineral-core solutions under heavier loads. Trade enforcement related to forced-labor risk has also shaped procurement, prompting importers to adjust origin strategies and documentation practices to avoid detentions and delays. Domestic and nearshore investments in adjacent resilient families strengthen lead-time assurance across the broader category, which improves scheduling for high-utilization facilities. Portfolio variety and clear installation guidance remain points of differentiation in retail, as brands work to align product education with compliance readiness across the wood plastic composite flooring market.

Asia-Pacific is projected to post the fastest regional growth at 8.60% through 2031, reflecting urbanization, mid-market housing expansion, and ongoing improvements in channel infrastructure. Manufacturers continue to diversify capacity across the region to improve resilience and shorten transit times to key export destinations, which mitigates geopolitical and policy risk. Regional supply chains increasingly emphasize materials documentation and low-emission finishes to maintain access to regulated markets, and these efforts support smoother customs clearance and customer confidence. Growing adoption of thicker cores and attached pads aligns with buyer priorities for comfort and noise control in higher-density living. As online and offline channels mature in key cities, assortments that match popular interior styles and provide reliable delivery windows lift conversion for resilient floors across the region.

Europe maintains a substantial share driven by long-term modernization of housing stock and regulatory frameworks that prioritize low-emission products and safer surface chemistries, which influence specification criteria for resilient flooring. WPC's appeal in upstairs rooms and select commercial settings remains consistent, while stricter rules around certain chemical classes are steering reformulation in finishes and adhesives. Brands selling into the region are documenting materials choices with greater rigor and leaning on third-party testing to streamline compliance for institutional buyers. Portfolios that emphasize performance, certification, and aesthetic range are well placed to hold shelf space in specialty retail and builder channels. Consistency in regulatory interpretation and product labeling supports predictable planning in the wood plastic composite flooring market, which is valuable for cross-border programs.

- Shaw Industries (incl. Shaw Floors)

- COREtec Floors (USFloors/Shaw)

- Mannington Mills

- Mohawk Industries

- The Dixie Group (TRUCOR)

- Johnson Hardwood

- Lions Floor

- Southwind Floors

- MSI Surfaces

- AHF Products (Robbins)

- Metroflor (HMTX Industries)

- Karndean Designflooring

- Novalis Innovative Flooring

- Tarkett

- Karastan

- CFL Flooring

- Taizhou Huali New Materials

- Decno Group

- Provenza Floors

- Biyork

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 DIY-friendly click-lock rigid vinyl accelerates residential remodels

- 4.2.2 Waterproof and acoustic comfort advantages in multi-level housing

- 4.2.3 Premium WPC rebound amid quality issues in entry-level SPC tiers

- 4.2.4 Omnichannel discovery and visualization improve conversion

- 4.2.5 Insurance-driven water-loss replacements favor waterproof rigid floors

- 4.2.6 Extra-thick WPC (10-12 mm; up to 19 mm) as hardwood substitute without trim changes

- 4.3 Market Restraints

- 4.3.1 SPC's lower cost and higher dent resistance cannibalize WPC

- 4.3.2 Tightening PVC chemical policies and trade barriers raise compliance costs

- 4.3.3 Import-reliant WPC faces UFLPA and logistics disruptions

- 4.3.4 Commercial specs de-prioritize WPC for rolling loads in healthcare/education

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Industry

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts (Value in USD Billion)

- 5.1 By Product Type

- 5.1.1 Polyethylene

- 5.1.1.1 High-Density Polyethylene (HDPE)

- 5.1.1.2 Low-Density Polyethylene (LDPE)

- 5.1.2 Polyvinylchloride

- 5.1.2.1 Rigid PVC

- 5.1.2.2 Flexible PVC

- 5.1.3 Polypropylene

- 5.1.3.1 Homopolymer Polypropylene

- 5.1.3.2 Copolymer Polypropylene

- 5.1.4 Other Product Types

- 5.1.1 Polyethylene

- 5.2 By Thickness

- 5.2.1 3.5-4 mm

- 5.2.2 5-6 mm

- 5.2.3 6.5-8 mm

- 5.2.4 Above 8 mm

- 5.3 By Installation Method

- 5.3.1 Joist-and-Clip System

- 5.3.2 Glue-Down

- 5.3.3 Interlocking/Click-lock

- 5.3.4 Others

- 5.4 By End User

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.5 By Distribution Channel

- 5.5.1 B2C / Retail Consumers

- 5.5.1.1 Home Centers

- 5.5.1.2 Specialty Flooring Stores

- 5.5.1.3 Online

- 5.5.1.4 Local Hardware Shops (unorganized market)

- 5.5.1.5 Other Distribution Channels

- 5.5.2 B2B / Contractors / Builders

- 5.5.1 B2C / Retail Consumers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 Canada

- 5.6.1.2 United States

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.6.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 South-East Asia

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East & Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East & Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Shaw Industries (incl. Shaw Floors)

- 6.4.2 COREtec Floors (USFloors/Shaw)

- 6.4.3 Mannington Mills

- 6.4.4 Mohawk Industries

- 6.4.5 The Dixie Group (TRUCOR)

- 6.4.6 Johnson Hardwood

- 6.4.7 Lions Floor

- 6.4.8 Southwind Floors

- 6.4.9 MSI Surfaces

- 6.4.10 AHF Products (Robbins)

- 6.4.11 Metroflor (HMTX Industries)

- 6.4.12 Karndean Designflooring

- 6.4.13 Novalis Innovative Flooring

- 6.4.14 Tarkett

- 6.4.15 Karastan

- 6.4.16 CFL Flooring

- 6.4.17 Taizhou Huali New Materials

- 6.4.18 Decno Group

- 6.4.19 Provenza Floors

- 6.4.20 Biyork

7 Market Opportunities & Future Outlook

- 7.1 Domestic/nearshore WPC capacity to mitigate tariff/UFLPA risk and shorten lead times

- 7.2 Ultra-thick WPC (>=10-12 mm; 19 mm) for premium hardwood replacement in remodels