|

시장보고서

상품코드

2073375

보안 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Security Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

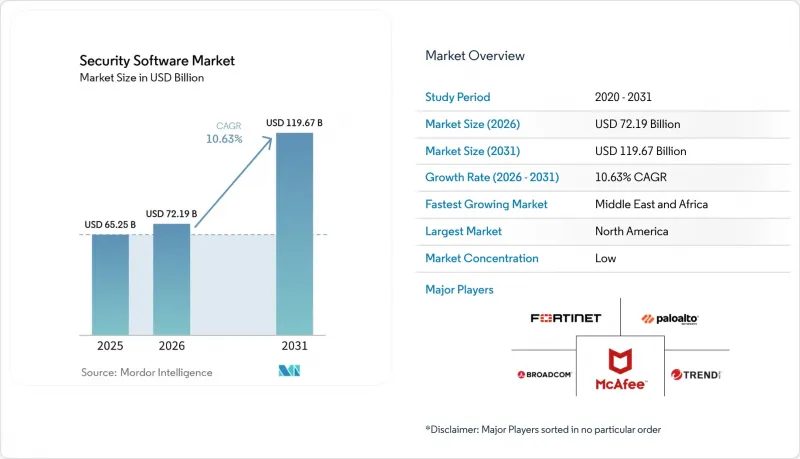

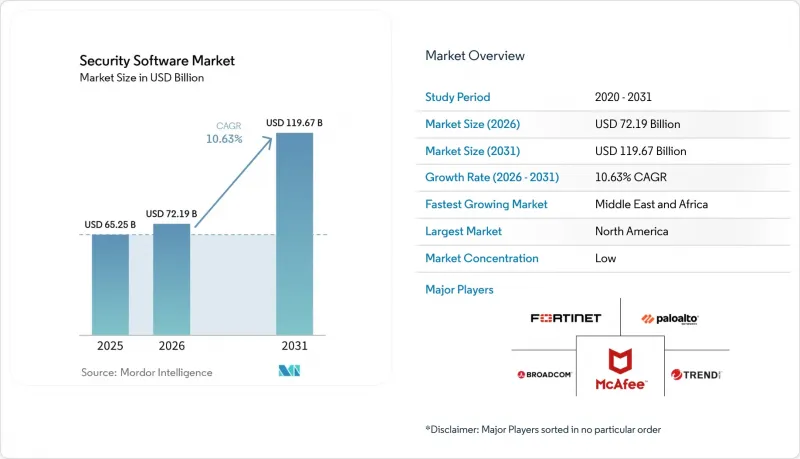

Mordor Intelligence에 의하면, 보안 소프트웨어 시장 규모는 2025년에 652억 5,000만 달러로 평가되었습니다. 2026년 721억 9,000만 달러에서 2031년까지 1,196억 7,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 10.63%를 나타낼 전망입니다.

본 보고서는 제품 유형(안티바이러스/안티멀웨어, 방화벽 및 UTM, 기타), 도입 형태(On-Premise, 클라우드 기반, 기타), 기업 규모(대기업, 중소기업), 용도(모바일 보안, 소비자, 기타), 최종 이용 산업(은행, 금융서비스 및 보험(BFSI), 헬스케어, 소매 및 전자상거래, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 보안 소프트웨어 시장 동향 및 인사이트

사이버 공격 건수와 고도화 추세

공격자들은 스피어 피싱, 딥페이크 음성, 폴리모픽 악성코드를 자동화하는 생성형 AI 도구를 무기로 활용하고 있으며, 기업들은 적응성이 높고 분석 중심의 방어 체제로 전환할 수밖에 없는 상황에 처해 있습니다. 2024년에는 기록된 산업 분야 사고의 25.7%가 제조 시설을 표적으로 삼았으며, 철강 제조업체인 Nucor사는 보안 침해 사고를 겪은 후 전체 감지 체계를 재검토하게 되었습니다. 작년 전 세계 공격의 31%를 아시아태평양(APAC)이 차지했으며, 이 지역의 사이버 범죄로 인한 비용은 2025년까지 3조 3,000억 달러에 달했습니다. 이러한 위협 동향에 따라 보안 소프트웨어 시장에서 통합형 확장 감지 및 대응(XDR) 플랫폼의 도입이 가속화되고 있습니다.

GDPR(EU 개인정보보호규정), CCPA, DORA 및 업종별 사이버 규제 준수 의무

규제 당국은 대략적인 원칙이 아니라 기술적인 관리 조치를 규정하고 있습니다. 2025년 1월에 시행된 EU의 '디지털 운영 복원력법(DORA)'는 금융 기업에 대해 24시간 체제의 사고 보고 및 제3자 위험 모니터링을 유지할 것을 의무화하고 있습니다. 마찬가지로, '사이버 회복탄력성법' 하지만, 모든 연결 제품에서 '보안 설계(Secure by Design)' 소프트웨어가 필요합니다. 따라서 국경을 넘어 사업을 전개하는 조직들은 자동화된 규정 준수 대시보드를 선호하여 도입하고 있으며, 이는 보안 소프트웨어 시장의 플랫폼 매출을 끌어올리고 있습니다.

숙련된 사이버 보안 인력 부족이 총 소유 비용을 끌어올리고 있습니다.

세계적으로 480만 명의 보안 전문가가 부족하며, 미국만 해도 도입 과정의 복잡성에 대응하기 위해 추가로 26만 5,000명의 전문가가 필요합니다. 인력 부족으로 인해 급여가 상승하고 있기 때문에 구매자들은 자동화 기능이나 관리형 서비스 옵션을 갖춘 플랫폼을 선호하는 추세입니다. 벤더들은 수동 방식의 선별 작업을 최소화하기 위해 AI 기반 오케스트레이션 기능을 탑재하고 있지만, 초기 통합 작업에는 여전히 희소한 엔지니어링 기술이 필요하기 때문에 일부 업종에서는 도입 속도가 둔화되고 있습니다.

부문별 분석

ID 및 액세스 관리(IAM) 플랫폼은 2025년 매출의 22.65%를 차지하며, 경계 없는 전략에서 이 플랫폼이 수행하는 핵심적인 역할을 여실히 보여주었습니다. IAM(신원 및 접근 관리)용 보안 소프트웨어 시장 규모는 2026년 171억 8,000만 달러에서 2031년까지 364억 7,000만 달러로 확대되며, 연평균 성장률(CAGR) 16.25%를 나타낼 것으로 전망됩니다. IAM 제품군에는 현재 비밀번호 없는 인증, 적시 권한 관리, 행동 분석 기능이 통합되어 있어 기존의 VPN을 점차 대체하고 있습니다. 하이브리드 트래픽을 검사하는 데에는 여전히 방화벽이나 UTM의 업그레이드가 필수적이지만, 지출은 제로 트러스트 원칙에 부합하는 차세대 솔루션으로 점차 전환되고 있습니다. 암호화 소프트웨어에 대한 수요는 다가오는 양자 위협에 힘입어 증가하고 있으며, 구매자들은 NIST 인증을 받은 포스트 양자 모듈을 제공하는 공급업체를 우선적으로 선택하고 있습니다. 확장형 감지 및 대응(XDR) 제품군은 엔드포인트, 네트워크, SaaS의 텔레메트리 데이터를 통합하여 경보 피로를 줄이는 동시에, 벤더가 플랫폼의 더 광범위한 채택을 실현할 수 있는 기반을 마련하고 있습니다.

예측 기간 동안 경쟁사와의 차별화는 통합의 깊이와 AI의 설명 가능성에 달려 있습니다. 하드웨어 수준의 신뢰의 근원(Root of Trust), API 우선 아키텍처, 그리고 임베디드 규정 준수 매핑을 통합한 벤더들은 더 대규모의 다년 계약 갱신을 성사시키고 있습니다. 제품 로드맵에는 경량 에이전트, 기밀 컴퓨팅 지원, Policy-as-Code 기능이 점점 더 많이 도입되고 있으며, 이는 보안 소프트웨어 시장에서 현대적인 DevSecOps 파이프라인의 오케스트레이션 요구 사항을 충족시키고 있습니다.

2025년에는 클라우드 기반 도입이 매출의 61.50%를 차지했습니다. 이 조직은 유연한 확장성, 지속적인 기능 업데이트, 그리고 운영 비용(OPEX) 예산의 이점을 꼽고 있습니다. 클라우드를 통해 제공되는 솔루션의 보안 소프트웨어 시장 규모는 연평균 성장률(CAGR) 17.8%로 확대되어 2031년까지 1,006억 달러에 달할 것으로 전망됩니다. 규제 대상 워크로드의 경우, 하이브리드 모델이 여전히 필수적이기 때문에 주요 벤더들은 통합 모니터링을 위해 로그를 클라우드 분석 엔진으로 전송하는 On-Premise형 게이트웨이를 출시하고 있습니다.

이러한 변화로 인해 벤더들은 제어 플레인과 데이터 플레인의 분리를 요구받고 있으며, 단일 정책 세트 하에서 컨테이너 클러스터, 에지 노드, SaaS API 전반에 걸쳐 보안 조치를 적용할 수 있게 되었습니다. SASE(Secure Access Service Edge), CASB(Cloud Access Security Broker) 및 웹 격리 기능을 결합한 구독형 번들은 조달 주기를 단축할 수 있다는 점에서 호평을 받고 있습니다. On-Premise의 점유율은 점차 감소할 것이지만, 데이터 로컬리티 규제로 인해 국내에서 처리가 의무화되어 있는 국방, 중요 인프라 및 주권 클라우드 환경에서는 계속해서 입지를 유지할 것입니다.

지역별 분석

북미는 2025년 연방 사이버 보안 예산 275억 달러에 힘입어 2025년 매출의 37.65%를 차지하며 시장을 주도했습니다. 민관 데이터 공유 이니셔티브와 활기찬 벤더 생태계 덕분에 AI 기반 분석의 조기 도입이 가속화되고 있습니다. 미국 증권거래위원회(SEC) 규정에 따른 정보 유출 시 부과되는 높은 벌칙도 적극적인 투자를 더욱 촉진하고 있습니다.

유럽에서는 NIS2 지침 및 사이버 복원력법 등 조화로운 법규제의 혜택을 받고 있으며, 사고 대응 및 안전한 개발을 위한 통일된 기준이 마련되어 있습니다. 임베디드형 다국어 규정 준수 워크플로를 제공하는 벤더는 특히 EU 전역에 걸쳐 있는 금융 기관들 사이에서 지지를 얻고 있습니다.

중동은 각국 정부의 디지털 경제에 대한 야심 찬 노력에 힘입어 14.25%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 사우디아라비아의 사이버 보안 시장은 2025년에 133억 사우디아라비아 리얄(35억 달러)에 달했습니다. 국내 규정에 따라 현지 데이터센터 설치 및 정보 유출 발생 시 수 시간 이내 통보가 의무화되어 있어, 소프트웨어의 신속한 업그레이드가 요구되고 있습니다. 한편, 아시아태평양 각국 정부는 양자 위협과 국가 주도의 공격을 완화하기 위해 공동 보안 센터에 대한 투자를 확대하고 있으며, 이 지역은 보안 소프트웨어 시장에 있어 중요한 성장의 전초기지로서의 입지를 확고히 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.07According to Mordor Intelligence, the security software market size was valued at USD 65.25 billion in 2025 and estimated to grow from USD 72.19 billion in 2026 to reach USD 119.67 billion by 2031, at a CAGR of 10.63% during the forecast period (2026-2031).

This report is Segmented by Product Type (Antivirus/Anti-malware, Firewall & UTM, and Others), Deployment Mode (On-Premises, Cloud-Based and Others), Enterprise Size (Large Enterprises, SME), Application (Mobile Security, Consumer and Others), End-Use Industry (BFSI, Healthcare, Retail & E-Commerce and Others), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Security Software Market Trends and Insights

Escalating Volume & Sophistication of Cyber-Attacks

Attackers are weaponizing generative AI tools that automate spear-phishing, deepfake audio, and polymorphic malware, forcing enterprises to pivot toward adaptive, analytics-driven defenses. In 2024, 25.7% of recorded industrial incidents targeted manufacturing sites, prompting steelmaker Nucor to overhaul its entire detection stack after a breach. APAC accounted for 31% of global attacks last year, and regional cybercrime costs are forecast to reach USD 3.3 trillion by 2025. These threat dynamics accelerate adoption of unified extended detection and response (XDR) platforms within the security software market.

Mandatory Compliance with GDPR, CCPA, DORA & Sectoral Cyber-Rules

Regulators are prescribing technical controls rather than high-level principles. The EU Digital Operational Resilience Act, effective January 2025, compels financial firms to maintain 24-hour incident reporting and third-party risk oversight. Parallel mandates in the Cyber Resilience Act demand secure-by-design software across all connected products. Cross-border organizations therefore favor automated compliance dashboards, boosting platform revenue inside the security software market.

Shortage of Skilled Cyber Personnel Inflates Total Cost of Ownership

A global talent gap of 4.8 million security professionals persists, with the United States alone needing another 265,000 specialists to keep pace with deployment complexity. Scarcity pushes salaries higher, compelling buyers to favour platforms with automation and managed service options. While vendors embed AI-driven orchestration to minimize manual triage, the upfront integration effort still requires scarce engineering skill, slowing rollouts in some verticals.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Cloud Workload Expansion Demanding Zero-Trust Security

- Cyber-Insurance Underwriting Now Mandating Software Controls

- Fragmented Tool Sprawl Drives Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Identity and Access Management platforms generated 22.65% of 2025 revenue, underlining their central role in perimeter-less strategies. The security software market size for IAM is forecast to grow from USD 17.18 billion in 2026 to USD 36.47 billion by 2031, expanding at 16.25% CAGR. IAM suites now bundle password-less authentication, just-in-time privilege, and behavioural analytics, displacing legacy VPNs. Firewall and UTM upgrades remain essential for hybrid traffic inspection, yet spending is shifting toward next-gen offerings aligned to zero-trust principles. Encryption software demand is bolstered by looming quantum threats, with buyers prioritizing vendors offering NIST-validated post-quantum modules. Extended detection and response (XDR) suites unify endpoint, network, and SaaS telemetry, reducing alert fatigue and positioning vendors for wider platform adoption.

Over the forecast period, competitive differentiation will depend on integration depth and AI explainability. Vendors integrating hardware-level root-of-trust, API-first architecture, and built-in compliance mapping are securing larger multiyear renewals. Product roadmaps increasingly feature lightweight agents, confidential computing support, and policy-as-code functions, meeting the orchestration needs of modern DevSecOps pipelines within the security software market.

Cloud-based deployments captured 61.50% revenue in 2025. Organizations cite elastic scalability, continuous feature updates, and opex budgeting benefits. The security software market size for cloud-delivered solutions is projected to climb at an 17.8% CAGR, reaching USD 100.6 billion by 2031. Hybrid models remain vital for regulated workloads; hence leading vendors release on-premises gateways that forward logs to cloud analytics engines for central oversight.

The shift pushes vendors to decouple control planes from data planes, enabling enforcement across container clusters, edge nodes, and SaaS APIs under one policy set. Subscription bundles combining secure access service edge (SASE), cloud access security broker (CASB), and web isolation are resonating, as they cut procurement cycles. On-premises share will gradually decline yet persist in defence, critical infrastructure, and sovereign cloud environments where data-locality rules require in-country processing.

Complete Report Scope:

- By Product Type

- Antivirus / Anti-malware

- Firewall and UTM

- Encryption Software

- Identity and Access Management (IAM)

- Endpoint-protection Platform (EPP / EDR)

- Network Security Platforms

- Other Types

- By Deployment Mode

- On-premise

- Cloud-based

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SME)

- By Application

- Mobile Security

- Consumer Security Suites

- Enterprise / Data-centre Security

- By End-use Industry

- BFSI

- Healthcare

- Retail and e-Commerce

- Manufacturing

- Energy and Utilities

- Aerospace and Defence

- Telecommunications

- Government and Public Sector

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America dominated with 37.65% revenue in 2025, supported by the USD 27.5 billion 2025 federal cybersecurity budget. Public-private data-sharing initiatives and a vibrant vendor ecosystem accelerate early adoption of AI-driven analytics. High breach disclosure penalties under U.S. SEC rules further encourage proactive investment.

Europe benefits from harmonized legislation such as the NIS2 Directive and Cyber Resilience Act, providing unified benchmarks for incident response and secure development. Vendors offering built-in multilingual compliance workflows gain traction, especially among pan-EU financial institutions.

The Middle East posts the fastest 14.25% CAGR, spurred by sovereign digital-economy ambitions. Saudi Arabia's cybersecurity market reached SAR 13.3 billion (USD 3.5 billion) in 2025. National regulations mandate local data centers and breach notification within hours, compelling rapid software upgrades. Meanwhile, Asia-Pacific governments invest in joint security centers to mitigate quantum risks and state-sponsored attacks, positioning the region as a significant growth frontier for the security software market.

- Microsoft Corporation

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- Fortinet, Inc.

- Broadcom Inc. (Symantec)

- Check Point Software Technologies Ltd.

- International Business Machines Corporation (IBM)

- Trend Micro Incorporated

- CrowdStrike Holdings, Inc.

- McAfee Corp.

- Kaspersky Lab

- Sophos Group plc

- Bitdefender LLC

- Zscaler, Inc.

- Okta, Inc.

- Cloudflare, Inc.

- SentinelOne, Inc.

- Proofpoint, Inc.

- Rapid7, Inc.

- Qualys, Inc.

- Trellix (Musarubra US LLC)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating volume and sophistication of cyber-attacks

- 4.2.2 Mandatory compliance with GDPR, CCPA, DORA and sectoral cyber-rules

- 4.2.3 Rapid cloud workload expansion demanding zero-trust security

- 4.2.4 Cyber-insurance underwriting now mandating software controls

- 4.2.5 Convergence of OT and IT triggering spend on specialised ICS security

- 4.2.6 AI-powered "offensive security tooling" arms-race among threat actors

- 4.3 Market Restraints

- 4.3.1 Shortage of skilled cyber personnel inflates total cost of ownership

- 4.3.2 Fragmented tool sprawl drives integration complexity

- 4.3.3 Rising open-source security stack cannibalises licence revenue

- 4.3.4 Quantum-safe migration uncertainty delaying long-term contracts

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Ecosystem Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Antivirus / Anti-malware

- 5.1.2 Firewall and UTM

- 5.1.3 Encryption Software

- 5.1.4 Identity and Access Management (IAM)

- 5.1.5 Endpoint-protection Platform (EPP / EDR)

- 5.1.6 Network Security Platforms

- 5.1.7 Other Types

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud-based

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SME)

- 5.4 By Application

- 5.4.1 Mobile Security

- 5.4.2 Consumer Security Suites

- 5.4.3 Enterprise / Data-centre Security

- 5.5 By End-use Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare

- 5.5.3 Retail and e-Commerce

- 5.5.4 Manufacturing

- 5.5.5 Energy and Utilities

- 5.5.6 Aerospace and Defence

- 5.5.7 Telecommunications

- 5.5.8 Government and Public Sector

- 5.5.9 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 Israel

- 5.6.4.2 Saudi Arabia

- 5.6.4.3 United Arab Emirates

- 5.6.4.4 Turkey

- 5.6.4.5 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Cisco Systems, Inc.

- 6.4.3 Palo Alto Networks, Inc.

- 6.4.4 Fortinet, Inc.

- 6.4.5 Broadcom Inc. (Symantec)

- 6.4.6 Check Point Software Technologies Ltd.

- 6.4.7 International Business Machines Corporation (IBM)

- 6.4.8 Trend Micro Incorporated

- 6.4.9 CrowdStrike Holdings, Inc.

- 6.4.10 McAfee Corp.

- 6.4.11 Kaspersky Lab

- 6.4.12 Sophos Group plc

- 6.4.13 Bitdefender LLC

- 6.4.14 Zscaler, Inc.

- 6.4.15 Okta, Inc.

- 6.4.16 Cloudflare, Inc.

- 6.4.17 SentinelOne, Inc.

- 6.4.18 Proofpoint, Inc.

- 6.4.19 Rapid7, Inc.

- 6.4.20 Qualys, Inc.

- 6.4.21 Trellix (Musarubra US LLC)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment