|

시장보고서

상품코드

2073380

클라우드 관리형 스위치 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Cloud Managed Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

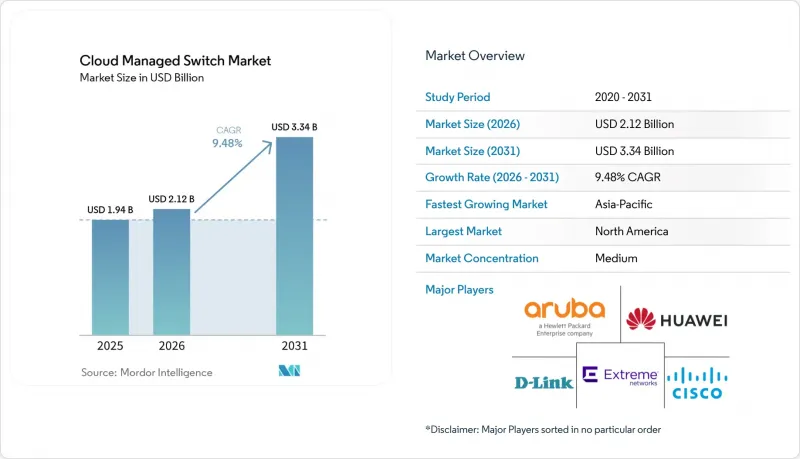

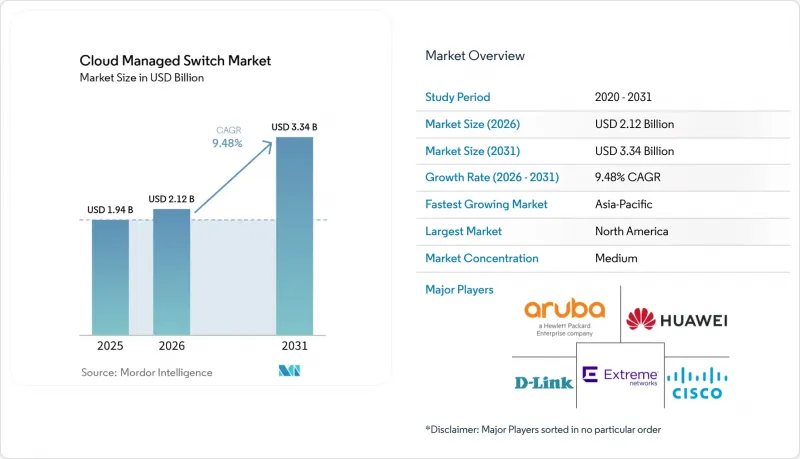

Mordor Intelligence에 의하면, 클라우드 관리형 스위치 시장 규모는 2025년 19억 4,000만 달러로 평가되었습니다. 2026년 21억 2,000만 달러에서 2031년까지 33억 4,000만 달러로 확대될 것으로 예측되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 9.48%를 나타낼 전망입니다.

본 보고서는 포트 수(8포트 이하, 16포트 모델, 기타), 스위치 용량(1 GbE, 2.5/5GbE 멀티기가, 기타), 기업 규모(대기업, 중소기업), 최종 사용자 산업(교육 기관, 기타), 배포 모델(퍼블릭 클라우드 관리형, 기타), 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러) 단위로 제시되어 있습니다.

세계의 클라우드 관리형 스위치 시장 동향 및 인사이트

멀티 기가비트 Wi-Fi 6/6E 백홀 수요 급증

기업들은 Wi-Fi 무선 기기의 도입 밀도를 높이고 있으며, 혼잡을 피하기 위해서는 새로운 Wi-Fi 6E 액세스 포인트 1대당 일반적으로 2.5기가비트 또는 5기가비트의 업링크가 필요합니다. 따라서 멀티 레이트(1/2.5/5/10 기가비트) BASE-T 포트를 탑재한 클라우드 관리형 스위치가 교육 기관, 의료 기관 및 대기업 캠퍼스에서 기존의 1기가비트 모델을 대체하고 있습니다. 각 벤더사는 기존 카테고리 6A 케이블을 재사용하는 멀티 기가비트 구축의 효과성을 검증하고 있으며, 업무에 지장을 주는 배선 공사를 다시 실시하는 것을 피하고 있습니다. 미국 및 서유럽 일부 지역의 조기 도입 기업들은 아시아태평양보다 12-18개월 앞서 6기가헤르츠 대역 개방의 혜택을 누렸으나, 현재 인도, 일본 및 아세안(ASEAN) 국가들에서 진행 중인 주파수 경매가 동기화된 갱신 주기를 촉발하고 있습니다. 채널 파트너들이 스위치, 액세스 포인트, 라이선스 계약을 단일 계약으로 통합함에 따라, CFO는 멀티 기가비트 백홀 업그레이드를 자본 지출이 아닌 운영비로 간주하게 되었으며, 이로 인해 예산 승인이 원활해지고 향후 3년 동안 대량 출하가 지속될 것입니다.

OPEX 모델을 도입하는 중소기업의 부상

중소기업에는 전담 네트워크 엔지니어가 부족하기 때문에 미리 설정되어 있고 자동으로 업데이트되며, 클라우드를 통해 자연어 기반의 문제 해결 기능을 제공하는 솔루션을 선호합니다. 구독 중심의 가격 정책을 통해 하드웨어, 펌웨어, 지원 서비스가 예측 가능한월이용료에 통합되어, 성장을 위한 활동에 투입할 자금을 확보할 수 있습니다. 매니지드 서비스 제공업체(MSP)는 연결성, 보안, 협업 기능을 턴키 솔루션으로 패키지화하여 이러한 기회를 활용함으로써, 사내에 IT 인력을 보유한 대기업 이외 시장에서도 수요를 확대되고 있습니다. 시장의 하위 계층에서 치열한 경쟁이 벌어지면서 공격적인 가격 정책이 유지되고 있는 반면, AI를 활용한 대시보드를 통해 MSP의 운영 비용이 절감되어, 한 명의 운영자가 수백 개의 거점을 동시에 관리할 수 있게 되었습니다. 계약 기간은 보통 3년에 달하기 때문에 OPEX 모델은 벤더와 파트너에게 확실한 수익 전망을 제공하며 생태계의 성장세를 더욱 강화하고 있습니다.

이전의 복잡성과 비용 장벽

On-Premise 컨트롤러에서 클라우드 관리로 전환할 경우, 대부분의 경우 데이터 전송 비용, 아키텍처 재구축, 새로운 라이선스 계약이 필요하며, 이 모든 비용을 합치면 프로젝트 예산이 15-25% 증가하게 됩니다. 독자적인 사양의 API나 고유한 ID 저장소는 여러 공급업체가 혼재된 환경을 더욱 복잡하게 만듭니다. 또한, 구형 하드웨어에 대한 지원 종료 발표로 인해 신속한 의사결정이 요구되고 있습니다. 지연 시간에 민감한 워크로드를 On-Premise에 남겨두는 기업은 완전한 마이그레이션이 완료될 때까지 두 개의 제어 플레인이 공존해야 하기 때문에 도구 분산이라는 위험을 감수하게 됩니다. 그 결과 발생하는 운영상의 부담으로 인해 투자 회수 기간이 2년 이상으로 길어지게 되어, 신중한 구매자들을 멀어지게 합니다.

부문별 분석

24포트 카테고리는 전력 예산과 랙 공간이 제한적인 대부분의 지점 및 중규모 캠퍼스의 통신실 환경에 적합하기 때문에 2025년 매출의 46.72%를 차지했습니다. 이러한 고정형 스위치는 앞으로도 계속해서 대량으로 출하될 것이지만, 성장세는 분산형 데이터센터의 스파인 계층을 지원하는 96포트 및 섀시 플랫폼에 집중될 전망입니다. 고밀도 섀시용 클라우드 관리형 스위치 시장은 하이퍼스케일러 및 AI 추론 클러스터 수요에 힘입어 연평균 성장률(CAGR) 18.43%로 확대될 것으로 전망됩니다. 현재 AI 훈련용 랙은 30kW 이상의 전력을 소비하고 있으며, 집중형 냉각 방식에서는 단일 관리 평면 하에서 여러 라인 카드를 통합하는 모듈식 백플레인이 선호되고 있습니다. 각 벤더는 현장에서 교체 가능한 팬, 전원 공급 장치, 패브릭 모듈을 제공하고 있으며, 이를 통해 고정 폼 팩터 장치를 능가하는 평균 고장 간격(MTBF)을 실현함으로써, 모델 훈련 중 가동 중단을 허용할 수 없는 운영자에게 매력적인 선택지가 되고 있습니다.

또한, Dell의 “PowerSwitch Z9664F-ON"는 2 랙 유닛 폼 팩터를 채택한 64포트 400기가비트 이더넷 스위치로, Enterprise SONiC Distribution 및 Dell SmartFabric OS10을 통해 하드웨어와 소프트웨어의 분리(disaggregation)를 지원합니다. 이를 통해 SmartFabric Services를 활용한 제로 터치 설치와 자율적인 패브릭 구축이 가능해집니다. 또한, 지점 도입의 경우 소매점의 키오스크나 원격의료 부스 등 설치 공간이 제한된 장소에서는 계속해서 8포트 및 16포트 스위치가 도입되고 있습니다. 교육 기관 및 호텔·관광 업계의 구매 담당자들은 포트 밀도와 수용 가능한 초기 비용 간의 균형이 잘 잡힌 48포트 모델을 선호하며, PoE 예산은 최신 액세스 포인트에 필요한 740와트의 기준치에 도달하고 있습니다. 24포트 모델의 상대적 시장 점유율은 하락하고 있지만, 새로운 IoT 엔드포인트, 배지 리더기, 센서 등이 액세스 계층 수요를 보완하고 있어 절대적인 출하 대수는 견조한 추세를 보이고 있습니다.

성숙기에 접어든 10기가비트 이더넷 부문은 트랜시버의 광범위한 공급과 비트당 비용이 저렴하다는 점 덕분에 2025년에는 36.77%의 점유율을 차지하며 시장을 주도했습니다. 그럼에도 불구하고, Wi-Fi 6E 액세스 포인트가 2.5/5 기가비트 업링크로 전환되고 엣지 서버에 25 기가비트 네트워크 인터페이스 카드가 표준으로 탑재됨에 따라, 25/40 기가비트 부문은 연평균 13.26%의 성장률을 보일 것으로 전망됩니다. 이러한 전환을 통해 기존 구리선 인프라를 유지하면서 더 높은 처리량을 실현할 수 있으므로, 캠퍼스 환경에 부담을 덜 주는 업그레이드 경로가 됩니다. 최상위 계층에서는 하이퍼스케일 클라우드가 이미 AI 가속기에 데이터를 공급하기 위해 400기가비트 및 800기가비트 패브릭을 도입하고 있습니다. 출하 대수는 적지만 평균 판매 가격이 높아 수익에 기여하는 비중이 크며, 조기 도입 기업들을 통해 수냉 설계에 대한 검증이 진행됨에 따라 해당 기술은 엔터프라이즈용 모델로도 확산될 것으로 보입니다.

1기가비트 대역은 예산 제약이나 레거시 컨트롤러로 인해 링크 속도가 제한되는 신흥 시장이나 기존 설비의 개보수 분야에서 여전히 중요한 위치를 차지하고 있습니다. 그렇긴 하지만, 성장의 핵심은 1/2.5/5/10 기가비트를 자동 협상하는 멀티레이트 스위치에 있으며, 포트별 전면적인 교체를 필요로 하지 않으면서도 미래에 대비할 수 있는 능력을 제공합니다. 2031년까지는 멀티레이트 실리콘이 보급형 제품 라인에도 널리 보급되어, 초저가 모델을 제외하고는 고정 1기가비트 칩을 대체하게 될 것입니다.

지역별 분석

북미는 Wi-Fi 6E 주파수 대역의 조기 확보, 수년에 걸친 교육 보조금, 그리고 AI 인프라에 대한 투자 가속화에 힘입어 2025년 매출의 36.77%를 차지했습니다. 클라우드 관리형 스위치의 업데이트 주기는 미국 및 캐나다 전역에서 진행 중인 구독형 소프트웨어로의 광범위한 전환 추세와 발맞추고 있으며, 각 벤더들은 6분기 연속으로 데이터센터용 스위치 수주가 10%대 중반의 성장세를 보이고 있다고 보고하고 있습니다. 이미 도입된 장비는 성숙기에 접어들었으나, 저전력 대체 장비 및 지속적인 사이버 보안 가시성에 대한 수요는 계속되고 있어, 2031년까지 해당 지역의 연평균 성장률(CAGR)은 8% 전후를 유지할 것으로 전망됩니다.

아시아태평양은 가장 빠르게 성장하는 지역으로, 중국, 인도 및 아세안(ASEAN) 회원국들이 스마트시티 그리드, 주권 클라우드, 5G 전송 네트워크에 자금을 투자하고 있어 연평균 15.32%의 성장률이 예상됩니다. 이 지역의 데이터센터용량은 2026년까지 17기가와트를 넘어설 것으로 전망되며, 랙당 전력 밀도는 이미 30kW를 돌파했습니다. 이로 인해 사업자들은 수냉식 섀시나 400/800 기가비트 패브릭으로의 전환을 강요받고 있습니다. 주권 조달 프레임워크에서는 네트워크, 컴퓨팅, 자금 조달이 한 세트로 제공되는 경우가 많으며, 국내 유력 기업들이 우대받는 한편, 관리 계획을 현지화하는 해외 공급업체에게도 진입의 여지가 남아 있습니다.

유럽의 동향은 퍼블릭 클라우드 도입을 제한하는 한편, 다양한 기능을 갖춘 프라이빗 클라우드 컨트롤러를 장려하는 엄격한 개인정보 보호 및 지속가능성 프레임워크에 의해 형성되고 있습니다. 프랑스의 SecNumCloud나 독일의 C5와 같은 인증 제도에서는 처리 장소에 대한 문서화 및 공급망의 투명성이 요구되며, 탄소 중립을 위한 로드맵을 갖춘 입찰자는 가산점 대상이 됩니다. 가맹국들이 캠퍼스 및 도시권의 교통망을 현대화함에 따라, 지원 종료에 앞서 업데이트 프로젝트를 의무화하는 소버린 클라우드 요건의 뒷받침을 받아, 2031년까지 유럽의 연평균 성장률(CAGR)은 약 7.8%로 상승할 것으로 전망됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the cloud managed switch market size is projected to expand from USD 1.94 billion in 2025 and USD 2.12 billion in 2026 to USD 3.34 billion by 2031, registering a CAGR of 9.48% between 2026 and 2031.

This report is Segmented by Port Count (8-Port and Below, 16-Port Models, and More), Switch Capacity (1 GbE, 2. 5/5 GbE Multigig, and More), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Educational Institutions, and More), Deployment Model (Public-Cloud Managed, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Cloud Managed Switch Market Trends and Insights

Surge in Multi-Gigabit Wi-Fi 6/6E Back-Haul Demand

Enterprises are densifying Wi-Fi radio deployments, and each new Wi-Fi 6E access point typically requires 2.5 gigabit or 5 gigabit uplinks to avoid congestion. Cloud-managed switches equipped with multi-rate 1/2.5/5/10-gigabit BASE-T ports therefore replace legacy 1-gigabit models in education, healthcare, and large corporate campuses. Vendors have validated multi-gigabit deployments that reuse existing Category 6A cabling, avoiding disruptive rewiring. Early adopters in the United States and parts of Western Europe benefited from 6 gigahertz spectrum clearance 12-18 months ahead of Asia-Pacific, but spectrum auctions across India, Japan, and ASEAN economies are now triggering synchronized refresh cycles. As channel partners bundle switches, access points, and license subscriptions under a single contract, CFOs perceive multi-gigabit back-haul upgrades as an operational rather than capital event, smoothing budget approvals and sustaining volume shipments over the next three years.

Rise of Small and Medium Enterprises Adopting OPEX Models

SMEs lack dedicated network engineers and favor solutions that arrive pre-provisioned, self-update, and deliver natural-language troubleshooting from the cloud. Subscription-first pricing turns hardware, firmware, and support into one predictable monthly fee, freeing cash for growth initiatives. Managed-service providers (MSPs) capitalize by packaging connectivity, security, and collaboration into turnkey offerings, expanding addressable demand beyond enterprises with in-house IT staff. Competitive intensity at the lower end of the market sustains aggressive price points, while AI-driven dashboards reduce MSP overhead and let a single operator manage hundreds of sites concurrently. Because contract lengths typically span three years, the OPEX model locks in revenue visibility for vendors and partners, further reinforcing ecosystem momentum.

Migration Complexity and Cost Barriers

Moving from on-premises controllers to cloud management often incurs data-egress fees, re-architecting efforts, and new licensing commitments that collectively inflate project budgets by 15-25%. Proprietary APIs and unique identity stores further complicate dual-vendor environments, while end-of-life announcements for older hardware force accelerated decision making. Enterprises that keep latency-sensitive workloads on-site risk tool fragmentation, as two control planes must co-exist until full migration completes. The resulting operational overhead extends payback periods out to two years or more, deterring conservative buyers.

Other drivers and restraints analyzed in the detailed report include:

- Edge and IoT Proliferation Needing Remote Switch Management

- Sustainability-Focused PoE+ Power Optimization

- Data-Sovereignty-Driven On-Prem Mandates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 24-port category captured 46.72% of 2025 revenue because it fits most branch and midsize campus closets, where power budgets and rack space are limited. These fixed-configuration switches will continue to ship in volume, but growth skews toward 96-port and chassis platforms that anchor spine layers in distributed data centers. The cloud managed switch market for high-density chassis is projected to expand at a 18.43% CAGR, driven by hyperscaler and AI inference cluster demand. AI training racks now draw over 30 kilowatts, and centralized cooling favors modular backplanes that consolidate multiple line cards under one management plane. Vendors offer field-replaceable fans, power supplies, and fabric modules, driving mean-time-between-failure metrics that surpass fixed-form-factor devices and appeal to operators who cannot tolerate downtime during model training.

Furthermore, Dell's PowerSwitch Z9664F-ON, a 64-port 400-gigabit Ethernet switch in 2-rack-unit form factor, supports disaggregated hardware and software via Enterprise SONiC Distribution and Dell SmartFabric OS10, enabling zero-touch installation and autonomous fabric deployment through SmartFabric Services. Furthermore, branch deployments continue to deploy 8-port and 16-port switches where space is tight, such as retail kiosks or remote healthcare pods. Education and hospitality buyers favor 48-port models that balance port density with acceptable upfront cost, and PoE budgets reach the 740-watt threshold required for modern access points. While the relative share of 24-port units will slip, absolute shipments remain healthy because new IoT endpoints, badge readers, and sensors replenish access-layer demand.

The mature 10 gigabit Ethernet segment dominated 2025 at 36.77% share due to broad transceiver availability and favorable cost per bit. Still, the 25/40 gigabit cohort is set to grow 13.26% annually as Wi-Fi 6E access points migrate to 2.5/5 gigabit uplinks and edge servers standardize on 25 gigabit network interface cards. This transition preserves the installed copper plant while unlocking higher throughput, making it a low-friction upgrade path for campuses. At the top end, hyperscale clouds already deploy 400 gigabit and 800 gigabit fabrics to feed AI accelerators. Although volumes are small, outsized average selling prices lift revenue contribution, and early adopters validate liquid-cooling designs that will trickle down to enterprise variants.

The 1 gigabit tier remains meaningful in emerging markets and brown-field retrofits where budget limitations or legacy controllers cap link speeds. Nevertheless, growth concentrates in multi-rate switches that auto-negotiate 1/2.5/5/10 gigabit, offering future readiness without a port-by-port forklift. By 2031, multi-rate silicon will permeate even entry-level lines, displacing static 1 gigabit chips except in ultra-low-cost models.

Complete Report Scope:

- By Port Count

- 8-port and below

- 16-port Models

- 24-port Models

- 48-port Models

- 96-port and Chassis-based

- By Switch Capacity (Data-rate)

- 1 GbE

- 2.5/5 GbE (Multigig)

- 10 GbE

- 25/40 GbE

- 100 GbE and above

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By End-user Industry

- Educational Institutions

- Healthcare Facilities

- Hospitality and Retail Locations

- Public Sector and Smart Cities

- Other End user Industries

- By Deployment Model

- Public-cloud managed

- Vendor-hosted private cloud

- Self-hosted virtual controller (on-prem IaaS)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Australia and New Zealand

- Rest of the Asia-Pacific

- Middle East and Africa

- Middle East

- UAE

- Saudi Arabia

- Turkey

- Rest of the Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America held 36.77% of 2025 revenue, buoyed by early Wi-Fi 6E spectrum clearance, multi-year education grants, and accelerating AI infrastructure investment. Cloud managed switch refresh cycles align with broader shifts toward subscription software across the United States and Canada, and vendors report mid-teens data-center switch order growth for six consecutive quarters. Although the installed base is maturing, demand persists for power-efficient replacements and sustained cybersecurity visibility, keeping the regional CAGR near 8% through 2031.

Asia-Pacific is the fastest-growing territory, forecast to expand at 15.32% annually as China, India, and ASEAN members pour funding into smart-city grids, sovereign clouds, and 5G transport networks. Regional data-center capacity is on track to exceed 17 gigawatts by 2026, and rack power densities now breach 30 kilowatts, pushing operators toward liquid-cooled chassis and 400/800 gigabit fabrics. Sovereign procurement frameworks often bundle networking, compute, and financing, favoring domestic champions but still leaving room for foreign suppliers that localize management plans.

Europe's trajectory is shaped by stringent privacy and sustainability frameworks that constrain public-cloud adoption but incentivize feature-rich private-cloud controllers. Certifications such as SecNumCloud in France and C5 in Germany require documented processing locations and transparent supply chains, and bidders with carbon-neutral roadmaps secure bonus scoring. As member states modernize campus and metropolitan transport networks, Europe's CAGR should rise to roughly 7.8% through 2031, underpinned by sovereign-cloud mandates that force refresh projects ahead of support sunsets.

- Cisco Systems

- HPE (Aruba)

- Juniper Networks (Mist)

- Extreme Networks

- Huawei Technologies

- Arista Networks

- Ubiquiti Inc.

- CommScope (Ruckus)

- Fortinet

- TP-Link

- D-Link Corporation

- NETGEAR Inc.

- Alcatel-Lucent Enterprise

- Ruijie Networks

- Cambium Networks

- Zyxel Communications

- Allied Telesis

- MikroTik

- Dahua Technology

- H3C Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Multi-gigabit Wi-fi 6/6E Back-haul Demand

- 4.2.2 Rise of Small and Medium Enterprises (SMEs) Adopting OPEX Models

- 4.2.3 Edge and IoT Proliferation Needing Remote Switch Management

- 4.2.4 Sustainability-focused PoE+ Power Optimisation

- 4.2.5 Open-ran Transport Network Build-outs

- 4.2.6 AI-driven Network Analytics in Cloud Dashboards

- 4.3 Market Restraints

- 4.3.1 Migration Complexity and Cost Barriers

- 4.3.2 Data-sovereignty-driven On-prem Mandates

- 4.3.3 Semiconductor Supply-chain Volatility

- 4.3.4 Vendor Lock-in to Proprietary Clouds

- 4.4 Industry Supply-Chain Analysis

- 4.5 Macroeconomic Impact Assessment

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook (SDN, NetOps Automation)

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Port Count

- 5.1.1 8-port and below

- 5.1.2 16-port Models

- 5.1.3 24-port Models

- 5.1.4 48-port Models

- 5.1.5 96-port and Chassis-based

- 5.2 By Switch Capacity (Data-rate)

- 5.2.1 1 GbE

- 5.2.2 2.5/5 GbE (Multigig)

- 5.2.3 10 GbE

- 5.2.4 25/40 GbE

- 5.2.5 100 GbE and above

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-user Industry

- 5.4.1 Educational Institutions

- 5.4.2 Healthcare Facilities

- 5.4.3 Hospitality and Retail Locations

- 5.4.4 Public Sector and Smart Cities

- 5.4.5 Other End user Industries

- 5.5 By Deployment Model

- 5.5.1 Public-cloud managed

- 5.5.2 Vendor-hosted private cloud

- 5.5.3 Self-hosted virtual controller (on-prem IaaS)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Australia and New Zealand

- 5.6.4.7 Rest of the Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 UAE

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of the Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Cisco Systems

- 6.4.2 HPE (Aruba)

- 6.4.3 Juniper Networks (Mist)

- 6.4.4 Extreme Networks

- 6.4.5 Huawei Technologies

- 6.4.6 Arista Networks

- 6.4.7 Ubiquiti Inc.

- 6.4.8 CommScope (Ruckus)

- 6.4.9 Fortinet

- 6.4.10 TP-Link

- 6.4.11 D-Link Corporation

- 6.4.12 NETGEAR Inc.

- 6.4.13 Alcatel-Lucent Enterprise

- 6.4.14 Ruijie Networks

- 6.4.15 Cambium Networks

- 6.4.16 Zyxel Communications

- 6.4.17 Allied Telesis

- 6.4.18 MikroTik

- 6.4.19 Dahua Technology

- 6.4.20 H3C Technologies

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment