|

시장보고서

상품코드

2073431

탄소섬유 강화 플라스틱(CFRP) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Carbon Fiber Reinforced Plastic (CFRP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

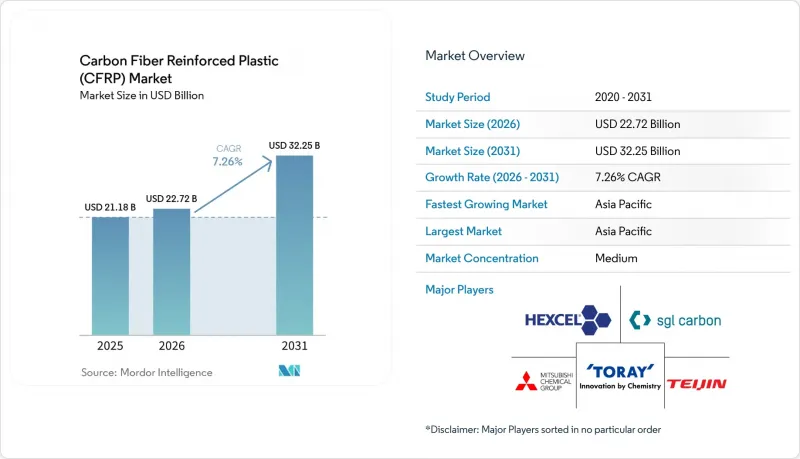

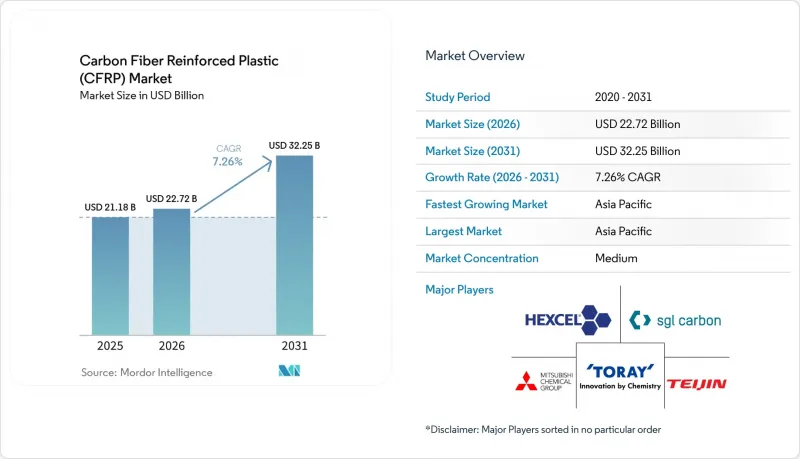

Mordor Intelligence에 의하면, 탄소섬유 강화 플라스틱(CFRP) 시장 규모는 2025년에 211억 8,000만 달러로 평가되었습니다. 2026년 227억 2,000만 달러에서 2031년까지 322억 5,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 7.26%를 나타낼 전망입니다.

본 보고서에서는 업계를 수지 유형(열경화성 CFRP 및 열가소성 CFRP), 원료 전구체(PAN, 피치, 레이온) 및 기타(리그닌계 등), 최종 사용자 산업(항공우주, 자동차, 풍력 발전 산업 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류하고 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 탄소섬유 강화 플라스틱(CFRP) 시장 동향 및 분석

민간 항공기 미수주 물량의 급증

민간 항공 분야에서 1만 5,000대를 넘는 전례 없는 미인도 주문량으로 인해, 탄소섬유 복합재료에 대한 지속적인 수요가 발생하고 있습니다. 항공기 제조업체들이 열가소성 수지로 만든 2차 구조재의 채택을 추진하고 있는 것은 성능을 저하시키지 않으면서 제조 속도를 높이기 위함입니다. 공급업체들은 이에 대응하고, 위험을 분산시키며, 공급 차질을 방지하기 위해 여러 섬유 공급처의 인증 절차를 진행하고 있습니다.

전동화가 가속화되는 CFRP 배터리 케이스

현재 전기차 제조업체들은 알루미늄 제품에 비해 케이스 무게를 최대 91%까지 줄일 수 있는 탄소섬유 배터리 하우징을 지정하고 있습니다. 1Kg의 경량화 분량마다 추가 배터리용량으로 활용할 수 있어, 차량 크기를 늘리지 않고도 주행 거리를 연장할 수 있습니다. 난연성 열가소성 수지와 일체형 열관리층 덕분에 복합재료는 엄격한 안전 기준을 충족할 수 있게 되었으며, 탄소섬유 강화 플라스틱 시장은 대량 생산되는 자동차 분야로 더욱 깊이 침투하고 있습니다.

항공우주 등급 PAN 전구체의 높은 비용

항공우주 규격에 부합하는 폴리아크릴로니트릴(PAN)은 1kg당 33-66달러에 판매되고 있어, 비용에 민감한 분야로의 진출을 제한하고 있습니다. 엄격한 청정도 및 균일성 기준을 충족하는 공급업체가 적어, 공급의 집중화로 인한 위험이 발생하고 있습니다. 수용성 전구체에 대한 연구는 비용 절감을 기대하게 하지만, 보수적인 항공우주 공급망에서 상업적 실증에 이르기까지는 시간이 걸릴 것으로 보입니다.

부문별 분석

2025년, 탄소섬유 강화 플라스틱 시장 점유율의 72.15%를 열경화성 시스템이 차지했으며, 이는 항공우주 분야가 오랫동안 에폭시 프리프레그에 의존해 온 데 기인합니다. 그러나 열가소성 솔루션은 2031년까지 연평균 성장률(CAGR) 8.02%로 성장을 지속하고, 있으며, 이는 신속한 가공 및 재활용성에 대한 수요가 증가하고 있음을 반영합니다. 에어버스의 열가소성 수지 재질 동체 패널은월70대 이상의 생산 속도에 대응할 수 있는 사이클 타임 단축을 실현했으며, 자동차 부품 공급업체에서는 프레스 가공 사이클을 수 초까지 단축하고 있습니다.

또한, 열가소성 복합재료는 조립 공정에서 용접이나 재용융이 가능하기 때문에 모빌리티, eVTOL, 수소 저장 분야의 탄소섬유 강화 플라스틱 시장 규모를 확대되고 있습니다. CF-PEEK 부품은 CF-에폭시의 311 MPa에 비해 425 MPa의 인장 강도를 발휘하며, 더 높은 연속 사용 온도에도 견딥니다. 이러한 변화는 항공기 주익에서 열경화성 수지를 대체하기에는 아직 한참 모자라지만, 부품당 비용이 재료 선정에 결정적인 영향을 미치는 2차 구조나 자동차 부품 등 폭넓은 분야에서 활용될 수 있게 해줍니다.

지역별 분석

아시아태평양은 2025년에 탄소섬유 강화 플라스틱 시장의 42.05%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 8.43%로 가장 높은 성장세를 보일 전망입니다. 중국에서만 해도 풍력 발전, 전기차, 수소 인프라 프로젝트에 힘입어 2023년에는 약 6만 9,000톤의 복합재료를 소비했습니다. 그러나 T1000급 섬유공급 부족이 여전히 지속되고 있으며, 수출 규제로 인한 역풍이 항공우주 분야의 성장세를 둔화시킬 가능성이 있습니다.

북미는 항공우주 프로그램과 수소 모빌리티 시범 사업을 활용하고 있습니다. 보잉의 미수주 물량에 더해, 신생 eVTOL 기업들이 견고한 수요 기반을 뒷받침하고 있으며, 재활용 플랜트 및 대체 전구체에 대한 투자를 통해 국내 공급 강화가 추진되고 있습니다. 헥셀사는 물류상의 어려움이 있었음에도 불구하고, 2024년 1분기 상업용 항공우주 부문 매출이 5.2% 증가했다고 보고했습니다.

유럽은 지속가능성 분야에서 선도적인 역할을 하고 있습니다. 에어버스의 열가소성 수지 관련 노력과 EU의 재활용 규제가 순환형 경제의 발전을 뒷받침하고 있습니다. 또한, 이 지역에서는 모두 탄소섬유를 대량으로 사용하는 수소 탱크 제조와 해상 풍력 발전에 대한 투자도 진행되고 있습니다. 솔베이와 보잉 간의 장기 공급 계약은 유럽 생산자들이 지역 내 부가가치 확보를 강화해 나가는 가운데에도 대서양을 가로지르는 협력 관계가 지속되고 있음을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the carbon fiber reinforced plastic market size was valued at USD 21.18 billion in 2025 and estimated to grow from USD 22.72 billion in 2026 to reach USD 32.25 billion by 2031, at a CAGR of 7.26% during the forecast period (2026-2031).

This report Segments the Industry by Resin Type (Thermoset CFRP and Thermoplastic CFRP), Raw-Material Precursor (PAN, Pitch, Rayon) and Others (Lignin-Based, Etc. ), End-User Industry (Aerospace, Automotive, Wind Power Industry, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD)..

Global Carbon Fiber Reinforced Plastic (CFRP) Market Trends and Insights

Surge in Commercial Aircraft Backlog

The commercial aviation sector's unprecedented order backlog exceeding 15,000 aircraft creates sustained demand for carbon fiber composites. Air-framer push for thermoplastic secondary structures aims at faster build rates without sacrificing performance. Suppliers respond by qualifying multiple fiber sources to diversify risk and assure uninterrupted deliveries.

Electrification Accelerating CFRP Battery Enclosures

Electric-vehicle makers now specify carbon-fiber battery housings that cut enclosure weight by up to 91% versus aluminum. Each kilogram saved can be redeployed as extra battery capacity, extending range without enlarging the vehicle footprint. Flame-retardant thermoplastics and integrated thermal-management layers help composites meet strict safety codes, moving the carbon fiber reinforced plastic market deeper into high-volume automotive production.

High Cost of Aerospace-grade PAN Precursor

Aerospace-qualified polyacrylonitrile (PAN) sells for USD 33-66 per kg, limiting crossover into cost-sensitive sectors. Few suppliers meet stringent cleanliness and consistency norms, creating supply concentration risk. Water-soluble precursor research promises cost cuts, yet commercial validation in conservative aerospace supply chains will take time.

Other drivers and restraints analyzed in the detailed report include:

- Mega-blade Wind Turbines (>100 m) Adopting CFRP Spar Caps

- Hydrogen Mobility Pressure-vessel Build-out

- Industrial-grade Fibre Capacity Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thermoset systems commanded 72.15% of the carbon fiber reinforced plastic market share in 2025, cemented by aerospace's long reliance on epoxy prepregs. Yet thermoplastic solutions record an 8.02% CAGR through 2031, reflecting rising needs for fast processing and recyclability. Airbus's thermoplastic fuselage panels show cycle-time savings compatible with monthly production rates above 70 airframes, while automotive suppliers cut stamping cycles to seconds.

Thermoplastic composites also expand the carbon fiber reinforced plastic market size in mobility, eVTOL, and hydrogen storage because they can be welded or re-melted during assembly. CF-PEEK parts deliver tensile strength of 425 MPa versus 311 MPa for CF-epoxy, together with higher continuous-use temperatures. The shift is far from replacing thermosets in primary aircraft wings, but it unlocks a broad set of secondary structures and automotive parts where cost per component dictates material choice.

Complete Report Scope:

- By Resin Type

- Thermoset Carbon Fiber Reinforced Plastics (CFRP)

- Thermoplastic Carbon Fiber Reinforced Plastics (CFRP)

- By Raw-Material Precursor

- Polyacrylonitrile (PAN)

- Pitch

- Rayon

- Others (Lignin-based, Recycled CF (Carbon Fiber))

- By End-user Industry

- Aerospace

- Automotive

- Wind Power Industry

- Sports and Leisure

- Building and Construction

- Other End-user Industry

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle East and Africa

- North America

Geography Analysis

Asia-Pacific captured 42.05% of the carbon fiber reinforced plastic market in 2025 and exhibits the highest 8.43% CAGR through 2031. China alone consumed about 69,000 t of composites in 2023, propelled by wind, EV, and hydrogen infrastructure projects. Yet lingering gaps in T1000-level fibers and export-control headwinds could temper its aerospace momentum.

North America leverages aerospace programs and hydrogen-mobility pilots. Boeing's backlog plus emerging eVTOL firms sustain a robust demand base, while investments in recycling plants and alternative precursors aim to fortify domestic supply. Hexcel reported 5.2% commercial-aerospace revenue growth in Q1 2024 despite logistics challenges.

Europe anchors sustainability leadership. Airbus's thermoplastic initiatives and EU recycling regulations spur circular-economy advances. The region also channels investment into hydrogen tank manufacturing and offshore wind, both heavy carbon-fiber users. Solvay's long-term supply deal with Boeing underlines transatlantic collaboration even as European producers tighten local value retention.

- Toray Industries Inc.

- Hexcel Corporation

- SGL Carbon

- Mitsubishi Chemical Corporation

- Teijin Limited

- Solvay

- DowAksa

- Formosa Plastics Corporation, U.S.A.

- Gurit Services AG

- TPI Composites

- HS HYOSUNG ADVANCED MATERIALS

- Nippon Graphite Fiber Co., Ltd.

- Rochling

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in commercial aircraft backlog

- 4.2.2 Electrification accelerating Carbon Fiber Reinforced Plastics (CFRP) battery enclosures

- 4.2.3 Mega-blade wind turbines (less than 100 m) adopting Carbon Fiber Reinforced Plastics (CFRP) spar caps

- 4.2.4 Hydrogen mobility pressure-vessel build-out

- 4.2.5 eVTOL & urban-air-mobility platforms favouring thermoplastic CFRP

- 4.2.6 Closed-loop recycling unlocking low-cost recycled Carbon Fiber (rCF)

- 4.3 Market Restraints

- 4.3.1 High cost of aerospace-grade Polyacrylonitrile (PAN) precursor

- 4.3.2 Industrial-grade fibre capacity bottlenecks

- 4.3.3 Export controls on high-modulus fibre

- 4.3.4 Immature end-of-life recycling infrastructure

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Thermoset Carbon Fiber Reinforced Plastics (CFRP)

- 5.1.2 Thermoplastic Carbon Fiber Reinforced Plastics (CFRP)

- 5.2 By Raw-Material Precursor

- 5.2.1 Polyacrylonitrile (PAN)

- 5.2.2 Pitch

- 5.2.3 Rayon

- 5.2.4 Others (Lignin-based, Recycled CF (Carbon Fiber))

- 5.3 By End-user Industry

- 5.3.1 Aerospace

- 5.3.2 Automotive

- 5.3.3 Wind Power Industry

- 5.3.4 Sports and Leisure

- 5.3.5 Building and Construction

- 5.3.6 Other End-user Industry

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 South Korea

- 5.4.4.4 India

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/ Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Toray Industries Inc.

- 6.4.2 Hexcel Corporation

- 6.4.3 SGL Carbon

- 6.4.4 Mitsubishi Chemical Corporation

- 6.4.5 Teijin Limited

- 6.4.6 Solvay

- 6.4.7 DowAksa

- 6.4.8 Formosa Plastics Corporation, U.S.A.

- 6.4.9 Gurit Services AG

- 6.4.10 TPI Composites

- 6.4.11 HS HYOSUNG ADVANCED MATERIALS

- 6.4.12 Nippon Graphite Fiber Co., Ltd.

- 6.4.13 Rochling

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Introduction of Carbon Nanomaterials in Carbon Fiber Reinforced Plastics (CFRP)