|

시장보고서

상품코드

2073472

바이오 바닐린 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Bio Vanillin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

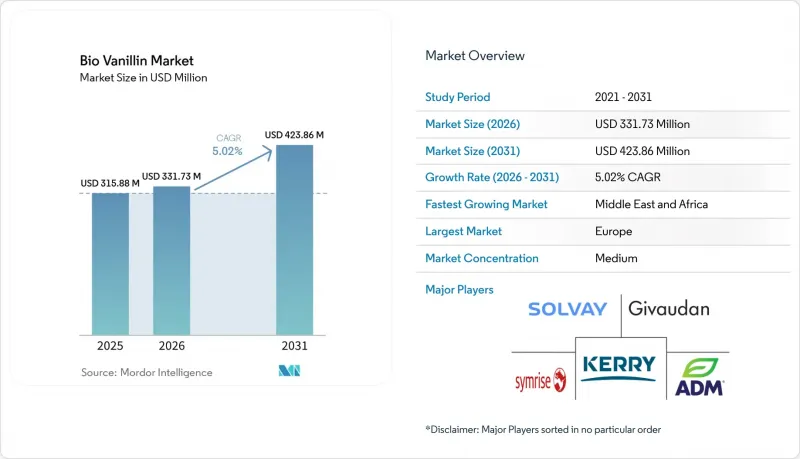

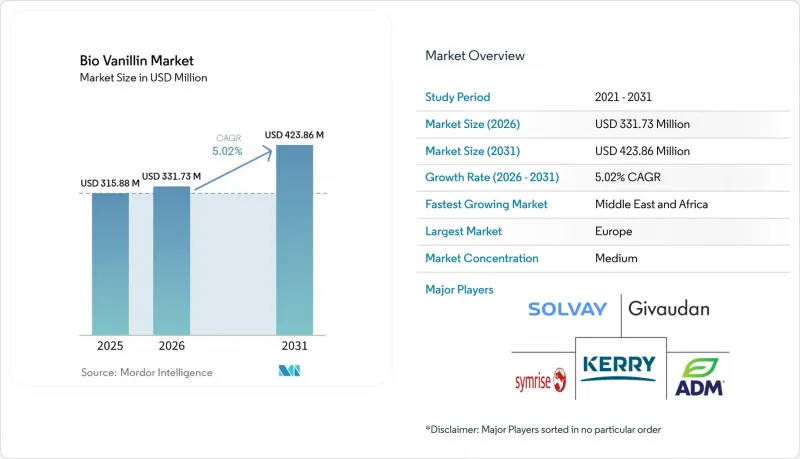

Mordor Intelligence에 의하면, 바이오 바닐린 시장 규모는 2025년 3억 1,588만 달러로 평가되었습니다. 2026년에는 3억 3,173만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 5.02%로 성장을 지속하여, 2031년에는 4억 2,386만 달러에 이를 것으로 예측됩니다.

본 보고서는 형태(분말, 액체), 순도 등급(식품 등급, 의약품 등급, 향료 등급), 용도(식품 및 음료, 의약품, 향료·퍼스널케어) 및 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 바이오 바닐린 시장 동향 및 분석

식품 및 음료 부문에서 지속가능성을 중시하는 수요

식품 및 음료 업계의 지속가능성 노력은 바닐린 조달 전략을 근본적으로 변화시키고 있으며, 주요 제조업체들은 측정 가능한 환경적 이점을 보여주는 바이오 유래 대체재를 점점 더 우선적으로 선택하고 있습니다. 보레가드사의 노르웨이 전나무를 원료로 한 목재 유래 바닐린 생산은 석유 유래 바닐린에 비해 CO2 배출량을 90% 감축하고 있으며, 기업의 환경 보호 노력과 조화를 이루는 설득력 있는 지속가능성 기준을 확립하고 있습니다. 지속가능성에 대한 요구는 탄소 발자국 고려에 그치지 않고, 물 사용량, 폐기물 발생량, 재생 가능 자원 이용에까지 미치고 있으며, 종합적인 환경 관리를 추구하는 기업들에게 바이오 바닐린은 전략적 원료로서의 입지를 확고히 하고 있습니다.

"천연" 표시에 관한 규제 관련 지원

주요 시장의 규제 체계는 "천연"이라는 용어를 엄격하게 정의하고, 석유 유래의 합성 대체품을 배제함으로써, 생명공학을 통해 생산된 바닐린에 명확한 경쟁 우위를 부여하고 있습니다. 미국 주류·담배 세무청(TTB)은 특정 생명공학 공정을 통해 얻은 바닐린을 천연 바닐린으로 명시적으로 인정하고 있으며, 이에 따라 Advanced Biotech나 Apple Flavors와 같은 기업들은 프리미엄 가격 책정이 가능한 ‘"천연"로고를 부착하여 자사 제품을 판매할 수 있습니다. 21 CFR 172.510에 근거한 FDA(미국 식품의약국)의 규정에 따르면, 승인된 생명공학 기법을 통해 생산된 경우, 바이오 바닐린을 함유한 천연 향료 물질은 "일반적으로 안전하다고 인정되는(GRAS)"상태를 확인하기 위한 명확한 절차를 제시하고 있습니다. 규제 환경은 투명성과 추적성 요건의 강화 방향으로 진화하고 있으며, 이는 천연 유래 원료와 지속 가능한 생산 방식을 입증할 수 있는 생명공학을 통해 생산된 바닐린에는 명확한 경쟁 우위를 가져다주는 반면, 합성 대체재에게는 또 다른 장벽이 되고 있습니다.

높은 생산 비용

생명공학을 통해 생산된 바닐린과 합성 대체품 간의 상당한 비용 차이는 시장 확대에 있어 가장 큰 장벽이 되고 있으며, 상업적 실현 가능성을 확보하기 위해서는 생산의 경제성을 신중하게 최적화해야 합니다. 현재의 생명공학 기반 생산 방식에서는 발효 인프라, 기질 비용, 후공정, 품질 관리 요건과 관련된 고유한 비용 문제를 겪고 있는 반면, 합성 생산 방식에서는 확립된 석유화학 공정을 통해 이러한 문제를 회피하고 있습니다. 천연 바닐린의 가격이 1Kg당 700달러인 반면, 합성 바닐린은 1Kg당 15달러로, 이 46배에 달하는 가격 차이로 인해 시장 침투는 "천연 유래"표시가 충분한 가격 프리미엄을 가져다주는 고급 용도로만 제한되어 있습니다. 이러한 비용상의 문제는 합성 생산 시설에서는 필요하지 않은 전문 설비, 숙련된 인력, 그리고 규제 준수를 위한 인프라가 필요하다는 점으로 인해 더욱 심각해지고 있으며, 신규 시장 진출기업들에게 추가적인 진입 장벽이 되고 있습니다.

부문별 분석

2025년 기준으로, 분말 형태의 바이오 바닐린은 70.73%의 시장 점유율을 차지했습니다. 이는 뛰어난 안정성, 장기 보존성, 정확한 투여량 및 일관된 풍미를 요구하는 다양한 식품 가공 용도에 적합함을 반영한 것입니다. 분말 제품이 시장을 독점하고 있는 이유는 액체 제품에 비해 산화나 흡습의 영향을 덜 받기 때문이며, 장기 보존성이 필요하거나 다양한 환경 조건에서도 일관된 제품 성능을 요구하는 제조업체에게 바람직한 선택지가 되고 있습니다.

액상 바이오 바닐린은 시장 점유율은 작지만, 2031년까지 연평균 성장률(CAGR)이 8.58%로 가장 높은 성장률을 나타낼 것으로 전망됩니다. 이는 즉각적인 용해성과 균일한 분산이 중요한 성능 요인으로 작용하는 음료 제조업체 및 액체 식품 분야 수요 증가에 힘입은 것입니다. 액상 제제는 신속한 풍미 방출과 생체 이용률 향상이 요구되는 용도, 특히 바닐린의 항산화 특성이 단순한 향미 부여 이상의 기능적 이점을 제공하는 의약품 및 영양보조식품 분야에서 주목을 받고 있습니다.

지역별 분석

유럽은 엄격한 천연 향료 규제, 확립된 생명공학 인프라, 그리고 프리미엄 천연 성분을 선호하는 소비자의 기호에 힘입어 2025년에는 32.33%의 점유율로 시장의 주도적 지위를 유지했으며, 이러한 요인들이 바이오 바닐린 도입에 유리한 시장 환경을 조성하고 있습니다. 중동 및 아프리카는 식품 가공 산업의 확대, 천연 원료에 대한 소비자의 인식 제고, 그리고 프리미엄 제품 채택을 뒷받침하는 가처분 소득 증가에 힘입어 2031년까지 연평균 성장률(CAGR) 7.51%로 가장 빠른 성장이 예상됩니다.

북미 시장은 확고한 입지를 갖춘 생명공학 기업, 지원적인 규제 체계, 그리고 식품, 의약품, 퍼스널케어 분야에서 바이오 바닐린의 채택을 촉진하는 클린 라벨 제품에 대한 소비자 수요의 혜택을 누리고 있습니다. 이 지역 시장 발전은 바닐린 생산 능력 확대를 위해 약 1,500만 달러를 투자한 Borregaard와 같은 기업과, 농업 폐기물을 활용해 비용 경쟁력 있는 생산 방식을 개발하고 있는 Spero Renewables와 같은 신생 기업들에 의해 뒷받침되고 있습니다.

아시아태평양 시장은 현재 시장 점유율이 제한적이긴 하지만, 식품 가공 활동의 활성화, 중산층의 확대, 천연 성분에 대한 소비자의 선호 변화 등이 장기적인 시장 역학을 긍정적으로 변화시켜 큰 성장 기회를 내포하고 있습니다. 지역별 다양성은 규제 환경, 소비자 선호도, 산업 발전 수준의 차이를 반영하고 있으며, 이러한 요인들이 각 지역의 바이오 바닐린 시장 침투 및 성장 전략에 영향을 미치고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.07According to Mordor Intelligence, the bio vanillin market size is expected to grow from USD 315.88 million in 2025 to USD 331.73 million in 2026 and is forecast to reach USD 423.86 million by 2031 at 5.02% CAGR over 2026-2031.

This report is Segmented by Form (Powder, and Liquid), Purity Grade (Food Grade, Pharma Grade, and Fragrance Grade), Application (Food and Beverage, Pharmaceutical, and Fragrance and Personal Care), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Bio Vanillin Market Trends and Insights

Sustainability-Driven Demand from the Food and Beverage Sector

The food and beverage industry's commitment to sustainability is fundamentally reshaping vanillin procurement strategies, with major manufacturers increasingly prioritizing bio-based alternatives that demonstrate measurable environmental benefits. Borregaard's wood-based vanillin production from Norway Spruce achieves a 90% reduction in CO2 emissions compared to oil-based vanillin, establishing a compelling sustainability benchmark that resonates with corporate environmental commitments. The sustainability imperative extends beyond carbon footprint considerations to encompass water usage, waste generation, and renewable resource utilization, positioning bio vanillin as a strategic ingredient for companies pursuing comprehensive environmental stewardship.

Regulatory Support for "Natural" Label Claims

Regulatory frameworks across major markets are creating distinct competitive advantages for biotechnologically produced vanillin through precise definitions of "natural" that exclude petroleum-derived synthetic alternatives. The U.S. Alcohol and Tobacco Tax and Trade Bureau explicitly recognizes vanillin derived from specific biotechnological processes as natural vanillin, allowing companies like Advanced Biotech and Apple Flavors to market their products with natural labeling claims that command premium pricing. FDA (Food and Drug Administration) regulations under 21 CFR 172.510 provide clear pathways for natural flavoring substances, including bio vanillin, to achieve Generally Recognized as Safe (GRAS) status when produced through approved biotechnological methods. The regulatory environment is evolving toward greater transparency and traceability requirements, creating additional barriers for synthetic alternatives while providing clear competitive advantages for biotechnologically produced vanillin that can demonstrate natural sourcing and sustainable production methods.

High Production Cost

The substantial cost differential between biotechnologically produced vanillin and synthetic alternatives represents the most significant barrier to market expansion, with production economics requiring careful optimization to achieve commercial viability. Current biotechnological production methods face inherent cost challenges related to fermentation infrastructure, substrate costs, downstream processing, and quality control requirements that synthetic production avoids through established petrochemical pathways. The price gap between natural vanillin at USD 700 per kilogram and synthetic vanillin at USD 15 per kilogram creates a 46-fold cost differential that limits market penetration to premium applications where natural labeling commands sufficient price premiums. The cost challenge is compounded by the need for specialized equipment, skilled personnel, and regulatory compliance infrastructure that synthetic production facilities do not require, creating additional barriers to entry for new market participants.

Other drivers and restraints analyzed in the detailed report include:

- Growing Consumer Preference for Plant-Based and Vegan Products

- Technological Advancements in Biotechnological Production

- Lack of Awareness in Developing Countries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Powder form bio vanillin commands 70.73% market share in 2025, reflecting its superior stability characteristics, extended shelf life, and compatibility with diverse food processing applications that require precise dosing and consistent flavor delivery. The powder segment's dominance stems from its reduced susceptibility to oxidation and moisture absorption compared to liquid alternatives, making it the preferred choice for manufacturers requiring long-term storage capabilities and consistent product performance across varying environmental conditions.

Liquid bio vanillin, despite representing a smaller market share, is projected to achieve the fastest growth at 8.58% CAGR through 2031, driven by increasing demand from beverage manufacturers and liquid food applications where immediate solubility and homogeneous distribution are critical performance factors. Liquid formulations are gaining traction in applications requiring rapid flavor release and enhanced bioavailability, particularly in pharmaceutical and nutraceutical products where vanillin's antioxidant properties provide functional benefits beyond flavoring.

Complete Report Scope:

- By Form

- Powder

- Liquid

- By Purity Grade

- Food Grade

- Pharma Grade

- Fragrance Grade

- By Application

- Food and Beverages

- Ice Cream

- Baked Goods

- Beverages

- Chocolate & Confectionery

- Other Food and Beverage Applications

- Pharmaceutical

- Fragrance and Personal Care

- Food and Beverages

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Geography Analysis

Europe maintains market leadership with 32.33% share in 2025, supported by stringent natural flavoring regulations, established biotechnology infrastructure, and consumer preferences for premium natural ingredients that create favorable market conditions for bio vanillin adoption. The Middle East and Africa region is positioned for the fastest growth at 7.51% CAGR through 2031, driven by expanding food processing industries, increasing consumer awareness of natural ingredients, and growing disposable income that supports premium product adoption.

North American markets benefit from established biotechnology companies, supportive regulatory frameworks, and consumer demand for clean label products that drive bio vanillin adoption across food, pharmaceutical, and personal care applications. The region's market development is supported by companies like Borregaard, which has invested approximately USD 15 million to expand vanillin production capacity, and emerging players like Spero Renewables developing cost-competitive production methods from agricultural waste.

Asia-Pacific markets present significant growth opportunities despite current market share limitations, with increasing food processing activity, growing middle-class populations, and evolving consumer preferences for natural ingredients creating favorable long-term market dynamics. The geographic diversification reflects varying regulatory environments, consumer preferences, and industrial development levels that influence bio vanillin market penetration and growth strategies across different regions.

- Kerry Group plc

- Givaudan SA

- Solvay S.A.

- Symrise AG

- Archer-Daniels-Midland Company

- Borregaard AS

- Europabio

- Advanced Biotech

- BASF SE

- Camlin Fine Sciences Ltd

- International Flavors & Fragrances

- Biosynth Ltd

- Oamic Ingredients USA

- Takasago International Corporation

- Axxence Aromatic GmbH

- Evolva Holding SA

- Ennolys by Lesaffre

- Xi'an Healthful Biotechnology Co.,Ltd

- Jeneil Biotech

- Niranbio Chemical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sustainability-driven demand from the food and beverage sector

- 4.2.2 Regulatory support for natural label claims

- 4.2.3 Growing consumer preference for plant-based and vegan products

- 4.2.4 Technological advancements in biotechnological production

- 4.2.5 Rising import tariffs on synthetic vanillin

- 4.2.6 Expansion of clean label trends in premium products

- 4.3 Market Restraints

- 4.3.1 High production cost

- 4.3.2 Lack of awareness in developing countries

- 4.3.3 Regulatory and labeling compliance costs

- 4.3.4 Competition from alternative natural flavorings

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Form

- 5.1.1 Powder

- 5.1.2 Liquid

- 5.2 By Purity Grade

- 5.2.1 Food Grade

- 5.2.2 Pharma Grade

- 5.2.3 Fragrance Grade

- 5.3 By Application

- 5.3.1 Food and Beverages

- 5.3.1.1 Ice Cream

- 5.3.1.2 Baked Goods

- 5.3.1.3 Beverages

- 5.3.1.4 Chocolate & Confectionery

- 5.3.1.5 Other Food and Beverage Applications

- 5.3.2 Pharmaceutical

- 5.3.3 Fragrance and Personal Care

- 5.3.1 Food and Beverages

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Moves

- 6.2 Market Ranking Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Kerry Group plc

- 6.3.2 Givaudan SA

- 6.3.3 Solvay S.A.

- 6.3.4 Symrise AG

- 6.3.5 Archer-Daniels-Midland Company

- 6.3.6 Borregaard AS

- 6.3.7 Europabio

- 6.3.8 Advanced Biotech

- 6.3.9 BASF SE

- 6.3.10 Camlin Fine Sciences Ltd

- 6.3.11 International Flavors & Fragrances

- 6.3.12 Biosynth Ltd

- 6.3.13 Oamic Ingredients USA

- 6.3.14 Takasago International Corporation

- 6.3.15 Axxence Aromatic GmbH

- 6.3.16 Evolva Holding SA

- 6.3.17 Ennolys by Lesaffre

- 6.3.18 Xi'an Healthful Biotechnology Co.,Ltd

- 6.3.19 Jeneil Biotech

- 6.3.20 Niranbio Chemical