|

시장보고서

상품코드

2073586

ASEAN의 사이버 보안 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)ASEAN Cyber Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

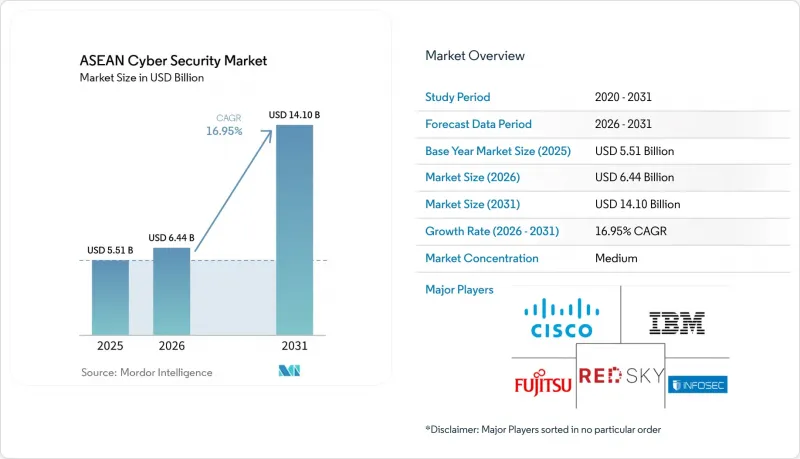

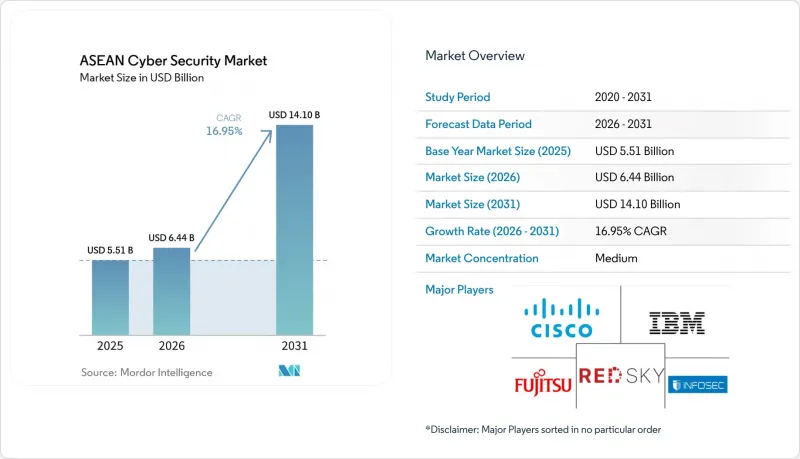

Mordor Intelligence에 의하면, ASEAN의 사이버 보안 시장 규모는 2025년에 55억 1,000만 달러로 평가되었습니다. 2026년 64억 4,000만 달러에서 2031년까지 141억 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 16.95%를 나타낼 전망입니다.

본 보고서에서는 업계를 “제공 형태(솔루션 및 서비스)”, “구축 방식(On-Premise 및 클라우드)”, “최종 사용자 업종(은행, 금융서비스 및 보험(BFSI), 의료, IT 및 통신, 산업·방위, 제조, 소매 및 전자상거래, 에너지 및 유틸리티, 기타), "최종 사용자 기업의 규모(중소기업(SME) 및 대기업)", 그리고 "국가"별로 분류하고 있습니다.

ASEAN의 사이버 보안 시장 동향 및 인사이트

싱가포르가 주도하는 BFSI 부문에서 제로 트러스트 도입 가속화

싱가포르의 각 은행들은 2024년 금융관리청이 기술 위험 지침을 개정한 데 따라 제로 트러스트 도입을 가속화했습니다. 현재 말레이시아와 태국의 금융기관들도 오픈 뱅킹 API, 모바일 지갑, 클라우드 코어를 보호하기 위해 유사한 접근 방식을 채택하고 있습니다. Globe사의 GCash는 연간 거래액 1조 필리핀 페소를 보호하기 위해 사내 사이버 보안 팀을 5배로 확대했습니다. 이는 인력 확충이 아키텍처 변경과 병행하여 진행되고 있음을 보여줍니다. 벤더들은 신원 거버넌스, 마이크로 세분화, 지속적인 인증 분야의 라이선스 판매량 증가로 이익을 얻고 있으며, 서비스 제공업체들은 설계 및 관리형 감지 의무화로 인해 혜택을 보고 있습니다. 규제 당국이 복원력 테스트를 중시하는 가운데, 제로 트러스트는 모범 사례에서 표준으로 자리 잡으며, 아세안(ASEAN) 사이버 보안 시장의 지속적인 지출 증가세를 뒷받침하고 있습니다.

인도네시아의 제조업 및 스마트시티 분야에서 IoT로 인한 공격 표적 영역의 폭발적인 확대

자바섬과 수마트라섬에서 진행되고 있는 인더스트리 4.0 시범 프로젝트에서는 악의적인 네트워크에 대한 내성이 전혀 고려되지 않은 센서, AGV(무인 운반차), 엣지 게이트웨이가 도입되고 있습니다. 바탐에 위치한 얼라이언스 런드리 시스템즈의 5G 대응 생산 라인은 아세안 전역의 프로젝트를 반영하고 있으며, 각 공장에는 수만 개에 달하는 관리 대상 외 엔드포인트가 설치되어 있어 네트워크 세분화, NAC(네트워크 액세스 제어), 이상 분석이 요구되고 있습니다. 현지 시스템 통합사업자들은 전 세계 OEM 기업들과 제휴하여 OT 보안 개선을 추진하고 있는 반면, 보험사들은 보험 인수 전에 자산 발견 감사를 점점 더 강력하게 요구하고 있습니다. 방콕과 호치민시에서 시행되고 있는 이와 유사한 스마트 시티 그리드는 IoT를 중심으로 한 위협 모델링에 대한 지역 전반 수요를 높여, ASEAN의 사이버 보안 시장의 두 자릿수 성장을 뒷받침하고 있습니다.

중소기업의 멀티 클라우드 SecOps에 따른 높은 총 소유 비용

2024년에 65만 9,000건의 공격을 겪었음에도 불구하고, 보안 사고에 대비가 되어 있다고 보고한 베트남 기업은 고작 11%에 불과합니다. AWS, Azure, Google Cloud에 걸쳐 사용되는 전용 도구의 필요성은 라이선스 중복, 복잡한 통합, 그리고 분석가의 업무 부담 급증을 초래하고 있습니다. 교육, 위협 인텔리전스 피드, 연중무휴 24시간 모니터링은 운영 비용을 더욱 증가시켜, 많은 중소기업이 최소한의 대책만 마련할 수밖에 없게 만들고, 아세안(ASEAN) 사이버 보안 시장에서 보안 대책의 격차를 확대시키고 있습니다.

부문별 분석

2025년, 솔루션은 아세안(ASEAN) 사이버 보안 시장 점유율의 54.12%를 차지했으며, 엔드포인트, 네트워크, 클라우드를 통합적으로 제어하는 플랫폼에 대한 수요가 이를 주도했습니다. ID 및 액세스 관리 제품군, 차세대 방화벽, XDR 스택이 초기 구매 주기를 주도하고 있으며, 이는 락인 효과를 창출하여 공급업체와의 계약 갱신을 공고히 하고 있습니다. 기업들이 기술 부족과 지속적인 모니터링 및 맞춤형 규정 준수 매핑이 필요한 규제 감사에 직면함에 따라, 전문 서비스 및 관리형 서비스 시장은 연평균 성장률(CAGR) 18.95%로 확대되고 있습니다. 말레이시아가 2025년까지 2만 5,000명의 사이버 방어 인력을 양성한 것은 이 서비스의 중요성을 여실히 보여주고 있습니다.

조직들이 Tier 1 경보 대응, 퍼플팀을 통한 시뮬레이션, 규정 준수 문서 작성을 외부에 위탁함에 따라, 서비스에 기인한 ASEAN의 사이버 보안 시장 규모는 2031년까지 10억 달러 중반대에 달할 것으로 전망됩니다. 지역의 MSSP(관리형 보안 서비스 제공업체)는 자문, 통합, 운영을 성과 기반 계약에 결합하여 제공하고 있으며, 제조업 및 유틸리티 등 디지털화가 뒤처진 분야의 도입을 가속화하고 있습니다.

2025년, 클라우드 도입은 아세안(ASEAN) 사이버 보안 시장 규모의 57.34%를 차지했으며, 중소기업 및 신규 사업 분야에서 SaaS 도입이 확대됨에 따라 증가했습니다. Prisma Cloud, GuardDuty, Defender for Cloud는 초기 설비 투자(CAPEX) 없이 신속한 위협 감지, 보안 태세 평가 및 자동화된 시정 조치를 가능하게 하므로, 가격에 민감한 경제권에서 매력적인 선택지가 되고 있습니다. 데이터 상주 요건에 얽매여 있는 은행이나 의료 기관에서는 여전히 하이브리드형 참조 아키텍처가 채택되고 있지만, 이러한 기관들조차도 시각화 도구를 멀티클라우드 워크로드까지 확장하고 있습니다.

시프트 레프트 방식의 DevSecOps, 컨테이너 보안, CNAPP 플랫폼이 표준 조달 대상으로 자리 잡으면서, 아세안(ASEAN) 사이버 보안 시장에서는 클라우드 보안 지출이 계속해서 연평균 성장률(CAGR) 19.88%로 성장을 지속하고 있습니다. On-Premise형 어플라이언스의 교체 주기가 5년 이상으로 길어지면서, 클라우드 네이티브 제어 방식으로의 구조적인 전환이 확고해지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 세분화

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.07According to Mordor Intelligence, the ASEAN cybersecurity market size was valued at USD 5.51 billion in 2025 and estimated to grow from USD 6.44 billion in 2026 to reach USD 14.1 billion by 2031, at a CAGR of 16.95% during the forecast period (2026-2031).

This report Segments the Industry Into by Offering (Solutions, and Services), Deployment Mode (On-Premise, and Cloud), End-User Vertical (BFSI, Healthcare, IT and Telecom, Industrial and Defense, Manufacturing, Retail and E-Commerce, Energy and Utilities, Manufacturing, and Others), End-User Enterprise Size (Small and Medium Enterprises (SMEs), and Large Enterprises), and Country.

ASEAN Cyber Security Market Trends and Insights

Intensifying Zero-Trust Adoption in Singapore-led BFSI Sector

Banks in Singapore accelerated zero-trust rollouts after the Monetary Authority updated its technology risk guidelines in 2024. Financial institutions across Malaysia and Thailand now mirror the approach to secure open-banking APIs, mobile wallets and cloud cores. Globe's GCash grew its internal cyber team five-fold to protect PHP 1 trillion in annual transactions, illustrating how headcount expansion parallels architectural change. Vendors gain from higher licence volumes for identity governance, micro-segmentation and continuous authentication, while service providers benefit from design and managed detection mandates. As regulators emphasise resilience tests, zero-trust has moved from best practice to baseline, underpinning sustained spending momentum in the ASEAN cybersecurity market.

Explosive IoT-Inflicted Attack Surface in Indonesian Manufacturing and Smart-Cities

Industry 4.0 pilots across Java and Sumatra add sensors, AGVs and edge gateways that were never hardened for hostile networks. Alliance Laundry Systems' 5G-enabled line in Batam mirrors projects across ASEAN, with each plant hosting tens of thousands of unmanaged endpoints that demand network segmentation, NAC and anomaly analytics. Local system integrators partner global OEMs to retrofit OT-security, while insurers increasingly insist on asset-discovery audits before underwriting. Similar smart-city grids in Bangkok and Ho Chi Minh City amplify the region-wide call for IoT-centric threat modelling, sustaining double-digit growth in the ASEAN cybersecurity market.

High Total-Cost-of-Ownership for Multi-Cloud SecOps in SMEs

Only 11% of Vietnamese firms report incident preparedness despite facing 659,000 attacks in 2024. The need for dedicated tooling across AWS, Azure and Google Cloud drives licence duplication, complex integration and spiraling analyst workloads. Training, threat-intel feeds and 24/7 monitoring further elevate opex, forcing many SMEs to opt for baseline controls, widening the exposure gap inside the ASEAN cybersecurity market.

Other drivers and restraints analyzed in the detailed report include:

- ASEAN Government-Funded SOC and CERT Investments

- Surging E-Commerce Data-Leak Fines Under PDPA

- Fragmented Data-Protection Regulations Across 10 Member States

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions captured 54.12% of ASEAN cybersecurity market share in 2025, anchored by demand for integrated platforms that unify endpoint, network and cloud controls. Identity-and-access suites, next-generation firewalls and XDR stacks dominate initial purchase cycles, creating lock-in effects that fortify vendor renewals. Professional and managed services rise at 18.95% CAGR as enterprises confront skills shortages and regulatory audits that require continuous monitoring and bespoke compliance mapping. Malaysia's plan to train 25,000 cyber defenders by 2025 underscores the services imperative.

The ASEAN cybersecurity market size attributable to services will likely reach mid-single-billion-dollar levels by 2031 as organizations outsource tier-one alert handling, purple-team simulations and compliance documentation. Regional MSSPs bundle advisory, integration and operations in outcome-based contracts, accelerating adoption among late-digitizing sectors such as manufacturing and utilities.

Cloud deployments held 57.34% of the ASEAN cybersecurity market size in 2025, rising on the back of SaaS adoption among SMEs and greenfield ventures. Prisma Cloud, GuardDuty and Defender for Cloud enable rapid threat-hunting, posture scoring and automated remediation without upfront capex, making them attractive in price-sensitive economies. Hybrid reference architecture remains for banks and healthcare groups bound by data-residency mandates, yet even these institutions extend visibility tooling to multi-cloud workloads.

The ASEAN cybersecurity market continues to record 19.88% CAGR in cloud-security spend as shift-left DevSecOps, container security and CNAPP platforms become default procurement. On-premise appliance refresh cycles stretch to five years or more, solidifying the structural tilt toward cloud-native controls.

Complete Report Scope:

- By Offering

- Solutions

- Application Security

- Cloud Security

- Data Security

- Identity and Access Management

- Infrastructure Protection

- Integrated Risk Management

- Network Security Equipment

- Endpoint Security

- Other Services

- Services

- Professional Services

- Managed Services

- Solutions

- By Deployment Mode

- On-Premise

- Cloud

- By End-User Vertical

- BFSI

- Healthcare

- IT and Telecom

- Industrial and Defense

- Manufacturing

- Retail and E-commerce

- Energy and Utilities

- Manufacturing

- Others

- By End-User Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Country

- Singapore

- Malaysia

- Thailand

- Indonesia

- Philippines

- Vietnam

- Rest of ASEAN (Brunei, Cambodia, Laos, Myanmar)

List of Companies Covered in this Report:

- Cisco Systems Inc.

- Fortinet Inc.

- Palo Alto Networks Inc.

- Trend Micro Incorporated

- IBM Corporation

- Check Point Software Technologies Ltd.

- Huawei Technologies Co. Ltd.

- Microsoft Corp.

- Kaspersky Lab

- Dell Technologies Inc.

- Broadcom Inc. (Symantec Enterprise)

- Splunk Inc.

- Sophos Ltd.

- Darktrace plc

- Zscaler Inc.

- F5 Inc.

- CrowdStrike Holdings Inc.

- Imperva Inc.

- Cybereason Inc.

- SEC Consult (Atos Group)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Intensifying Zero-Trust Adoption in Singapore-led BFSI Sector

- 4.2.2 Explosive IoT-inflicted Attack Surface in Indonesian Manufacturing & Smart-Cities

- 4.2.3 ASEAN Government-Funded SOC & CERT Investments

- 4.2.4 Rapid SASE Roll-outs Among Thai Telcos to Monetise 5G Enterprise Edge

- 4.2.5 Growing Cyber-Insurance Mandates for Listed Firms on SGX & Bursa Malaysia

- 4.2.6 Surging e-Commerce Data-Leak Fines under PDPA (Thailand & Philippines)

- 4.3 Market Restraints

- 4.3.1 High Total-Cost-of-Ownership for Multi-Cloud SecOps in SMEs

- 4.3.2 Fragmented Data-Protection Regulations Across 10 Member States

- 4.3.3 Shortage of GIAC-Certified Professionals in Emerging CLMV Cluster

- 4.3.4 Low Cyber-Resilience Culture within Family-Owned Conglomerates

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Key Use Cases and Case Studies

- 4.9 Impact on Macroeconomic Factors of the Market

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.1.1 Application Security

- 5.1.1.2 Cloud Security

- 5.1.1.3 Data Security

- 5.1.1.4 Identity and Access Management

- 5.1.1.5 Infrastructure Protection

- 5.1.1.6 Integrated Risk Management

- 5.1.1.7 Network Security Equipment

- 5.1.1.8 Endpoint Security

- 5.1.1.9 Other Services

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By End-User Vertical

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 IT and Telecom

- 5.3.4 Industrial and Defense

- 5.3.5 Manufacturing

- 5.3.6 Retail and E-commerce

- 5.3.7 Energy and Utilities

- 5.3.8 Manufacturing

- 5.3.9 Others

- 5.4 By End-User Enterprise Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

- 5.5 By Country

- 5.5.1 Singapore

- 5.5.2 Malaysia

- 5.5.3 Thailand

- 5.5.4 Indonesia

- 5.5.5 Philippines

- 5.5.6 Vietnam

- 5.5.7 Rest of ASEAN (Brunei, Cambodia, Laos, Myanmar)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Cisco Systems Inc.

- 6.4.2 Fortinet Inc.

- 6.4.3 Palo Alto Networks Inc.

- 6.4.4 Trend Micro Incorporated

- 6.4.5 IBM Corporation

- 6.4.6 Check Point Software Technologies Ltd.

- 6.4.7 Huawei Technologies Co. Ltd.

- 6.4.8 Microsoft Corp.

- 6.4.9 Kaspersky Lab

- 6.4.10 Dell Technologies Inc.

- 6.4.11 Broadcom Inc. (Symantec Enterprise)

- 6.4.12 Splunk Inc.

- 6.4.13 Sophos Ltd.

- 6.4.14 Darktrace plc

- 6.4.15 Zscaler Inc.

- 6.4.16 F5 Inc.

- 6.4.17 CrowdStrike Holdings Inc.

- 6.4.18 Imperva Inc.

- 6.4.19 Cybereason Inc.

- 6.4.20 SEC Consult (Atos Group)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment