|

시장보고서

상품코드

2073629

북미의 배터리 관리 시스템 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)North America Battery Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

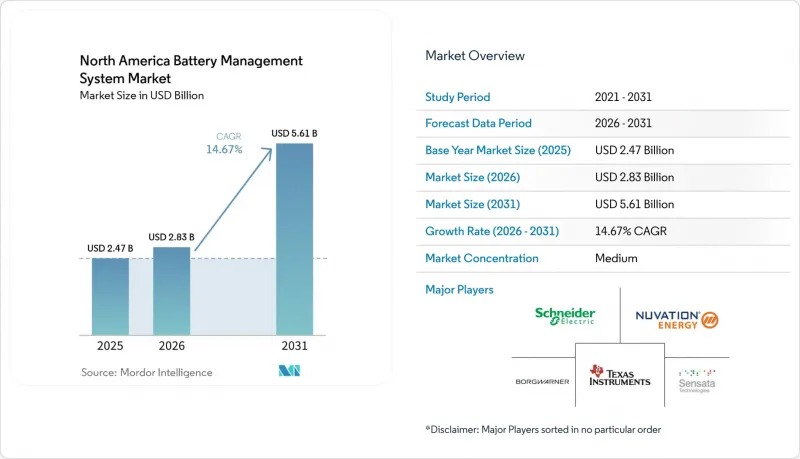

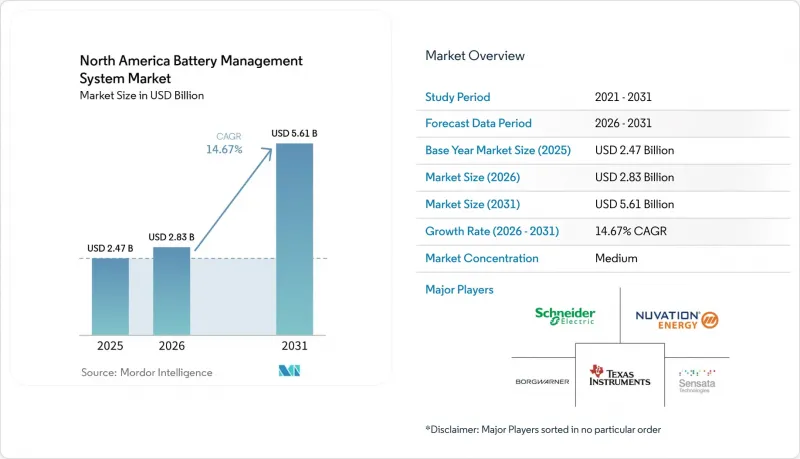

Mordor Intelligence에 의하면, 북미 배터리 관리 시스템(BMS) 시장 규모는 2025년 24억 7,000만 달러, 2026년 28억 3,000만 달러에서 2031년까지 56억 1,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 14.67%를 나타낼 전망입니다.

본 보고서는 배터리 유형(리튬이온, 납산, 니켈, 플로우, 전고체), 토폴로지(집중형, 분산형, 모듈형, 하이브리드형), 구성 요소(하드웨어, 소프트웨어), 전압(저전압, 중전압, 고전압), 용도(자동차, 고정형 에너지 저장, 가정용 전자기기, 산업용/통신용 UPS 등), 지역(미국, 캐나다, 멕시코)별로 분류되어 있습니다. 예측치는 금액(달러)으로 표시되어 있습니다.

북미 배터리 관리 시스템 시장 동향 및 인사이트

전기차 보급 가속화와 제로 배출 규제

북미 배터리 관리 시스템 시장에서 전기차 정책은 직접적인 판매 압박에서 구매 지원 및 인프라 구축으로 점차 전환되고 있습니다. 캐나다는 2026년 2월, 최대 5,000캐나다달러(3,600미국달러)의 전기차 구매 인센티브를 부활시켰으며, 이 결정과 함께 충전 인프라 구축에 15억 캐나다달러(11억 미국달러)를 투자했습니다. 이러한 수요 견인은 일반적으로 차량 교체 주기를 더욱 안정화시켜, 장기적인 BMS의 지속적인 수요를 뒷받침하게 됩니다. 미국에서는 차량의 부품 구성에 연동된 관세 정책도 자동차 제조업체들이 전기차 플랫폼 및 배터리 팩 조립의 현지화를 더욱 촉진하도록 유도하고 있습니다. 이러한 시너지 효과로 인해 북미 배터리 관리 시스템 시장에서 전기차 도입 대수가 증가함에 따라, 정밀 모니터링, 열 관리, 보증 분석의 대상이 되는 차량군이 확대되고 있습니다.

연방 및 주 정부의 에너지 저장 인센티브

에너지 저장에 대한 인센티브는 북미 배터리 관리 시스템 시장에서 여전히 가장 확실한 성장 동력 중 하나입니다. 2026년에 착공하는 프로젝트는 국내 조달 비율 및 근로 조건이 충족될 경우, 최대 50%의 투자 세액 공제 대상이 됩니다. 또한, FEOC(외국 기업에 대한 지급) 회수 규정에 따라 조달 결정 시 더욱 신중한 접근이 요구되고 있습니다. 이는 금지된 외국 기업에 대한 지급이 자산의 사용 연수에 걸쳐 당초의 세제상 우대 조치를 위태롭게 할 가능성이 있기 때문입니다. 이로 인해 UL 1973 인증을 획득한 G5 플랫폼을 미국 및 캐나다에서 제조하고 있는 Nuvation Energy와 같은 국내 공급업체들의 입지가 강화되고 있습니다. 또한, 캐나다 주 정부의 프로그램 역시 계량기 뒤편 분야 수요를 확대하고 있으며, 북미 배터리 관리 시스템 시장의 조달 결정에 있어 UL 1973 및 UL 9540 준수 여부는 여전히 중요한 요소로 작용하고 있습니다.

과열로 인한 안전 리콜

안전상의 리콜은 전기차 보급에 단기적인 평판상의 압박을 주는 한편, 북미 배터리 관리 시스템 시장에서 보다 강력한 제어 로직에 대한 수요를 높이고 있습니다. 2025년 10월, 리콜 번호 25V655에 따라 미국에서 1만 9,077대의 닛산 리프가 리콜 대상이 되었습니다. 이는 레벨 3 충전 중 발생하는 급격한 과열 위험이 리튬 침전물 및 과충전 상태에서의 제어 불량과 관련이 있었기 때문입니다. 이러한 현상은 OEM이나 공급업체가 센싱, 열 모델링 및 검증에 대한 투자를 확대하도록 유도하는 경우가 많습니다. 단기적인 문제로는 리콜 관련 뉴스가 소비자들의 구매 의욕을 위축시켜 신차에 해당 기능이 탑재되는 속도를 늦출 가능성이 있다는 점입니다. 또한, ISO 26262 및 UL 2580 규격 준수는 비용과 개발 기간 증가로 이어져, 중소규모의 신규 진출기업들에게는 시장 진입이 더욱 어려워지고 있습니다.

부문별 분석

2025년, 리튬 이온 배터리는 배터리 유형별 부문에서 68.4%를 차지하며, 북미 배터리 관리 시스템 시장의 현재 수요에서 중심적인 위치를 유지했습니다. 이러한 위상은 전기차 플랫폼의 표준화, 성숙한 공급망, 그리고 리튬 이온의 거동을 바탕으로 이미 학습된 소프트웨어 모델을 반영한 것입니다. 또한, 이미 도입된 시스템의 경우에도 액체 전해질 셀용 충전 상태(SOC), 밸런스 제어, 열 거동 모델 분야에서 실적이 있는 공급업체가 유리한 입장에 있습니다. 이러한 장점 덕분에, 조달 규정이나 새로운 화학 성분이 개발 계획에 변화를 가져오기 시작하고 있음에도 불구하고, 단기적으로는 리튬 이온 배터리가 자동차 및 에너지 저장 분야에서 지배적인 위치를 유지할 것으로 전망됩니다.

고체 배터리용 배터리 관리 시스템은 2031년까지 연평균 성장률(CAGR) 31.8%를 나타낼 것으로 예측되며, 이는 북미 배터리 관리 시스템 시장에서 가장 빠르게 진행될 배터리 유형의 전환이 될 것입니다. 고체 전해질에는 다른 감지 기법이 필요하며, 기존의 쿨롱 계수법이나 개방 회로 전압법으로는 이러한 저항 프로파일에 대한 신뢰성이 낮기 때문에 각 공급업체들은 일찍부터 시장 진출을 추진하고 있습니다. 납축전지, 니켈계 전지, 흐름 전지는 산업용 UPS, 하이브리드 파워트레인, 수 시간에 걸친 전력 저장 등 여전히 제한적인 용도로 사용되고 있지만, 플랫폼으로서의 성장세는 고체 전지만큼 강하지는 않습니다. IEC 62619 및 ISO 26262에 기반한 조기 알고리즘 인증은 인증 비용을 증가시키는 한편, 고체 배터리 프로그램이 양산 단계로 넘어갈 때 공급업체에게 더 견고한 전환 장벽이 될 것입니다.

분산형 토폴로지는 2025년에 이 부문의 39.3%를 차지하고, 연평균 성장률(CAGR) 21.1%로 성장할 것으로 전망됩니다. 이는 북미 배터리 관리 시스템 시장의 주요 설계 사례 중에서는 이례적인 일입니다. 전력 회사는 이 아키텍처가 고장의 확산을 억제하고 모듈식 확장을 지원하기 때문에 이를 선호합니다. 구매자들이 시스템의 격리성, 복원력 및 장애 발생 시 부분적인 가동 시간을 더욱 중요하게 여기게 됨에 따라, 이러한 경향은 더욱 강해지고 있습니다. 또한, 이 설계는 단일 고장이 고가의 설비에 영향을 미칠 수 있는 대규모 에너지 저장 시설에서 보험 및 운영상의 위험을 줄이는 데에도 도움이 됩니다.

집중형 토폴로지는 설치 면적이 작고, 차량 안전 규정에 따른 형식 인증 절차가 간소하기 때문에 여전히 많은 자동차 프로그램에 적합합니다. 모듈식 시스템은 800V 전기차 배터리 팩이나 재사용된 에너지 저장 시스템에서 이용 사례에 따라 채널 수를 보다 효율적으로 조정할 수 있기 때문에 보급이 확대되고 있습니다. 보그워너의 모듈형 BMS 플랫폼은 자동차 부품 공급업체들이 그 유연성을 승용차 및 상용차 프로그램에 걸쳐 적용되는 크로스 플랫폼 경쟁력으로 전환하고 있음을 보여줍니다. 또한, 동일한 설비에서 집중 제어를 통한 저비용과 분산형 센싱을 통한 내장애성을 동시에 실현하고자 하는 고객의 요구에 부응하는 하이브리드 설계도 등장하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the north america battery management system market size is projected to expand from USD 2.47 billion in 2025 and USD 2.83 billion in 2026 to USD 5.61 billion by 2031, registering a CAGR of 14.67% between 2026 and 2031.

This report is Segmented by Battery Type (Li-Ion, Lead-Acid, Nickel, Flow, Solid-State), Topology (Centralized, Distributed, Modular, Hybrid), Component (Hardware, Software), Voltage (Low, Medium, High), Application (Automotive, Stationary Storage, Consumer Electronics, Industrial/Telecom UPS, and More), Geography (United States, Canada, Mexico). Forecasts are in Terms of Value (USD).

North America Battery Management System Market Trends and Insights

Accelerating EV Penetration & Zero-Emission Mandates

EV policy in the North America battery management system market is moving from direct sales pressure toward purchase support and infrastructure buildout. Canada reinstated EV purchase incentives of up to CAD 5,000 (USD 3,600) in February 2026 and paired that decision with CAD 1.5 billion (USD 1.1 billion) for charging infrastructure. This kind of demand pull usually produces steadier vehicle replacement cycles, which supports repeat BMS demand over a longer period. In the United States, tariffs tied to vehicle content are also pushing automakers to localize more EV platforms and pack assembly. The combined effect is a larger installed EV base and a wider addressable fleet for advanced monitoring, thermal management, and warranty analytics in the North America battery management system market.

Federal/Provincial Energy-Storage Incentives

Energy-storage incentives remain one of the clearest growth supports for the North America battery management system market. Projects that begin construction in 2026 can qualify for investment tax credits of up to 50% when domestic content and labor conditions are met. FEOC recapture rules also make sourcing decisions more sensitive because payments to prohibited foreign entities can jeopardize the original tax benefit over the life of the asset. That is improving the position of domestic suppliers such as Nuvation Energy, whose UL 1973-certified G5 platform is manufactured in the United States and Canada. Provincial programs in Canada are also building behind-the-meter demand and keeping UL 1973 and UL 9540 compliance at the center of procurement decisions in the North America battery management system market.

Safety Recalls From Thermal Runaway

Safety recalls are raising demand for stronger control logic in the North America battery management system market, even though they also create short-term reputational pressure on EV adoption. In October 2025, recall number 25V655 covered 19,077 Nissan LEAF units in the United States because rapid overheating risk during Level 3 charging was linked to lithium deposits and weak control under high charge conditions. Events like this often push OEMs and suppliers to spend more on sensing, thermal models, and validation. The near-term problem is that recall headlines can slow consumer adoption and reduce the pace of new vehicle installations. Compliance with ISO 26262 and UL 2580 also adds cost and engineering time, which makes entry harder for smaller participants.

Other drivers and restraints analyzed in the detailed report include:

- Declining Li-Ion Battery Costs

- Utility-Led V2G Pilots Need Advanced BMS

- Dependence On Imported Cells

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion held 68.4% of the battery type segment in 2025, which kept it at the center of current demand in the North America battery management system market. That position reflects EV platform standardization, mature supply chains, and software models already trained around lithium-ion behavior. The installed base also favors suppliers with proven state-of-charge, balancing, and thermal models for liquid-electrolyte cells. These advantages should keep lithium-ion dominant in near-term vehicle and storage programs, even as sourcing rules and new chemistries begin to change development plans.

Solid-state battery management systems are forecast to grow at a 31.8% CAGR through 2031, making this the fastest-moving battery type shift in the North America battery management system market. Suppliers are engaging early because solid electrolytes need different sensing approaches, and conventional Coulomb-counting and open-circuit voltage methods are less reliable against these resistance profiles. Lead-acid, nickel-based, and flow batteries still serve narrower uses such as industrial UPS, hybrid powertrains, and multi-hour storage, but they do not carry the same platform momentum. Early algorithm certification under IEC 62619 and ISO 26262 raises qualification cost, yet it also creates a stronger switching barrier for suppliers once solid-state programs move into scaled production.

Distributed topology held 39.3% of the segment in 2025 and is also projected to grow at a 21.1% CAGR, which is unusual for a leading design in the North America battery management system market. Utilities prefer this architecture because it limits fault propagation and supports modular expansion. That preference has strengthened as buyers place more value on system isolation, resilience, and partial uptime during failures. The design also helps reduce insurance and operations exposure on large storage assets where a single fault can affect a high-value installation.

Centralized topology still fits many automotive programs because it offers a compact footprint and a simpler homologation path under vehicle safety rules. Modular systems are gaining ground in 800-volt EV packs and repurposed battery storage because channel counts can be adjusted more efficiently to the use case. BorgWarner's modular BMS platform shows how vehicle suppliers are turning that flexibility into a cross-platform advantage across passenger and commercial programs. Hybrid designs are also emerging where customers want the lower cost of central control and the fault tolerance of distributed sensing in the same installation.

Complete Report Scope:

- By Battery Type

- Lithium-ion

- Lead-acid

- Nickel-based

- Flow Batteries

- Solid-state

- By Topology

- Centralized

- Distributed

- Modular

- Hybrid

- By Component

- Hardware

- Software

- By Voltage Range

- Low (Up to 36 V)

- Medium (36 to 60 V)

- High (Above 60 V)

- By Application

- Automotive

- Stationary Energy Storage

- Consumer Electronics

- Industrial and Telecom UPS

- Medical Devices

- Aerospace and Marine

- By Country

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- Texas Instruments Inc.

- Sensata Technologies Inc.

- BorgWarner Inc.

- Nuvation Energy

- Eberspaecher Vecture Inc.

- Schneider Electric SE

- Johnson Controls plc

- Analog Devices Inc.

- STMicroelectronics N.V.

- Continental AG

- Renesas Electronics Corp.

- Panasonic Corp.

- Leclanche SA

- Navitas Systems

- Cummins Inc.

- Lithium Balance A/S

- LG Energy Solution

- ION Energy

- Romeo Power Inc.

- Ewert Energy Systems Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating EV penetration & zero-emission mandates

- 4.2.2 Federal / provincial energy-storage incentives

- 4.2.3 Declining Li-ion battery costs

- 4.2.4 Utility-led V2G pilots need advanced BMS

- 4.2.5 Cold-climate thermal-management start-ups (Canada)

- 4.2.6 Cloud-connected BaaS revenue models

- 4.3 Market Restraints

- 4.3.1 Safety recalls from thermal runaway

- 4.3.2 Dependence on imported cells

- 4.3.3 Few functional-safety labs in Mexico

- 4.3.4 SoC-algorithm patent thicket

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment & Funding Landscape

5 Market Size & Growth Forecasts

- 5.1 By Battery Type

- 5.1.1 Lithium-ion

- 5.1.2 Lead-acid

- 5.1.3 Nickel-based

- 5.1.4 Flow Batteries

- 5.1.5 Solid-state

- 5.2 By Topology

- 5.2.1 Centralized

- 5.2.2 Distributed

- 5.2.3 Modular

- 5.2.4 Hybrid

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.2 Software

- 5.4 By Voltage Range

- 5.4.1 Low (Up to 36 V)

- 5.4.2 Medium (36 to 60 V)

- 5.4.3 High (Above 60 V)

- 5.5 By Application

- 5.5.1 Automotive

- 5.5.2 Stationary Energy Storage

- 5.5.3 Consumer Electronics

- 5.5.4 Industrial and Telecom UPS

- 5.5.5 Medical Devices

- 5.5.6 Aerospace and Marine

- 5.6 By Country

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments}

- 6.4.1 Texas Instruments Inc.

- 6.4.2 Sensata Technologies Inc.

- 6.4.3 BorgWarner Inc.

- 6.4.4 Nuvation Energy

- 6.4.5 Eberspaecher Vecture Inc.

- 6.4.6 Schneider Electric SE

- 6.4.7 Johnson Controls plc

- 6.4.8 Analog Devices Inc.

- 6.4.9 STMicroelectronics N.V.

- 6.4.10 Continental AG

- 6.4.11 Renesas Electronics Corp.

- 6.4.12 Panasonic Corp.

- 6.4.13 Leclanche SA

- 6.4.14 Navitas Systems

- 6.4.15 Cummins Inc.

- 6.4.16 Lithium Balance A/S

- 6.4.17 LG Energy Solution

- 6.4.18 ION Energy

- 6.4.19 Romeo Power Inc.

- 6.4.20 Ewert Energy Systems Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment