|

시장보고서

상품코드

1637761

차세대 스토리지 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Next-generation Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

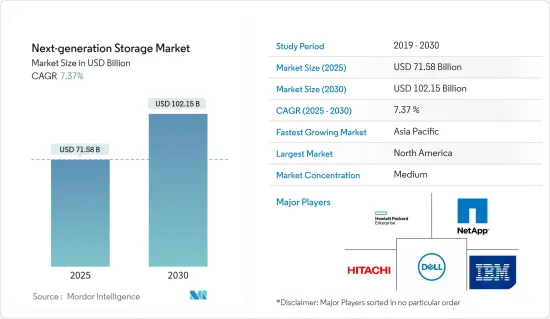

차세대 스토리지 시장 규모는 2025년에 715억 8,000만 달러로 추정되고, 예측 기간(2025-2030년)의 CAGR은 7.37%로 전망되며, 2030년에는 1,021억 5,000만 달러에 이를 것으로 예측됩니다.

디지털 사회의 급속한 발전과 함께 모바일 서비스, 빅 데이터, 클라우드 컴퓨팅, 소셜 네트워킹 애플리케이션 개발이 가속화되고 있습니다. 차세대 스토리지 기술은 IT 기업, 자동차 회사, 데이터센터 등 다양한 최종 사용자 업계의 데이터 보존을 지원하는 제품 및 솔루션의 고급 포트폴리오를 다룹니다. IT 기업은 파일 크기 증가, 대규모 비정형 데이터 및 빅 데이터로 인해 데이터 관리에서 많은 문제에 직면하고 있습니다.

주요 하이라이트

- 기존의 데이터 스토리지 기술은 대량의 일상 데이터를 처리할 수 없습니다. 차세대 데이터 스토리지 인프라는 증가하는 데이터 스토리지 수요에 대응하기 때문에 안정적이고 빠르며 비용 효율적인 솔루션을 제공합니다.

- 또한 차세대 스토리지 기술 시장은 빅 데이터 스토리지, 엔터프라이즈 데이터 스토리지 및 기타 클라우드 기반 서비스를 포함한 광범위한 용도에서 정보 기술 분야에 진출하고 있습니다. 스토리지와 그 조치는 상단 및 하단 라인에 큰 영향을 줄 수 있습니다. IT 조직은 보안 스토리지에 대한 투자에서 비즈니스에 이익을 주는 신기술에 대한 투자로 보다 적극적으로 전환할 것으로 기대되고 있습니다.

- 2023년 4월, 버스트 데이터는 휴렛 팩커드 엔터프라이즈(HPE)가 버스트 데이터의 주요 파일 소프트웨어 플랫폼을 새로운 HPE GreenLake for File Storage 서비스에 통합했다고 발표했습니다. 새로운 HPE GreenLakefor File Storage에 버스트 데이터 고유의 혁신적인 스케일 아웃 소프트웨어 아키텍처를 활용함으로써 기업 고객은 비정형 데이터를 대규모 성능으로 관리하고 보다 신속한 데이터 인사이트를 얻을 수 있습니다.

- 그러나 클라우드 기반 스토리지에는 구성 오류, 불충분한 데이터 거버넌스, 불충분한 액세스 제어 등 많은 보안 문제가 있습니다. 이러한 클라우드 스토리지의 보안 문제는 기업 데이터를 권한이 없는 제3자에게 공개할 수 있어 시장 성장의 억제요인이 되고 있습니다.

- COVID-19의 유행은 차세대 스토리지 시장, 특히 클라우드 스토리지에서 사용되는 솔루션에 긍정적인 영향을 미쳤습니다. 스토리지 벤더는 COVID-19 코로나바이러스의 대유행 중 연구자, 기업, 재택근무 사용자, 파트너 기업의 비즈니스 운영 및 원격 근무을 지원하기 위해 자사의 하드웨어 및 소프트웨어 기술의 일부를 무료로 제공하고 있었습니다.

차세대 스토리지 시장 동향

직접 어태치드 스토리지(DAS)가 현저한 성장을 이룹니다.

- Direct Attached Storage(DAS)는 네트워크를 통해 컴퓨터에 연결된 다른 스토리지 시스템과는 달리 PC 및 서버와 같은 컴퓨터에 직접 연결되는 가장 오래되고 가장 전통적인 데이터 스토리지 시스템입니다.

- DAS는 많은 조직의 스토리지 전략에서 중요한 역할을 하는 다른 스토리지 시스템에 비해 고성능, 설정 및 구성의 용이성, 데이터에 대한 빠른 액세스, 저렴한 비용과 같은 특정 이점을 제공합니다.

- DAS는 서버가 데이터를 읽고 쓰는 데 네트워크를 가로 지르지 않아도 되므로 네트워크 스토리지보다 더 나은 성능을 사용자에게 제공할 수 있습니다. 이러한 이유로 많은 조직이 높은 성능을 필요로 하는 용도에 DAS를 활용합니다. DAS는 네트워크 기반 스토리지 시스템보다 복잡하지 않으므로 배포 및 유지 관리가 쉽고 비용도 절감됩니다.

- 더욱이, 가상화 기술의 발전은 특히 시장의 하이퍼컨버지드 인프라(HCI) 시스템에서 DAS에 새로운 숨결을 불어넣고 있습니다. HCI 시스템은 여러 서버와 DAS 스토리지 노드로 구성되며 스토리지는 논리 리소스 풀에 집계되므로 기존 DAS보다 유연한 스토리지 솔루션을 제공합니다.

- 일반적으로 DAS는 SAS 및 SATA와 같은 고속 컴퓨터 버스 인터페이스의 장점과 시스템의 RAM 및 프로세서에 데이터가 가까운 위치에 있기 때문에 직접 연결된 컴퓨터 시스템에 높은 스토리지 성능을 제공합니다.

- 2022년 5월 TerraMaster는 대용량 데이터를 저장하는 중앙 위치가 필요한 고객을 위한 새로운 8베이 DAS(Direct Attached Storage) 어플라이언스를 출시했습니다. NAS와 달리 DAS는 PC 및 기타 장치에 직접 연결된 케이블을 통해 로컬로 사용됩니다. 새로운 TerraMaster D8-332는 최대 160TB의 용량을 가진 업무용 RAID 스토리지입니다.

- DAS의 일반적인 용도 중 하나는 데이터센터입니다. 웹 호스팅과 같은 용도에서는 DAS가 사용되며 고객은 전용 스토리지 장치를 전용 서버에 연결하기를 원합니다. DAS는 또한 운영 체제 및 하이퍼바이저를 시작하기 위한 스토리지로도 데이터 사용 센터에서 일반적으로 사용됩니다.

북미가 가장 큰 시장 점유율을 차지

- 북미의 차세대 스토리지 시장은 세계 벤더와 소비자들의 지역 집중이 진행되고 있기 때문에 높은 성장률을 보일 것으로 보입니다.

- 미국은 전 세계적으로 데이터센터의 최고 시장 중 하나입니다. 또한 Google은 2022년 4월 전국 데이터센터와 사무실에 95억 달러를 투자할 계획을 발표했습니다. 이 거대 기업은 조지아 주, 텍사스 주, 뉴욕 주, 캘리포니아 주 등 미국 각 주에 14개의 데이터센터를 건설 및 확장 할 예정입니다. 이러한 데이터센터에 대한 투자 증가는 시장에도 큰 성장 기회를 가져오고 있습니다.

- 또한 데이터를 많이 사용하는 사물 인터넷(IoT) 장비는 차세대 스토리지의 또 다른 신흥 시장을 구성하고 있습니다. 이 용도는 주로 광범위합니다. 공장 4.0 형태의 산업 자동화는 하나의 부문입니다. 하지만 IoT에는 웨어러블, 헬스케어, 항공, 스마트 홈, 스마트 팜, 스마트 미터, 스마트 물류 등 스마트로 시작하는 모든 것이 포함됩니다.

- 스탠포드 대학과 Avast의 조사에 따르면 북미의 가정은 세계에서 가장 IoT 장치의 설치 밀도가 높습니다. 특히 이 지역의 가정의 66%가 적어도 하나의 IoT 장치를 소유하고 있습니다. 또한 북미 가정의 25%는 3대 이상의 기기를 소유하고 있습니다.

- 게다가 인터넷 트래픽과 사용자 생성 데이터 증가가 시장 성장에 기여하고 있으며, 북미는 IP 트래픽량이 가장 많습니다. CISCO에 따르면 이 지역의 IP 트래픽은 2022년까지 월간 108.4EB에 달한다고 합니다.

- 에릭슨 보고서에 따르면 북미에서 스마트폰 1대당 월간 모바일 데이터 사용량의 평균은 2028년 55GB에 이를 것으로 예상됩니다. 개선된 5G 네트워크와 무제한 데이터 플랜은 이 지역에서 더 많은 5G 가입자를 유치할 것으로 보입니다. 동영상 기반 앱, 가상현실 및 증강현실, 게임은 엄청난 데이터 트래픽을 생성합니다. 2028년에는 북미의 5G 계약수가 세계의 90%를 웃돌아 전지역 중 가장 높아질 것으로 예측했습니다.

차세대 스토리지 업계 개요

차세대 스토리지 시장은 반고체화되어 있으며 여러 주요 기업으로 구성되어 있습니다. 시장 점유율 측면에서 현재 소수의 주요 기업이 시장을 독점하고 있습니다. 그러나 메모리 패키징 기술의 혁신과 함께 많은 기업들이 신흥국의 미개척 신시장에서 존재감을 높이고 있습니다.

- 2023년 5월-NetApp은 새로운 최신 블록 스토리지 제품과 랜섬웨어 공격으로부터 복구할 때 넷업의 최고 성능을 강조하는 보증을 발표했습니다. 넷업은 이 발표를 통해 IT 예산 제한, IT 복잡성, 지속가능성에 대한 긴급성 증가, 사이버 위협의 지속적인 급증 등 고객의 중요한 과제를 해결하기 위해 노력하고 있습니다.

- 2023년 4월-Pure Storage는 차세대 통합 블록 파일 스토리지 서비스를 발표했습니다. 이 새로운 스토리지 서비스는 단일 세계 자원 풀에서 네이티브 블록 서비스 및 파일 서비스에 대한 액세스를 제공합니다. 통합 스토리지 아키텍처는 블록 스토리지 및 파일 스토리지 포맷을 지원하여 기업이 다양한 방식으로 데이터를 저장하고 탐색할 수 있도록 합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력도-Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- COVID-19의 업계에 대한 영향 평가

- 기술 스냅샷

- 자기 스토리지

- 솔리드 스테이트 스토리지

- 소프트웨어 정의 스토리지(SDS)

- 클라우드 스토리지

- 통합 스토리지

- 기타 스토리지 기술

제5장 시장 역학

- 시장 성장 촉진요인

- 디지털 데이터량 증가

- 솔리드 스테이트 디바이스의 채용 증가

- 스마트폰, 노트북, 태블릿의 보급 확대

- 시장 성장 억제요인

- 클라우드 및 서버 기반 서비스에서 데이터 보안 부족

제6장 시장 세분화

- 스토리지 시스템별

- 직접 어태치드 스토리지(DAS)

- 네트워크 접속형 스토리지(NAS)

- 스토리지 영역 네트워크(SAN)

- 스토리지 아키텍처별

- 파일 오브젝트 베이스 스토리지(FOBS)

- 블록 스토리지

- 최종 사용자 업계별

- BFSI

- 소매

- IT 및 통신

- 헬스케어

- 미디어 및 엔터테인먼트

- 기타 최종 사용자 산업

- 지역별

- 북미

- 유럽

- 아시아태평양

- 세계 기타 지역

제7장 경쟁 구도

- 기업 프로파일

- Dell Inc.

- Hewlett Packard Enterprise Company

- NetApp Inc.

- Hitachi Ltd

- IBM Corporation

- Toshiba Corp.

- Pure Storage Inc.

- DataDirect Networks.

- Scality Inc.

- Fujitsu Ltd.

- Netgear Inc.

제8장 투자 분석

제9장 시장의 미래

AJY 25.02.12The Next-generation Storage Market size is estimated at USD 71.58 billion in 2025, and is expected to reach USD 102.15 billion by 2030, at a CAGR of 7.37% during the forecast period (2025-2030).

With the sizeable and exponential growth in the digital world, there has been an accelerating development in mobile services, Big Data, cloud computing, and social networking applications. Next-generation storage technology deals with an advanced portfolio of products and solutions, which help store data across various end-user industries, including IT firms, automotive companies, and data centers. With the increasing file sizes and a massive amount of unstructured and Big Data, IT companies face plenty of problems while dealing with data management.

Key Highlights

- Conventional data storage technologies cannot handle a large amount of everyday data. The next-generation data storage infrastructure offers a reliable, faster, and cost-effective solution to meet the growing data storage demands.

- Further, the next-generation storage technology market is moving into the information technology sector, with an extensive range of applications across Big Data storage, enterprise data storage, and other cloud-based services. Storage and how it is addressed can significantly impact the top and bottom lines. IT organizations are expected to be more willing to move from making a safe storage investment to investing in new technologies that can benefit the business.

- In April 2023, VAST Data announced that Hewlett Packard Enterprise (HPE) had incorporated VAST Data's leading file software platform into the new HPE GreenLake for File Storage service. By leveraging VAST's unique and innovative scale-out software architecture for the new HPE GreenLakefor File Storage, enterprise customers can manage unstructured data with massive performance and achieve faster data insights.

- However, many security issues are associated with cloud-based storage, such as misconfiguration, insufficient data governance, and poor access controls, among others. Such cloud storage security issues that can expose enterprise data to unauthorized parties can act as a restraint on market growth.

- The COVID-19 pandemic outbreak positively impacted the next-generation storage market, especially solutions used in cloud storage. Storage vendors were making some of their hardware and software technology available for free to help researchers, businesses, work-from-home users, and partners run their businesses and work remotely during the COVID-19 coronavirus pandemic.

Next-generation Storage Market Trends

Direct Attached Storage (DAS) to Witness Significant Growth

- Direct Attached Storage (DAS) is the oldest and most conventional data storage system connected directly to a computer, such as a PC or server, unlike other storage systems connected to a computer over a network.

- DAS offers specific benefits compared to other storage systems that play an essential role in many organizations' storage strategies: high performance, easiness during the setup and configuration, fast access to data, and low cost.

- DAS can provide users with better performance than network storage because the server does not have to traverse the network to read or write data. For this reason, many organizations utilize his DAS for applications that require high performance. DAS is also less complex than network-based storage systems, making them easier to implement and maintain and less expensive.

- Moreover, growing advances in virtualization technology are breathing new life into DAS, especially in the market's hyper-converged infrastructures (HCI) systems. The HCI system consists of multiple servers and DAS storage nodes, and the storage is aggregated into logical resource pools, providing a more flexible storage solution than traditional DAS.

- Generally, DAS offers high storage performance to the computer system it is directly attached to, owing to the advantage of fast computer bus interfaces, such as SAS and SATA, and the close location of data to the system's RAM and processor.

- In May 2022, TerraMaster recently released a new 8-bay Direct Attached Storage (DAS) appliance for customers who need a central location to store large amounts of data. Unlike NAS, DAS is used locally via a cable connected directly to a PC or other device. The new TerraMaster D8-332 is professional RAID storage with up to 160TB capacity.

- One common application of DAS is in data centers. Applications like web hosting use DAS, where customers want their private storage devices connected to their dedicated server. DAS is also commonly utilized in data use centers as storage for booting operating systems and hypervisors.

North America Occupies the Largest Market Share

- The country's next-generation storage market will witness a high growth rate due to the increasing regional concentration of global vendors and consumers.

- The United States remains one of the top markets for data centers globally. Also, in April 2022, Google announced plans to invest USD 9.5 billion in data centers and offices nationwide. The tech giant will be building or expanding 14 data centers in the US states like Georgia, Texas, New York, and California, among others. Such increasing investments in data centers are also creating considerable growth opportunities for the market.

- Moreover, the data-heavy Internet of Things (IoT) devices constitute another emerging market for next-generation storage. These applications primarily cover a wide range. Industrial automation in the form of Factory 4.0 is one segment. Still, the IoT also includes wearables, healthcare, aviation, plus about anything that begins with smart, such as smart homes, smart farms, smart metering, and smart logistics, among others.

- According to a Stanford University and Avast study, homes in the North American region have the highest density of IoT devices installed worldwide. Notably, 66% of households in the region have at least one of her IoT devices. Additionally, 25% of North American homes have three or more devices.

- Additionally, increasing Internet traffic and user-generated data contribute to the market growth, with North America having the highest volume of IP traffic. According to CISCO, IP traffic in the region will reach 108.4 EB per month by 2022.

- According to Ericsson's report, the average monthly mobile data usage per smartphone is likely to reach 55 GB in 2028 in North America. The improved 5G network and unlimited data plans will attract more 5G subscribers in the region. Video-based apps, virtual/augmented reality, and gaming generate huge data traffic. In 2028, the company predicts that 5G subscriptions in North America will be more than 90%world's, the highest among all regions.

Next-generation Storage Industry Overview

The next-generation storage market is semi-consolidated and consists of some major players. In terms of market share, few of the key players currently dominate the market. However, with innovation in memory packaging technology, many companies are increasing their market presence across untapped new markets of emerging economies.

- May 2023 - NetApp announced a new modern block storage offering and a guarantee highlighting NetApp's best-in-class ability to recover from ransomware attacks. Through this launch, the company aims to address critical customer challenges, including restricted IT budgets, increasing IT complexity, increased urgency around sustainability, and the continued exponential growth of cyber threats.

- April 2023 - Pure Storage Inc. announced introducing a next-generation unified block and file storage service. This new storage service provides access to native block and file services from a single, global pool of resources. A unified storage architecture supports block and file storage formats, allowing organizations to store and view data in various ways.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of COVID-19 Impact on the Industry

- 4.4 Technology Snapshot

- 4.4.1 Magnetic Storage

- 4.4.2 Solid State Storage

- 4.4.3 Software Defined Storage (SDS)

- 4.4.4 Cloud Storage

- 4.4.5 Unified Storage

- 4.4.6 Other Storage Technologies

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Volume of Digital Data

- 5.1.2 Rising Adoption of Solid-state Devices

- 5.1.3 Increasing Proliferation of Smartphones, Laptops, and Tablets

- 5.2 Market Restraints

- 5.2.1 Lack of Data Security in Cloud- and Server-based Services

6 MARKET SEGMENTATION

- 6.1 Storage System

- 6.1.1 Direct Attached Storage (DAS)

- 6.1.2 Network Attached Storage (NAS)

- 6.1.3 Storage Area Network (SAN)

- 6.2 Storage Architecture

- 6.2.1 File and Object-based Storage (FOBS)

- 6.2.2 Block Storage

- 6.3 End User Industry

- 6.3.1 BFSI

- 6.3.2 Retail

- 6.3.3 IT and Telecom

- 6.3.4 Healthcare

- 6.3.5 Media and Entertainment

- 6.3.6 Other End-user Industries

- 6.4 Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia Pacific

- 6.4.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Dell Inc.

- 7.1.2 Hewlett Packard Enterprise Company

- 7.1.3 NetApp Inc.

- 7.1.4 Hitachi Ltd

- 7.1.5 IBM Corporation

- 7.1.6 Toshiba Corp.

- 7.1.7 Pure Storage Inc.

- 7.1.8 DataDirect Networks.

- 7.1.9 Scality Inc.

- 7.1.10 Fujitsu Ltd.

- 7.1.11 Netgear Inc.