|

시장보고서

상품코드

1938989

자동차용 커넥터 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Automotive Connector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

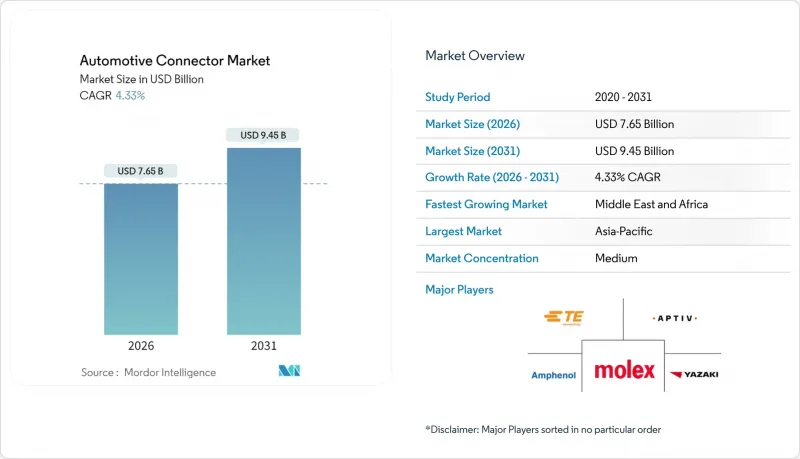

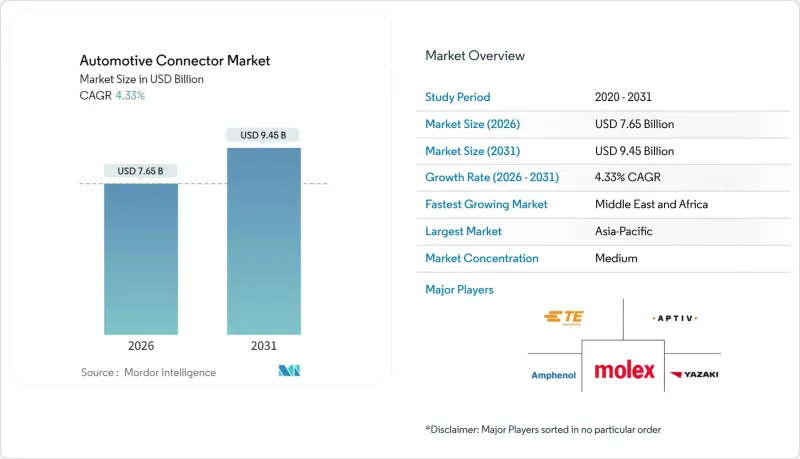

자동차용 커넥터 시장은 2025년에 73억 3,000만 달러로 평가되었으며, 2026년 76억 5,000만 달러에서 2031년까지 94억 5,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 4.33%로 예상됩니다.

표면적으로는 완만한 성장을 지속하고 있지만, 구성비는 빠르게 변화하고 있습니다. 내연기관 파워트레인 관련 수요는 정체된 반면, 고전압 및 고속 데이터 인터커넥트 수요는 확대되고 있습니다. 분산형 ECU에서 구역별 전자 구조로 전환하여 하네스 길이를 단축하고 차량 중량을 줄일 수 있습니다. 이로 인해 커넥터의 복잡성이 증가하고, 고밀도 및 혼합 신호 처리 능력이 부족한 기존 공급업체는 교체 리스크가 발생합니다. 엄격한 안전 규제, 데이터 집약형 ADAS 기능, 800V 배터리 시스템의 보급으로 IP67/IP6K9K 표준을 충족하면서 전력 및 멀티 기가비트 신호를 전송하는 밀폐형 고성능 인터페이스에 대한 수요가 가속화되고 있습니다. 반도체 수준의 제조 정밀도와 소프트웨어 통합 지원을 겸비한 공급업체는 OEM이 요구하는 내결함성 링크, 무선 업데이트 기능, 사이버 보안 지원 데이터 경로에 대한 수요를 충족시킬 수 있는 우위를 점할 수 있습니다.

세계 자동차용 커넥터 시장 동향 및 인사이트

전동화 및 고전압 E 파워트레인 가속화

48V 및 800V 전기 아키텍처로의 전환은 커넥터 요구 사항을 근본적으로 재구성하고 기존 12V 시스템을 넘어 전기 터보 충전, 회생 제동, 고출력 충전 기능을 지원합니다. 앱티브의 고전압 인터커넥트는 400V-1000V의 전압 범위와 최대 250A의 전류 용량을 지원하여 업계의 급속 충전 및 효율 향상에 대한 요구를 충족시킵니다.

48V 마일드 하이브리드 시스템의 등장은 듀얼 전압 아키텍처에 대한 과제를 야기하고 있습니다. 12V 레거시 시스템과 48V 전력 공급 네트워크를 안전하게 분리하고 관리할 수 있는 커넥터가 요구되고 있습니다. TE Connectivity의 AMP+HVA 280 시스템은 이러한 진화를 구현하고 있으며, 통합된 고전압 인터록과 2단계 플로팅 래치를 통해 최대 850V의 애플리케이션에서 향상된 안전성을 제공합니다. 이러한 전동화 물결은 승용차를 넘어 상용차까지 확대되고 있으며, 이튼의 전력 연결 솔루션은 대형 차량 애플리케이션에서 효율적인 에너지 전송을 실현하여 광범위한 운송 전동화 요구를 지원하고 있습니다. 단일 차량 내에서 여러 전압 영역을 관리해야 하는 복잡성은 절연을 유지하고, 진단 기능을 제공하며, 다양한 작동 조건에서 페일 세이프 작동을 보장할 수 있는 고급 커넥터 시스템에 대한 수요를 촉진하고 있습니다.

점점 더 엄격해지는 세계 안전 및 배출가스 규제

규제 프레임워크에서 첨단 안전 시스템 도입이 점점 더 의무화되고 있으며, EU에서는 신차에 자동 비상 브레이크와 전방 충돌 경보를 장착할 것을 요구하고 있습니다. 이는 센서 통합 및 실시간 데이터 처리를 위한 커넥터 수요를 직접적으로 촉진하고 있습니다. 미국 도로교통안전국(NHTSA)이 추진하는 차량-차량 간 통신(V2V) 표준은 5.9GHz DSRC 및 셀룰러 V2X 프로토콜을 지원할 수 있는 고주파 및 저지연 커넥터에 대한 새로운 요구사항을 창출하고 있습니다. CISPR 25 전자기 호환성 표준은 특히 10GHz 이상의 전도성 방출에서 더욱 엄격해지고 있으며, 커넥터 제조업체는 고도의 차폐 및 필터링 기능을 통합해야 합니다.

소프트웨어 정의 차량으로의 전환은 이러한 요구를 더욱 증폭시키고 있습니다. 무선 업데이트 및 지속적인 모니터링 시스템에는 신호 무결성 및 사이버 보안 기능이 강화된 커넥터가 필요하기 때문입니다. 중국의 신에너지 자동차 의무화 정책 및 캘리포니아주의 첨단 클린카 II 규제는 특히 배터리 관리 시스템 및 충전 인프라에서 커넥터 사양에 지역적 차이를 만들어내고 있습니다. 이에 따라 전 세계 공급업체들은 다양한 규제 환경에 적응하면서도 비용 효율성을 유지할 수 있는 플랫폼 유연성을 갖춘 솔루션 개발을 요구받고 있습니다.

구리 및 금속 상품 가격 변동

공급 제약과 재생에너지 및 전기자동차 분야의 수요 급증으로 구리 가격이 상승하여 자동차 커넥터 공급망 전체에 심각한 비용 압력을 가하고 있습니다. 전기자동차는 기존 내연기관차보다 훨씬 많은 구리가 필요하며, 전기자동차 1대에는 약 83kg의 구리가 함유되어 있는 반면, 기존 자동차는 23kg입니다. 이 때문에 가격 변동이 자동차용 커넥터 비용에 미치는 영향이 증폭되고 있습니다. Copperweld의 구리 피복 알루미늄 도체 및 구리 피복 강철 도체와 같은 바이메탈 솔루션은 전기적 성능 특성을 유지하면서 구리 사용량을 최대 83%까지 줄일 수 있는 대안으로 기대를 모으고 있습니다. 또한, 구리 광산이 정치적으로 불안정한 지역에 집중되어 있다는 점도 공급망 리스크를 더욱 높이고 있습니다. 동시에 무역 마찰과 수출 규제가 가격 변동을 더욱 악화시키고 있으며, 자동차 제조업체들은 헤지 전략과 장기 공급 계약을 도입할 수밖에 없는 상황입니다. 이로 인해 커넥터 조달 및 설계 최적화의 유연성이 제한될 수 있습니다.

부문 분석

파워트레인 분야는 2025년 자동차 커넥터 시장 규모에서 33.10%로 가장 큰 비중을 차지할 것으로 예상되며, 내연기관(ICE)과 하이브리드 파워트레인 모두에서 엔진 관리, 변속기 제어, 연료 분사 시스템의 중요성이 지속되고 있음을 반영하고 있습니다. 그러나 ADAS 및 자율주행 시스템은 첨단 안전 기능에 대한 규제 요건과 자동차 자동화 수준 향상을 위한 업계의 발전으로 인해 2026년부터 2031년까지 연평균 17.25%의 CAGR로 가장 빠르게 성장하는 부문으로 부상할 것으로 예상됩니다.

안전 및 보안 분야는 에어백 시스템, 전자식 안정성 제어, 충돌 방지 기술의 통합 확대로 혜택을 받고 있습니다. 동시에, 본체 배선 및 전력 분배 부문은 여러 기능을 더 적은 수의 고급 제어 장치에 통합하는 구역별 아키텍처의 도입에 적응하고 있습니다. 편안함, 편의성, 엔터테인먼트 시스템은 모든 차량 부문에서 프리미엄 기능에 대한 소비자의 기대가 높아지면서 꾸준한 성장세를 보이고 있습니다. 동시에 내비게이션 및 계기류 애플리케이션은 고해상도 디스플레이와 증강현실 인터페이스를 지원하는 방향으로 진화하고 있습니다.

전기자동차 전용 충전 및 에너지 관리 애플리케이션의 출현은 기존 자동차 커넥터 시장에 존재하지 않았던 새로운 카테고리를 상징하며, 전기 파워트레인에 대한 업계의 근본적인 변화를 강조하고 있습니다. 이러한 부문 변화는 기계식에서 전자식 차량 시스템으로의 광범위한 전환을 반영하고 있으며, 전통적인 파워트레인용 커넥터는 배터리 시스템, DC-DC 컨버터, 회생 제동 네트워크를 관리할 수 있는 고전압 및 고전류 솔루션으로 대체되고 있습니다. ADAS 애플리케이션의 급속한 성장은 고주파 및 저지연 전송에 대한 전문성을 갖춘 커넥터 공급업체에게 기회를 제공합니다. 이러한 시스템에서는 여러 소스의 센서 데이터를 동시에 실시간으로 처리해야 하기 때문입니다.

승용차는 2025년 기준 자동차 커넥터 시장 점유율의 53.65%를 차지하며, 높은 생산량과 차량당 전자부품 증가의 혜택을 누리고 있습니다. 그러나 이륜차는 2031년까지 CAGR 11.05%로 가장 빠르게 성장하는 부문입니다. 소형 상용차는 E-Commerce의 성장과 라스트 마일 배송의 최적화에 힘입어 안정적인 수요를 유지하고 있습니다. 한편, 중대형 상용차에서는 견고하고 고성능의 커넥터 솔루션을 필요로 하는 첨단 텔레매틱스 및 차량 관리 시스템의 채택이 확대되고 있습니다. 상용차 부문은 커넥터의 내구성과 내환경성 혁신을 주도하고 있으며, 이러한 용도는 승용차에서 요구되는 IP67/IP6K9K 등급과 극한의 온도 범위에서 작동할 수 있는 IP67/IP6K9K 등급을 요구합니다.

이륜차의 성장은 도시화 추세와 혼잡한 도심에서의 전기 교통수단에 대한 규제적 지원을 반영하고 있으며, 공간 제약이 있는 용도에 최적화된 소형 및 경량 커넥터에 대한 수요를 창출하고 있습니다. 상용차 운영자들이 운영비 절감과 배기가스 규제 대응을 위해 상용차 전기화가 가속화되고 있습니다. 이에 따라 급속 충전 및 고에너지 밀도 배터리 시스템을 지원하는 고전압 커넥터에 대한 수요가 증가하고 있습니다. 자율주행 기술이 서로 다른 궤도로 발전함에 따라 승용차와 상용차의 구분이 점점 더 중요해지고 있습니다. 통제된 운영 환경과 전용 인프라 투자를 통해 상용 애플리케이션은 더 빨리 높은 수준의 자동화를 달성할 수 있습니다.

지역별 분석

아시아태평양은 촘촘한 전자부품 공급망, 세계 최고 수준의 자동차 생산량, 전기자동차 및 버스에 대한 국가 정책으로 인해 2025년 기준 자동차 커넥터 시장 매출의 38.20%를 차지하며 선두를 유지했습니다. 중국 OEM 업체는 구역별 하네스를 자체 생산하고 있으며, 기술이전 조항에 따라 2차 커넥터 제조업체를 현지 합작회사로 끌어들이고 있습니다. 일본의 기존 제조사들은 스미토모전기의 '30VISION' 등 CASE 프로그램을 추진하며 800V 플랫폼에 최적화된 컴팩트한 저삽입력 모델을 출시하고 있습니다. 국내 업체는 배터리 기술을 활용하여 셀-투-팩 구조에 대응하는 고전류 기판 단자를 개발 중입니다. 동남아시아 국가에서는 범용 압착 부품의 저렴한 인건비가 장점이지만, 열대성 호우에 대응하는 IP67 규격에 대한 수요가 증가하면서 가격대를 불문하고 자동차 커넥터 시장의 확대가 가속화되고 있습니다.

중동 및 아프리카는 현재 규모는 작지만 2031년까지 CAGR 14.85%로 예상됩니다. 이는 주권재부기금에 의한 전기자동차 공장 및 충전 회랑의 정비에 따른 것입니다. 사우디는 EV 클러스터에 대한 자금 지원과 고전압 케이블의 현지 조달을 추진하고 있습니다. 레오니의 아가디르 신공장은 북아프리카의 와이어링 하니스 시장의 모멘텀을 상징합니다. 가혹한 고온 및 분진 환경은 고온 내성 LCP 하우징 및 강화 개스킷 플랜지에 대한 수요를 불러일으켰습니다. 지역 조달 규정에 따라 다국적 기업들은 현지 폴리머 컴파운드에 대한 인증을 요구하고 있으며, 내성을 강화하는 동시에 이중 검증 과정을 요구하고 있습니다.

북미와 유럽은 성숙하면서도 혁신이 풍부한 시장입니다. 미국 OEM 업체들은 고급 차량에 핸즈프리 레벨3 자율주행 시스템을 통합하고, 20Gbps 보드 커넥터와 실리콘 등급 클린룸 공정의 공급을 촉진하고 있습니다. 유럽의 기후 목표는 400kW급 급속 충전 허브의 보급을 가속화하고, 온도 센서가 내장된 1,000V 접촉기 도입을 의무화하고 있습니다. 두 지역 모두 순환 경제를 의무화하고 있으며, TE Connectivity의 "Green Stock" 프로그램은 초과 재고를 재사용하여 매립 폐기물과 탄소발자국을 줄입니다. 2024년 공급망 혼란은 자동차 커넥터 시장에서 전략적 자율성을 확보하기 위해 주석 도금과 플라스틱 성형의 국내 회귀를 가속화했습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09The automotive connector market was valued at USD 7.33 billion in 2025 and estimated to grow from USD 7.65 billion in 2026 to reach USD 9.45 billion by 2031, at a CAGR of 4.33% during the forecast period (2026-2031).

Growth remains moderate on the surface, yet the mix changes quickly: demand linked to internal-combustion powertrains plateaus while high-voltage and high-speed data interconnects scale up. The shift from distributed ECUs to zonal electronic structures compresses harness length, trimming vehicle weight. It raises connector complexity, creating displacement risk for legacy suppliers that lack high-density, mixed-signal capabilities. Rigorous safety regulations, data-rich ADAS features, and 800 V battery systems propel orders for sealed, high-performance interfaces that carry power and multi-gigabit signals while meeting IP67/IP6K9K ratings. Suppliers that combine semiconductor-grade manufacturing precision with software integration support are positioned to win as OEMs demand fault-tolerant links, over-the-air updatability, and cyber-secure data paths.

Global Automotive Connector Market Trends and Insights

Accelerating Electrification and Higher-Voltage E-Powertrains

The transition to 48V and 800V electrical architectures fundamentally reshapes connector requirements, moving beyond traditional 12V systems to support electric turbocharging, regenerative braking, and high-power charging capabilities. Aptiv's high-voltage interconnects now support voltage ranges from 400V to 1000V with current capacities up to 250A, addressing the industry's shift toward faster charging and improved efficiency.

The emergence of 48V mild hybrid systems creates a dual-voltage architecture challenge, requiring connectors to safely isolate and manage 12V legacy systems and 48V power delivery networks. TE Connectivity's AMP+ HVA 280 system exemplifies this evolution, featuring integrated high-voltage interlocks and two-stage floating latches for enhanced safety in applications up to 850V. This electrification wave extends beyond passenger vehicles to commercial fleets, where Eaton's power connection solutions enable efficient energy transfer in heavy-duty applications, supporting the broader transportation electrification mandate. The complexity of managing multiple voltage domains within a single vehicle drives demand for sophisticated connector systems that can maintain isolation, provide diagnostic capabilities, and ensure fail-safe operation across diverse operating conditions.

Stricter Global Safety and Emission Mandates

Regulatory frameworks increasingly mandate advanced safety systems, with the EU requiring autonomous emergency braking and forward collision warning in new vehicles, directly driving connector demand for sensor integration and real-time data processing. The NHTSA's push for vehicle-to-vehicle communication standards creates new requirements for high-frequency, low-latency connectors capable of supporting 5.9 GHz DSRC and cellular V2X protocols. CISPR 25 electromagnetic compatibility standards have become increasingly stringent, particularly for conducted emissions above 10 GHz, forcing connector manufacturers to integrate advanced shielding and filtering capabilities.

The shift toward software-defined vehicles amplifies these requirements, as over-the-air updates and continuous monitoring systems demand connectors with enhanced signal integrity and cybersecurity features. China's New Energy Vehicle mandate and California's Advanced Clean Cars II regulation create regional variations in connector specifications, particularly for battery management systems and charging infrastructure, requiring global suppliers to develop platform-flexible solutions that can adapt to diverse regulatory environments while maintaining cost efficiency.

Volatile Copper and Metal Commodity Prices

Copper prices are rising, driven by supply constraints and surging demand from renewable energy and electric vehicle sectors, creating significant cost pressures across the automotive connector supply chain. Electric vehicles require significantly more copper than traditional ICE vehicles, with each EV containing approximately 83 kilograms of copper compared to 23 kilograms in conventional vehicles, amplifying the impact of price volatility on automotive connector costs. Copperweld's bimetallic solutions, including Copper-Clad Aluminum and Copper-Clad Steel conductors, offer potential alternatives that can reduce copper usage by up to 83% while maintaining electrical performance characteristics. The concentration of copper mining in politically unstable regions creates additional supply chain risks. At the same time, trade tensions and export restrictions further exacerbate price volatility, forcing automotive OEMs to implement hedging strategies and long-term supply contracts that may limit flexibility in connector sourcing and design optimization.

Other drivers and restraints analyzed in the detailed report include:

- Surge in In-Vehicle Infotainment and Connectivity Units

- Rapid ADAS and Autonomous Functionality Penetration

- Shortage of High-Performance Resins (PPS, LCP)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Powertrain applications maintain the largest market share at 33.10% of the automotive connector market size in 2025, reflecting the continued importance of engine management, transmission control, and fuel injection systems across both ICE and hybrid powertrains. However, ADAS and autonomous systems emerge as the fastest-growing segment at 17.25% CAGR from 2026-2031, driven by regulatory mandates for advanced safety features and the industry's progression toward higher levels of vehicle automation.

Safety and security applications benefit from the increasing integration of airbag systems, electronic stability control, and collision avoidance technologies. At the same time, body wiring and power distribution segments adapt to zonal architecture implementations that consolidate multiple functions into fewer, more sophisticated control units. Comfort, convenience, and entertainment systems experience steady growth as consumer expectations for premium features expand across all vehicle segments. At the same time, navigation and instrumentation applications evolve to support high-resolution displays and augmented reality interfaces.

The emergence of charging and energy management applications specifically for electric vehicles represents a new category that didn't exist in traditional automotive connector markets, highlighting the industry's fundamental transformation toward electrified powertrains. This segmentation shift reflects the broader transition from mechanical to electronic vehicle systems, where traditional powertrain connectors face displacement by high-voltage, high-current solutions capable of managing battery systems, DC-DC converters, and regenerative braking networks. The rapid growth in ADAS applications creates opportunities for connector suppliers with expertise in high-frequency, low-latency transmission, as these systems require real-time processing of sensor data from multiple sources simultaneously.

Passenger cars command 53.65% of the automotive connector market share in 2025, benefiting from high production volumes and increasing electronic content per vehicle. Yet, two-wheelers represent the fastest-growing segment at 11.05% CAGR through 2031. Light commercial vehicles maintain steady demand driven by e-commerce growth and last-mile delivery optimization. Meanwhile, medium and heavy commercial vehicles increasingly adopt advanced telematics and fleet management systems that require ruggedized, high-performance connector solutions. The commercial vehicle segments drive innovation in connector durability and environmental resistance, as these applications demand IP67/IP6K9K ratings and operation across extreme temperature ranges that exceed passenger car requirements.

The growth in two-wheelers reflects urbanization trends and regulatory support for electric transportation in congested city centers, creating demand for compact, lightweight connectors optimized for space-constrained applications. Commercial vehicle electrification accelerates as fleet operators seek to reduce operating costs and meet emission regulations. This drives demand for high-voltage connectors supporting rapid charging and energy-dense battery systems. The segmentation between passenger and commercial vehicles becomes increasingly relevant as autonomous driving technologies develop along different trajectories, with commercial applications potentially achieving higher automation levels sooner due to controlled operating environments and dedicated infrastructure investments.

The Automotive Connector Market Report is Segmented by Application (Powertrain, Safety and Security, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Propulsion Type (ICE Vehicles, Hybrid Electric Vehicles, and More), Connector Type (Wire-To-Wire, Wire-To-Board, and More), Connection Sealing (Sealed and Unsealed), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained leadership with 38.20% of the automotive connector market revenue in 2025, thanks to dense electronics supply chains, the world's highest vehicle output, and state policies favoring electric cars and buses. Chinese OEMs build zonal harnesses in-house, pulling tier-two connector makers into local joint ventures under technology-transfer clauses. Japanese incumbents pursue CASE programs such as Sumitomo's "30VISION," launching compact, low-insertion-force models optimized for 800 V platforms. Korean suppliers channel battery know-how into high-current board terminals that support cell-to-pack architectures. Southeast Asian nations offer lower labor costs for commodity crimping yet increasingly demand IP67 ratings for tropical downpours, widening the automotive connector market across price tiers.

The Middle East and Africa, while small today, are poised for a 14.85% CAGR through 2031 as sovereign wealth funds seed electric-vehicle plants and charging corridors. Saudi Arabia bankrolls EV clusters and sources high-voltage cabling locally; Leoni's new Agadir plant exemplifies North-African wire harness momentum. Harsh heat and dust provoke demand for high-temperature LCP housings and reinforced gasket flanges. Regional content rules push multinationals to qualify domestic polymer compounds, adding resilience yet demanding duplicate validation runs.

North America and Europe represent mature but innovation-rich arenas. United States OEMs integrate hands-free Level 3 stacks on premium trims, spurring the supply of 20 Gbps board connectors and silicon-grade cleanroom processes. Europe's climate targets accelerate 400 kW fast-charge hubs, obliging 1,000 V contactors with embedded temperature sensors. Both regions chase circular-economy mandates; TE Connectivity's Green Stock program repurposes excess inventory, cutting landfill waste and carbon footprints. Supply chain shocks during 2024 catalyzed the on-shoring of tin plating and plastic molding to secure strategic autonomy within the automotive connector market.

- TE Connectivity Ltd

- Yazaki Corporation

- Aptiv PLC

- Molex Inc. (Koch Industries)

- Sumitomo Wiring Systems Ltd

- Luxshare Precision Industry Co., Ltd

- Hirose Electric Co., Ltd

- J.S.T. Mfg Co., Ltd

- Amphenol Corporation

- Furukawa Electric Co., Ltd

- Rosenberger Hochfrequenztechnik GmbH

- Leoni AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating electrification and higher-voltage e-powertrains

- 4.2.2 Rapid ADAS and autonomous functionality penetration

- 4.2.3 Software-defined vehicles requiring high-speed data links

- 4.2.4 Stricter global safety and emission mandates

- 4.2.5 Shift to zonal e/e architectures driving high-density connectors

- 4.2.6 Surge in in-vehicle infotainment and connectivity units

- 4.3 Market Restraints

- 4.3.1 Volatile copper and metal commodity prices

- 4.3.2 Shortage of high-performance resins (PPS, LCP)

- 4.3.3 Reliability challenges in harsh automotive environments

- 4.3.4 EMI compliance hurdles at more than 10 Gbps signal speeds

- 4.4 Value / Supply-Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value in USD)

- 5.1 By Application

- 5.1.1 Powertrain

- 5.1.2 Safety and Security

- 5.1.3 Body Wiring and Power Distribution

- 5.1.4 Comfort, Convenience and Entertainment

- 5.1.5 Navigation and Instrumentation

- 5.1.6 ADAS and Autonomous Systems

- 5.1.7 Charging and Energy Management (EV)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy Commercial Vehicles

- 5.2.4 Two-Wheelers

- 5.2.5 Bus and Coach

- 5.3 By Propulsion Type

- 5.3.1 Internal Combustion Engine (ICE) Vehicles

- 5.3.2 Hybrid Electric Vehicles (HEV)

- 5.3.3 Plug-in Hybrid Electric Vehicles (PHEV)

- 5.3.4 Battery Electric Vehicles (BEV)

- 5.3.5 Fuel-Cell Electric Vehicles (FCEV)

- 5.4 By Connector Type

- 5.4.1 Wire-to-Wire

- 5.4.2 Wire-to-Board

- 5.4.3 Board-to-Board

- 5.4.4 I/O and Circular

- 5.4.5 FFC/FPC and Micro

- 5.4.6 High-Speed / High-Voltage

- 5.5 By Connection Sealing

- 5.5.1 Sealed

- 5.5.2 Unsealed

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Indonesia

- 5.6.4.6 Vietnam

- 5.6.4.7 Philippines

- 5.6.4.8 Australia

- 5.6.4.9 New Zealand

- 5.6.4.10 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Egypt

- 5.6.5.6 Nigeria

- 5.6.5.7 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 TE Connectivity Ltd

- 6.4.2 Yazaki Corporation

- 6.4.3 Aptiv PLC

- 6.4.4 Molex Inc. (Koch Industries)

- 6.4.5 Sumitomo Wiring Systems Ltd

- 6.4.6 Luxshare Precision Industry Co., Ltd

- 6.4.7 Hirose Electric Co., Ltd

- 6.4.8 J.S.T. Mfg Co., Ltd

- 6.4.9 Amphenol Corporation

- 6.4.10 Furukawa Electric Co., Ltd

- 6.4.11 Rosenberger Hochfrequenztechnik GmbH

- 6.4.12 Leoni AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment