|

시장보고서

상품코드

1686527

지휘 통제 시스템 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Command And Control Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

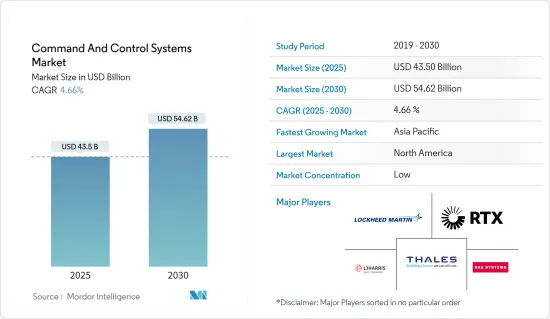

지휘 통제 시스템 시장 규모는 2025년에 435억 달러로 추정되고, 예측 기간인 2025-2030년 CAGR 4.66%로 성장할 전망이며, 2030년에는 546억 2,000만 달러에 달할 것으로 예측됩니다.

정치적 분쟁과 전황의 격화, 테러리즘의 확대, 국경을 넘은 분쟁 증가가 세계의 방위력 강화로 이어졌습니다. 군사비 증가는 기존 C2 시스템 능력이 업계의 기준에 미달하기 때문에 군대가 신세대 C2 시스템 조달에 주력하도록 촉진했습니다. 현재 진행 중인 군사 근대화 계획 및 선진 방위 시스템 조달을 위한 지출 증가는 예측 기간 동안 시장을 견인할 것으로 보입니다.

전시 중, 방위 부문은 특히 C4ISR 시스템에 있어서, 통신, 전략 입안, 의사 결정에 사용되기 때문에 시대 지연의 기술을 포함할 수 없습니다. C2 시스템은 C4ISR 시스템의 중요한 일부이며, 그 성장은 매우 빠를 것으로 예상됩니다. 선진적인 시스템을 개발하기 위한 연구개발 활동은 향후 몇 년간 시장에 성장 기회를 가져올 가능성이 있습니다. 위성통신(SATCOM)은 원격지나 가혹한 환경에서 C2를 위한 강화된 능력을 제공함으로써 현대 군사작전의 확고한 일부가 되었습니다. SATCOM의 이용 확대는 향후 몇 년간 시장에 새로운 기회를 가져다 줄 것으로 예상됩니다.

그러나 지휘 통제 시스템은 레거시 시스템, 통신 네트워크, 하드웨어 플랫폼 등 기존 인프라와 통합되어야 합니다. 서로 다른 OEM에 의해 개발되거나 서로 다른 프로토콜로 작동하는 다양한 시스템 간의 원활한 상호 운용성과 데이터 교환을 보장해야 하기 때문에 통합은 복잡합니다. 이러한 통합 문제는 프로젝트 지연, 비용 초과, 운영 비효율성을 초래할 수 있습니다.

또한 새로운 위협을 선점하고 이에 대응하는 최신 솔루션을 개발하기 위해서는 최신 C2 시스템의 연구 개발에 끊임없는 투자가 필수적입니다. 상호 운용성과 확장성은 최신 지휘 통제 시스템의 중요한 특징이며 변화하는 운영 환경에 적응을 가능하게 하고 있습니다.

지휘 통제 시스템 시장 동향

예측 기간 동안 육상 플랫폼이 현저한 성장을 보입니다.

육상 기반의 지휘 통제 시스템 분야는 전장에서의 사용률이 높기 때문에 예측 기간 동안 최대 시장 점유율을 차지할 것으로 예측됩니다. 군사 근대화 프로그램 증가 및 방위군에 의한 선진 방어 시스템 조달이 시장 성장의 원동력이 되고 있습니다. 다양한 지정학적 문제 및 테러리스트와 적대적 활동 증가로 인한 세계 군사작전 증가는 고정기지관제센터와 육상사령본부의 건설 수요를 증가시켰습니다.

육상 C2 시스템은 전장의 부대와 지상 국원 간의 통신 브리지로서 기능합니다. 예를 들어 2023년 10월 엘빗시스템즈의 자회사인 엘빗시스템즈 스웨덴 AB는 스웨덴 육군의 디지털화 프로그램 LSS Mark에 통합 파트너로 참여하기 위해 1억 7,000만 달러의 계약을 따냈습니다. 통합 파트너로서 엘빗 시스템스 스웨덴은 지휘소와 차량부터 하차 시스템까지 다양한 플랫폼 상의 지휘 제어 시스템의 통합, 설치, 유지보수, 업그레이드를 수행합니다.

이와 같이 첨단 지휘통제시스템의 조달에 대한 투자 증가와 각국의 인프라 개발에 대한 연간 국방예산의 배분 증가가 시장의 육상 부문 성장을 뒷받침하고 있습니다.

아시아태평양은 예측기간 동안 현저한 성장을 보일 것으로 예측

아시아태평양은 예측 기간 동안 현저한 성장을 이룰 것으로 보입니다. 이러한 성장은 중국, 인도, 한국 등의 국가에 의한 국방 지출 증대 및 군사 근대화 계획의 고조에 기인하고 있습니다. 통제선(LOC)을 둘러싼 인도와 중국의 긴장이 높아지고, 국경을 넘은 분쟁 증가, 아시아 전역에서의 테러 활동의 활성화가 아시아 국가들이 국방 분야에 대한 지출 증가로 이어졌습니다.

게다가 인도, 중국, 일본, 호주 등의 국가들은 여러 공중, 육상, 우주, 해군의 근대화 프로그램에 참가하고 있습니다. 예를 들면, 록히드 마틴 오스트레일리아는 2022년 8월, 오스트레일리아 공군(RAAF) 및 국방 과학기술 그룹(DSTG)과 제휴해, 시스템의 검토를 실시했습니다. 인공지능을 활용하여 다양한 영역에 걸친 지휘통제의 전술적 차원에서 신속한 의사결정을 지원하기 위함입니다.

마찬가지로 일본에서는 2024년 1월, 노스롭 그라만사와 미쓰비시전기 주식회사가, 일본의 지상 시스템용의 통합적인 방공 및 미사일 방위 능력에 대해 협력하는 계약을 체결했습니다. 양사는 각각의 기술을 조합해 일본의 방공 및 미사일 방위 능력을 통합하는 네트워킹 솔루션을 개발합니다. 이것은 다양한 방위 시스템 간에 표적 정보를 공유하는 것입니다. 상황 인식 향상, 상호운용성 향상, 효과적인 자원관리에 의해 일본의 방위 능력을 높입니다.

지휘 통제 시스템 산업 개요

지휘 통제 시스템 시장은 단편화되어 있으며, 여러 세계 기업과 현지 기업이 시장에서 큰 점유율을 차지하고 있습니다. 유명한 기업으로는 L3 Harris Technologies Inc., Lockheed Martin Corporation, THALES, RTX Corporation, BAE Systems plc 등을 들 수 있습니다.

시장 경쟁이 치열해짐에 따라 주요 OEM은 방위군을 위한 차세대 솔루션 개발에 주력하고 있습니다. 예를 들면, 2023년 11월, 우주 시스템 사령부(SSC)는, 미국 우주군과 미국 우주 사령부에 위성 제어 능력을 제공하기 위해, Command-and-Control System-Consolidated(CCS-C) Sustainment and Resiliency(C-SAR) 계약의 일환으로서 8년간 5억 7,900만 달러의 계약을 Kratos Defense and Security Solutions에 발주했습니다. 계약에 따라 클레이토스는 국방위성통신시스템(DSCS) III, 선진 초고주파(AEHF), 밀스터 위성통신시스템, 광대역 세계위성(WGS) 위성시스템을 직접 지원합니다.

마찬가지로 2023년 8월 미국 공군의 연구자들은 15분 이내에 세계적인 위협에 대응하기 위한 군용 기술을 성숙시키고 실증하고 보급하기 위해 13개의 방위 기술 기업의 지원과 협력을 얻고 있습니다. 미 공군 당국은 2023년 7월, 9억 5,000만 달러를 투자할 가능성이 있는 JADC2(Joint All Domain Command and Control) 프로그램에 13사를 추가한다고 발표했습니다. 미국 공군의 이 프로그램은, 복수의 플랫폼을 통합해 새로운 전투 능력을 실현하는 오픈 아키텍처의 시스템 및 패밀리에 있어서, 모든 군사 영역에 걸치는 시스템을 개발하는 것을 목적으로 하고 있습니다.

이러한 기술 혁신, 연구개발에 대한 주목 고조 및 다양한 방위조직에 의한 선진 시스템 도입이 시장의 성장을 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자 및 소비자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 플랫폼별

- 육상

- 하늘

- 바다

- 우주

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 기타 라틴아메리카

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 프로파일

- RTX Corporation

- THALES

- General Dynamics Corporation

- L3Harris Technologies, Inc.

- BAE Systems plc

- Honeywell International Inc.

- Saab AB

- CACI International Inc

- Kratos Defense & Security Solutions, Inc.

- Leonardo SpA

- Lockheed Martin Corporation

제7장 시장 기회 및 향후 동향

AJY 25.04.29The Command And Control Systems Market size is estimated at USD 43.50 billion in 2025, and is expected to reach USD 54.62 billion by 2030, at a CAGR of 4.66% during the forecast period (2025-2030).

Increasing political disputes and warfare situations, growing terrorism, and growing cross-border conflicts led to the strengthening of global defense capabilities. Increasing military expenditure facilitated the armies to focus more on procuring new generation C2 systems, as the capabilities of the existing C2 systems are not up to the industry benchmark. The ongoing military modernization programs and rising spending on procurement of advanced defense systems will drive the market during the forecast period.

During wartime, defense departments cannot include any obsolete technologies, especially in C4ISR systems, because these systems are used for communication, strategic planning, and decision-making. C2 systems are a crucial part of C4ISR systems, whose growth is expected to be very rapid. The ongoing R&D activities to develop advanced systems may provide growth opportunities for the market in the coming years. Satellite communications (SATCOM) became a firmly established part of modern military operations by providing enhanced capabilities for C2 in remote and austere environments. The growing use of SATCOM is expected to bring new opportunities for the market in the coming years.

However, command and control systems need to integrate with existing infrastructure, including legacy systems, communication networks, and hardware platforms. Integration is complex because it must ensure seamless interoperability and data exchange between diverse systems, which might developed by different OEMs or operate on different protocols. Such integration challenges can lead to project delays, cost overruns, and operational inefficiencies.

Moreover, constant investment in research and development for the latest C2 systems is essential for staying ahead of emerging threats and developing the latest solutions to counter them. Interoperability and scalability are key traits of the latest command and control systems, allowing them to adapt to changing operational environments.

Command and Control Systems Market Trends

Land Based Platform Will Showcase Remarkable Growth During the Forecast Period

The land-based command and control systems segment is estimated to hold the largest market share during the forecast period due to its high usage on the battlefield. The increasing number of military modernization programs and procurement of advanced defense systems by the defense forces drive the market growth. The growing military operations worldwide due to various geopolitical issues and the growth of terrorist and hostile activities increased the demand for building fixed-base control centers and land-based command headquarters.

The land-based C2 systems act as a communication bridge between troops and ground station personnel on the battlefield. For instance, in October 2023, Elbit Systems Ltd. subsidiary Elbit Systems Sweden AB was awarded a contract of USD 170 million to participate as an integration partner in the Swedish Army digitalization program LSS Mark. As the integration partner, Elbit Systems Sweden will integrate, install, maintain, and upgrade command and control systems on a variety of platforms, from command posts and vehicles to dismounted systems.

Thus, growing investment in the procurement of advanced command and control systems and an increase in annual defense budget allocation to infrastructure development of various countries drive the growth of the market land-based segment.

Asia-Pacific is Estimated to Show Remarkable Growth During the Forecast Period

Asia-Pacific will experience significant growth during the forecast period. The growth is attributed to growing defense expenditure and rising military modernization programs by countries like China, India, South Korea, and others. Increasing tensions between India and China over the line of control (LOC), rising cross-border conflicts, and growing terrorist activities across the region led to increased spending on the defense sector by Asian countries.

In addition, countries such as India, China, Japan, and Australia participate in several airborne, land, space, and naval modernization programs. For instance, in August 2022, Lockheed Martin Australia partnered with the Royal Australian Air Force (RAAF) and Defence Science and Technology Group (DSTG) to explore systems. It is to leverage artificial intelligence to support rapid decision-making at tactical levels of command and control across various domains.

Similarly, in Japan, in January 2024, Northrop Grumman Corporation and Mitsubishi Electric Corporation signed an agreement to collaborate on integrated air and missile defense capabilities for Japan's ground-based systems. The companies will combine their respective technologies to develop a networking solution to integrate Japan's air and missile defense capabilities. It is to share target information across various defense systems. It will increase Japan's defense capability by improving situational awareness, increased interoperability, and effective resource management.

Command and Control Systems Industry Overview

The market for command and control systems is fragmented, with the presence of several global and local players holding significant shares of the market. Some of the prominent players are L3Harris Technologies Inc., Lockheed Martin Corporation, THALES, RTX Corporation, and BAE Systems plc.

With growing competition in the market, key OEMs are focusing on the development of next-generation solutions for defense forces. For instance, in November 2023, Space Systems Command (SSC) awarded an eight-year USD 579 million contract to Kratos Defense and Security Solutions as part of the Command-and-Control System-Consolidated (CCS-C) Sustainment and Resiliency (C-SAR) contract to provide satellite control capabilities to US Space Force and US Space Command. As per the contract, Kratos will provide direct support to Defense Satellite Communications System (DSCS) III, Advanced Extremely High Frequency (AEHF), Milstar Satellite Communications System, and Wideband Global Satellite (WGS) satellite systems.

Similarly, in August 2023, the US Air Force researchers are taking the support and assistance of an additional 13 defense tech companies to mature, demonstrate, and proliferate technologies for military forces to respond to global threats in 15 minutes or less. US Air Force officials announced the 13 additional companies in July 2023 in the potential USD 950 million Joint All Domain Command and Control (JADC2) program. This US Air Force program aims to develop systems across all military domains in an open-architecture family of systems that integrate several platforms to enable new warfighting capabilities.

Such growing focus on innovation, research, and development, and the introduction of advanced systems from various defense organizations are driving the market growth.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Platform

- 5.1.1 Land

- 5.1.2 Air

- 5.1.3 Sea

- 5.1.4 Space

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 India

- 5.2.3.2 China

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Rest of Latin America

- 5.2.5 Middle East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 South Africa

- 5.2.5.3 Saudi Arabia

- 5.2.5.4 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 RTX Corporation

- 6.2.2 THALES

- 6.2.3 General Dynamics Corporation

- 6.2.4 L3Harris Technologies, Inc.

- 6.2.5 BAE Systems plc

- 6.2.6 Honeywell International Inc.

- 6.2.7 Saab AB

- 6.2.8 CACI International Inc

- 6.2.9 Kratos Defense & Security Solutions, Inc.

- 6.2.10 Leonardo S.p.A

- 6.2.11 Lockheed Martin Corporation