|

시장보고서

상품코드

1776873

헬스케어용 빅데이터 시장 : 업계 동향과 예측 - 컴퍼넌트별, 하드웨어 유형별, 소프트웨어 유형별, 서비스 유형별, 전개 옵션별, 응용 분야별, 헬스케어 분야별, 최종 사용자별, 경제 상황별, 지역별, 주요 참가 기업별Big Data in Healthcare Market: Industry Trends and Global Forecasts - Distribution by Component, Hardware, Software, Service, Deployment Option, Application Area, Healthcare Vertical, End User, Economic Status, Geography and Leading Players |

||||||

세계의 헬스케어용 빅데이터 시장 규모는 2035년까지 예측 기간 동안 19.20%의 연평균 복합 성장률(CAGR)로 확대되어 현재 780억 달러에서 2035년까지 5,400억 달러로 성장할 것으로 예측됩니다.

시장 세분화는 시장 규모와 시장 기회를 다음 매개 변수로 구분합니다.

구성요소

- 하드웨어

- 소프트웨어

- 서비스

하드웨어 유형

- 스토리지 디바이스

- 네트워킹 인프라

- 서버

소프트웨어 유형

- 전자 의료 기록

- 진료 관리 소프트웨어

- 수익주기 관리 소프트웨어

- 워크포스 관리 소프트웨어

서비스 유형

- 기술적 분석

- 진단 애널리틱스

- 예측 분석

- 처방적 분석

배포 옵션

- 클라우드 기반

- On-Premise

응용 분야

- 임상 데이터 관리

- 재무관리

- 운용관리

- 집단 건강 관리

헬스케어 분야별

- 헬스케어 서비스

- 의료기기

- 의약품

- 기타

최종 사용자

- 클리닉

- 의료보험 대리점

- 병원

- 기타

경제 상황

- 고소득국

- 고중소득국

- 저중소득국

주요 지역

- 북미

- 유럽

- 아시아

- 라틴아메리카

- 중동 및 북아프리카

- 기타 지역

세계의 헬스케어용 빅데이터 시장 : 성장과 동향

헬스케어용 빅데이터란, 계속적으로 확대되어 기존 툴에서는 효율적으로 보존 및 처리할 수 없는 방대한 양의 데이터를 가리킵니다. 빅데이터는 방대한 양의 기존 데이터를 이용하여 환자에게 개인화된 케어를 제공하는 과제를 기회로 바꿉니다. 또한 빅데이터는 집단건강관리, 전자관리(EHR) 관리, 제약연구, 원격의료 및 원격건강 등 헬스케어 업계의 다양한 분야에서 이용할 수 있습니다.

헬스케어 영역에서 빅데이터의 보급이 진행되고 있기 때문에 헬스케어의 빅데이터 시장 규모에는 큰 임팩트가 있습니다. 게다가 빅데이터는 금융 분야에도 큰 영향을 미치고 있습니다.

세계의 헬스케어 빅데이터 시장 : 주요 인사이트

이 보고서는 세계의 헬스케어용 빅데이터 시장의 현재 상태를 파악하고 업계 내 잠재적 성장 기회를 확인합니다.

- 405개 이상의 기업이 헬스케어용 빅데이터 활용을 지원하기 위한 맞춤형 솔루션과 서비스를 제공하고 있으며, 그 중 약 55%가 데이터 관리 및 분석을 위한 데이터 웨어하우스와 데이터 레이크를 제공합니다.

- 서비스 제공업체의 대부분(65% 이상)은 북미, 특히 미국에 거점을 두고 있으며, 미국에 거점을 두는 서비스 제공업체의 대부분(56%)은 중견기업, 이어서 대기업(26%)입니다.

- 시장 상황는 매우 단편화되어 있어, 다른 지역 정세별을 거점으로 하는 신규 참가 기업과 기존 기업의 양쪽이 존재하는 것이 특징으로, 이러한 기업의 55% 가까이가 중견 기업입니다.

- 다양한 분석 모델이 임상 데이터, 업무 데이터, 재무 데이터로부터 인사이트를 도출하고 있습니다.

- 경쟁력을 높이기 위해 각 회사는 기존 능력을 적극적으로 업그레이드하고 새로운 능력을 추가하여 각각의 포트폴리오와 제휴 빅 데이터 제품을 강화하고 있습니다.

- 헬스케어 시장에서 빅데이터의 진화에 영향을 미치는 주요 촉진요인과 장벽을 분석함으로써, 이 영역에서의 현재와 미래의 비즈니스 기회를 보다 깊이 이해하기 위한 귀중한 인사이트를 얻을 수 있습니다.

- 클라우드 기반 솔루션과 서비스 채용 증가에 견인되어 헬스케어의 빅데이터 시장은 향후 12년간 CAGR 19.06%로 성장할 가능성이 높습니다.

- 예측되는 시장 기회는 다양한 유형의 하드웨어, 서비스, 소프트웨어 등 빅 데이터의 다양한 구성 요소에 잘 분산될 것으로 예측됩니다.

- 고소득국가는 업무관리를 최적화하기 위해 빅데이터 솔루션의 도입을 우선하고 헬스케어 업무의 효율성과 유효성 강화에 연결하여 시장수익을 견인하고 있습니다.

- 원격 의료 서비스와 맞춤형 의료에 대한 수요가 높아짐에 따라, 헬스케어에 있어서의 빅 데이터 시장은 다양한 지역에 거점을 두는 참가 기업에 유리한 기회를 제공합니다.

세계의 헬스케어용 빅데이터 시장 : 주요 부문

컴포넌트별로는 시장은 빅데이터 하드웨어, 빅데이터 소프트웨어, 빅데이터 서비스로 구분됩니다.

하드웨어 유형별로 시장은 스토리지 디바이스, 네트워크 인프라, 서버로 구분됩니다.

소프트웨어 유형별로 시장은 전자 의료 기록, 진료 관리 소프트웨어, 수익주기 관리 소프트웨어, 노동력 관리 소프트웨어로 구분됩니다.

서비스 유형별로 시장은 기술 분석, 진단 분석, 예측 분석 및 처방 분석으로 구분됩니다. 현재, 진단 애널리틱스 분야가 헬스케어용 빅데이터 시장에서 가장 높은 비율(30% 이상)을 차지하고 있습니다. 또한 처방적 분석 부문의 건강 관리에서 빅데이터 시장은 상대적으로 높은 CAGR로 성장할 가능성이 높습니다.

시장은 배포 옵션별로 클라우드 기반 배포와 On-Premise 배포로 구분됩니다. 이 개발이 제공하는 다양한 이점을 통해 현재 클라우드 기반 부문이 의료 분야의 빅 데이터 시장에서 최대 점유율(약 60%)을 차지하고 있습니다.

응용 분야별로는 시장은 임상 데이터 관리, 재무 관리, 운영 관리, 집단 건강 관리로 구분됩니다.

헬스케어 분야별로는 헬스케어 서비스, 의료기기, 의약품, 기타 분야로 구분됩니다.

최종 사용자별로 세계 시장은 클리닉, 의료보험기관, 병원 등으로 구분됩니다. 현재 병원 부문이 최대 시장 점유율(40% 이상)을 차지하고 있습니다.

경제 상황별로는 시장은 고소득국가, 고중소득국가, 저중소득국가로 구분됩니다.

주요 지역별로 보면 시장은 북미, 유럽, 아시아, 중동, 아프리카, 기타로 구분됩니다.

헬스케어용 빅데이터 시장 진출 기업 예

- Accenture

- Akka Technologies

- Altamira.ai

- Amazon Web Services

- Athena Global Technologies

- atom Consultancy Services(ACS)

- Avenga

- Happiest Minds

- InData Labs

- Itransition

- Kellton

- Keyrus

- Lutech

- Microsoft

- Nagarro

- Nous Infosystems

- NTT data

- Oracle

- Orange Mantra

- Oxagile

- Scalefocus

- Softweb Solutions

- Solix Technologies

- Spindox

- Tata Elxsi

- Teradata

- Trianz(formerly CBIG Consulting)

- Trigyn Technologies

- XenonStack

본 보고서에서는 세계의 헬스케어용 빅데이터 시장에 대해 조사했으며, 시장 개요와 함께, 컴퍼넌트별, 하드웨어 유형별, 소프트웨어 유형별, 서비스 유형별, 전개 옵션별, 응용 분야별, 헬스케어 분야별, 최종 사용자별, 경제 상황별, 지역별 동향 및 시장 진출기업 프로파일 등의 정보를 제공합니다.

목차

제1장 서문

제2장 조사 방법

- 장의 개요

- 조사의 전제

- 프로젝트 조사 방법

- 예측조사방법

- 견고한 품질관리

- 중요한 고려 사항

- 주요 시장 세분화

제3장 경제적 및 기타 프로젝트 특유의 고려 사항

- 장의 개요

- 시장 역학

제4장 주요 요약

제5장 소개

- 장의 개요

- 빅데이터 개요

- 빅데이터 분석

- 헬스케어용 빅데이터의 응용

- 장래의 전망

제6장 시장 상황

제7장 중요한 인사이트

- 장의 개요

- 의료 서비스 제공업체의 빅데이터 : 중요한 인사이트

제8장 기업 경쟁력 분석

- 장의 개요

- 전제 및 주요 파라미터

- 조사 방법

- 의료 서비스 제공업체의 빅데이터: 기업 경쟁력 분석

제9장 기업 프로파일 북미의 의료 서비스 제공업체의 빅데이터

- 장의 개요

- 북미의 주요 진출기업의 상세 프로파일

- Amazon Web Services

- Microsoft

- Oracle

- Teradata

- 북미의 다른 진출기업 프로파일

- Itransition

- Nous Infosystems

- Oxagile

- Softweb Solutions

- Solix Technologies

- Trianz(formerly CBIG Consulting)

제10장 기업 프로파일: 유럽의 의료 서비스 제공업체의 빅 데이터

- 장의 개요

- 유럽 주요 진출기업의 상세 프로파일

- Accenture

- Keyrus

- 유럽의 다른 진출기업 프로파일

- Akka Technologies

- Altamira.ai

- atom Consultancy Services(ACS)

- Avenga

- Lutech

- Nagarro

- Scalefocus

- Spindox

제11장 기업 프로파일: 아시아 및 세계 기타 지역에서 의료 서비스 제공업체의 빅 데이터

- 장의 개요

- 아시아 및 기타 국가의 주요 진출기업의 상세 프로파일

- Tata Elxsi

- Kellton

- 아시아 및 기타 국가의 기타 진출기업 프로파일

- Athena Global Technologies

- Happiest Minds

- InData Labs

- NTT data

- OrangeMantra

- Trigyn Technologies

- XenonStack

제12장 시장 영향 분석 : 촉진요인, 억제요인, 기회, 과제

제13장 헬스케어 시장에서의 세계 빅데이터

- 장의 개요

- 주요 전제와 조사 방법

- 헬스케어 시장에 있어서의 세계의 빅 데이터, 과거 동향(2018년 이후)과 예측(2035년까지)

- 주요 시장 세분화

제14장 헬스케어용 빅데이터 시장(컴포넌트별)

- 장의 개요

- 주요 전제와 조사 방법

- 헬스케어용 빅데이터 시장 : 컴포넌트별

- 데이터의 삼각측량과 검증

제15장 헬스케어용 빅데이터 시장(하드웨어별)

- 장의 개요

- 주요 전제와 조사 방법

- 헬스케어용 빅데이터 시장 : 하드웨어 유형별

- 데이터의 삼각측량과 검증

제16장 헬스케어용 빅데이터 시장(소프트웨어 유형별)

- 장의 개요

- 주요 전제와 조사 방법

- 헬스케어용 빅데이터 시장 : 소프트웨어 유형별

- 데이터의 삼각측량과 검증

제17장 헬스케어용 빅데이터 시장(서비스별)

- 장의 개요

- 주요 전제와 조사 방법

- 헬스케어용 빅데이터 시장 : 서비스 유형별

- 데이터의 삼각측량과 검증

제18장 헬스케어 시장에서의 빅 데이터(전개 옵션)

- 장의 개요

- 주요 전제와 조사 방법

- 헬스케어용 빅데이터 시장 : 전개 옵션별

- 데이터의 삼각측량과 검증

제19장 헬스케어용 빅데이터 시장(응용 분야별)

- 장의 개요

- 주요 전제와 조사 방법

- 헬스케어용 빅데이터 시장 : 응용 분야별

- 데이터의 삼각측량과 검증

제20장 헬스케어용 빅데이터 시장(헬스케어 분야별)

- 장의 개요

- 주요 전제와 조사 방법

- 헬스케어용 빅데이터 시장 : 헬스케어 분야별

- 데이터의 삼각측량과 검증

제21장 헬스케어용 빅데이터 시장(최종 사용자별)

- 장의 개요

- 주요 전제와 조사 방법

- 헬스케어용 빅데이터 시장 : 최종 사용자별

- 데이터의 삼각측량과 검증

제22장 헬스케어용 빅데이터 시장(경제 상황별)

- 장의 개요

- 주요 전제와 조사 방법

- 헬스케어용 빅데이터 시장 : 경제 상황별

- 데이터의 삼각측량과 검증

제23장 헬스케어용 빅데이터 시장(지역별)

- 장의 개요

- 주요 전제와 조사 방법

- 헬스케어용 빅데이터 시장 : 지역별 분포

- 데이터의 삼각측량과 검증

제24장 헬스케어용 빅데이터 시장, 주요 기업의 수익 예측

- 장의 개요

- 주요 전제와 조사 방법

- Microsoft

- Optum

- IBM

- Oracle

- Allscripts

제25장 결론

제26장 주요 인사이트

제27장 부록 I: 표 형식 데이터

제28장 부록 II: 기업 및 조직 목록

JHS 25.08.01GLOBAL BIG DATA IN HEALTHCARE MARKET: OVERVIEW

As per Roots Analysis, the big data in healthcare market is estimated to grow from USD 78 billion in the current year to USD 540 billion by 2035, at a CAGR of 19.20% during the forecast period, till 2035.

The market sizing and opportunity analysis has been segmented across the following parameters:

Component

- Hardware

- Software

- Services

Type of Hardware

- Storage Devices

- Networking Infrastructure

- Servers

Type of Software

- Electronic Health Record

- Practice Management Software

- Revenue Cycle Management Software

- Workforce Management Software

Type of Service

- Descriptive Analytics

- Diagnostic Analytics

- Predictive Analytics

- Prescriptive Analytics

Deployment Option

- Cloud-based

- On-premises

Application Area

- Clinical Data Management

- Financial Management

- Operational Management

- Population Health Management

Healthcare Vertical

- Healthcare Services

- Medical Devices

- Pharmaceuticals

- Other Verticals

End User

- Clinics

- Health Insurance Agencies

- Hospitals

- Other End Users

Economic Status

- High Income Countries

- Upper-Middle Income Countries

- Lower-Middle Income Countries

Key Geographical Regions

- North America

- Europe

- Asia

- Latin America

- Middle East and North Africa

- Rest of the World

GLOBAL BIG DATA IN HEALTHCARE MARKET: GROWTH AND TRENDS

Big Data in healthcare refers to the vast amount of data that is continuously expanding and cannot be efficiently stored or processed using traditional tools. Notably, over the past few years, the popularity of big data / big data analytics tools and technologies has increased exponentially in healthcare due to the large volumes of data being generated in this domain. Big data in healthcare turns the challenges into opportunities to provide personalized care to the patients by using huge amounts of existing data. Further, big data can be used across different verticals of healthcare industry, such as in population health management, Electronic Health Record (EHR) management, pharmaceutical research, and telemedicine and telehealth.

Owing to the increasing popularity of big data in healthcare domain, there is a huge impact of big data in healthcare market size. Big data analysis is used not only in healthcare market but also used in different sectors for the growth of the organization and to forecast future trends using machine learning and artificial intelligence. Moreover, big data has also had a considerable impact on the financial sector. Big data in the healthcare domain has several advantages and the integration of predictive analytics and machine learning algorithms with big data can enable early detection of diseases, personalized treatment plans, and precision medicine.

GLOBAL BIG DATA IN HEALTHCARE MARKET: KEY INSIGHTS

The report delves into the current state of global big data in healthcare market and identifies potential growth opportunities within industry. Some key findings from the report include:

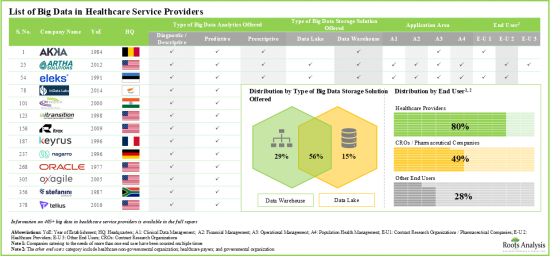

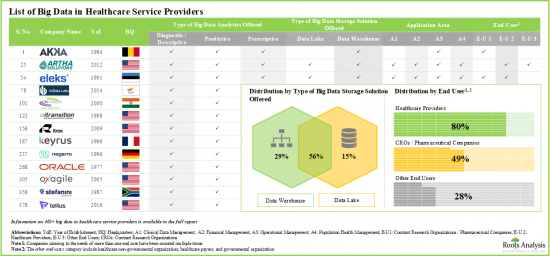

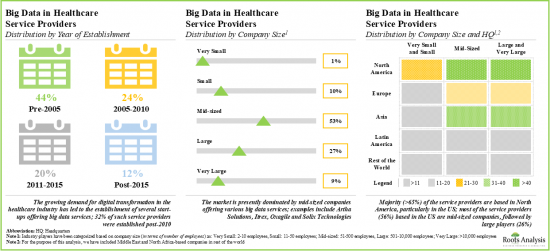

- More than 405 players claim to offer customized solutions and services to support big data in healthcare initiatives, with around 55% offering data warehouses and data lakes for data management and analytics.

- Majority (>65%) of the service providers are based in North America, particularly in the US; most of the service providers (56%) based in the US are mid-sized companies, followed by large players (26%).

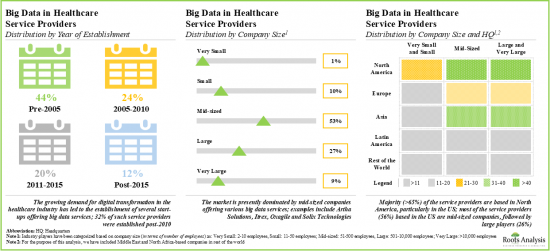

- The market landscape is highly fragmented, featuring the presence of both new entrants and established players based across different geographical regions; close to 55% of such players are mid-sized companies.

- Various analytical models derive insights from clinical, operational and financial data; 23% of the players offer a comprehensive software suite of big data analytics including predictive, prescriptive, and descriptive analytics.

- In pursuit of building a competitive edge, players are actively upgrading their existing capabilities and adding new competencies in order to augment their respective portfolios and affiliated big data offerings.

- By analyzing the key drivers and barriers affecting the evolution of big data in healthcare market, valuable insights can be generated leading to a deeper understanding of the current and future opportunities within this domain.

- Driven by the increasing adoption of cloud-based solutions and services, the big data in healthcare market is likely to grow at a CAGR of 19.06% over the next 12 years.

- The projected market opportunity is anticipated to be well distributed across different components of big data, including various types of hardware, services and software.

- High-income countries are driving market revenues by prioritizing the deployment of big data solutions to optimize operational management, leading to enhanced efficiency and effectiveness in healthcare operations.

- With the rise in demand for telehealth services and personalized medicine, the big data in healthcare market presents lucrative opportunities for players based across various geographies.

GLOBAL BIG DATA IN HEALTHCARE MARKET: KEY SEGMENTS

Hardware Segment Occupies the Largest Share of the Big Data in Healthcare Market

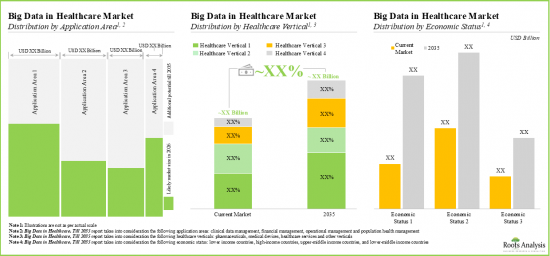

Based on the component, the market is segmented into big data hardware, big data software and big data services. At present, hardware segment holds the maximum (>40%) share of the global big data in healthcare market. Additionally, due to the rising adoption of advanced technologies, and ongoing investments in innovation, the hardware segment is likely to grow at a faster pace compared to the other segments.

By Type of Hardware, Storage Devices Segment is the Fastest Growing Segment of the Global Big Data in Healthcare Market

Based on the type of hardware, the market is segmented into storage devices, networking infrastructure and servers. Currently, storage devices segment captures the highest proportion (~60%) of the big data in healthcare market. Further, this segment is likely to grow at a relatively higher CAGR.

Electronic Health Record Segment Occupy the Largest Share of the Big Data in Healthcare Market

Based on the type of software, the market is segmented into electronic health record, practice management software, revenue cycle management software, and workforce management software. At present, the electronic health record segment holds the maximum share (>45%) of the big data in healthcare market. In addition, workforce management software segment is likely to grow at a relatively higher CAGR.

By Type of Service, the Diagnostic Analytics Segment is the Fastest Growing Segment of the Big Data in Healthcare Market During the Forecast Period

Based on the type of service, the market is segmented into descriptive analytics, diagnostic analytics, predictive analytics, and prescriptive analytics. Currently, the diagnostic analytics segment captures the highest proportion (>30%) of the big data in healthcare market. Further, it is worth highlighting that the big data in healthcare market for prescriptive analytics segment is likely to grow at a relatively higher CAGR.

Cloud-based Segment Account for the Largest Share of the Global Big Data in Healthcare Market

Based on the deployment option, the market is segmented into cloud-based deployment and on-premises deployment. Currently, cloud-based segment holds the maximum share (~60%) of the big data in healthcare market owing to the various benefits offered by cloud-based deployment, such as scalability, flexibility, cost-effectiveness, ease of implementation and maintenance, and data accessibility. This trend is likely to remain the same in the coming years.

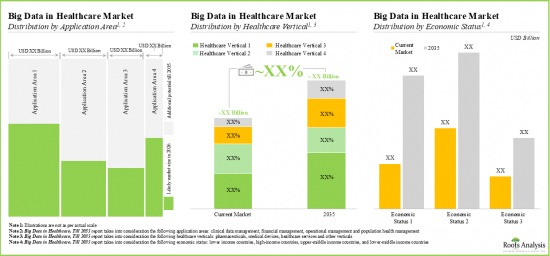

By Application Area, Operational Management Segment is Likely to Dominate the Big Data in Healthcare Market

Based on the application area, the market is segmented into clinical data management, financial management, operational management, and population health management. At present, the operational management segment holds the maximum share (>30%) of the big data in healthcare market. Additionally, the population health management segment is expected to show the highest growth potential during the forecast period, growing at a higher CAGR, compared to the other segments.

The Healthcare Services Segment in Healthcare Vertical Occupy the Largest Share of the Big Data in Healthcare Market

Based on the healthcare vertical, the market is segmented into healthcare services, medical devices, pharmaceuticals, and other verticals. While healthcare services segment is expected to be the primary driver of the overall market, it is worth highlighting that the global big data in healthcare market for medical devices segment is likely to grow at a relatively higher CAGR of more than 20%.

Currently, Hospitals Segment Holds the Largest Share of the Big Data in Healthcare Market

Based on end users, the global market is segmented into clinics, health insurance agencies, hospitals, and other end users. Currently, the hospitals segment holds the largest market share (>40%). However, the big data in healthcare market for clinics segment is expected to witness substantial growth in the coming years.

By Economic Status, the Upper-Middle Income Countries Segment is the Fastest Growing Segment of the Big Data in Healthcare Market During the Forecast Period

Based on the economic status, the market is segmented into high income countries, upper-middle income countries, and lower-middle income countries. Currently, the high-income countries segment captures the highest proportion (~85%) of the big data in healthcare market. Further, it is worth highlighting that the big data in healthcare market for upper-middle income countries segment is likely to grow at a relatively higher CAGR.

North America Accounts for the Largest Share of the Market

Based on key geographical regions, the market is segmented into North America, Europe, Asia, Middle East and North Africa, Latin America and Rest of the World. Currently, North America (~60%) dominates the big data in healthcare market and accounts for the largest revenue share. However, the market in Asia-Pacific is expected to grow at a higher CAGR.

Example Players in the Big Data in Healthcare Market

- Accenture

- Akka Technologies

- Altamira.ai

- Amazon Web Services

- Athena Global Technologies

- atom Consultancy Services (ACS)

- Avenga

- Happiest Minds

- InData Labs

- Itransition

- Kellton

- Keyrus

- Lutech

- Microsoft

- Nagarro

- Nous Infosystems

- NTT data

- Oracle

- Orange Mantra

- Oxagile

- Scalefocus

- Softweb Solutions

- Solix Technologies

- Spindox

- Tata Elxsi

- Teradata

- Trianz (formerly CBIG Consulting)

- Trigyn Technologies

- XenonStack

PRIMARY RESEARCH OVERVIEW

The opinions and insights presented in this study were influenced by discussions conducted with multiple stakeholders. The research report features detailed transcripts of interviews conducted with the following industry stakeholders:

- Chief Executive Officer and Founder, Company A

- Chief Executive Officer and Co-Founder, Company B

- Chief People Officer and Co-Founder, Company C

- Vice President, Company D

- Vice President, Company E

- Business Head, Company F

- Senior IT Inside Sales Lead, Company G

- Senior Manager, Company H

- Delivery Manager, Company I

- Strategy, Research and Analyst Relations Manager, Company J

- Business Development Manager, Company K

- Business Development Associate, Company L

- Business Development Specialist Advisor, Company M

- Business Development Executive, Company N

GLOBAL BIG DATA IN HEALTHCARE MARKET: RESEARCH COVERAGE

- Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the global big data in healthcare market, focusing on key market segments, including [A] component, [B] type of hardware, [C] type of software, [D] type of service, [E] deployment option, [F] application area, [G] healthcare vertical, [H] end user, [I] economic status and [J] key geographical regions.

- Market Landscape: A comprehensive evaluation of big data in healthcare service providers, considering various parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters, [D] business model, [E] type of offering, [F] type of big data analytics offered, [G] type of big data storage solution offered, [H] deployment option, [I] application area and [J] end user.

- Company Competitiveness Analysis: A comprehensive competitive analysis of big data in healthcare service providers, examining factors, such as [A] supplier strength and [B] portfolio strength.

- Company Profiles: In-depth profiles of companies engaged in offering big data analytics solutions across various geographies, focusing on [A] company overviews, [B] financial information (if available), [C] big data analytics offerings and capabilities and [D] recent developments and an informed future outlook.

- Market Impact Analysis: A thorough analysis of various factors, such as drivers, restraints, opportunities, and existing challenges that are likely to impact market growth.

KEY QUESTIONS ANSWERED IN THIS REPORT

- How many companies are currently engaged in this market?

- Which are the leading companies in this market?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

REASONS TO BUY THIS REPORT

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

ADDITIONAL BENEFITS

- Complimentary PPT Insights Packs

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2.RESEARCH METHODOLOGY

- 2.1.Chapter Overview

- 2.2.Research Assumptions

- 2.3.Project Methodology

- 2.4.Forecast Methodology

- 2.5.Robust Quality Control

- 2.6.Key Considerations

- 2.6.1.Demographics

- 2.6.2.Economic Factors

- 2.6.3.Government Regulations

- 2.6.4. Supply Chain

- 2.6.5.COVID Impact / Related Factors

- 2.6.6. Market Access

- 2.6.7. Healthcare Policies

- 2.6.8. Industry Consolidation

- 2.7. Key Market Segmentations

3. ECONOMIC AND OTHER PROJECT SPECIFIC CONSIDERATIONS

- 3.1. Chapter Overview

- 3.2. Market Dynamics

- 3.2.1. Time Period

- 3.2.1.1. Historical Trends

- 3.2.1.2. Current and Forecasted Estimates

- 3.2.2. Currency Coverage

- 3.2.2.1. Major Currencies Affecting the Market

- 3.2.2.2. Impact of Currency Fluctuations on the Industry

- 3.2.3. Foreign Exchange Impact

- 3.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

- 3.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 3.2.4. Recession

- 3.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 3.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 3.2.5. Inflation

- 3.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 3.2.5.2. Potential Impact of Inflation on the Market Evolution

- 3.2.1. Time Period

4. EXECUTIVE SUMMARY

- 4.1. Chapter Overview

5. INTRODUCTION

- 5.1. Chapter Overview

- 5.2. Overview of Big Data

- 5.2.1. Types of Big Data

- 5.2.1.1. Structured Data

- 5.2.1.2. Unstructured Data

- 5.2.1.3. Semi-Structured Data

- 5.2.2. Management and Storage of Big Data

- 5.2.1. Types of Big Data

- 5.3. Big Data Analytics

- 5.3.1. Types of Big Data Analytics

- 5.3.1.1. Descriptive Analytics

- 5.3.1.2. Diagnostic Analytics

- 5.3.1.3. Predictive Analytics

- 5.3.1.4. Prescriptive Analytics

- 5.3.1. Types of Big Data Analytics

- 5.4. Applications of Big Data in Healthcare

- 5.5. Future Perspective

6. OVERALL MARKET LANDSCAPE

- 6.1. Chapter Overview

- 6.2. Big Data in Healthcare Service Providers: Overall Market Landscape

- 6.3. Analysis by Year of Establishment

- 6.4. Analysis by Company Size

- 6.5. Analysis by Location of Headquarters

- 6.6. Analysis by Type of Business Model

- 6.7. Analysis by Type of Offering

- 6.8. Analysis by Type of Big Data Analytics Offered

- 6.9. Analysis by Type of Big Data Storage Solution Offered

- 6.10. Analysis by Deployment Option

- 6.11. Analysis by Application Area

- 6.12. Analysis by End User

7. KEY INSIGHTS

- 7.1. Chapter Overview

- 7.2. Big Data in Healthcare Service Providers: Key Insights

- 7.2.1. Analysis by Year of Establishment and Company Size

- 7.2.2. Analysis by Company Size and Location of Headquarters

- 7.2.3. Analysis by Type of Offering and Company Size

- 7.2.4. Analysis by Type of Big Data Analytics Offered and Application Area

- 7.2.5. Analysis by Company Size, Application Area and End User

8. COMPANY COMPETITIVENSS ANALYSIS

- 8.1. Chapter Overview

- 8.2. Assumptions and Key Parameters

- 8.3. Methodology

- 8.4. Big Data in Healthcare Service Providers: Company Competitiveness Analysis

- 8.4.1. Big Data in Healthcare Service Providers based in North America

- 8.4.1.1. Small Service Providers based in North America

- 8.4.1.2. Mid-sized Service Providers based in North America

- 8.4.1.3. Large Service Providers based in North America

- 8.4.1.4. Very LargeService Providers based in North America

- 8.4.2. Big Data in Healthcare Service Providers based in Europe

- 8.4.2.1. Small Service Providers based in Europe

- 8.4.2.2. Mid-sized Service Providers based in Europe

- 8.4.2.3. Large and Very Large Service Providers based in Europe

- 8.4.3. Big Data in Healthcare Service Providers based in Asia and Rest of the World

- 8.4.3.1. Small Service Providers based in Asia and Rest of the World

- 8.4.3.2. Mid-sized Service Providers based in Asia and Rest of the World

- 8.4.3.3. Large Service Providers based in Asia and Rest of the World

- 8.4.3.4. Very Large Service Providers based in Asia and Rest of the World

- 8.4.1. Big Data in Healthcare Service Providers based in North America

9. COMPANY PROFILES: BIG DATA IN HEALTHCARE SERVICE PROVIDERS IN NORTH AMERICA

- 9.1. Chapter Overview

- 9.2. Detailed Company Profiles of Leading Players in North America

- 9.2.1. Amazon Web Services

- 9.2.1.1. Company Overview

- 9.2.1.2. Financial Information

- 9.2.1.3. Big Data Offerings and Capabilities

- 9.2.1.4. Recent Developments and Future Outlook

- 9.2.2. Microsoft

- 9.2.2.1. Company Overview

- 9.2.2.2. Financial Information

- 9.2.2.3. Big Data Offerings and Capabilities

- 9.2.2.4. Recent Developments and Future Outlook

- 9.2.3. Oracle

- 9.2.3.1. Company Overview

- 9.2.3.2. Financial Information

- 9.2.3.3. Big Data Offerings and Capabilities

- 9.2.3.4. Recent Developments and Future Outlook

- 9.2.4. Teradata

- 9.2.4.1. Company Overview

- 9.2.4.2. Financial Information

- 9.2.4.3. Big Data Offerings and Capabilities

- 9.2.4.4. Recent Developments and Future Outlook

- 9.2.1. Amazon Web Services

- 9.3. Short Company Profiles of Other Prominent Players in North America

- 9.3.1. Itransition

- 9.3.1.1. Company Overview

- 9.3.1.2. Big Data Offerings and Capabilities

- 9.3.2 Nous Infosystems

- 9.3.2.1. Company Overview

- 9.3.2.2. Big Data Offerings and Capabilities

- 9.3.3 Oxagile

- 9.3.3.1. Company Overview

- 9.3.3.2. Big Data Offerings and Capabilities

- 9.3.4 Softweb Solutions

- 9.3.4.1. Company Overview

- 9.3.4.2. Big Data Offerings and Capabilities

- 9.3.5 Solix Technologies

- 9.3.5.1. Company Overview

- 9.3.5.2. Big Data Offerings and Capabilities

- 9.3.6 Trianz (formerly CBIG Consulting)

- 9.3.6.1. Company Overview

- 9.3.6.2. Big Data Offerings and Capabilities

- 9.3.1. Itransition

10. COMPANY PROFILES: BIG DATA IN HEALTHCARE SERVICE PROVIDERS IN EUROPE

- 10.1. Chapter Overview

- 10.2. Detailed Company Profiles of Leading Players in Europe

- 10.2.1. Accenture

- 10.2.1.1. Company Overview

- 10.2.1.2. Financial Information

- 10.2.1.3. Big Data Offerings and Capabilities

- 10.2.1.4. Recent Developments and Future Outlook

- 10.2.2. Keyrus

- 10.2.2.1. Company Overview

- 10.2.2.2. Financial Information

- 10.2.2.3. Big Data Offerings and Capabilities

- 10.2.2.4. Recent Developments and Future Outlook

- 10.2.1. Accenture

- 10.3. Short Company Profiles of Other Prominent Players in Europe

- 10.3.1. Akka Technologies

- 10.3.1.1. Company Overview

- 10.3.1.2. Big Data Offerings and Capabilities

- 10.3.2 Altamira.ai

- 10.3.2.1. Company Overview

- 10.3.2.2. Big Data Offerings and Capabilities

- 10.3.3 atom Consultancy Services (ACS)

- 10.3.3.1. Company Overview

- 10.3.3.2. Big Data Offerings and Capabilities

- 10.3.4 Avenga

- 10.3.4.1. Company Overview

- 10.3.4.2. Big Data Offerings and Capabilities

- 10.3.5 Lutech

- 10.3.5.1. Company Overview

- 10.3.5.2. Big Data Offerings and Capabilities

- 10.3.6 Nagarro

- 10.3.6.1. Company Overview

- 10.3.6.2. Big Data Offerings and Capabilities

- 10.3.7 Scalefocus

- 10.3.7.1. Company Overview

- 10.3.7.2. Big Data Offerings and Capabilities

- 10.3.8 Spindox

- 10.3.8.1. Company Overview

- 10.3.8.2. Big Data Offerings and Capabilities

- 10.3.1. Akka Technologies

11. COMPANY PROFILES: BIG DATA IN HEALTHCARE SERVICE PROVIDERS IN ASIA AND REST OF THE WORLD

- 11.1. Chapter Overview

- 11.2. Detailed Company Profiles of Leading Players in Asia and Rest of the World

- 11.2.1. Tata Elxsi

- 11.2.1.1. Company Overview

- 11.2.1.2. Big Data Offerings and Capabilities

- 11.2.1.3. Recent Developments and Future Outlook

- 11.2.2. Kellton

- 11.2.2.1. Company Overview

- 11.2.2.2. Financial Information

- 11.2.2.3. Big Data Offerings and Capabilities

- 11.2.2.4. Recent Developments and Future Outlook

- 11.2.1. Tata Elxsi

- 11.3. Short Company Profiles of Other Prominent Players in Asia and Rest of the World

- 11.3.1. Athena Global Technologies

- 11.3.1.1. Company Overview

- 11.3.1.2. Big Data Offerings and Capabilities

- 11.3.2 Happiest Minds

- 11.3.2.1. Company Overview

- 11.3.2.2. Big Data Offerings and Capabilities

- 11.3.3 InData Labs

- 11.3.3.1. Company Overview

- 11.3.3.2. Big Data Offerings and Capabilities

- 11.3.4 NTT data

- 11.3.4.1. Company Overview

- 11.3.4.2. Big Data Offerings and Capabilities

- 11.3.5 OrangeMantra

- 11.3.5.1. Company Overview

- 11.3.5.2. Big Data Offerings and Capabilities

- 11.3.6 Trigyn Technologies

- 11.3.6.1. Company Overview

- 11.3.6.2. Big Data Offerings and Capabilities

- 11.3.7 XenonStack

- 11.3.7.1. Company Overview

- 11.3.7.2. Big Data Offerings and Capabilities

- 11.3.1. Athena Global Technologies

12. MARKET IMPACT ANALYSIS: DRIVERS, RESTRAINTS, OPPORTUNITIES AND CHALLENGES

- 12.1. Chapter Overview

- 12.2. Market Drivers

- 12.3. Market Restraints

- 12.4. Market Opportunities

- 12.5. Market Challenges

- 12.6. Conclusion

13. GLOBAL BIG DATA IN HEALTHCARE MARKET

- 13.1. Chapter Overview

- 13.2. Key Assumptions and Methodology

- 13.3. Global Big Data in Healthcare Market, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 13.3.1. Scenario Analysis

- 13.3.1.1. Conservative Scenario

- 13.3.1.2. Optimistic Scenario

- 13.3.1. Scenario Analysis

- 13.4. Key Market Segmentations

14. BIG DATA IN HEALTHCARE MARKET, BY COMPONENT

- 14.1. Chapter Overview

- 14.2. Key Assumptions and Methodology

- 14.3. Big Data in Healthcare Market: Distribution by Component

- 14.3.1. Big Data Hardware: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 14.3.2. Big Data Software: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 14.3.3. Big Data Services: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 14.4. Data Triangulation and Validation

15. BIG DATA IN HEALTHCARE MARKET, BY TYPE OF HARDWARE

- 15.1. Chapter Overview

- 15.2. Key Assumptions and Methodology

- 15.3. Big Data in Healthcare Market: Distribution by Type of Hardware

- 15.3.1. Storage Devices: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 15.3.2. Servers: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 15.3.3. Networking Infrastructure: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 15.4. Data Triangulation and Validation

16. BIG DATA IN HEALTHCARE MARKET, BY TYPE OF SOFTWARE

- 16.1. Chapter Overview

- 16.2. Key Assumptions and Methodology

- 16.3. Big Data in Healthcare Market: Distribution by Type of Software

- 16.3.1. Electronic Health Record: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 16.3.2. Revenue Cycle Management Software: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 16.3.3. Practice Management Software: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 16.3.4. Workforce Management Software: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 16.4. Data Triangulation and Validation

17. BIG DATA IN HEALTHCARE MARKET, BY TYPE OF SERVICE

- 17.1. Chapter Overview

- 17.2. Key Assumptions and Methodology

- 17.3. Big Data in Healthcare Market: Distribution by Type of Services

- 17.3.1. Diagnostic Analytics: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 17.3.2. Descriptive Analytics: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 17.3.3. Predictive Analytics: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 17.3.4. Prescriptive Analytics: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 17.4. Data Triangulation and Validation

18. BIG DATA IN HEALTHCARE MARKET, BY DEPLOYMENT OPTION

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Big Data in Healthcare Market: Distribution by Deployment Option

- 18.3.1. Cloud-based Deployment: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 18.3.2. On-premises Deployment: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 18.4. Data Triangulation and Validation

19. BIG DATA IN HEALTHCARE MARKET, BY APPLICATION AREA

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Big Data in Healthcare Market: Distribution by Application Area

- 19.3.1. Operational Management: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.3.2. Clinical Data Management: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.3.3. Financial Management: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.3.4. Population Health Management: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.4. Data Triangulation and Validation

20. BIG DATA IN HEALTHCARE MARKET, BY HEALTHCARE VERTICAL

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Big Data in Healthcare Market: Distribution by Healthcare Vertical

- 20.3.1. Healthcare Services: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.3.2. Pharmaceuticals: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.3.3. Medical Devices: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.3.4. Other Verticals: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.4. Data Triangulation and Validation

21. BIG DATA IN HEALTHCARE MARKET, BY END USER

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Big Data in Healthcare Market: Distribution by End User

- 21.3.1. Hospitals: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.3.2. Health Insurance Agencies: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.3.3. Clinics: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.3.4. Other End Users: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.4. Data Triangulation and Validation

22. BIG DATA IN HEALTHCARE MARKET, BY ECONOMIC STATUS

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Big Data in Healthcare Market: Distribution by Economic Status

- 22.3.1. High Income Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.1. US: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.2. Canada: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.3. Germany: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.4. UK: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.5. UAE: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.6. South Korea: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.7. France: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.8. Australia: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.9. New Zealand: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.10. Italy: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.11. Saudi Arabia: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.12. Nordic Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.2. Upper-Middle Income Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.2.1. China: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.2.2. Russia: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.2.3. Brazil: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.2.4. Japan: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.2.5. South Africa: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.3. Lower-Middle Income Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.3.1. India: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1. High Income Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.4. Data Triangulation and Validation

23. BIG DATA IN HEALTHCARE MARKET, BY GEOGRAPHY

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Big Data in Healthcare Market: Distribution by Geography

- 23.3.1. North America: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.3.2. Europe: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.3.3. Asia: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.3.4. Middle East and North Africa: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.3.5. Latin America: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.3.6. Rest of the World: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.4. Data Triangulation and Validation

24. BIG DATA IN HEALTHCARE MARKET, REVENUE FORECAST OF LEADING PLAYERS

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Microsoft: Revenue Generated from Big Data in Healthcare Offerings Since FY 2018

- 24.4. Optum: Revenue Generated from Big Data in Healthcare Offerings Since FY 2018

- 24.5. IBM: Revenue Generated from Big Data in Healthcare Offerings Since FY 2018

- 24.6. Oracle: Revenue Generated from Big Data in Healthcare Offerings Since FY 2018

- 24.7. Allscripts: Revenue Generated from Big Data in Healthcare Offerings Since FY 2018

25. CONCLUSION

- 25.1. Chapter Overview

26. EXECUTIVE INSIGHTS

- 26.1. Chapter Overview

- 26.2. Company A

- 26.2.1. Company Snapshot

- 26.2.2. Interview Transcript

- 26.3. Company B

- 26.3.1. Company Snapshot

- 26.3.2. Interview Transcript

- 26.4. Company C

- 26.4.1. Company Snapshot

- 26.4.2. Interview Transcript

- 26.5. Company D

- 26.5.1. Company Snapshot

- 26.5.2. Interview Transcrip

- 26.6. Company E

- 26.6.1. Company Snapshot

- 26.6.2. Interview Transcript

- 26.7. Company F

- 26.7.1. Company Snapshot

- 26.7.2. Interview Transcript

- 26.8. Company G

- 26.8.1. Company Snapshot

- 26.8.2. Interview Transcript

- 26.9. Company H

- 26.9.1. Company Snapshot

- 26.9.2. Interview Transcript

- 26.10. Company I

- 26.10.1. Company Snapshot

- 26.10.2. Interview Transcript

- 26.11. Company J

- 26.11.1. Company Snapshot

- 26.11.2. Interview Transcript

- 26.12. Company K

- 26.12.1. Company Snapshot

- 26.12.2. Interview Transcript

- 26.13. Company L

- 26.13.1. Company Snapshot

- 26.13.2. Interview Transcript

- 26.14. Company M

- 26.14.1. Company Snapshot

- 26.14.2. Interview Transcript

- 26.15. Company N

- 26.15.1. Company Snapshot

- 26.15.2. Interview Transcript