|

시장보고서

상품코드

1993593

호주의 약물전달 기기 시장 : 업계 동향과 세계 예측(-2035년) - 제품 유형별, 응용 분야별, 최종사용자별Australia Drug Delivery Devices Market: Industry Trends and Global Forecasts, till 2035 - Distribution by Type of Product, Application Area and End-user |

||||||

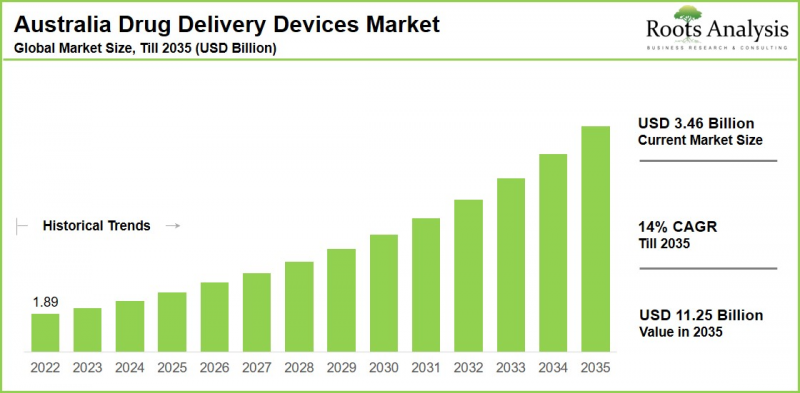

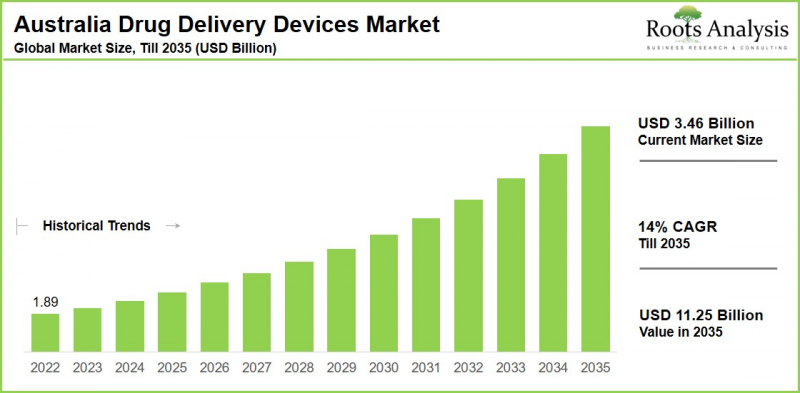

호주의 약물전달 기기 시장 규모는 현재 34억 6,000만 달러에서 2035년까지 112억 5,000만 달러에 달할 것으로 추정되고, 2035년까지 예측 기간 동안 CAGR로 14%의 성장이 전망됩니다.

호주의 약물전달 기기 시장 : 성장과 트렌드

약물전달 기기는 천식, 만성폐쇄성폐질환(COPD), 당뇨병, 암, 심혈관질환, 만성 통증 등 다양한 질환의 치료에 활용되고 있습니다. 이러한 장치는 약물의 정확하고 정확한 투여를 가능하게 하여 약물의 효과와 환자의 복약 순응도를 높이는 동시에 부작용을 감소시킵니다. 최근 약물전달 기기의 발전은 스마트 커넥티비티, 나노기술, 표적 지향성 방출에 초점을 맞추고 있으며, 환자의 복약 순응도를 높이고 정확한 투여를 실현하고 있습니다.

호주의 약물전달 기기 시장은 당뇨병 등 만성질환 유병률 증가와 더불어 고령화에 따른 심혈관질환 및 자가면역질환의 증가로 인해 꾸준한 성장세를 보이고 있습니다. 이러한 요인으로 인해 주사제, 흡입기, 서방형 임플란트, 자가주사기 등 정확하고 사용하기 쉬운 디바이스에 대한 수요가 증가하고 있습니다. 또한, 연결성을 갖춘 스마트 자가주사기, 무통 경피투여가 가능한 마이크로니들 패치, 생분해성 임플란트, AI를 활용한 실시간 투약이 가능한 웨어러블 펌프, 무침 시스템과 같은 기술의 발전은 약물 순응도와 효과를 높이는 한편, 호주의 디지털 헬스 전략과 홈케어 프로그램을 지원하고 있으며, 이러한 요소들이 모여 호주 약물전달 기기 시장의 성장을 촉진하고 있습니다.

성장 촉진요인 : 시장 확대의 전략적 원동력

호주의 약물전달 기기 시장은 광범위한 인구통계학적, 기술적, 정책적 변화를 반영하는 여러 가지 상호 연관된 성장 촉진요인에 의해 주도되고 있습니다. 또한, 만성질환, 암, 심혈관질환의 유병률이 급증함에 따라 환자 예후를 개선하고 입원율을 낮추기 위해 자가주사기 및 서방형 임플란트와 같은 효율적인 표적 지향성 전달 시스템에 대한 수요가 급증하고 있습니다. 스마트 커넥티드 흡입기, 경피흡수율을 높이는 마이크로니들 패치, 실수를 최소화하는 프리필드 시린지, 실시간 모니터링에 사용되는 AI 통합 웨어러블 펌프와 같은 기술 발전은 호주의 디지털 헬스 생태계와 조화를 이루며 복약 순응도 및 유효성을 향상시킵니다. 높이고 있습니다. 정부의 지원, 의료 인프라에 대한 투자, 원격의료를 촉진하는 정책은 이 지역에서 약물전달 기기의 채택을 더욱 가속화하고 있습니다.

시장 과제 : 진행을 가로막는 심각한 장벽

이러한 호재에도 불구하고 시장 확대와 시장 진입을 가로막는 심각한 도전에 직면해 있습니다. Therapeutic Goods Administration(TGA)의 엄격한 규제로 인해 승인 절차가 길어지고 비용도 많이 소요됩니다. Class III 의료기기의 경우, 비용이 9만 5,000 호주달러를 초과하는 경우가 많으며, 2026년까지 단계적으로 규정 준수가 도입되기 때문에 혁신가들에게 장벽이 되어 제품 출시가 늦어지고 있습니다. 첨단 기술 개발 및 획득에 드는 비용이 높기 때문에 특히 지방에서는 저렴한 가격의 제공과 접근성이 제한되어 있습니다. 또한, PBS(Pharmaceutical Benefits Scheme) 등의 제도에 의한 상환의 장애물이 신규 의료기기의 시장 침투를 복잡하게 만들고 있습니다. 벡톤 디킨슨(Becton Dickinson), 노바티스(Novartis)와 같은 주요 기업과의 치열한 경쟁과 함께 의료진과 환자들 사이에서 불필요한 천자 사고 감소와 같은 이점에 대한 인식이 낮기 때문에 채택률이 둔화되고 있습니다. 또한, 2025년까지 오젬픽과 같은 GLP-1 제제의 공급 부족이 지속될 것으로 예상되는 공급망 취약성과 전문화된 제조 공정의 필요성이 자본 집약적인 이 부문의 리스크를 증가시키고 있습니다.

호주의 약물전달 기기 시장에 대해 조사했으며, 시장 규모 추정과 기회 분석, 경쟁 상황, 기업 프로파일 등의 정보를 전해드립니다.

목차

제1장 서문

제2장 조사 방법

제3장 시장 역학

제4장 거시경제 지표

제5장 주요 요약

제6장 소개

제7장 시장 구도

제8장 기업 개요 : 호주의 약물전달 기기 시장

제9장 파트너십과 제휴

제10장 시장의 영향 분석

제11장 호주의 약물전달 기기 시장

제12장 호주의 약물전달 기기 시장 : 제품 유형별

제13장 호주의 약물전달 기기 시장 : 응용 분야별

제14장 호주의 약물전달 기기 시장 : 최종사용자별

제15장 결론

제16장 부록 I : 표형식 데이터

제17장 부록 II : 기업과 조직 리스트

KSMAustralia Drug Delivery Devices Market: Overview

As per Roots Analysis, the Australia drug delivery devices market is estimated to grow from USD 3.46 billion in the current year to USD 11.25 billion by 2035 at a CAGR of 14% during the forecast period, till 2035.

Australia Drug Delivery Devices Market: Growth and Trends

Drug delivery devices are utilized for a variety of conditions, including asthma, chronic obstructive pulmonary disease (COPD), diabetes, cancer, cardiovascular diseases, and chronic pain. These devices facilitate accurate and focused administration of medications, enhancing effectiveness and patient adherence while reducing adverse effects. Recent advancements in drug delivery devices focus on smart connectivity, nanotechnology, and targeted release for better patient compliance and precision dosing.

The market for drug delivery devices in Australia is showing consistent growth, driven by the increasing prevalence of chronic illnesses such as diabetes along with growing cardiovascular and autoimmune disorders in an aging demographic. Such factors elevate the need for accurate, user-friendly devices like injectables, inhalers, sustained-release implants, and auto-injectors. In addition, advancements in technology, such as smart auto-injectors with connectivity, microneedle patches for painless transdermal delivery, biodegradable implants, wearable pumps that use AI for real-time dosing, and needle-free systems, are enhancing adherence and effectiveness while supporting Australia's digital health strategy and home care programs, collectively promoting the growth of the drug delivery devices market in Australia.

Growth Drivers: Strategic Enablers of Market Expansion

Australia's drug delivery devices market is propelled by several interconnected growth drivers that reflect broader demographic, technological, and policy shifts. Further, the surging prevalence of chronic diseases, cancer and cardiovascular conditions creates acute demand for efficient, targeted delivery systems like auto-injectors and sustained-release implants to improve patient outcomes and reduce hospitalization rates. Technological advancements, including smart connected inhalers, microneedle patches enhancing transdermal absorption, pre-filled syringes minimizing errors, and AI-integrated wearable pumps for real-time monitoring, boost adherence and efficacy while aligning with Australia's digital health ecosystem. Government support through initiatives, investments in healthcare infrastructure, and policies promoting telemedicine further accelerate adoption of drug delivery devices in this region.

Market Challenges: Critical Barriers Impeding Progress

Despite these tailwinds, the market grapples with significant challenges that hinder expansion and market entry. Stringent Therapeutic Goods Administration (TGA) regulations impose lengthy, costly approval processes often exceeding AUD 95,000 for Class III devices with phased compliance rollouts into 2026 creating barriers for innovators and delaying product launches. High development and acquisition costs for advanced technologies limit affordability and accessibility, especially in rural areas, while reimbursement hurdles from schemes like the Pharmaceutical Benefits Scheme (PBS) complicate market penetration for novel devices. Intense competition from major players like Becton Dickinson and Novartis, coupled with low awareness among healthcare providers and patients about benefits like reduced needless-stick injuries, slows adoption rates. Additionally, supply chain vulnerabilities, as seen in ongoing GLP-1 shortages like Ozempic into 2025, and the need for specialized manufacturing heighten risks in this capital-intensive sector.

Australia Drug Delivery Devices Market: Key Segments

Type of Product

- Inhalers

- Injection Devices

- Transdermal Patches

Application Area

- Oncology

- Infectious Diseases

- Respiratory Diseases

- Diabetes

End User

- Hospitals

- Diagnostic Centers

- Home Care Settings

- Others

Example Players in the Australia Drug Delivery Devices Market

- AbbVie

- Bayer

- Becton Dickinson and Company

- GlaxoSmithKline

- Johnson & Johnson

- Novartis

- Novo Nordisk

- Pfizer

- Sanofi

- SiBiono GeneTech

- Teva Pharmaceutical Industries

- Viatris

Key Questions Answered in this Report

- How many drug delivery device developers in Australia are currently engaged in this market?

- Which are the leading companies in this market?

- Which country dominates the Australia drug delivery devices market?

- What are the key trends observed in the Australia drug delivery devices market?

- What factors are likely to influence the evolution of this market?

- What are the primary challenges faced by Australia drug delivery devices market?

- What is the current and future Australia drug delivery devices market size?

- What is the CAGR of Australia drug delivery devices market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

- The report can aid businesses in identifying future opportunities in any sector. It also helps in understanding if those opportunities are worth pursuing.

- The report helps in identifying customer demand by understanding the needs, preferences, and behavior of the target audience in order to tailor products or services effectively.

- The report equips new entrants with requisite information regarding a particular market to help them build successful business strategies.

- The report allows for more effective communication with the audience and in building strong business relations.

Complementary Benefits

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. MARKET DYNAMICS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Major Currencies Affecting the Market

- 4.2.2.2. Factors Affecting Currency Fluctuations on the Industry

- 4.2.2.3. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Currency Exchange Rate

- 4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.4.2. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Value and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.8.3. Trade Policies

- 4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

- 4.2.8.5. Impact of Trade Barriers on the Market

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. Stock Market Performance

- 4.2.11.7. Cross-Border Dynamics

- 4.2.1. Time Period

- 4.3. Conclusion

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Overview of Drug Delivery Devices

- 6.3. Key Design Features and Development Process

- 6.4. Classification of Connected / Smart Drug Delivery Devices

- 6.5. Type of Device

- 6.6. Regulatory Guidelines for Drug Delivery Devices

- 6.7. Advantages and Limitations of Drug Delivery Devices

- 6.8. Future Perspective

7. MARKET LANDSCAPE

- 7.1. Chapter Overview

- 7.2. Australia Drug Delivery Devices Market: Overall Market Landscape

- 7.2.1. Analysis by Year of Establishment

- 7.2.2. Analysis by Company Size

- 7.2.3. Analysis by Location of Headquarters

- 7.2.4. Analysis by Stage of Development

- 7.2.5. Analysis by Type of Device

- 7.2.6. Analysis by Therapeutic Area

8. COMPANY PROFILES: AUSTRALIA DRUG DELIVERY DEVICES MARKET

- 8.1. Chapter Overview

- 8.2. Becton Dickinson and Company

- 8.2.1. Company Overview

- 8.2.2. Product Portfolio

- 8.2.3. Financial Information

- 8.2.4. Recent Developments and Future Outlook

- 8.3. SiBiono GeneTech

- 8.4. Bayer

- 8.5. Novartis

- 8.6. GlaxoSmithKline

- 8.7. Teva Pharmaceutical Industries

- 8.8. AbbVie

- 8.9. Novo Nordisk

- 8.10. Johnson & Johnson

- 8.11. Sanofi

- 8.12. Viatris

- 8.13. Pfizer

9. PARTNERSHIPS AND COLLABORATIONS

- 9.1. Chapter Overview

- 9.2. Partnership Models

- 9.3. Australia Drug Delivery Devices Market: Partnerships and Collaborations

- 9.3.1. Analysis by Year of Partnership

- 9.3.2. Analysis by Type of Partnership

- 9.3.3. Most Active Players: Analysis by Number of Partnerships

- 9.3.4. Analysis by Geography

- 9.3.4.1. Intercontinental and Intracontinental Agreements

- 9.3.4.2. Local and International Agreements

10. MARKET IMPACT ANALYSIS

- 10.1. Chapter Overview

- 10.2. Market Drivers

- 10.3. Market Restraints

- 10.4. Market Opportunities

- 10.5. Market Challenges

- 10.6. Conclusion

11. AUSTRALIA DRUG DELIVERY DEVICES MARKET

- 11.1. Chapter Overview

- 11.2. Key Assumptions and Methodology

- 11.3. Australia Drug Delivery Devices Market: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 11.4. Roots Analysis Perspective on Market Growth

- 11.5 Scenario Analysis

- 11.5.1. Conservative Scenario

- 11.5.2. Optimistic Scenario

- 11.6. Key Market Segmentations

12. AUSTRALIA DRUG DELIVERY DEVICES MARKET, BY TYPE OF PRODUCT

- 12.1. Chapter Overview

- 12.2. Key Assumptions and Methodology

- 12.3. Australia Drug Delivery Devices Market: Distribution by Type of Product

- 12.3.1. Inhalers, Historical Trends (Since 2023) and Forecasted (Till 2035)

- 12.3.2. Injection Devices, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 12.3.3. Transdermal Patches, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 12.4. Data Triangulation and Validation

13. AUSTRALIA DRUG DELIVERY DEVICES MARKET, BY APPLICATION AREA

- 13.1. Chapter Overview

- 13.2. Assumptions and Methodology

- 13.3. Australia Drug Delivery Devices Market: Distribution by Application Area

- 13.3.1 Oncology: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 13.3.2. Infectious Diseases: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 13.3.3. Respiratory Diseases: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 13.3.4. Diabetes: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 13.4. Data Triangulation and Validation

14. AUSTRALIA DRUG DELIVERY DEVICES MARKET, BY END USER

- 14.1. Chapter Overview

- 14.2. Assumptions and Methodology

- 14.3. Australia Drug Delivery Devices Market: Distribution by End User

- 14.3.1 Hospitals: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 14.3.2. Surgery Centers / Clinics: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 14.3.3. Home Care Settings: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 14.3.4. Others: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 14.4. Data Triangulation and Validation