|

시장보고서

상품코드

2037814

차세대 RNA 치료제 시장(제2판) : 치료법별, 분자 유형별, 대상 질환별, 투여 경로별, 지역별 및 주요 기업별 - 동향과 예측(-2035년)Next Generation RNA Therapeutics Market (2nd Edition) by Type of Modality, Type of Molecule, Target Indication, Route of Administration, Geographical Regions and Leading Players-Trends and Forecast Till 2035 |

||||||

차세대 RNA 치료제 시장 - 개요

차세대 RNA 치료제 시장 규모는 2029년 1억 달러에서 2035년까지 27억 달러로 성장하며, 2035년까지의 예측 기간에 CAGR 63.1%로 확대할 것으로 추정되고 있습니다.

차세대 RNA 치료제 시장 - 성장과 동향

RNA 기반 치료법은 시간이 지남에 따라 현대 의학 분야에서 가장 중요한 치료 접근법 중 하나가 되었습니다. RNA 치료제는 단백질 발현과 유전자 활성 조절에 있으며, 매우 중요한 역할을 하고 있습니다. 또한 기존 치료법에 비해 치료 효과와 안전성 측면에서 우수한 특성을 가지고 있습니다. 그러나 이 분자들은 매우 불안정하여 충분한 농도로 투여하는 것이 어렵기 때문에 몇 가지 문제가 발생합니다.

세계의 업계 리더들은 앞서 언급한 과제를 극복하기 위해 차세대 RNA 치료제 및 백신 개발을 추진하고 있습니다. 또한 많은 기업이 혁신적인 RNA 치료제 및 백신의 창출, 개발, 제조를 위한 최첨단 기술 플랫폼을 제공하고 있습니다.

순환 RNA(circRNA), 끝없는 RNA(eRNA), 자가 증폭 RNA(saRNA), 전이 RNA(tRNA)는 구조적 안정성, 발현 특이성, 표적 전달성, 비면역원성 특성이 개선된 새로운 치료법의 한 예입니다. 이러한 특성으로 인해 유방암, 독감 등 다양한 치료 용도로 활용이 가능합니다. RNA 치료 및 백신 산업의 현재 동향과 전망을 고려할 때, 가까운 장래에 시장은 견고한 CAGR로 성장할 것으로 예상됩니다.

성장 요인 - 시장 확대의 전략적 촉진요인

RNA 치료제 및 RNA 백신 시장은 현대 의학에 미치는 변혁적 영향력을 지원하는 여러 요인에 의해 급속한 성장 궤도를 견인하고 있습니다. 주요 성장 요인 중 하나는 mRNA 기반 COVID-19 백신에 대한 실세계에서의 강력한 입증입니다. 이는 진화하는 병원균에 대한 높은 효능을 유지하면서 신속한 개발, 시험 및 도입이 가능하다는 것을 보여주었습니다. 이러한 성공은 플랫폼에 대한 신뢰를 크게 높였고, 벤처 캐피탈, 전략적 제휴, 종양학, 희귀 유전질환, 만성질환, 맞춤형 백신 등 다양한 치료 분야에 걸쳐 파이프라인을 확장하는 형태로 많은 투자를 이끌어냈습니다.

이러한 모멘텀은 안정성과 표적 전달에 대한 기존 과제를 해결하는 첨단 지질 나노입자 및 엑소좀 기반 전달 시스템 개발 등 지속적인 기술 발전으로 더욱 강화되고 있습니다. 또한 자가증폭 RNA 플랫폼과 같은 혁신 기술로 용량 및 비용 최적화가 가능해졌고, AI를 활용한 툴의 통합으로 시퀀스 설계, 최적화 및 후보물질 선정 과정이 가속화되고 있습니다. 또한 감염성 질환, 암, 유전성 질환을 포함한 전 세계 질병 부담의 증가와 희귀질환 치료제의 패스트트랙 지정 및 승인 건수 증가와 같은 지원적인 규제 프레임워크가 결합되어 시장 수요를 지속적으로 견인하고 있습니다. 동시에, 생명공학 기업, 위탁개발 및 제조업자(CDMO), 연구기관이 협력하는 첨단 협력적 생태계가 정밀의료 접근법에 대한 혁신과 투자를 촉진하고 있으며, 이를 통해 RNA 기반 치료법이 단백질 발현을 선택적으로 유도하거나 질병 관련 유전자를 침묵시킬 수 있습니다. 단백질의 발현을 선택적으로 유도하거나 질병 관련 유전자를 침묵시키는 RNA 기반 치료법이 가능해졌습니다.

시장 과제 - 발전을 가로막는 심각한 장애물

앞서 언급한 장점에도 불구하고 RNA 치료제 및 RNA 백신 시장은 전환 속도를 늦추고 광범위한 도입에 대한 장벽을 높일 수 있는 심각한 장애물에 직면해 있습니다. 제조는 여전히 매우 복잡하고 자본 집약적이며, 전용 클린룸 시설, 엄격한 품질관리, 노동 집약적인 정제 공정이 필요하므로 비용이 크게 증가합니다. 이러한 문제는 원자재 공급과 숙련된 인력 확보에 병목현상을 일으켜 생산량을 제한하고, 예기치 못한 안전 신호와 불일치로 인한 리콜의 위험을 증가시키는 경우가 많습니다.

또한 RNA 분자는 취약하고 RNase에 의해 빠르게 분해되기 쉽기 때문에 전달에 대한 문제도 여전히 남아있습니다. 반면, 지질 운반체의 경우 엔도솜으로부터의 탈출 효율이 낮거나, 표적 외 효과, 특히 간 이외의 부위에서 면역 활성화와 같은 문제에 자주 직면하고 있으며, 이는 효능을 떨어뜨리거나 독성 우려를 유발할 수 있습니다. 물류 문제는 엄격한 초저온 저장 및 유통 요구 사항으로 인해 자원이 부족한 지역에서의 보급을 심각하게 제한하고 있습니다. 이러한 문제는 지역별 규제 프레임워크의 변화, 듀얼유즈 기술과 관련된 지정학적 리스크, 그리고 잘못된 정보로 인한 일반 대중의 거부감으로 인해 더욱 복잡해지고 있으며, 이로 인해 개발 기간이 길어지고, 중소 혁신가들의 재정적 리스크가 증가하며, 주류로 진입하기 위해서는 지속적인 혁신이 필요함을 강조합니다. 주류로서의 실용화를 실현하기 위해서는 지속적인 혁신이 필요함을 강조하고 있습니다.

차세대 RNA 치료제 시장 - 주요 인사이트

이 보고서는 차세대 치료제 시장의 현황을 상세히 분석하고 업계내 잠재적인 성장 기회를 파악합니다. 보고서의 주요 조사 결과는 다음과 같습니다. :

- 다양한 업계 플레이어별로 개발중인 차세대 치료제의 73%는 신약개발 및 전임상 단계에 있습니다. 이러한 치료법의 대부분은 주로 감염성 질환의 치료에 초점을 맞추고 있습니다.

- 임상 단계에 있는 차세대 치료제의 80%는 임상 1상 및 1, 2상 단계에 있습니다. 특히 임상 단계에 있는 차세대 치료제/백신의 약 60%는 근육내 투여를 목적으로 설계되어 있습니다.

- 개발 초기 단계에 있음에도 불구하고 순환 RNA 치료는 빠르게 발전하는 치료 분야를 형성하고 있습니다. 이 매우 안정적이고 효율적인 치료법은 가까운 시일 내에 큰 주목을 받을 것으로 예상됩니다.

- 약 40%의 치료제가 개발 후기 단계에서 평가되고 있으며, 치료제 개발에 있으며, 차세대 RNA 기술의 큰 잠재력을 보여주고 있습니다.

- 임상시험의 대부분(21%)이 2024년에 등록되었습니다. 특히 RNA 치료제 및 백신 분야에서 완료된 임상시험의 대부분(약 60%)은 감염질환에 초점을 맞춘 임상시험이었습니다.

- 최근 다양한 질병을 대상으로 한 RNA 치료제 및 백신 연구가 활발히 진행되고 있으며, 이에 따라 많은 업계 관계자들이 이 분야의 임상시험을 추가로 진행하는 것에 주목하고 있습니다.

- RNA 치료제 및 백신 관련 특허의 약 30%가 2024년에 공개될 것으로 예상되며, 이는 RNA 기반 치료제 및 기술 분야의 수많은 발전을 반영합니다.

- 이 시장에서 체결된 거래의 53%는 saRNA 치료제/백신 임상연구에 초점을 맞추고 있습니다. 그 중 50%의 파트너십은 종양성 질환을 대상으로 한 치료제 평가에 초점을 맞추고 있습니다.

- 이 분야에 대한 투자의 약 40%가 2021년에 보고되었으며, 특히 벤처캐피털이 가장 주요한 자금 조달 모델로 부상하고 있으며, 시리즈 A 라운드가 64%의 거래를 차지하고 있습니다.

- 2029년 시장 규모는 약 1억 달러로 추정됩니다. 이 수치는 2035년까지의 예측 기간 중 CAGR 63.1%로 성장하여 2035년에는 약 27억 달러에 달할 것으로 예상됩니다.

차세대 RNA 치료제 시장

시장 규모 및 기회 분석은 다음 매개 변수를 기반으로 세분화됩니다. :

치료법

- 치료법

- 백신

분자 유형

- circRNA

- sacRNA

- saRNA

대상 질환

- 진행성 고형암

- 간세포암

- 유전성 골수 부전 증후군

- 방사선에 의한 구강건조증 및 타액 분비 감소

- 계절성 독감

투여 경로

- 유관내 투여

- 근육내 투여

- 종양내 투여

- 정맥 투여

지역

- 북미

- 미국

유럽

- 프랑스

- 독일

- 이탈리아

- 스페인

- 영국

- 기타

아시아태평양

- 싱가포르

차세대 RNA 치료제 시장 - 주요 부문

RNA 치료제 중 가장 큰 시장 점유율을 차지하고 있는 치료제는 무엇인가?

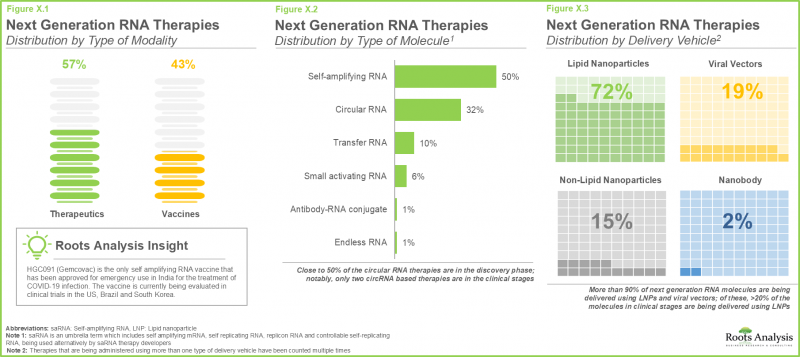

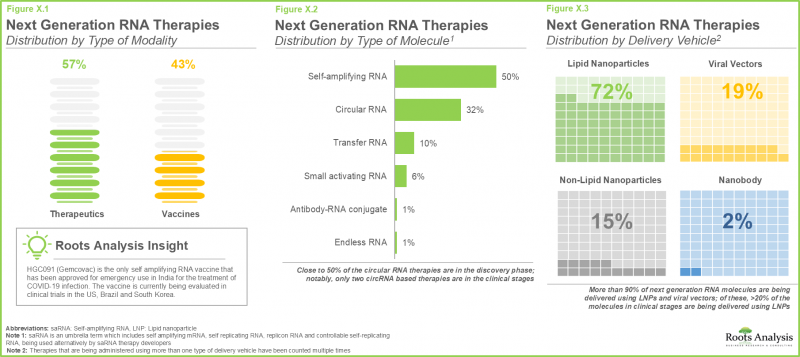

차세대 RNA 치료제 시장은 백신, 치료제 등 다양한 모달리티로 분류됩니다. 차세대 RNA 치료제 시장 예측에 따르면 2035년에는 치료제의 하위 부문이 더 큰 비중(80% 이상)을 차지할 것으로 예상됩니다. 또한 예측 기간 중 이 하위 부문은 상당한 속도로 성장할 것으로 예상됩니다. 이는 주로 치료제가 백신보다 더 넓은 활용 가능성을 가지고 있기 때문입니다. 치료제는 급성 질환과 만성질환을 모두 치료할 수 있으므로 시장 잠재력이 높아집니다. 이에 반해 백신은 주로 예방이 목적이며, 감염병을 대상으로 합니다.

차세대 RNA 치료제 분야에서 가장 빠른 성장을 보일 것으로 예상되는 분자 유형은 무엇인가?

업계 예측에 따르면 2035년까지 saRNA 분자가 전체 시장의 약 60%를 차지할 것으로 예상됩니다. 또한 시장에서 saRNA 분자의 비율이 크게 증가하여 예측 기간 중 CAGR 73.6%로 확대될 것으로 예상됩니다. 이는 siRNA와 같은 다른 RNA 치료법과는 달리 이중나선 구조로 인해 전사 수준에서 유전자 발현이 강화되기 때문입니다. 이를 통해 질병 치료에 사용할 수 있는 단백질을 더 많이 생산할 수 있습니다.

RNA 치료제에서 가장 큰 시장 점유율을 차지하는 적응증은 무엇인가?

차세대 RNA 치료제 시장 분석에 따르면 2035년에는 진행성 고형암의 하위 부문이 가장 큰 시장 점유율(약 35%)을 차지할 것으로 예측됩니다. 이러한 추세는 전 세계에서 암 질환의 유병률이 증가하고 있으며, 암 질환이 여전히 심각한 건강 문제로 대두되고 있기 때문인 것으로 보입니다. 또한 유전성 골수부전증후군의 하위 부문은 단기적으로 비교적 높은 CAGR을 기록할 것으로 예상됩니다. 이러한 성장은 유전성 골수 부전 질환의 희소성과 단일 유전자 질환이라는 특성 외에도 현재 효과적인 치료 옵션이 부족하기 때문입니다.

북미: 시장 점유율 1위로 시장 선도

북미는 차세대 RNA 치료제 시장에서 가장 큰 시장 점유율(65% 이상)을 차지할 것으로 예상됩니다. 이는 RNA 생물학에 대한 막대한 공적 자금 투입으로 이 분야의 임상 활동이 활발해졌기 때문입니다.

차세대 RNA 치료제 시장 주요 기업 사례

- AlphaVax

- Arcturus Therapeutics

- BioNTech

- HDT Bio

- MiNA Therapeutics

- VLP Therapeutics

차세대 RNA 치료제 시장 - 조사 범위

- 시장 규모 및 기회 분석: 이 보고서는 차세대 RNA 치료제 시장에 대한 상세한 분석을 통해 [A] 치료제 유형, [B] 분자 유형, [C] 치료 영역, [D] 투여 경로, [E] 및 [F] 주요 지역과 같은 주요 시장 부문에 초점을 맞추고 있습니다.

- 시장 현황: 승인되었거나 개발 단계에 있는 차세대 RNA 치료제 및 RNA 백신에 대해 [A] 양식 유형, [B] 분자 유형, [C] 전달 벡터 유형, [D] 개발 단계, [E] 치료 영역, [F] 주요 틈새 시장(circRNA 및 saRNA) 등 다양한 매개변수를 종합적으로 평가합니다. 등 다양한 매개변수를 고려하여 종합적으로 평가하고 있습니다. 또한 본 장에서는 [G] 설립연도, [H] 기업 규모, [I] 본사 소재지, [J] 가장 활발한 기업(치료제 수 기준)을 기준으로 다양한 차세대 RNA 치료제 및 RNA 백신 개발 기업에 대한 분석이 포함되어 있습니다.

- 기술동향: 차세대 RNA 치료제 및 RNA 백신 개발을 지원하기 위해 개발 및 도입되고 있는 기술에 대해 [A] 분자 분류, [B] 분자 유형, [C] 기술 능력, [D] 치료 영역, [E] 개발의 가장 진전된 단계 등 다양한 매개변수를 고려하여 종합적으로 평가하고 합니다. 본 장에서는 [F] 설립연도, [G] 기업규모, [H] 본사 소재지, [I] 사업모델을 기준으로 다양한 차세대 RNA 치료제 및 RNA 백신 기술 개발 기업에 대한 분석을 수록했습니다.

- 약물 프로파일: 개발이 마무리 단계에 있는 약물 후보물질에 대해 [A] 개발사 정보, [B] 약물 개요, [C] 임상시험 정보, [D] 임상시험 평가지표, [E] 임상시험 결과, [F] 예상 매출에 초점을 맞춘 상세한 프로파일을 제공합니다.

- 임상시험 분석: [A] 임상시험 등록 연도, [B] 임상시험 현황, [C] 임상시험 단계, [D] 등록 환자 수, [E] 스폰서 유형, [F] 치료 영역, [G] 임상시험 설계, [H] 주요 기관(임상시험 수 기준), [I] 중점 분야, [J] 지역 등의 파라미터를 기준으로 다양한 차세대 RNA 치료제 및 및 RNA 백신에 대한 완료, 진행 중, 계획 중인 임상시험을 검토합니다.

- 특허 분석: 차세대 RNA 치료제 및 RNA 백신 관련 출원/등록된 각종 특허에 대해 [A] 특허 유형(등록, 출원, 기타), [B] 특허 공개 연도, [C] 특허 관할권, [D] CPC 분류 기호, [E] 새로운 중점 분야, [F] 특허 경과 기간, [G] 주요 산업계/비산업계 플레이어(출원/등록 특허 수 기준) 및 특허 평가액에 기반. 주요 산업계/비산업계 플레이어(출원/등록 특허 수 기준), [H] 특허 평가액 기준.

- 제휴 및 공동연구: 이 분야에서 체결된 제휴 관계에 대해 [A] 제휴 연도, [B] 제휴 유형, [C] 분자 유형, [D] 제휴 중점 분야, [E] 제휴 목적, [F] 치료 분야, [G] 가장 활발한 플레이어(제휴 건수 기준), [H] 이 시장에서 제휴 활동의 지역별 분포 등 몇 가지 관련 매개변수를 분석합니다. 등 몇 가지 관련 파라미터를 기반으로 분석을 수행합니다.

- 자금조달 및 투자 분석: [A] 자금조달 연도, [B] 자금조달 형태, [C] 분자 유형, [D] 투자 금액, [E] 지역, [F] 자금조달 목적, [G] 개발 단계, [H] 치료 분야, [I] 가장 활발한 플레이어(자금조달 건수 및 금액 기준) 및 [J] 주요 투자자(자금조달 건수 기준) 등 몇 가지 관련 파라미터를 기반으로 이 분야에 대한 투자를 상세히 평가합니다.

- 주요 제약사 분석: [A] 구상 수, [B] 구상 시작연도, [C] 구상 유형, [D] 구상 목적, [E] 구상 중점 분야, [F] 본사 소재지 등 몇 가지 관련 파라미터를 기준으로 주요 제약사별 차세대 RNA 치료제 의약품 및 RNA 백신에 초점을 맞춘 다양한 구상을 종합적으로 검토합니다.

목차

제1장 배경

제2장 조사 방법

제3장 시장 역학

제4장 거시경제 지표

제5장 개요

제6장 서론

제7장 시장 구도 : RNA 치료제와 RNA 백신

제8장 테크놀러지 상황 개요

제9장 약물 개요

제10장 임상시험 분석

제11장 특허 분석

제12장 파트너십과 협력 관계

제13장 자금조달과 투자 분석

제14장 대형 제약회사 구상

제15장 차세대 RNA 치료제 세계 시장

제16장 차세대 RNA 치료제 시장(치료법별)

제17장 차세대 RNA 치료제 시장(분자 유형별)

제18장 차세대 RNA 치료제 시장(대상 질환별)

제19장 차세대 RNA 치료제 시장(투여 경로별)

제20장 차세대 RNA 치료제 시장(지역별)

제21장 차세대 RNA 치료제 시장(주요 기업별)

제22장 차세대 RNA 치료제 시장, 의약품 판매 예측

제23장 시장 기회 분석 : 북미

제24장 시장 기회 분석 : 유럽

제25장 시장 기회 분석 : 아시아태평양

제26장 결론

제27장 부록 I : 표형식 데이터

제28장 부록 II : 기업 및 조직 리스트

KSA 26.06.01Next Generation RNA Therapeutics Market: Overview

As per Roots Analysis, the next generation therapeutics market is estimated to grow from USD 0.1 billion in 2029 to USD 2.7 billion by 2035, at a CAGR of 63.1% during the forecast period, till 2035.

Next Generation RNA Therapeutics Market: Growth and Trends

RNA-based treatments have become one of the most important therapeutic approaches in the contemporary healthcare sector over time. RNA therapeutics play a critical role in protein expression and the regulation of gene activity. Additionally, when compared to conventional treatment methods, they provide improved therapeutic and safety characteristics. The extremely unstable nature of these molecules and their distribution in sufficient concentrations, however, raise several issues.

Global industry leaders are pushing the development of next-generation RNA therapies and vaccines to get over the aforementioned obstacles. Further, several companies also provide cutting-edge technological platforms for the creation, development, and production of innovative RNA therapies and vaccines.

Circular RNA (circRNA), endless RNA (eRNA), self-amplifying RNA (saRNA), and transfer RNA (tRNA) are examples of emerging modalities that exhibit improved structural stability, expression specificity, targeted delivery, and non-immunogenic characteristics. These characteristics allow their utilization across various therapeutic applications including breast cancer and influenza. Given the current trends and anticipated potential of the RNA therapies and vaccines industry, the market is expected to grow at a healthy CAGR in the near future.

Growth Drivers: Strategic Enablers of Market Expansion

The RNA therapeutics and RNA vaccines market is driven by a numerous factors underscoring its transformative impact on modern medicine and supporting its accelerated growth trajectory. A key growth driver has been the strong real-world validation of mRNA-based COVID-19 vaccines, which demonstrated the ability for rapid development, testing, and deployment while maintaining high efficacy against evolving pathogens. This success has significantly strengthened confidence in the platform, triggering substantial investments in the form of venture capital, strategic partnerships, and pipeline expansion across therapeutic areas such as oncology, rare genetic disorders, chronic diseases, and personalized vaccines.

This momentum is further reinforced by ongoing technological advancements, including the development of advanced lipid nanoparticle and exosome-based delivery systems that address prior challenges related to stability and targeted delivery. Additionally, innovations such as self-amplifying RNA platforms have enabled dose and cost optimization, while the integration of AI-driven tools has accelerated sequence design, optimization, and candidate selection timelines. Moreover, the increasing global burden of diseases including infectious diseases, cancer, and genetic disorders combined with supportive regulatory frameworks, such as fast-track designations for orphan drugs and a growing number of product approvals, continues to drive market demand. At the same time, a highly collaborative ecosystem involving biotechnology companies, contract development and manufacturing organizations (CDMOs), and research institutions is fostering innovation and investment in precision medicine approaches, enabling RNA-based therapies to selectively direct protein expression or silence disease-associated genes.

Market Challenges: Critical Barriers Impeding Progress

Despite the abovementioned advantages, the RNA therapeutics and RNA vaccines market faces significant hurdles, that can slow the pace of transition and raise barriers for widespread implementation. Manufacturing remains exceptionally complex and capital-intensive, requiring specialized cleanroom facilities, rigorous quality oversight, and labor-intensive purification steps that significantly increase costs. These challenges also create bottlenecks in raw material supply and skilled personnel availability, often limiting production volumes and increasing vulnerability to recalls due to unexpected safety signals or inconsistencies.

In addition, delivery hurdles persist as RNA molecules are fragile and prone to rapid degradation by RNases, while lipid carriers frequently struggle with inefficient endosomal escape, off-target effects, or immune activation that can diminish potency or raise toxicity concerns, particularly outside the liver. Logistical challenges stem from stringent ultra-cold storage and distribution requirements, which significantly limit reach in low-resource settings. These issues are further compounded by evolving regional regulatory frameworks, geopolitical risks associated with dual-use technologies, and persistent public hesitancy driven by misinformation, collectively extending timelines, increasing financial risks for smaller innovators, and underscoring the need for continued innovation to achieve mainstream viability.

Next Generation RNA Therapeutics Market: Key Insights

The report delves into the current state of the next generation therapeutics market and identifies potential growth opportunities within industry. Some key findings from the report include:

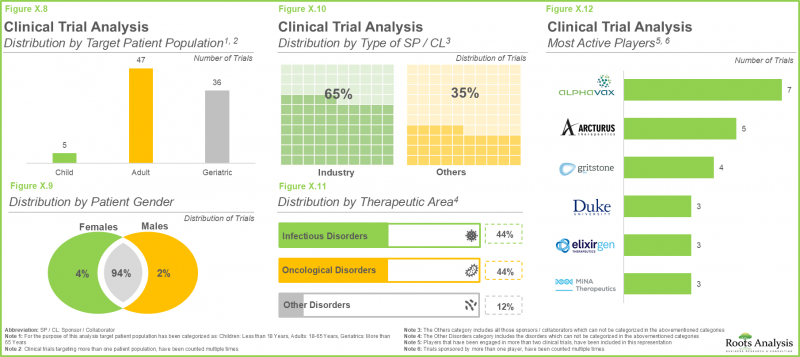

- 73% of the next generation therapies being developed by various industry players are in discovery and preclinical stages; most of these therapies primarily focus on the treatment of infectious diseases.

- 80% of the clinical stage next generation therapies are in phase I and phase I / II; notably, around 60% clinical stage next generation therapies / vaccines are designed for intramuscular administration.

- Despite being in early stages of development, circular RNA therapies form a rapidly advancing therapy segment; this highly stable and efficient therapeutic modality is anticipated to gain significant popularity in the coming future.

- ~40% therapies are being evaluated in late-stages of development, highlighting the significant potential of next generation RNA technologies in therapy development.

- Majority of the clinical trials (21%) were registered in 2024; notably, most of the (~60%) clinical trials completed in the RNA therapeutics and vaccines domain were focused on infectious diseases.

- Recently, the exploration of RNA therapeutics and vaccines in targeting various disorders has gained momentum, consequently drawing attention from several industry players to conduct more trials in this domain.

- Around 30% of the patents related to RNA therapeutics and vaccines have been published in 2024, reflecting numerous advancements in the field of RNA-based therapies and technologies.

- 53% of the deals inked in this market are focused on clinical research of saRNA therapeutics / vaccines; of these, 50% partnerships focus on the evaluation of therapies targeting oncological disorders.

- Around 40% of the investments made in this domain were reported in the year 2021; notably venture capital emerged as the most prominent funding model, with Series A rounds accounting for 64% of transactions.

- In 2029, the market size is estimated to be around USD 0.1 billion; this value is further projected to reach about USD 2.7 billion in 2035, growing at an annualized CAGR of 63.1%, during the forecast period till 2035.

Next Generation RNA Therapeutics Market

The market sizing and opportunity analysis has been segmented across the following parameters:

Type of Modality

- Therapeutics

- Vaccines

Type of Molecule

- circRNA

- sacRNA

- saRNA

Target Indication

- Advanced Solid Tumors

- Hepatocellular Carcinoma

- Inherited Bone Marrow Failure Syndrome

- Radiation-Induced Xerostomia and Hyposalivation

- Seasonal Influenza

Route of Administration

- Intraductal Route

- Intramuscular Route

- Intratumoral Route

- Intravenous Route

Geographical Regions

- North America

- US

Europe

- France

- Germany

- Italy

- Spain

- UK

- Rest of Europe

Asia-Pacific

- Singapore

Next Generation RNA Therapeutics Market: Key Segments

Which Modality Holds the Biggest Market Share for RNA Therapeutics?

The market for next-generation RNA treatments is segmented across various modalities, including vaccines and therapeutics. According to the next generation RNA therapeutics market forecast, the therapeutics sub-segment is expected to hold a larger proportion (>80%) in 2035. Furthermore, during the forecast period, this sub-segment is anticipated to increase at a notable rate. This is mainly because medicines have a wider range of possible applications than vaccinations. Therapeutics can treat both acute and chronic illnesses, increasing their market potential, in contrast to vaccines, which are mostly preventive and target infectious diseases.

Which molecule type exhibits the fastest growth in the next-generation RNA therapeutics sector?

According to the industry prediction, saRNA molecules are expected to have around 60% of the total market share by 2035. Additionally, the market is anticipated to see a significant rise in the proportion of saRNA molecules, expanding at a CAGR of 73.6% over the course of the projected period. This is because, in contrast to other RNA therapies like siRNAs, its double-stranded structure allows for enhanced gene expression at the transcriptional level. This guarantees the development of larger amounts of proteins that can be used to treat illnesses.

Which Target Indication Has the Biggest Market Share for RNA Therapeutics?

The advanced solid tumors subsegment is anticipated to hold the largest (~35%) market share in 2035, according to the next generation RNA therapies market analysis. This trend can be attributed to the rising global prevalence of oncological diseases, which continue to pose significant health challenges. Furthermore, the hereditary bone marrow failure syndrome sub-segment is anticipated to register a comparatively higher CAGR in the near term. This growth is driven by the rarity and predominantly monogenic nature of inherited bone marrow failure disorders, coupled with the current lack of effective therapeutic options.

North America: Taking the Lead in the Market with the Highest Share

North America is expected to have the largest market share (more than 65%) for next-generation RNA therapies. This is due to significant public funding in RNA biology, which has driven increased clinical activity within the field.

Example Players in Next Generation RNA Therapeutics Market

- AlphaVax

- Arcturus Therapeutics

- BioNTech

- HDT Bio

- MiNA Therapeutics

- VLP Therapeutics

Next Generation RNA Therapeutics Market: Research Coverage

- Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the next generation RNA therapeutics market , focusing on key market segments, including [A] type of modality, [B] type of molecule, [C] therapeutic areas, [D] route of administration [E] and [F] key geographical regions.

- Market Landscape: A comprehensive evaluation of next generation RNA therapeutics and RNA vaccines that are either approved or being evaluated in different stages of development, considering various parameters, such as [A] type of modality, [B] type of molecule, [C] type of delivery vehicle, [D] phase of development [E] therapeutic area and [F] key niche market segments (circRNA and saRNA). Additionally, the chapter includes analysis of various next generation RNA therapeutic and RNA vaccine developers, based on their [G] year of establishment, [H] company size, [I] location of headquarters and [J] most active players (in terms of number of therapies).

- Technology Landscape: A comprehensive evaluation of technologies that are being developed / deployed to support the development of next generation RNA therapeutics and RNA vaccines, considering various parameters, such as [A] class of molecule, [B] type of molecule, [C] capabilities of the technology, [D] therapeutic area and [E] highest phase of development. Additionally, the chapter features analysis of various next generation RNA therapeutic and RNA vaccine technology developers, based on their [F] year of establishment, [G] company size, [H] location of headquarters and [I] operational model.

- Drug Profiles: In-depth profiles of drug candidates that are in advanced stages of development, focusing on [A] details on its developer, [B] drug overview, [C] clinical trial information, [D] clinical trial endpoints, [E] clinical trial results and [F] estimated sales.

- Clinical Trial Analysis: Examination of completed, ongoing, and planned clinical studies of various next generation RNA therapeutics and RNA vaccines, based on parameters like [A] trial registration year, [B] trial status, [C] trial phase, [D] patients enrolled, [E] type of sponsor, [F] therapeutic area, [G] study design, [H] leading organizations (in terms of number of trials), [I] focus area and [J] geography.

- Patent Analysis: Detailed analysis of various patents filed / granted related to next generation RNA therapeutics and RNA vaccines based on [A] type of patent (granted patents, patent applications and others), [B] patent publication year, [C] patent jurisdiction, [D] CPC symbols, [E] emerging focus areas, [F] patent age, [G] leading industry / non-industry players (in terms of number of patents filed / granted) and [H] patent valuation.

- Partnerships and Collaborations: An analysis of partnerships established in this sector based on several relevant parameters, such as the [A] year of partnership, [B] type of partnership, [C] type of molecule, [D] focus of partnership, [E] purpose of partnership, [F] therapeutic area, [G] most active players (in terms of number of partnerships) and [H] the regional distribution of partnership activity in this market.

- Funding and Investment Analysis: A detailed evaluation of the investments made in this domain based on several relevant parameters, such as [A] year of funding, [B] type of funding, [C] type of molecule, [D] amount invested, [E] geography, [F] purpose of funding, [G] stage of development, [H] therapeutic area, [I] most active players (in terms of number and amount of funding instances) and [J] leading investors (in terms of number of funding instances).

- Big Pharma Analysis: A comprehensive examination of various initiatives focused on next generation RNA therapeutics and RNA vaccines undertaken by major pharmaceutical companies based on several relevant parameters, such as [A] number of initiatives, [B] year of initiative, [C] type of initiative, [D] purpose of initiative, [E] focus of initiative and [F] location of headquarters.

Key Questions Answered in this Report

- Which are the leading companies in the next generation RNA therapeutics market?

- Which region dominates the next generation RNA therapeutics market?

- What are the key trends observed in the next generation RNA therapeutics market?

- What factors are likely to influence the evolution of this market?

- What are the primary challenges faced by next generation RNA therapeutics developers?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

- The report can aid businesses in identifying future opportunities in any sector. It also helps in understanding if those opportunities are worth pursuing.

- The report helps in identifying customer demand by understanding the needs, preferences, and behavior of the target audience in order to tailor products or services effectively.

- The report equips new entrants with requisite information regarding a particular market to help them build successful business strategies.

- The report allows for more effective communication with the audience and in building strong business relations.

Additional Benefits

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. BACKGROUND

- 1.1. Context

- 1.2. Project Objectives

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. MARKET DYNAMICS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Major Currencies Affecting the Market

- 4.2.2.2. Factors Affecting Currency Fluctuations on the Industry

- 4.2.2.3. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Currency Exchange Rate

- 4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.4.2. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.8.3. Trade Policies

- 4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

- 4.2.8.5. Impact of Trade Barriers on the Market

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. Stock Market Performance

- 4.2.11.7. Cross Border Dynamics

- 4.2.1. Time Period

- 4.3. Conclusion

5. EXECUTIVE SUMMARY

- 5.1. Executive Summary: Market Landscape

- 5.2. Executive Summary: Market Trends

- 5.3. Executive Summary: Market Forecast and Opportunity Analysis

6. INTRODUCTION

- 6.1. Overview of Next Generation RNA Therapeutics and Vaccines

- 6.2. Evolution of Next Generation RNA Therapeutics and Vaccines

- 6.3. Types of Next Generation RNA Molecules

- 6.4. Key Aspects of Next Generation RNA Molecules

- 6.5. Key Challenges Associated with Traditional RNA Modalities

- 6.6. Advantages of Using Next Generation RNA Modalities

7. MARKET LANDSCAPE: RNA THERAPEUTICS AND RNA VACCINES

- 7.1. Overview of RNA Therapeutics and RNA Vaccines Therapies

- 7.1.1. Analysis by Type of Modality

- 7.1.2. Analysis by Type of Molecule

- 7.1.3. Analysis by Delivery Vehicle

- 7.1.4. Analysis by Stage of Development

- 7.1.5. Analysis by Therapeutic Area

- 7.1.6. Most Active Players: Analysis by Number of Therapies

- 7.2. RNA Therapeutics and RNA Vaccines: Clinical Stage Therapies Landscape

- 7.2.1. Analysis by Phase of Development

- 7.2.2. Analysis by Route of Administration

- 7.2.3. Analysis by Therapeutic Area

- 7.3. RNA Therapeutics and RNA Vaccines: Therapy Developers Landscape

- 7.3.1. Analysis by Year of Establishment

- 7.3.2. Analysis by Company Size

- 7.3.3. Analysis by Location of Headquarters

- 7.4. RNA Therapeutics and RNA Vaccines: Self-amplifying RNA Therapies Landscape

- 7.4.1. Analysis by Phase of Development

- 7.4.2. Analysis by Therapeutic Area

- 7.4.3. Most Active Players: Analysis by Number of Therapies

- 7.5. RNA Therapeutics and RNA Vaccines: Circular RNA Therapies Landscape

- 7.5.1. Analysis by Phase of Development

- 7.5.2. Analysis by Therapeutic Area

- 7.5.3. Most Active Players: Analysis by Number of Therapies

8. TECHNOLOGY LANDSCAPE

- 8.1. Overview of RNA Therapeutics and RNA Vaccines Technologies

- 8.1.1. Analysis by Class of Molecule

- 8.1.2. Analysis by Type of Molecule

- 8.1.3. Analysis by Capabilities of the Technology

- 8.1.4. Analysis by Therapeutic Area

- 8.1.5. Analysis by Highest Stage of Development

- 8.1.6. Analysis by Class of Molecule and Therapeutic Area

- 8.1.7. Analysis by Class of Molecule and Highest Stage of Development

- 8.1.8. Analysis by Type of Molecule and Capabilities of the Technology

- 8.2. RNA Therapeutics and RNA Vaccines: Next Generation RNA Technology / Platform Developers Landscape

- 8.2.1. Analysis by Year of Establishment

- 8.2.2. Analysis by Company Size

- 8.2.3. Analysis by Location of Headquarters

- 8.2.4. Analysis by Operational Model

9. DRUG PROFILES

- 9.1. ARCT-154

- 9.1.1. Company Overview

- 9.1.2. Drug Overview

- 9.1.3. Clinical Trial Information

- 9.1.4. Clinical Trial Endpoints

- 9.1.5. Clinical Trial Results

- 9.2. Gemcovac

- 9.3. VLPCOV-01

- 9.4. AVX901

- 9.5. BNT161

- 9.6. MTL-CEBPA + Sorafenib

10. CLINICAL TRIAL ANALYSIS

- 10.1. Methodology and Key Parameters

- 10.2. RNA Therapeutics and RNA Vaccines: Clinical Trial Analysis

- 10.2.1. Analysis by Trial Registration Year

- 10.2.2. Analysis by Trial Status

- 10.2.3. Analysis by Trial Registration Year and Trial Status

- 10.2.4. Analysis by Trial Phase

- 10.2.5. Analysis of Patients Enrolled by Trial Phase

- 10.2.6. Analysis of Patients Enrolled by Trial Registration Year

- 10.2.7. Analysis by Study Design

- 10.2.8. Analysis by Target Patient Population

- 10.2.9. Analysis by Patient Gender

- 10.2.10. Analysis by Type of Sponsor / Collaborator

- 10.2.11. Analysis by Therapeutic Area

- 10.2.12. Most Active Players: Analysis by Number of Trials

- 10.2.13. Analysis by Geography

11. PATENT ANALYSIS

- 11.1. Methodology and Key Parameters

- 11.2. RNA Therapeutics and RNA Vaccines: Patent Analysis

- 11.2.1. Analysis by Publication Year

- 11.2.2. Analysis by Type of Patent

- 11.2.3. Analysis of Granted Patents and Patent Applications by Publication Year

- 11.2.4. Analysis by Type of Applicant

- 11.2.5. Analysis by Application Year

- 11.2.6. Analysis by Patent Jurisdiction (Region)

- 11.2.7. Analysis by Patent Jurisdiction (Country)

- 11.2.8. Analysis by Patent Age

- 11.2.9. Leading Industry Players: Analysis by Number of Patents

- 11.2.10. Leading Non-Industry Players: Analysis by Number of Patents

- 11.2.11. Leading Individual Assignees: Analysis by Number of Patents

- 11.2.12. Analysis by CPC Symbols

- 11.3. Patent Benchmarking Analysis

- 11.4. Patent Valuation Analysis

12. PARTNERSHIPS AND COLLABORATIONS

- 12.1. Partnership Models

- 12.2. RNA Therapeutics and RNA Vaccines: Partnerships and Collaborations

- 12.2.1. Analysis by Year of Partnership

- 12.2.2. Analysis by Type of Partnership

- 12.2.3. Analysis by Year and Type of Partnership

- 12.2.4. Analysis by Year of Partnership and Type of Molecule

- 12.2.5. Analysis by Purpose of Partnership

- 12.2.6. Analysis by Focus Area of Partnership

- 12.2.7. Analysis by Therapeutic Area

- 12.2.8. Most Active Players: Analysis by Number of Partnerships

- 12.2.9. Analysis by Geography

- 12.2.9.1. Local and International Deals

- 12.2.9.2. Intracontinental and Intercontinental Deals

13. FUNDING AND INVESTMENT ANALYSIS

- 13.1. Funding Models

- 13.2. Funding Lifecycle Analysis

- 13.3. Investment Case: Risk and Return

- 13.4. RNA Therapeutics and RNA Vaccines: Funding and Investment Analysis

- 13.4.1. Analysis by Year of Funding

- 13.4.2. Analysis by Type of Funding

- 13.4.3. Analysis by Year and Type of Funding

- 13.4.4. Analysis of Amount Invested by Year of Funding

- 13.4.5. Analysis of Amount Invested by Type of Funding

- 13.4.6. Analysis by Geography

- 13.4.7. Analysis by Type of Molecule

- 13.4.8. Analysis by Purpose of Funding

- 13.4.9. Analysis by Stage of Development

- 13.4.10. Analysis by Therapeutic Area

- 13.4.11. Most Active Players: Analysis by Number of Funding Instances

- 13.4.12. Most Active Players: Analysis by Amount Invested

- 13.4.13. Most Active Investors: Analysis by Number of Funding Instances

- 13.5. Evolution and Relative Assessment of Funding Models

- 13.6. Summary of Funding and Investment Opportunities

14. BIG PHARMA INITIATIVES

- 14.1. Analysis Methodology

- 14.2. RNA Therapeutics and RNA Vaccines: Big Pharma Initiatives

- 14.2.1. Most Active Players: Analysis by Number of Big Pharma Initiatives

- 14.2.2. Analysis by Year of Initiative

- 14.2.3. Analysis by Type of Initiative

- 14.2.4. Analysis by Focus Area of Initiative

- 14.2.5. Analysis by Purpose of Initiative

- 14.2.6. Analysis by Type of Molecule

- 14.2.7. Analysis by Therapeutic Area

- 14.2.8. Analysis by Location of Headquarters

15. GLOBAL NEXT GENERATION RNA THERAPEUTICS MARKET

- 15.1. Forecast Model

- 15.2. Key Assumptions

- 15.3. Forecast Methodology

- 15.4. Global Next Generation RNA Therapeutics Market: Forecasted Estimates (till 2035)

- 15.4.1. Scenario Analysis

- 15.4.1.1. Conservative Scenario

- 15.4.1.2. Optimistic Scenario

- 15.4.1. Scenario Analysis

- 15.5. Key Market Segmentations

16. NEXT GENERATION RNA THERAPEUTICS MARKET, BY TYPE OF MODALITY

- 16.1. Next Generation RNA Therapeutics Market: Distribution by Type of Modality

- 16.1.1. Next Generation RNA Therapeutics Market for Therapeutics: Forecasted Estimates (till 2035)

- 16.1.2. Next Generation RNA Therapeutics Market for Vaccines: Forecasted Estimates (till 2035)

17. NEXT GENERATION RNA THERAPEUTICS MARKET, BY TYPE OF MOLECULE

- 17.1. Next Generation RNA Therapeutics Market: Distribution by Type of Molecule

- 17.1.1. Next Generation RNA Therapeutics Market for sacRNA: Forecasted Estimates (till 2035)

- 17.1.2. Next Generation RNA Therapeutics Market for saRNA: Forecasted Estimates (till 2035)

- 17.1.3. Next Generation RNA Therapeutics Market for circRNA: Forecasted Estimates (till 2035)

18. NEXT GENERATION RNA THERAPEUTICS MARKET, BY TARGET INDICATION

- 18.1. Next Generation RNA Therapeutics Market: Distribution by Target Indication

- 18.1.1. Next Generation RNA Therapeutics Market for Hepatocellular Carcinoma: Forecasted Estimates (till 2035)

- 18.1.2. Next Generation RNA Therapeutics Market for Seasonal Influenza: Forecasted Estimates (till 2035)

- 18.1.3. Next Generation RNA Therapeutics Market for Advanced Solid Tumors: Forecasted Estimates (till 2035)

- 18.1.4. Next Generation RNA Therapeutics Market for Radiation-Induced Xerostomia and Hyposalivation: Forecasted Estimates (till 2035)

- 18.1.5. Next Generation RNA Therapeutics Market for Inherited Bone Marrow Failure Syndromes: Forecasted Estimates (till 2035)

19. NEXT GENERATION RNA THERAPEUTICS MARKET, BY ROUTE OF ADMINISTRATION

- 19.1. Next Generation RNA Therapeutics Market: Distribution by Route of Administration

- 19.1.1. Next Generation RNA Therapeutics Market for Intravenous Route: Forecasted Estimates (till 2035)

- 19.1.2. Next Generation RNA Therapeutics Market for Intramuscular Route: Forecasted Estimates (till 2035)

- 19.1.3. Next Generation RNA Therapeutics Market for Intratumoral Route: Forecasted Estimates (till 2035)

- 19.1.4. Next Generation RNA Therapeutics Market for Intraductal Route: Forecasted Estimates (till 2035)

20. NEXT GENERATION RNA THERAPEUTICS MARKET, BY GEOGRAPHICAL REGIONS

- 20.1. Next Generation RNA Therapeutics Market: Distribution by Geographical Regions

- 20.1.1. Next Generation RNA Therapeutics Market in North America: Forecasted Estimates (till 2035)

- 20.1.1.1. Next Generation RNA Therapeutics Market in the US: Forecasted Estimates (till 2035)

- 20.1.2. Next Generation RNA Therapeutics Market in Europe: Forecasted Estimates (till 2035)

- 20.1.2.1. Next Generation RNA Therapeutics Market in the UK: Forecasted Estimates (till 2035)

- 20.1.2.2. Next Generation RNA Therapeutics Market in Germany: Forecasted Estimates (till 2035)

- 20.1.2.3. Next Generation RNA Therapeutics Market in France: Forecasted Estimates (till 2035)

- 20.1.2.4. Next Generation RNA Therapeutics Market in Italy: Forecasted Estimates (till 2035)

- 20.1.2.5. Next Generation RNA Therapeutics Market in Spain: Forecasted Estimates (till 2035)

- 20.1.2.6. Next Generation RNA Therapeutics Market in Rest of Europe: Forecasted Estimates (till 2035)

- 20.1.3. Next Generation RNA Therapeutics Market in Asia-Pacific: Forecasted Estimates (till 2035)

- 20.1.3.1. Next Generation RNA Therapeutics Market in Singapore: Forecasted Estimates (till 2035)

- 20.1.1. Next Generation RNA Therapeutics Market in North America: Forecasted Estimates (till 2035)

21. NEXT GENERATION RNA THERAPEUTICS MARKET, BY LEADING PLAYERS

22. NEXT GENERATION RNA THERAPEUTICS MARKET, SALES FORECAST OF DRUGS

- 22.1. Next Generation RNA Therapeutics: Drug Sales Forecast

- 22.1.1. MTL-CEBPA

- 22.1.2. BNT 161 / PF-07926307

- 22.1.3. STX-001

- 22.1.4. RXRG001

- 22.1.5. EXG-34217

23. MARKET OPPORTUNITY ANALYSIS: NORTH AMERICA

- 23.1. Next Generation RNA Therapeutics Market in North America: Distribution by Type of Modality

- 23.1.1. Next Generation RNA Therapeutics Market in North America for Therapeutics: Forecasted Estimates (till 2035)

- 23.1.2. Next Generation RNA Therapeutics Market in North America for Vaccines: Forecasted Estimates (till 2035)

- 23.2. Next Generation RNA Therapeutics Market in North America: Distribution by Type of Molecule

- 23.2.1. Next Generation RNA Therapeutics Market in North America for sacRNA: Forecasted Estimates (till 2035)

- 23.2.2. Next Generation RNA Therapeutics Market in North America for saRNA: Forecasted Estimates (till 2035)

- 23.2.3. Next Generation RNA Therapeutics Market in North America for circRNA: Forecasted Estimates (till 2035)

- 23.3. Next Generation RNA Therapeutics Market in North America: Distribution by Target Indication

- 23.3.1. Next Generation RNA Therapeutics Market in North America for Hepatocellular Carcinoma: Forecasted Estimates (till 2035)

- 23.3.2. Next Generation RNA Therapeutics Market in North America for Seasonal Influenza: Forecasted Estimates (till 2035)

- 23.3.3. Next Generation RNA Therapeutics Market in North America for Advanced Solid Tumors: Forecasted Estimates (till 2035)

- 23.3.4. Next Generation RNA Therapeutics Market in North America for Radiation-Induced Xerostomia and Hyposalivation: Forecasted Estimates (till 2035)

- 23.3.5. Next Generation RNA Therapeutics Market in North America for Inherited Bone Marrow Failure Syndromes: Forecasted Estimates (till 2035)

- 23.4. Next Generation RNA Therapeutics Market in North America: Distribution by Route of Administration

- 23.4.1. Next Generation RNA Therapeutics Market in North America for Intravenous Route: Forecasted Estimates (till 2035)

- 23.4.2. Next Generation RNA Therapeutics Market in North America for Intramuscular Route: Forecasted Estimates (till 2035)

- 23.4.3. Next Generation RNA Therapeutics Market in North America for Intratumoral Route: Forecasted Estimates (till 2035)

- 23.4.4. Next Generation RNA Therapeutics Market in North America for Intraductal Route: Forecasted Estimates (till 2035)

24. MARKET OPPORTUNITY ANALYSIS: EUROPE

- 24.1. Next Generation RNA Therapeutics Market in Europe: Distribution by Type of Modality

- 24.1.1. Next Generation RNA Therapeutics Market in Europe for Therapeutics: Forecasted Estimates (till 2035)

- 24.1.2. Next Generation RNA Therapeutics Market in Europe for Vaccines: Forecasted Estimates (till 2035)

- 24.2. Next Generation RNA Therapeutics Market in Europe: Distribution by Type of Molecule

- 24.2.1. Next Generation RNA Therapeutics Market in Europe for sacRNA: Forecasted Estimates (till 2035)

- 24.2.2. Next Generation RNA Therapeutics Market in Europe for saRNA: Forecasted Estimates (till 2035)

- 24.2.3. Next Generation RNA Therapeutics Market in Europe for circRNA: Forecasted Estimates (till 2035)

- 24.3. Next Generation RNA Therapeutics Market in Europe: Distribution by Target Indication

- 24.3.1. Next Generation RNA Therapeutics Market in Europe for Hepatocellular Carcinoma: Forecasted Estimates (till 2035)

- 24.3.2. Next Generation RNA Therapeutics Market in Europe for Seasonal Influenza: Forecasted Estimates (till 2035)

- 24.3.3. Next Generation RNA Therapeutics Market in Europe for Advanced Solid Tumors: Forecasted Estimates (till 2035)

- 24.3.4. Next Generation RNA Therapeutics Market in Europe for Radiation-Induced Xerostomia and Hyposalivation: Forecasted Estimates (till 2035)

- 24.3.5. Next Generation RNA Therapeutics Market in Europe for Inherited Bone Marrow Failure Syndromes: Forecasted Estimates (till 2035)

- 24.4. Next Generation RNA Therapeutics Market in Europe: Distribution by Route of Administration

- 24.4.1. Next Generation RNA Therapeutics Market in Europe for Intravenous Route: Forecasted Estimates (till 2035)

- 24.4.2. Next Generation RNA Therapeutics Market in Europe for Intramuscular Route: Forecasted Estimates (till 2035)

- 24.4.3. Next Generation RNA Therapeutics Market in Europe for Intratumoral Route: Forecasted Estimates (till 2035)

- 24.4.4. Next Generation RNA Therapeutics Market in Europe for Intraductal Route: Forecasted Estimates (till 2035)

25. MARKET OPPORTUNITY ANALYSIS: ASIA-PACIFIC

- 25.1. Next Generation RNA Therapeutics Market in Asia-Pacific: Distribution by Type of Modality

- 25.1.1. Next Generation RNA Therapeutics Market in Asia-Pacific for Therapeutics: Forecasted Estimates (till 2035)

- 25.1.2. Next Generation RNA Therapeutics Market in Asia-Pacific for Vaccines: Forecasted Estimates (till 2035)

- 25.2. Next Generation RNA Therapeutics Market in Asia-Pacific: Distribution by Type of Molecule

- 25.2.1. Next Generation RNA Therapeutics Market in Asia-Pacific for sacRNA: Forecasted Estimates (till 2035)

- 25.2.2. Next Generation RNA Therapeutics Market in Asia-Pacific for saRNA: Forecasted Estimates (till 2035)

- 25.2.3. Next Generation RNA Therapeutics Market in Asia-Pacific for circRNA: Forecasted Estimates (till 2035)

- 25.3. Next Generation RNA Therapeutics Market in Asia-Pacific: Distribution by Target Indication

- 25.3.1. Next Generation RNA Therapeutics Market in Asia-Pacific for Hepatocellular Carcinoma: Forecasted Estimates (till 2035)

- 25.3.2. Next Generation RNA Therapeutics Market in Asia-Pacific for Seasonal Influenza: Forecasted Estimates (till 2035)

- 25.3.3. Next Generation RNA Therapeutics Market in Asia-Pacific for Advanced Solid Tumors: Forecasted Estimates (till 2035)

- 25.3.4. Next Generation RNA Therapeutics Market in Asia-Pacific for Radiation-Induced Xerostomia and Hyposalivation: Forecasted Estimates (till 2035)

- 25.3.5. Next Generation RNA Therapeutics Market in Asia-Pacific for Inherited Bone Marrow Failure Syndromes: Forecasted Estimates (till 2035)

- 25.4. Next Generation RNA Therapeutics Market in Asia-Pacific: Distribution by Route of Administration

- 25.4.1. Next Generation RNA Therapeutics Market in Asia-Pacific for Intravenous Route: Forecasted Estimates (till 2035)

- 25.4.2. Next Generation RNA Therapeutics Market in Asia-Pacific for Intramuscular Route: Forecasted Estimates (till 2035)

- 25.4.3. Next Generation RNA Therapeutics Market in Asia-Pacific for Intratumoral Route: Forecasted Estimates (till 2035)

- 25.4.4. Next Generation RNA Therapeutics Market in Asia-Pacific for Intraductal Route: Forecasted Estimates (till 2035)