|

시장보고서

상품코드

1913355

아크 용접 장비 시장 : 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Arc Welding Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

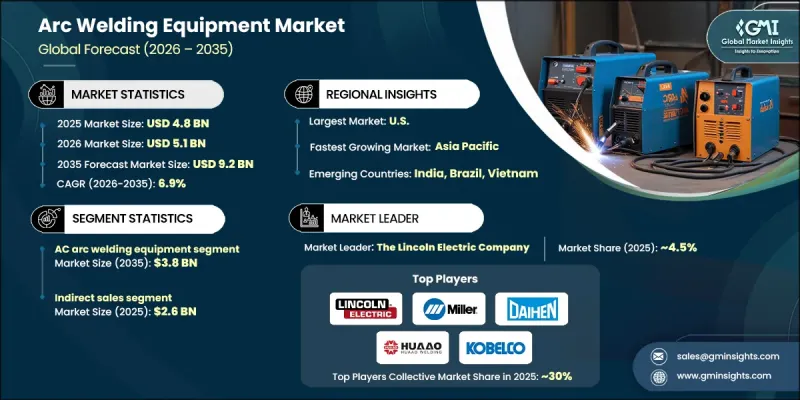

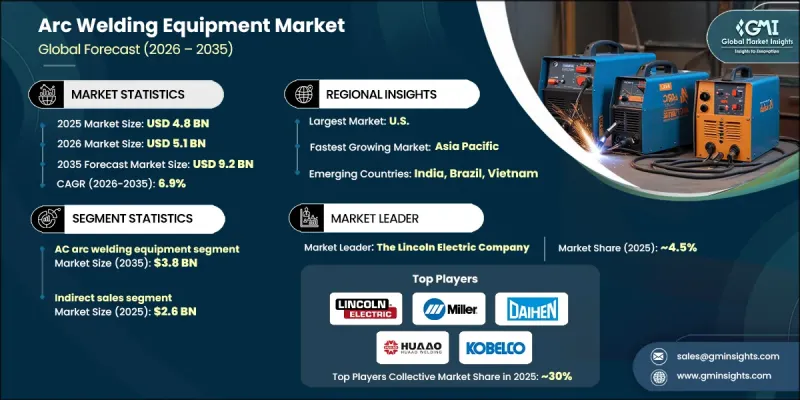

세계의 아크 용접 장비 시장은 2025년 48억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 6.9%로 성장할 전망이며, 92억 달러에 이를 것으로 예측됩니다.

직장의 안전과 설비 설계를 규정하는 규제 프레임워크은 아크 용접 작업에 의존하는 업계 전체 수요를 크게 좌우하고 있습니다. 전압 임계값, 전기 절연, 접지 프로토콜 및 기류 기준에 대한 엄격한 요구 사항은 규제에 따른 용접 시스템 및 안전 대책 솔루션의 도입을 추진하고 있습니다. 용접과 관련된 건강 위험에 대한 인식 증가는 적절한 환기, 배기 관리 및 호흡 보호의 필요성을 더욱 강화하고 있습니다. 노동 안전 규제에서는 내열성, 내화성 및 내전기 노출성을 갖춘 보호구의 사용이 의무화됨과 동시에 시인성과 안면 보호에 관한 성능 기준도 규정되어 있습니다. 이러한 규칙은 장비 설계, 시설 개조 및 구매 판단에 종합적으로 영향을 미칩니다. 제조업체 및 최종 사용자가 컴플라이언스, 작업 안전 및 근로자 보호를 선호하는 동안 고급 아크 용접 장비에 대한 수요는 계속 증가하고 있습니다. 시장 성장은 생산성을 지원하면서 장기적인 직업 위험을 줄이는 보다 안전하고 규제 준수 기술에 대한 지속적인 투자를 반영합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 시 가치 | 48억 달러 |

| 예측 금액 | 92억 달러 |

| CAGR | 6.9% |

2025년 교류 아크 용접 장비는 40.3%의 점유율을 차지했으며, 2035년까지 연평균 복합 성장률(CAGR) 7%로 성장이 예상됩니다. 이 부문은 비용 경쟁력 및 다양한 전기적 조건 하에서도 안정된 성능을 지원하는 작동 특성의 장점이 있습니다. 개방 전압 레벨에 대한 규제 제한은 제품 설계에 직접 영향을 미치며 제조업체는 수동 및 자동 용도 모두에서 확립된 안전 기준을 준수하는 장비 개발을 촉구합니다.

간접 판매 채널은 2025년에 26억 달러를 창출해 55%의 점유율을 차지했습니다. 이 경로는 표준화 제품, 교체 부품 및 소모품의 광범위한 유통을 지원하는 동시에 제조업체가 직접 대응하지 않는 지역 및 고객층에 도달하는 것을 확대합니다. 간접 채널은 특히 2차 시장 및 소규모 운영 환경에서 확장성, 유연성 및 비용 효율성을 제공합니다.

북미의 아크 용접 장비 시장은 2025년 38.2%의 점유율을 차지했으며, 2035년까지 연평균 복합 성장률(CAGR) 7.1%로 성장할 것으로 예측됩니다. 강력한 제조 능력, 안전 기준의 엄격한 시행, 지속적인 장비 업그레이드가 지역 우위를 지원합니다. 규제 요건에 따라 상세한 기술 요건이 정해지며, 이는 구매 행동 및 장비 교체 사이클에 직접적인 영향을 미칩니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 엄격한 안전 규제

- 지속적인 철강 생산 및 인프라 정비

- 건강 리스크에 대한 의식의 고조가 안전한 기술의 촉진에 연결

- 업계의 잠재적 위험 및 과제

- 높은 자본 비용 및 통합 비용

- 기술자 부족 및 컴플라이언스 부담

- 기회

- 재생에너지 및 그린 인프라 프로젝트 확대

- AI 구동형 및 IoT 대응 용접 솔루션 개발

- 성장 촉진요인

- 성장 가능성 분석

- 장래 시장 동향

- 가격 동향 분석

- 지역 및 용접 기술

- 기술 및 혁신 동향

- 현행 기술

- 신흥 기술

- 규제 프레임워크

- 지역별

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 제품 포트폴리오 벤치마크

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 용접 기술별(2022-2035년)

- 실드 메탈 아크 용접(SMAW)

- 가스 금속 아크 용접(GMAW/MIG)

- 플럭스입 아크 용접(FCAW)

- 가스 텅스텐 아크 용접(GTAW)

- 서브 머지 아크 용접(SAW)

- 기타(플라즈마 아크 용접(PAW) 등)

제6장 시장 추계 및 예측 : 전원별(2022-2035년)

- 교류 아크 용접 장비

- 직류 아크 용접 장비

- 기타

제7장 시장 추계 및 예측 : 최종 이용 산업별(2022-2035년)

- 자동차 및 운송

- 중공업 및 제조

- 건설 및 인프라

- 조선 및 해양 산업

- 항공우주 및 방위 산업

- 에너지 및 전력

- 석유 및 가스

- 기타

제8장 시장 추계 및 예측 : 유통 채널별(2022-2035년)

- 직접 판매

- 간접 판매

제9장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제10장 기업 프로파일

- Ador Welding

- Amada Miyachi America

- Arcon Welding Equipment

- CLOOS Welding Equipment

- Daihen

- Denyo

- ESAB

- Fronius International

- Illinois Tool Works(ITW Welding)

- Jinan Huaao Electric Welding Machine

- Kobe Steel(Kobelco)

- Miller Electric Mfg.(part of ITW Welding)

- OTC Daihen

- Panasonic Welding Systems

- The Lincoln Electric Company

The Global Arc Welding Equipment Market was valued at USD 4.8 billion in 2025 and is estimated to grow at a CAGR of 6.9% to reach USD 9.2 billion by 2035.

Regulatory frameworks governing workplace safety and equipment design strongly shape demand across industries that rely on arc welding operations. Strict requirements related to voltage thresholds, electrical insulation, grounding protocols, and airflow standards have increased the adoption of compliant welding systems and supporting safety solutions. Growing recognition of welding-related health risks has further intensified the need for proper ventilation, exhaust management, and respiratory protection. Occupational safety regulations mandate protective equipment with resistance to heat, fire, and electrical exposure, while also specifying performance standards for visibility and facial protection. These rules collectively influence equipment engineering, facility upgrades, and purchasing decisions. As manufacturers and end users prioritize compliance, operational safety, and workforce protection, demand for advanced arc welding equipment continues to rise. The market's growth reflects sustained investment in safer, regulation-aligned technologies that support productivity while reducing long-term occupational risk.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.8 Billion |

| Forecast Value | $9.2 Billion |

| CAGR | 6.9% |

In 2025, the AC arc welding equipment accounted for a 40.3% share and is expected to grow at a CAGR of 7% through 2035. This segment benefits from cost competitiveness and operational characteristics that support stable performance under varying electrical conditions. Regulatory limits on open-circuit voltage levels directly influence product design, prompting manufacturers to align equipment development with established safety thresholds for both manual and automatic applications.

The indirect sales channel generated USD 2.6 billion in 2025, representing a 55% share. This route supports the broad distribution of standardized products, replacement components, and consumables while extending reach into regions and customer groups not served directly by manufacturers. Indirect channels offer scalability, flexibility, and cost efficiency, particularly in secondary markets and smaller operational settings.

North America Arc Welding Equipment Market held a 38.2% share in 2025 and is forecast to grow at a CAGR of 7.1% through 2035. Strong manufacturing capacity, strict enforcement of safety standards, and consistent equipment upgrades support regional dominance. Regulatory mandates establish detailed technical requirements that directly influence purchasing behavior and equipment replacement cycles.

Key companies active in the Global Arc Welding Equipment Market include The Lincoln Electric Company, ESAB, Fronius International, Panasonic Welding Systems, Illinois Tool Works, Miller Electric Mfg., OTC Daihen, Daihen, Denyo, Ador Welding, CLOOS Welding Equipment, Amada Miyachi America, Kobe Steel, Jinan Huaao Electric Welding Machine, and Arcon Welding Equipment. Companies in the Global Arc Welding Equipment Market strengthen their competitive position through continuous product innovation, regulatory compliance, and expansion of distribution networks. Manufacturers invest in safety-focused engineering, energy efficiency, and digital monitoring capabilities to meet evolving industry standards. Strategic partnerships with distributors enhance market reach, while localized manufacturing improves supply reliability. After-sales service, training support, and consumables integration help build long-term customer relationships.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Welding technology trends

- 2.2.3 Power source trends

- 2.2.4 End use industry trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspective: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

- 2.5 Strategic recommendations

- 2.5.1 Supply chain diversification strategy

- 2.5.2 Product portfolio enhancement

- 2.5.3 Partnership and alliance opportunities

- 2.5.4 Cost management and pricing strategy

- 2.6 Decision framework

- 2.6.1 Investment priority matrix

- 2.6.2 ROI analysis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent safety regulations

- 3.2.1.2 Sustained steel production and infrastructure build-out

- 3.2.1.3 Health risk awareness encouraging safer technologies

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High capital and integration costs

- 3.2.2.2 Technical skills shortage and compliance burden

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of renewable energy and green infrastructure projects

- 3.2.3.2 Development of AI-driven and IoT enabled welding solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Price trend analysis

- 3.5.1 Region and welding technology

- 3.6 Technology and innovation landscape

- 3.6.1 Current technology

- 3.6.2 Emerging technologies

- 3.7 Regulatory framework

- 3.7.1 By region

- 3.7.1.1 North America

- 3.7.1.2 Europe

- 3.7.1.3 Asia Pacific

- 3.7.1.4 Latin America

- 3.7.1.5 Middle East and Africa

- 3.7.1 By region

- 3.8 Porter's five forces analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Product portfolio benchmarking

- 4.7 Key developments

- 4.7.1 Mergers & acquisitions

- 4.7.2 Partnerships & collaborations

- 4.7.3 New Product Launches

- 4.7.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Welding Technology 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Shielded metal arc welding (SMAW)

- 5.3 Gas metal arc welding (GMAW/MIG)

- 5.4 Flux-cored arc welding (FCAW)

- 5.5 Gas tungsten arc welding (GTAW)

- 5.6 Submerged arc welding (SAW)

- 5.7 Others (plasma arc welding (PAW), etc.)

Chapter 6 Market Estimates & Forecast, By Power Source, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 AC arc welding equipment

- 6.3 DC arc welding equipment

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Automotive & transportation

- 7.3 Heavy industry & fabrication

- 7.4 Construction & infrastructure

- 7.5 Shipbuilding & marine

- 7.6 Aerospace & defense

- 7.7 Energy and power

- 7.8 Oil and gas

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 U.K.

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 10.1 Ador Welding

- 10.2 Amada Miyachi America

- 10.3 Arcon Welding Equipment

- 10.4 CLOOS Welding Equipment

- 10.5 Daihen

- 10.6 Denyo

- 10.7 ESAB

- 10.8 Fronius International

- 10.9 Illinois Tool Works (ITW Welding)

- 10.10 Jinan Huaao Electric Welding Machine

- 10.11 Kobe Steel (Kobelco)

- 10.12 Miller Electric Mfg. (part of ITW Welding)

- 10.13 OTC Daihen

- 10.14 Panasonic Welding Systems

- 10.15 The Lincoln Electric Company