|

시장보고서

상품코드

1876802

자동차용 반도체 시장 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Automotive Semiconductor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

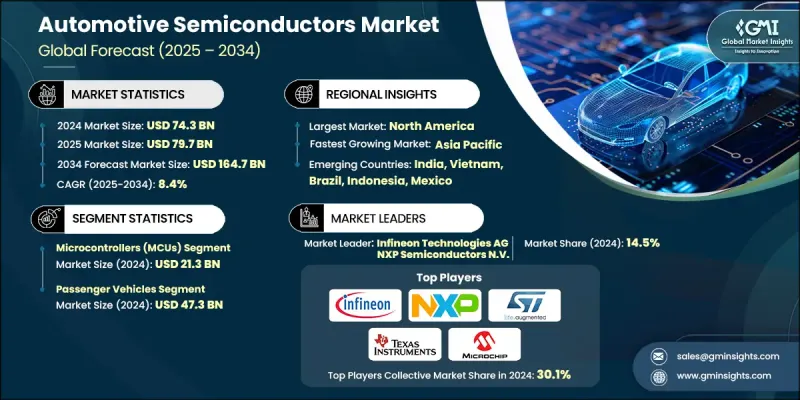

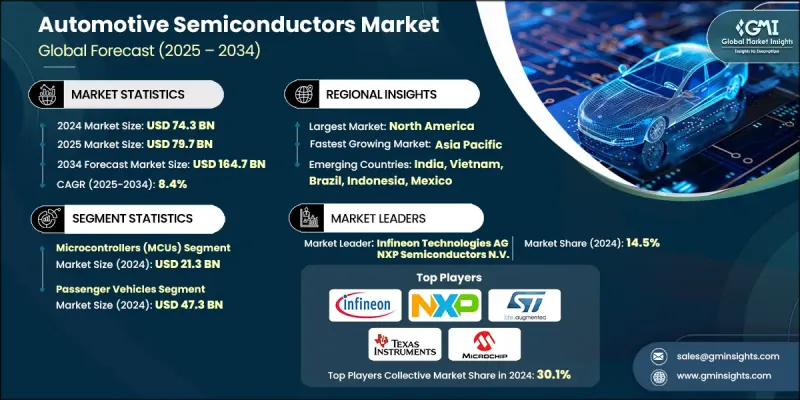

세계의 자동차용 반도체 시장은 2024년에 743억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 8.4%로 성장하여 1,647억 달러에 이를 것으로 예측됩니다.

전기자동차의 보급 확대와 파워트레인 기술의 지속적인 발전이 맞물려 자동차용 반도체 수요를 견인하고 있습니다. 차량의 전동화가 진행되면서 첨단운전자보조시스템(ADAS)와 자율주행 시스템의 급속한 발전으로 자동차의 안전성과 운영 효율성이 변화하고 있습니다. 인포테인먼트 시스템, 차량 커넥티비티 솔루션, V2X 통신의 통합이 진행되면서 반도체의 채용이 더욱 가속화되고 있습니다. 또한, 배출가스 규제 및 규제 기준 강화로 인해 자동차 제조업체들은 연비 향상과 배출가스 저감을 위해 반도체 기반 제어 시스템을 도입해야 하는 상황에 직면해 있습니다. 전 세계적으로 전기화 및 지능형 모빌리티로의 전환은 에너지 변환, 배터리 관리, 차량 지능화에 중요한 역할을 하는 반도체 칩이 보다 스마트하고 지속 가능한 자동차 생태계를 지원함으로써 반도체 산업의 구조를 재편하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 743억 달러 |

| 예측 금액 | 1,647억 달러 |

| CAGR | 8.4% |

마이크로컨트롤러 분야는 2024년 213억 달러 규모에 달했습니다. 자동차, 특히 전기자동차 및 ADAS 탑재 모델의 전자기기 증가에 따라 고성능 자동차 마이크로컨트롤러에 대한 수요는 지속적으로 증가하고 있습니다. 이 부품들은 파워트레인 제어, 배터리 관리, 에어백, 인포테인먼트, 도메인 컨트롤러 등의 시스템에 필수적입니다. 소프트웨어 정의 차량(SDV)의 부상과 함께 MCU에 대한 의존도가 확대되고 있습니다. MCU는 여러 서브시스템에 걸쳐 고속의 실시간 컴퓨팅과 고도의 차량 협업을 실현하기 때문입니다.

소형 상용차(LCV) 부문은 2034년까지 연평균 복합 성장률(CAGR) 7.9%를 보일 것으로 예측됩니다. 도시 배송 차량의 전동화와 커넥티드 텔레매틱스의 통합이 이러한 성장의 주요 요인입니다. 클래스 2 상용차 생산 증가와 차량의 지속가능성에 대한 관심이 높아짐에 따라 LCV 전동화 및 디지털 모니터링을 위해 설계된 반도체에 대한 수요가 꾸준히 증가하고 있습니다.

미국 자동차용 반도체 시장은 2024년 174억 달러 규모에 달했습니다. 전기차 보급 가속화와 더불어 정부의 우대정책과 엄격한 규제 프레임워크가 국내 전체 반도체 수요를 견인하고 있습니다. 각 제조업체들은 구역별 E/E 아키텍처에 대한 OEM의 요구에 부응하기 위해 연구개발 전략을 재검토하고, 안전성과 신뢰성에 대한 AEC-Q100 Grade 1 표준을 충족하는 첨단 AI 및 ML 기반 프로세서를 개발 중입니다.

ZF Friedrichshafen AG, Renesas Electronics Corporation, ST Microelectronics N.V., Infineon Technologies AG, Analog Devices AG, NXP Semiconductors N.V., Rohm Advanced Micro Devices, Continental, Toshiba, Texas Instruments, Tower Semiconductor, TE Connectivity, Microchip Technology, On Semiconductor, Merexis N.V., Robert Bosch GmbH, Micron Corp. 테크놀로지, 알레그로 마이크로시스템즈 등이 있습니다. 주요 기업들은 시장에서의 입지를 강화하기 위해 혁신, 전략적 제휴, 생산능력 확대에 주력하고 있습니다. 전기자동차 및 자율주행차 아키텍처를 지원하는 칩 개발에 많은 투자를 통해 에너지 효율과 처리 속도를 향상시키고 있습니다. 자동차 제조업체(OEM) 및 Tier 1 공급업체와의 제휴는 신흥 차량 플랫폼에 맞는 제품 개발을 실현하는 데 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 미치는 요인

- 이익률 분석

- 파괴적 변화

- 향후 전망

- 제조업체

- 유통업체

- 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 신흥 비즈니스 모델

- 컴플라이언스 요건

- 지속가능성 대책

- 특허 및 지적재산 분석

- 지정학적 및 무역 동향

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 시장 집중도 분석

- 지역별

- 주요 기업의 경쟁 벤치마킹

- 재무 실적 비교

- 매출

- 이익률

- 연구개발

- 제품 포트폴리오 비교

- 제품 범위 폭

- 기술

- 혁신

- 지역별 프레즌스 비교

- 세계 전개 분석

- 서비스 네트워크 커버리지

- 지역별 시장 침투율

- 경쟁 포지셔닝 매트릭스

- 리더 기업

- 챌린저

- 팔로워

- 니치 기업

- 전략적 전망 매트릭스

- 재무 실적 비교

- 주요 발전, 2021-2024

- 인수합병(M&A)

- 제휴 및 협력 관계

- 기술적 진보

- 확대 및 투자 전략

- 지속가능성 시책

- 디지털 전환 대처

- 신흥/스타트업 경쟁 동향

제5장 시장 추산·예측 : 구성요소 유형별, 2021-2034

- 주요 동향

- 마이크로컨트롤러(MCU)

- 센서

- 파워 반도체

- 메모리

- 아날로그 및 혼합 신호 IC

- 기타

제6장 시장 추산·예측 : 차종별, 2021-2034

- 주요 동향

- 승용차

- 소형 상용차(LCV)

- 대형 상용차(HCV)

제7장 시장 추산·예측 : 용도별, 2021-2034

- 주요 동향

- 파워트레인 및 전동화

- 엔진 제어 장치(ECU)

- 배터리 관리 시스템(BMS)

- 차량내 충전기

- 기타

- 안전 시스템

- 첨단 운전자 보조 시스템(ADAS)

- 안티락 브레이크 시스템(ABS)

- 전자식 안정성 제어(ESC)

- 기타

- 차체 전자기기

- 도어, 시트및 창문 제어

- 조명(LED, 어댑티브 헤드 램프)

- HVAC 시스템

- 기타

- 섀시 및 서스펜션

- 전동 파워 스티어링(EPS)

- 서스펜션 제어 유닛

- 기타

- 인포테인먼트 및 텔레매틱스

- 오디오 처리 및 증폭기

- GPS 및 내비게이션 시스템

- 기타

제8장 시장 추산·예측 : 판매채널별, 2021-2034

- 주요 동향

- OEM

- 애프터마켓

제9장 시장 추산·예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 개요

- 세계의 주요 기업

- Infineon Technologies AG

- NXP Semiconductors N.V.

- STMicroelectronics N.V.

- Texas Instruments, Inc.

- Renesas Electronics Corporation

- Microchip Technology Inc.

- 지역별 주요 기업

- 북미 :

- Advanced Micro Devices(AMD)

- Analog Devices, Inc.

- Micron Technology

- Onsemi

- 유럽 :

- Continental

- Melexis N.V.

- Robert Bosch GmbH

- ZF Friedrichshafen AG

- 아시아태평양 :

- Toshiba

- Rohm Co., Ltd.

- Tower Semiconductor Ltd.

- 북미 :

- 니치/디스럽터 기업

- Allegro Microsystems

- TE Connectivity

The Global Automotive Semiconductor Market was valued at USD 74.3 billion in 2024 and is estimated to grow at a CAGR of 8.4% to reach USD 164.7 billion by 2034.

The growing adoption of electric mobility, coupled with the continuous evolution of powertrain technologies, is driving the demand for automotive semiconductors. Increasing vehicle electrification, along with the rapid advancement of ADAS and autonomous driving systems, is transforming automotive safety and operational efficiency. Rising integration of infotainment systems, vehicle connectivity solutions, and V2X communication is further accelerating semiconductor adoption. Additionally, tightening emission norms and regulatory standards are pushing OEMs to deploy semiconductor-based control systems for enhanced fuel efficiency and lower emissions. The global shift toward electric and intelligent mobility continues to reshape the semiconductor landscape, as these chips play a crucial role in energy conversion, battery management, and vehicle intelligence, supporting smarter and more sustainable automotive ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $74.3 Billion |

| Forecast Value | $164.7 Billion |

| CAGR | 8.4% |

The microcontroller segment was valued at USD 21.3 billion in 2024. Increasing electronic content in vehicles, especially within electric and ADAS-equipped models, continues to boost demand for high-performance automotive microcontrollers. These components remain integral to systems such as powertrain control, battery management, airbags, infotainment, and domain controllers. With the rise of software-defined vehicles (SDVs), the reliance on MCUs is expanding as they enable faster real-time computing and advanced vehicle coordination across multiple subsystems.

The light commercial vehicles (LCVs) segment is projected to register a CAGR of 7.9% throughout 2034. Electrification of urban delivery fleets and integration of connected telematics are key contributors to this growth. The increasing production of Class 2 commercial vehicles and the rising focus on fleet sustainability are creating steady demand for semiconductors designed for LCV electrification and digital monitoring.

U.S. Automotive Semiconductor Market generated USD 17.4 billion in 2024. The accelerating adoption of electric vehicles, coupled with favorable government incentives and stringent regulatory frameworks, is driving semiconductor demand across the nation. Manufacturers are realigning R&D strategies to match OEM requirements for zonal E/E architectures and developing advanced AI- and ML-based processors that meet AEC-Q100 Grade 1 standards for safety and reliability.

Prominent companies operating in the Global Automotive Semiconductor Market include ZF Friedrichshafen AG, Renesas Electronics Corporation, STMicroelectronics N.V., Infineon Technologies AG, Analog Devices, Inc., NXP Semiconductors N.V., Rohm Co., Ltd., Advanced Micro Devices, Continental, Toshiba, Texas Instruments, Inc., Tower Semiconductor Ltd., TE Connectivity, Microchip Technology Inc., Onsemi, Melexis N.V., Robert Bosch GmbH, Micron Technology, and Allegro Microsystems. Leading companies in the automotive semiconductor industry are focusing on innovation, strategic alliances, and capacity expansion to strengthen their market position. They are heavily investing in R&D to develop chips that support electric and autonomous vehicle architectures while enhancing energy efficiency and processing speed. Partnerships with OEMs and Tier-1 suppliers help in aligning product development with emerging vehicle platforms.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Component type trends

- 2.2.2 Vehicle type trends

- 2.2.3 Application trends

- 2.2.4 Sales channel trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical Success Factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Electrification and powertrain evolution is driving demand for automotive semiconductors

- 3.2.1.2 Increasing focus on advanced driver-assistance systems (ADAS) and autonomous driving

- 3.2.1.3 Rising integration of infotainment systems and in-vehicle networking

- 3.2.1.4 Growing need for connectivity and vehicle-to-everything (V2X) communication

- 3.2.1.5 Regulatory pressure and stricter emission standards are accelerating semiconductor adoption

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Supply Chain Disruptions

- 3.2.2.2 High R&D and Compliance Costs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Sustainability Measures

- 3.11 Patent and IP analysis

- 3.12 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates & Forecast, By Component Type, 2021-2034 (USD Billion & Units)

- 5.1 Key trends

- 5.2 Microcontrollers (MCUs)

- 5.3 Sensors

- 5.4 Power semiconductors

- 5.5 Memory

- 5.6 Analog & mixed-signal ICs

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Vehicle Type, 2021-2034 (USD Billion & Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.3 Light commercial vehicles (LCVs)

- 6.4 Heavy commercial vehicles (HCVs)

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion & Units)

- 7.1 Key trends

- 7.2 Powertrain & electrification

- 7.2.1 Engine control units (ECU)

- 7.2.2 Battery management systems (BMS)

- 7.2.3 Onboard chargers

- 7.2.4 Others

- 7.3 Safety systems

- 7.3.1 Advanced driver assistance systems (ADAS)

- 7.3.2 Anti-lock braking systems (ABS)

- 7.3.3 Electronic stability control (ESC)

- 7.3.4 Others

- 7.4 Body electronics

- 7.4.1 Door, seat & window control

- 7.4.2 Lighting (LED, Adaptive headlamps)

- 7.4.3 HVAC systems

- 7.4.4 Others

- 7.5 Chassis & suspension

- 7.5.1 Electric power steering (EPS)

- 7.5.2 Suspension control units

- 7.5.3 Others

- 7.6 Infotainment & telematics

- 7.6.1 Audio processing & amplifiers

- 7.6.2 GPS & navigation systems

- 7.6.3 Others

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021-2034 (USD Billion & Units)

- 8.1 Key trends

- 8.2 OEMs

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Infineon Technologies AG

- 10.1.2 NXP Semiconductors N.V.

- 10.1.3 STMicroelectronics N.V.

- 10.1.4 Texas Instruments, Inc.

- 10.1.5 Renesas Electronics Corporation

- 10.1.6 Microchip Technology Inc.

- 10.2 Regional Key Players

- 10.2.1 North America:

- 10.2.1.1 Advanced Micro Devices (AMD)

- 10.2.1.2 Analog Devices, Inc.

- 10.2.1.3 Micron Technology

- 10.2.1.4 Onsemi

- 10.2.2 Europe:

- 10.2.2.1 Continental

- 10.2.2.2 Melexis N.V.

- 10.2.2.3 Robert Bosch GmbH

- 10.2.2.4 ZF Friedrichshafen AG

- 10.2.3 Asia Pacific:

- 10.2.3.1 Toshiba

- 10.2.3.2 Rohm Co., Ltd.

- 10.2.3.3 Tower Semiconductor Ltd.

- 10.2.1 North America:

- 10.3 Niche / Disruptors

- 10.3.1 Allegro Microsystems

- 10.3.2 TE Connectivity