|

시장보고서

상품코드

1858982

디지털 치료제 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2024-2032년)Digital Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2024 - 2032 |

||||||

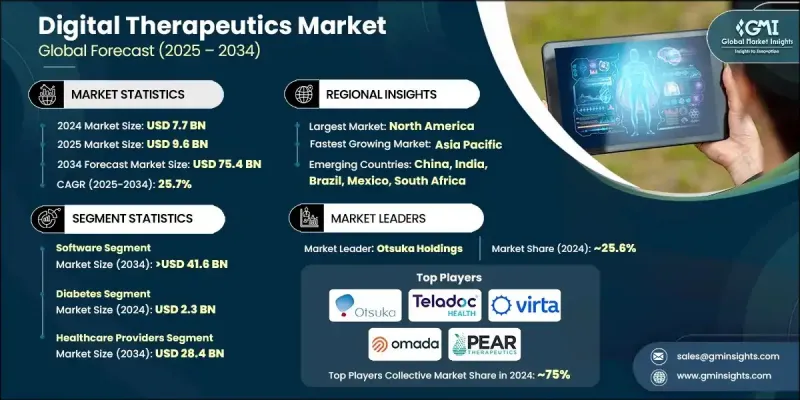

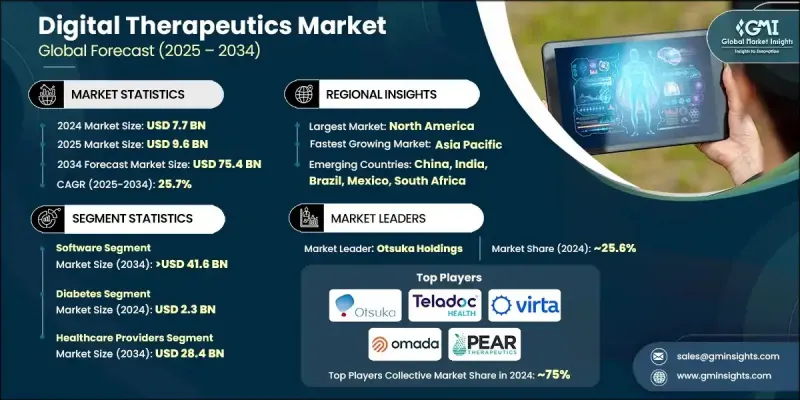

세계의 디지털 치료제 시장 규모는 2024년에 77억 달러로 평가되었고, CAGR 25.7%를 나타내 2034년에는 754억 달러에 이를 것으로 추정됩니다.

성장의 원동력이 되고 있는 것은 심혈관 질환, 당뇨병, 정신 질환 등의 만성 질환의 세계적인 유병률의 상승입니다. 이러한 건강 관리의 지속적인 과제는 비용 효율적이고 확장 가능하고 개별화된 치료법을 제공하는 디지털 치료제 수요를 촉진하고 있습니다. 이러한 소프트웨어 중심 의료 개입은 인공지능, 웨어러블, 게이미피케이션, 행동 건강 도구와의 통합을 통해 어드히어런스, 환자 결과, 참여도를 개선하고 있습니다. 단독으로 또는 전통적인 치료와 함께 작동하도록 설계된 이러한 도구는 현대 건강 관리의 기초가되고 있습니다. 의료 제공업체와 환자가 유연하고 비침습적인 솔루션을 추구함에 따라 디지털 치료제의 매력은 점점 더 커지고 있습니다. 임상적으로 입증된 결과를 가져오는 동시에 전반적인 의료 비용을 줄이는 능력은 고용주, 보험자 및 공공 의료 시스템에 특히 매력적입니다. 급여자의 지원 증가와 주요 시장에서 규제 당국의 수용 확대로 대사성 질환에서 정신 건강에 이르기까지 치료 분야의 개발과 개발이 더욱 가속화되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 77억 달러 |

| 예측 금액 | 754억 달러 |

| CAGR | 25.7% |

소프트웨어 분야는 2024년에 54.3%의 점유율을 차지했고, 2034년에는 CAGR 25.9%의 성장률로 416억 달러에 이를 것으로 예측됩니다. 이 부문에는 사용자 데이터, 행동 동향 및 AI 주도 알고리즘을 기반으로 맞춤형 치료 개입을 허용하는 On-Premise 및 클라우드 플랫폼이 포함됩니다. 이러한 솔루션은 습관 형성 및 만성 질환 관리를 촉진할 뿐만 아니라 스마트폰, 컴퓨터, 태블릿 등의 디지털 기기에 걸친 확장성과 접근성을 통해 널리 사용되고 있습니다. 접근이 용이해지고, 지속적인 치료를 원격으로 제공할 수 있게 됨으로써, 소프트웨어 기반의 디지털 치료제는 예방이나 지속적인 치료의 틀로 선호되는 모델이 되고 있습니다.

당뇨병 분야는 2024년에 23억 달러를 창출했습니다. 1형 당뇨병, 2형 당뇨병, 임신성 당뇨 등 모든 당뇨병의 이환율 증가는 실시간 모니터링 및 지속 가능한 라이프스타일 변경을 가능하게 하는 도구에 대한 수요 증가에 기여하고 있습니다. 디지털 치료제는 행동 코칭, 포도당 추적, 복약 알림, 분석 기반 인사이트 등 맞춤형 개입을 제공하며 장기 당뇨병 관리 계획에서 중요한 구성 요소로 자리매김하고 있습니다. 이 부문은 신진 대사 건강 관리에서 DTx에 대한 환자의 인식과 임상 인지 증가로 이익을 얻고 있습니다.

2024년 북미의 디지털 치료제 시장 점유율은 58.1%에 달했습니다. 이 지역의 강력한 건강 관리 인프라, 만성 질환의 유병률 상승, 유리한 규제 상황이 채용을 뒷받침하고 있습니다. 미국과 캐나다에서는 고용주들이 직원의 건강 증진과 보험료 절감으로 인해 직장의 웰니스 전략에 DTx 플랫폼을 도입하는 경우가 늘고 있습니다. 게다가 보험 상환이 널리 이용 가능하고 기술 도입이 견조하다는 것은 DTx의 주류 임상 및 웰니스 환경에의 통합을 뒷받침하고 있습니다.

세계 디지털 치료제 시장의 주요 기업은 Teladoc Health, Virta Health, LifeScan, Hyfe, Omada Health, Akili Interactive, Pear Therapeutics, Orexo, Otsuka Holdings, Click Therapeutics, Propeller Health(ResMed), AmerisourceBergen입니다. 디지털 치료제 기업은 현재 상태를 강화하기 위해 지불 기관, 제약 회사 및 의료 시스템과의 전략적 파트너십에 주력하고 도달 범위를 넓히고 상환 적용 범위를 확보하고 있습니다. 많은 기업들이 AI, 머신러닝, 실시간 환자 모니터링을 통해 플랫폼의 기능을 강화하기 위해 연구 개발에 많은 투자를 하면서 신흥 시장에 진출하기 위해 세계 판매망을 확대하고 있습니다. 규제 당국의 승인은 여전히 우선권이며, 기업은 보다 신속한 승인을 얻기 위해 당국과 긴밀하게 협력하고 있습니다. 전자 의료 기록과 원격 의료 플랫폼과의 통합은 또한 상호 운용성과 환자 참여를 향상시키는 것을 목표로 한 핵심적인 노력입니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 만성 질환 증가

- 비용 억제에 대한 수요 증가

- 퀄리티 오브 케어 제공 확대

- 높아지는 디지털 치료제 인기

- 업계의 잠재적 위험 및 과제

- 데이터 보안 및 프라이버시에 대한 우려

- 숙련 IT 전문가의 부족

- 시장 기회

- 예방 의료와 밸류 베이스 의료에의 변화 고조

- 병용 요법 모델의 확대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국

- 캐나다

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 북미

- 기술·정세

- 현재의 기술 동향

- 신흥기술

- 향후 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발표

- 확장 계획

제5장 시장 추계·예측 : 구성 요소별(2021-2034년)

- 주요 동향

- 소프트웨어

- On-Premise

- 클라우드 기반

- 하드웨어

- 웨어러블 기기

- 센서 및 모니터링 기기

- 기타 기기

- 서비스

- 컨설팅 및 통합

- 교육 및 훈련

- 기타 서비스

제6장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 당뇨병

- 비만

- 심혈관

- 정신 및 행동건강

- 고혈압

- 불면증

- 기타 용도

제7장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 의료 제공자

- 병원

- 진료소

- 원격의료 플랫폼

- 지불 기관

- 환자

- 기타 최종 사용

제8장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- AmerisourceBergen

- Akili Interactive

- Click Therapeutics

- Hyfe

- LifeScan

- Omada Health

- Orexo

- Otsuka Holdings

- Pear Therapeutics

- Propeller Health(ResMed)

- Teladoc Health

- Virta Health

The Global Digital Therapeutics Market was valued at USD 7.7 billion in 2024 and is estimated to grow at a CAGR of 25.7% to reach USD 75.4 billion by 2034.

The growth is fueled by the rising global prevalence of chronic illnesses such as cardiovascular diseases, diabetes, and mental health conditions. These ongoing healthcare challenges are driving demand for digital therapeutics, which deliver cost-efficient, scalable, and personalized treatment alternatives. These software-driven medical interventions are increasingly integrated with artificial intelligence, wearables, gamification, and behavioral health tools that improve adherence, patient outcomes, and engagement. Designed to work either independently or in conjunction with traditional treatments, these tools are becoming a cornerstone of modern healthcare. As providers and patients increasingly seek flexible and non-invasive solutions, the appeal of digital therapeutics continues to grow. Their ability to deliver clinically proven outcomes while reducing overall care costs makes them particularly attractive to employers, insurers, and public health systems. Growing support from payers and expanded regulatory acceptance across major markets are further accelerating development and deployment across therapeutic areas, from metabolic conditions to mental wellness.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.7 Billion |

| Forecast Value | $75.4 Billion |

| CAGR | 25.7% |

The software segment held a 54.3% share in 2024 and is anticipated to reach USD 41.6 billion by 2034, growing at a CAGR of 25.9%. This segment includes both on-premise and cloud-based platforms that enable tailored therapeutic interventions based on user data, behavioral trends, and AI-driven algorithms. These solutions not only promote habit formation and chronic disease management but are also widely adopted due to their scalability and accessibility across digital devices such as smartphones, computers, and tablets. The growing ease of access and ability to deliver continuous care remotely make software-based digital therapeutics a preferred model in preventive and ongoing treatment frameworks.

The diabetes segment generated USD 2.3 billion in 2024. Increasing rates of all forms of diabetes, Type 1, Type 2, and gestational, are contributing to rising demand for tools that enable real-time monitoring and sustainable lifestyle changes. Digital therapeutics provide tailored interventions, including behavioral coaching, glucose tracking, medication reminders, and analytics-based insights, positioning them as key components in long-term diabetes care plans. This segment continues to benefit from growing patient awareness and clinical recognition of DTx in metabolic health management.

North America Digital Therapeutics Market held 58.1% share in 2024. The region's strong healthcare infrastructure, rising prevalence of chronic conditions, and favorable regulatory landscape are boosting adoption. In the U.S. and Canada, employers are increasingly including DTx platforms in workplace wellness strategies to enhance employee health outcomes and reduce insurance expenditures. Additionally, widespread reimbursement availability and robust technology adoption are supporting the integration of DTx into mainstream clinical and wellness environments.

Key players in the Global Digital Therapeutics Market are Teladoc Health, Virta Health, LifeScan, Hyfe, Omada Health, Akili Interactive, Pear Therapeutics, Orexo, Otsuka Holdings, Click Therapeutics, Propeller Health (ResMed), and AmerisourceBergen. To strengthen their presence, digital therapeutics companies are focusing on strategic partnerships with payers, pharmaceutical firms, and healthcare systems to broaden reach and ensure reimbursement coverage. Many are expanding their global distribution networks to penetrate emerging markets while investing heavily in R&D to enhance platform functionality using AI, machine learning, and real-time patient monitoring. Regulatory approvals remain a priority, with companies working closely with agencies to gain faster clearances. Integration with electronic health records and telehealth platforms is another core focus, aimed at improving interoperability and patient engagement.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Component trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic disease

- 3.2.1.2 Rising demand for cost containment

- 3.2.1.3 Expansion of quality-of-care delivery

- 3.2.1.4 Growing popularity of digital therapeutics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data security and privacy concerns

- 3.2.2.2 Lack of skilled IT professionals

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing shift toward preventive and value-based care

- 3.2.3.2 Expansion of combination therapy models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.4.1 North America

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 On-premises

- 5.2.2 Cloud-based

- 5.3 Hardware

- 5.3.1 Wearable devices

- 5.3.2 Sensors and monitoring devices

- 5.3.3 Other devices

- 5.4 Services

- 5.4.1 Consulting and integration

- 5.4.2 Training and education

- 5.4.3 Other services

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Diabetes

- 6.3 Obesity

- 6.4 Cardiovascular

- 6.5 Mental & behavior health

- 6.6 Hypertension

- 6.7 Insomnia

- 6.8 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Healthcare providers

- 7.2.1 Hospitals

- 7.2.2 Clinics

- 7.2.3 Telehealth platforms

- 7.3 Payers

- 7.4 Patients

- 7.5 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AmerisourceBergen

- 9.2 Akili Interactive

- 9.3 Click Therapeutics

- 9.4 Hyfe

- 9.5 LifeScan

- 9.6 Omada Health

- 9.7 Orexo

- 9.8 Otsuka Holdings

- 9.9 Pear Therapeutics

- 9.10 Propeller Health (ResMed)

- 9.11 Teladoc Health

- 9.12 Virta Health