|

시장보고서

상품코드

1665403

스마트 테일게이트 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Smart Tailgate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

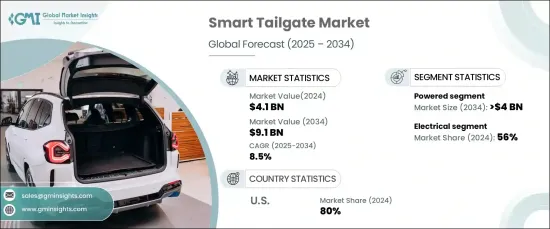

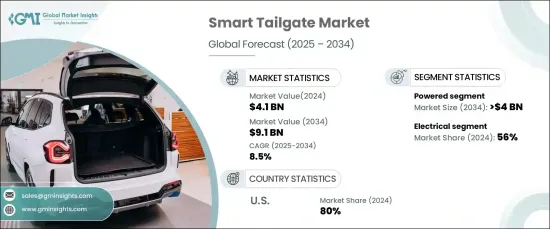

세계의 스마트테일 게이트 시장은 2024년에 41억 달러로 평가되며, 2025-2034년에 CAGR 8.5%로 성장할 것으로 예측됩니다. 이러한 성장의 주요 요인은 첨단 차량용 자동화 및 편의 기능에 대한 수요 증가에 기인합니다. 자동차 제조업체들은 혁신적인 기술을 도입하기 위해 차량 인터페이스를 지속적으로 강화하고 있습니다. 자동 개폐 기능을 갖춘 스마트 테일게이트 시스템은 핸즈프리 액세스를 제공하여 무거운 짐을 관리하는 사용자에게 특히 유용합니다. 사용자 친화적이고 기술적으로 진보된 솔루션에 대한 강조는 현대 자동차의 편의성 향상에 대한 소비자의 선호와 일치합니다.

또한 SUV 및 크로스오버와 같은 대형 차량의 인기가 높아짐에 따라 스마트 테일게이트의 채택이 크게 증가하고 있습니다. 이러한 시스템은 장애물을 감지하는 센서를 통합하여 부상이나 손상의 위험을 줄이기 때문에 안전과 보안을 강화하여 시장 성장을 가속하고 있습니다. 자동차의 안전 기능이 지속적으로 발전하고 있는 것은 기능성과 사용자 만족도를 향상시키는 데 있으며, 이러한 기술의 중요성을 강조하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작 금액 | 41억 달러 |

| 예상 금액 | 91억 달러 |

| CAGR | 8.5% |

시장은 수동, 전동, 핸즈프리 옵션으로 세분화되어 있으며, 2024년 시장 점유율은 전동식이 50% 이상을 차지했으며, 2034년까지 이 부문은 40억 달러 이상에 달할 것으로 예상되며, 이는 편리하고 첨단 차량 기능에 대한 소비자의 욕구가 증가하고 있음을 반영합니다. 전동식 스마트 테일게이트를 자동차에 통합하는 것은 진화하는 기대에 부응하고 경쟁력을 강화하려는 자동차 제조업체의 노력을 보여줍니다.

스마트 테일게이트의 메커니즘에는 전기, 유압, 공압이 있으며, 2024년 시장 점유율은 전기 시스템이 56%를 차지하며, 이는 조작이 간편하고 에너지 효율적인 솔루션을 원하는 소비자 수요에 의해 주도될 것으로 보입니다. 이러한 시스템은 버튼 개폐와 같은 기능을 통해 테일게이트의 제어를 단순화합니다. 원활한 무선 작동은 스마트하고 친환경적인 자동차에 대한 선호도가 높아짐에 따라 효율성과 접근성을 향상시키며, 무선으로 작동할 수 있습니다. 무선도어잠금 및 원격 제어와 같은 첨단 기술의 통합은 사용자의 편의성을 더욱 향상시켜 전동식 스마트 테일게이트 시스템의 매력을 더욱 강화합니다.

북미에서는 미국이 2024년 스마트 테일게이트 시장의 80%라는 놀라운 점유율을 차지하고 있습니다. 캠핑, 드라이브 여행 등 야외 레크리에이션 활동 증가로 첨단 기능이 탑재된 자동차에 대한 수요가 증가하고 있습니다. 소비자들은 자동차 구매시 편의성과 안전성을 우선시하므로 스마트 테일게이트는 높은 부가가치를 창출하고 있습니다. 이러한 시스템은 트렁크에 쉽게 접근할 수 있도록 도와주며, 외출하는 개인들의 요구를 충족시켜줍니다. 아웃도어 지향적인 라이프스타일과 장기적인 드라이브 여행으로의 전환은 지역 전체에서 스마트 테일게이트 시스템의 보급을 지속적으로 촉진하고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 조사 디자인

- 조사 어프로치

- 데이터 수집 방법

- 기본 추정과 계산

- 기준연도 산출

- 시장 추정의 주요 동향

- 예측 모델

- 1차 조사와 검증

- 1차 정보

- 데이터 마이닝 소스

- 시장 스코프와 정의

제2장 개요

제3장 산업 인사이트

- 에코시스템 분석

- 원료 공급업체

- 부품 공급업체

- 제조업체

- 유통 채널

- 최종사용자

- 공급업체 상황

- 이익률 분석

- 기술 혁신 상황

- 특허 분석

- 주요 뉴스 & 구상

- 규제 상황

- 비용 분석

- 영향요인

- 촉진요인

- 자동차 쾌적성 기능의 증가

- 소비자의 편리성에 대한 기대의 증가

- 자동차의 기술적 진보

- 자동차 고급품 부문의 성장

- 산업의 잠재적 리스크·과제

- 높은 제조 비용

- 기술적 복잡성

- 촉진요인

- 성장 가능성 분석

- Porter의 산업 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추정·예측 : 오퍼링별, 2021-2034년

- 주요 동향

- 수동

- 전동

- 핸즈 프리

제6장 시장 추정·예측 : 차종별, 2021-2034년

- 주요 동향

- 해치백

- 세단

- SUV차

제7장 시장 추정·예측 : 메커니즘별, 2021-2034년

- 주요 동향

- 전동

- 유압

- 공기압

제8장 시장 추정·예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 뉴질랜드

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트

- 남아프리카공화국

- 사우디아라비아

제9장 기업 개요

- Aisin Seiki

- Aptiv

- Bosch

- Brose

- Continental

- Ficosa

- Hella

- Huf Holding

- Johnson

- Kiekert

- Lear

- Magna

- Mitsuba

- Stabilus

- Zhejiang

The Global Smart Tailgate Market, valued at USD 4.1 billion in 2024, is projected to grow at a CAGR of 8.5% from 2025 to 2034. This expansion is largely driven by the increasing demand for advanced in-vehicle automation and convenience features. Automotive manufacturers are continuously enhancing vehicle interfaces to incorporate innovative technologies. Smart tailgate systems with automated opening and closing functions offer hands-free access, making them particularly useful for users managing heavy loads. The emphasis on user-friendly, tech-forward solutions aligns with consumer preferences for greater convenience in modern vehicles.

Additionally, the rising popularity of larger vehicles, such as SUVs and crossovers, has significantly boosted the adoption of smart tailgates. Safety and security enhancements also propel market growth, as these systems reduce the risk of injury or damage by integrating sensors to detect obstacles. The ongoing evolution of vehicle safety features highlights the importance of these technologies in improving functionality and user satisfaction.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.1 Billion |

| Forecast Value | $9.1 Billion |

| CAGR | 8.5% |

The market, segmented by offering into manual, powered, and hands-free options, saw the powered segment dominate with over 50% of the market share in 2024. By 2034, this segment is anticipated to surpass USD 4 billion, reflecting the growing consumer appetite for convenient, high-tech vehicle features. The integration of powered smart tailgates into vehicles demonstrates automakers' efforts to meet evolving expectations and enhance their competitive edge.

Mechanisms for smart tailgates include electrical, hydraulic, and pneumatic systems. Electrical systems held a 56% market share in 2024, driven by consumer demand for easily operable and energy-efficient solutions. These systems simplify tailgate control with features like button-operated opening and closing. The seamless, cordless operation improves efficiency and accessibility while aligning with the growing preference for smart, eco-friendly vehicles. The incorporation of advanced technologies like keyless entry and remote control further enhances user convenience and reinforces the appeal of electrical smart tailgate systems.

In North America, the United States dominated the regional smart tailgate market with an impressive 80% share in 2024. The rise in outdoor recreational activities, including camping and road trips, has led to increased demand for vehicles equipped with advanced features. Consumers prioritize convenience and safety when purchasing vehicles, making smart tailgates a valuable addition. These systems facilitate effortless access to the trunk, catering to the needs of individuals on the go. The shift towards outdoor-oriented lifestyles and longer road trips continues to drive the penetration of smart tailgate systems across the region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material providers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 Distribution channel

- 3.1.5 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Cost analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing vehicle comfort features

- 3.9.1.2 Rising consumer convenience expectations

- 3.9.1.3 Technological advancements in vehicles

- 3.9.1.4 Growing automotive luxury segment

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High manufacturing costs

- 3.9.2.2 Technical complexity

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Offering, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Manual

- 5.3 Powered

- 5.4 Hands-Free

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Hatchback

- 6.3 Sedan

- 6.4 SUVs

Chapter 7 Market Estimates & Forecast, By Mechanism, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Electrical

- 7.3 Hydraulic

- 7.4 Pneumatic

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 ANZ

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Aisin Seiki

- 9.2 Aptiv

- 9.3 Bosch

- 9.4 Brose

- 9.5 Continental

- 9.6 Ficosa

- 9.7 Hella

- 9.8 Huf Holding

- 9.9 Johnson

- 9.10 Kiekert

- 9.11 Lear

- 9.12 Magna

- 9.13 Mitsuba

- 9.14 Stabilus

- 9.15 Zhejiang