|

시장보고서

상품코드

1684572

PCR 플라스틱 포장 시장 : 기회, 성장 촉진요인, 산업 동향 분석(2025-2034년)PCR Plastic Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

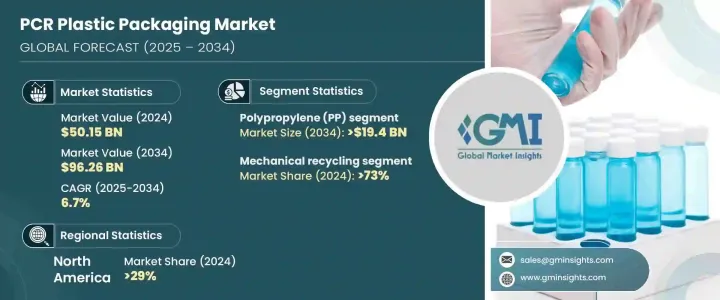

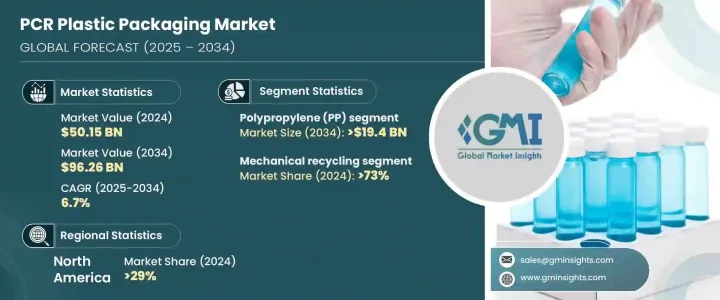

세계의 PCR 플라스틱 포장 시장은 2024년 501억 5,000만 달러로 평가되었으며, 2025년부터 2034년까지 연평균 성장률(CAGR) 6.7%로 성장할 것으로 예측됩니다.

이 시장은 지속 가능성이 비즈니스의 핵심 초점이 되고, 버진 플라스틱버진 플라스틱(신재 플라스틱) 대체재에 대한 수요가 계속 증가함에 따라 상당한 성장을 보이고 있습니다. 다양한 산업 분야의 기업들이 환경 목표를 달성하고 친환경 제품에 대한 소비자의 기대에 부응하기 위해 PCR 플라스틱을 점점 더 많이 채택하고 있습니다. 순환 경제로의 전환과 플라스틱 폐기물 관리에 대한 엄격한 규제가 시장의 확장을 더욱 촉진하고 있습니다.

플라스틱 시장은 플라스틱 종류에 따라 폴리에틸렌 테레프탈레이트(PET), 폴리에틸렌(PE), 폴리스티렌(PS), 폴리염화비닐(PVC), 폴리프로필렌(PP), 바이오 기반 플라스틱으로 세분화됩니다. 이 중 폴리프로필렌(PP)이 가장 빠른 성장을 보일 것으로 예상되며, 연평균 8.4%의 성장률로 2034년까지 194억 달러에 달할 것으로 전망됩니다. PP는 다용도성, 강도, 광범위한 응용 분야, 특히 식품, 헬스케어 및 소비재 포장 분야에서 각광받고 있습니다. 열과 화학 물질에 대한 내성이 강해 높은 안전 및 성능 표준이 요구되는 포장 솔루션에 신뢰할 수 있는 옵션입니다. 또한 가볍고 내구성이 뛰어난 포장재에 대한 관심이 높아지면서 PP에 대한 시장의 수요는 더욱 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 501억 5,000만 달러 |

| 예측 금액 | 962억 6,000만 달러 |

| CAGR | 6.7% |

PCR 플라스틱 포장 시장은 재활용 방법에 따라 기계적 재활용과 화학적 재활용으로 나뉩니다. 기계적 재활용 부문은 2024년에 73%로 가장 큰 점유율을 차지할 것으로 예상됩니다. 기계적 재활용은 비용 효율성과 확립된 방법으로 인해 계속해서 선두를 달리고 있습니다. 이 공정은 화학 구조를 변경하지 않고 플라스틱을 물리적으로 재처리하여 PET, PP, PE와 같은 일반적인 소재에 적합하게 만드는 것입니다. 재활용 인프라가 개선되고 재활용 함량이 높은 포장재에 대한 소비자 수요가 증가함에 따라 이 부문은 향후 몇 년 동안 우위를 유지할 것으로 예상됩니다. 화학 재활용은 아직 신흥 분야이지만 혼합 및 오염된 플라스틱을 처리할 수 있는 능력으로 주목받고 있어 향후 시장 성장을 위한 새로운 기회가 열릴 수 있습니다.

북미는 2024년 PCR 플라스틱 포장재 시장에서 29%의 점유율을 차지할 것으로 예상됩니다. 미국에서는 친환경 제품에 대한 수요 증가와 주 차원의 환경 규제 준수에 대한 필요성에 힘입어 시장이 빠르게 성장하고 있습니다. 탄소 발자국을 줄이고 재활용을 촉진하기 위해 지속 가능성 이니셔티브의 일환으로 PCR 플라스틱을 채택하는 기업이 점점 더 많아지고 있습니다. 이러한 변화는 특히 식품, 음료, 개인 위생용품과 같은 산업에서 두드러지게 나타나며, 생산 주기에서 쉽게 재활용 및 재사용할 수 있는 포장재 사용이 강조되고 있습니다. 첨단 재활용 기술에 대한 혁신과 투자에 집중하고 있는 이 지역은 세계 시장에서의 입지를 더욱 강화할 것으로 예상됩니다.

전반적으로 PCR 플라스틱 포장 시장은 진화하는 소비자 선호도, 규제 프레임워크, 재활용 기술의 발전에 힘입어 상당한 성장세를 보일 것으로 전망됩니다. 기업들이 지속 가능성을 지속적으로 우선시함에 따라 PCR 플라스틱의 채택이 가속화되어 가치 사슬 전반에 걸쳐 이해관계자들에게 새로운 기회를 창출할 것으로 보입니다.

목차

제1장 조사 방법과 조사 범위

- 시장 범위와 정의

- 기본 추정과 계산

- 예측 계산

- 데이터 소스

- 1차

- 2차

- 유료

- 공적

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 밸류체인에 영향을 주는 요인

- 변혁

- 장래 전망

- 제조업체

- 유통업체

- 이익률 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 포장 솔루션에서 재활용 콘텐츠 채택 가속화

- 확장된 생산자 책임(EPR) 프로그램의 확장

- 소비재에서 재활용 페트병에 대한 수요 증가

- 수요를 촉진하고 재활용 용량을 확대하는 데있어 애완 동물의 중요한 역할

- 순환 경제 원칙에 대한 브랜드 약속

- 업계의 잠재적 리스크 및 과제

- 다중 재료 포장 재활용의 복잡성

- 프리미엄 제품의 재활용 소재에 대한 부정적 인식

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추계 및 예측 : 플라스틱 유형별(2021-2034년)

- 주요 동향

- 폴리에틸렌테레프탈레이트(PET)

- 폴리에틸렌(PE)

- 폴리스티렌(PS)

- 폴리염화비닐(PVC)

- 폴리프로필렌(PP)

- 바이오 기반 플라스틱

제6장 시장 추계 및 예측 : 재활용별(2021-2034년)

- 주요 동향

- 기계 재활용

- 화학 재활용

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 병 및 트레이

- 가방 및 자루

- 파우치 및

- 컵 및 항아리

- 클램 쉘

- 욕조

- 기타

제8장 시장 추계 및 예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 소비자 가전제품

- 소비재

- 화장품 및 퍼스널케어

- 가정용품 및 청소용품

- 기타

- 식품 및 음료

- 헬스케어 및 의약품

- 소매

- 기타

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 3plastics

- Amcor

- Berry Global

- Cambrian Packaging

- Evergreen Resources

- Glenroy

- Longdapac

- Mondi

- Proampac

- PTT Global Chemical

- Red Pack

- Regent Plast

- Sanle Plastic

- Udinc

- Winpak

The Global PCR Plastic Packaging Market was valued at USD 50.15 billion in 2024 and is expected to grow at a CAGR of 6.7% between 2025 and 2034. This market is witnessing significant growth as sustainability becomes a core focus for businesses, and the demand for alternatives to virgin plastics continues to rise. Companies across various industries are increasingly adopting PCR plastics to align with environmental goals and meet consumer expectations for eco-friendly products. The shift toward circular economies and stricter regulations on plastic waste management are further driving the market's expansion.

The market is segmented by plastic type into polyethylene terephthalate (PET), polyethylene (PE), polystyrene (PS), polyvinyl chloride (PVC), polypropylene (PP), and bio-based plastics. Among these, polypropylene (PP) is expected to see the fastest growth, projected to grow at a CAGR of 8.4%, reaching USD 19.4 billion by 2034. PP is gaining traction due to its versatility, strength, and wide range of applications, especially in packaging for food, healthcare, and consumer goods. The material's resistance to heat and chemicals makes it a reliable option for packaging solutions that require high safety and performance standards. Additionally, the growing focus on lightweight and durable packaging materials is further boosting the demand for PP in the market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $50.15 Billion |

| Forecast Value | $96.26 Billion |

| CAGR | 6.7% |

The PCR plastic packaging market is also divided by recycling method into mechanical recycling and chemical recycling. The mechanical recycling segment held the largest share of 73% in 2024. Mechanical recycling continues to lead due to its cost-efficiency and established methods. This process involves physically reprocessing plastics without changing their chemical structure, making them suitable for common materials such as PET, PP, and PE. As recycling infrastructure improves and consumer demand for packaging with high recycled content rises, this segment is expected to maintain its dominance in the coming years. Chemical recycling, while still emerging, is gaining attention for its ability to handle mixed and contaminated plastics, which could open new opportunities for market growth in the future.

North America accounted for a 29% share of the PCR plastic packaging market in 2024. In the United States, the market is growing rapidly, driven by increasing demand for eco-friendly products and the need to comply with state-level environmental regulations. Companies are increasingly adopting PCR plastics as part of their sustainability initiatives, helping to reduce carbon footprints and promote recycling. This shift is particularly evident in industries like food, beverages, and personal care products, where there is a strong emphasis on using packaging materials that can be easily recycled and reused in production cycles. The region's focus on innovation and investment in advanced recycling technologies is expected to further strengthen its position in the global market.

Overall, the PCR plastic packaging market is poised for substantial growth, supported by evolving consumer preferences, regulatory frameworks, and advancements in recycling technologies. As businesses continue to prioritize sustainability, the adoption of PCR plastics is likely to accelerate, creating new opportunities for stakeholders across the value chain.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Disruptions

- 3.1.3 Future outlook

- 3.1.4 Manufacturers

- 3.1.5 Distributors

- 3.2 Profit margin analysis

- 3.3 Key news & initiatives

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Accelerated adoption of recycled content in packaging solutions

- 3.5.1.2 Expansion of extended producer responsibility (EPR) programs

- 3.5.1.3 Increased demand for recycled pet bottles in consumer goods

- 3.5.1.4 Pet's crucial role in driving demand and expanding recycling capacity

- 3.5.1.5 Brand commitment to circular economy principles

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 Complexity in recycling multi-material packaging

- 3.5.2.2 Negative perceptions of recycled materials in premium products

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Plastic Type, 2021-2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Polyethylene terephthalate (PET)

- 5.3 Polyethylene (PE)

- 5.4 Polystyrene (PS)

- 5.5 Polyvinyl chloride (PVC)

- 5.6 Polypropylene (PP)

- 5.7 Bio-based plastics

Chapter 6 Market Estimates & Forecast, By Recycling, 2021-2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Mechanical recycling

- 6.3 Chemical recycling

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Bottles & trays

- 7.3 Bags & sacks

- 7.4 Pouches & sachets

- 7.5 Cups & jars

- 7.6 Clamshells

- 7.7 Tubs

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 Consumer electronics

- 8.3 Consumer goods

- 8.3.1 Cosmetics & personal care

- 8.3.2 Household & cleaning products

- 8.3.3 Others

- 8.4 Food & beverage

- 8.5 Healthcare & pharmaceutical

- 8.6 Retail

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3plastics

- 10.2 Amcor

- 10.3 Berry Global

- 10.4 Cambrian Packaging

- 10.5 Evergreen Resources

- 10.6 Glenroy

- 10.7 Longdapac

- 10.8 Mondi

- 10.9 Proampac

- 10.10 PTT Global Chemical

- 10.11 Red Pack

- 10.12 Regent Plast

- 10.13 Sanle Plastic

- 10.14 Udinc

- 10.15 Winpak