|

시장보고서

상품코드

1910905

의약품 플라스틱 포장 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Pharmaceutical Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

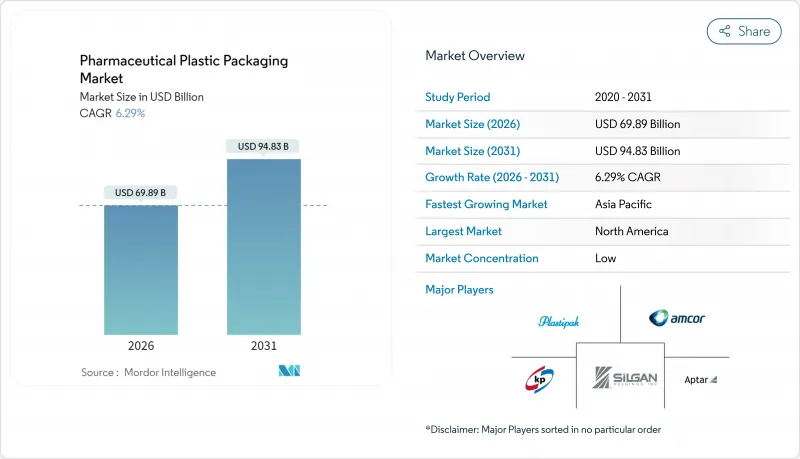

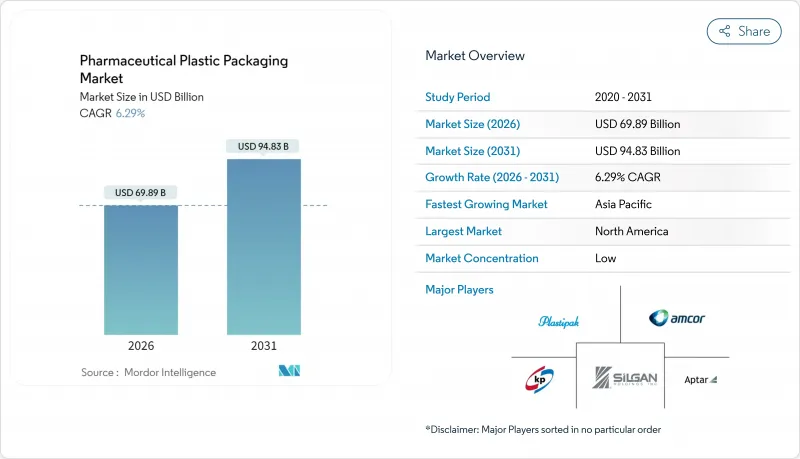

의약품 플라스틱 포장 시장은 2025년의 657억 5,000만 달러에서 2026년에는 698억 9,000만 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR 6.29%로 성장을 지속하여, 2031년에는 948억 3,000만 달러에 달할 전망입니다.

성장의 배경으로는 바이오 의약품 및 주사제의 점유율 확대, 보다 엄격한 추적성 규제, 재활용 가능하고 바이오 유래의 폴리머를 권장하는 지속가능성 요건의 급속한 성숙화를 들 수 있습니다. 2025년 2월에는 EU의 포장 및 포장폐기물 규정(PPWR)이 발효되어 2030년까지 완전 재활용 가능성을 의무화하고 재료 대체 프로그램을 가속화하고 있습니다. 북미 수요는 2025년 11월 의약품 유통망 안전법(DSCSA)의 기한에 따라 스마트하고 직렬화 대응 가능한 형식이 추진되는 혜택을 받고 있습니다. 아시아태평양의 제조업체는 규제 조화와 급증하는 제네릭 의약품의 생산량을 활용하여 이 지역의 성장 전망을 높이고 있습니다. 중견 컨버터 간의 통합(예 : 암코어와 베리 글로벌과의 135억 달러 규모 합병)은 PFAS 프리 배합과 순환형 경제에 대한 투자에 임하기 위한 규모를 형성하고 있습니다.

세계의 의약품 플라스틱 포장 시장의 동향 및 전망

바이오 의약품 및 주사제용 플라스틱 포장의 수요 증가

신규 승인 의약품에 차지하는 바이오 의약품의 비율이 증가하고 있으며, 알칼리 용출, 박리, 파손에 대한 감수성으로 인해 고도의 폴리머가 우선적인 1차 용기로서 자리잡고 있습니다. 게레스하이머사의 시클로올레핀 폴리머 주사기는 유리와 같은 투명성과 우수한 내파손성을 결합하여 고가의 생물학적 제제의 손실을 최소화합니다. 세계의 바이오 의약품 시장은 2030년까지 8,561억 달러에 이를 것으로 예측되고 있으며, 이는 고신뢰 주사제 포장에 대한 수요를 뒷받침하고 있습니다. 검증이 끝난 BFS(Blow-Fill-Seal) 용기는 단일클론항체에 대해 9개월에 걸친 효력이나 pH의 드리프트를 나타내지 않고, 따라서 무균 용도에서 폴리머의 도입 범위를 확대하고 있습니다. 팬데믹 기간 동안 유리 바이알의 부족은 공급망의 위험을 부각시키고 동등한 규제 승인을 얻은 플라스틱 용기를 우선시하는 이중 조달 정책을 촉구했습니다.

신흥 시장에서 제네릭 의약품의 생산 확대

중국의 규제 개혁과 특히 판매승인 보유자 제도의 도입으로 승인 사이클이 단축되고 위탁 제조 제휴가 촉진되어 포장 수요가 증가하고 있습니다. 베이징이 발표한 2025년 지침에는 2027년까지의 의약품 감시 체제 근대화를 위한 24개의 시책이 포함되어 있으며 적합 포장 라인에 대한 명확한 목표가 설정되어 있습니다. 인도와 ASEAN의 상호 승인 프로그램을 통해 규격 조화가 더욱 진행되어 컨버터는 단일 설계를 여러 시장에서 전개할 수 있게 되었습니다. 가격에 민감한 제네릭 의약품은 장거리 수출 운송 중에도 견고성을 유지하는 비용 효율적인 플라스틱을 선호합니다.

확대되는 플라스틱 폐기물 규제(EU SUP, EPR 등)

PPWR(포장 및 포장폐기물 규정)은 2030년까지 EU에서 판매되는 모든 포장재의 재활용 의무화를 규정하고, EPR(생산자 책임 재활용) 비용과 재생재 함유율 기준(PET 식품 포장은 30% 이상)을 도입하여 자본 부담과 컴플라이언스 부담을 증가시킵니다. 의약품 용기에 대해서는 의료 분야의 예외 규정이 있지만, 브랜드 소유자는 여전히 회수 계획에 대한 자금 제공, 다층 라미네이트의 재설계, 2026년까지 접촉 재료에 대한 PFAS의 단계적 폐지를 요구받고 있습니다. 2028년에 도입 예정인 세계통일체계는 디자인의 변경을 필요로 하고, 5%의 재료 절감 목표는 이미 얇아진 벽 두께 사양을 한층 더 압박합니다.

부문 분석

폴리프로필렌은 멸균 내성과 규제 대응성에 의해 2025년 시점에서 의약품 플라스틱 포장 시장의 30.12%를 차지하면서 주도적 지위를 유지했습니다. 그러나 바이오 및 재생 등급은 9.05%의 연평균 복합 성장률(CAGR)로 기존 소재를 능가하고 2031년까지 의약품 플라스틱 포장 시장을 재구축할 전망입니다. 애비엔트의 Mevopur 제품군은 ISO 10993 및 USP VI 인증을 유지하면서 최대 120%의 탄소 실적 저감을 실현하여 순환성과 컴플라이언스의 공존을 실증하고 있습니다. EU의 재생재 함유율 의무화나 FDA의 염료 사용 금지 방침에 의해 재생 원료 수요가 가속하고 있습니다. UPM사의 목재 병 출시는 리그닌이 풍부한 화학 기술의 상업적 실현성을 뒷받침하고 있습니다.

2세대 바이오 폴리올레핀과 화학적 재생 PET는 의약품 등급의 순도에 도달하여 설비 변경 없이 직접 대체를 가능하게 하고 있습니다. 그러나 의약품 등급 재생재의 공급이 제한되어 있기 때문에 즉각적인 규모 확대가 억제되어 가격 프리미엄이 발생하고 있습니다. 수지 대기업은 물류 단축을 위해 유럽 및 북미의 거점 근교에서 생산 능력을 확대하는 한편, 아시아 기업은 급증하는 수주 획득을 위한 수출용 재생 수지 인증 취득을 모색하고 있습니다. 이에 따라 의약품 플라스틱 포장 시장은 기존의 폴리프로필렌(PP)의 우위성과 PPWR(포장 및 포장폐기물 규정) 및 기업의 넷 제로 공약에 따른 재생 가능 폴리머의 신중하면서도 가속하는 침투와의 균형을 이루고 있습니다.

2025년 시점에서는 경구 고형 제제의 보급으로 병 및 고형 용기가 의약품 플라스틱 포장 시장의 26.05%를 차지했습니다. 그러나 프리필드 주사기 및 카트리지가 성장의 주역이며, 바이오 의약품, GLP-1 주사제, 가정용 약물의 보급에 따라 CAGR 8.29%로 확대되고 있습니다. BD사의 RFID 대응 iDFill 주사기는 디바이스와 포장을 일체화하고 DSCSA(의약품 유통망 안전법)의 요건에 적합한 실시간 추적성을 제공합니다.

디지털 연결성, 고점도 내성, 체내 주입기와의 호환성으로 이러한 용기는 범용품에서 고부가가치 엔지니어링 제품으로 진화하고 있습니다. 한편, 바이알이나 앰풀은 병원 조제에 여전히 필수적이지만, 용량대별 바이오 의약품에서는 충전 및 마무리 공정을 효율화하는 게레스하이머사의 폴리머제 EZ-fill 스마트 바이알로의 이행이 진행되고 있습니다. 스틱 팩, 샤쉐, 파우치는 우편 요금과 완충재 비용으로 경질 용기가 불리한 원격 약국의 발송용 포장재로서 발판을 굳히고 있습니다.

지역별 분석

북미는 2025년 시점에서 의약품 플라스틱 포장 시장의 36.05%를 차지하였고, 선진적인 GMP 플랜트, DSCSA 직렬화 기한, 리쇼어링 장려책에 의해 뒷받침되고 있습니다. FDA 지침은 연속 제조와 스마트 센서를 권장하고 있으며, 현지 컨버터는 포장 벽에 RFID 임베딩과 PFAS 프리 필름의 적격성 평가를 추진하고 있습니다. 수입 수지에 대한 관세는 국내 설비 가동률을 향상시키고, 바이오 원료에 대한 투자를 촉진하여 지정학적 충격에 취약한 공급망을 안정화하고 있습니다.

유럽에서는 규제의 엄격함과 지속가능성 리더십이 결합되어 견고하면서도 진화를 계속하는 시장 기반이 형성되고 있습니다. PPWR(포장 및 포장폐기물 규정)은 재활용성, EPR(생산자 책임 재활용) 비용, PFAS 금지를 의무화하고, 지역 컨버터에서 연구개발 예산을 자극하는 재설계를 촉구합니다. 일회용 플라스틱 지침의 규제는 단일 소재 블리스터 필름을 촉진하고 각국의 에코 모듈레이션 시스템은 저탄소 형식을 장려합니다. 북유럽 및 DACH 국가들은 사용된 흡입기 및 주사기의 파일럿 회수 시스템을 주도하여 폴리프로필렌의 클로즈드 루프 경로를 형성합니다.

아시아태평양은 2031년까지 의약품 플라스틱 포장 시장에서 가장 높은 CAGR 9.76%를 달성할 전망입니다. 중국은 2025년 행동계획 하에서 가속화되어 포장품질에 대한 감사를 ICH Q9에 정합시키는 동시에 녹색 공장에 자금을 제공합니다. 인도는 약전 시험과 디지털 추적성을 강화하여 스마트 라벨 공급업체에게 기회를 제공하고 있습니다. ASEAN 상호 승인은 수개월에 걸친 서류 작업을 줄여 수출업체가 회원국 간에 적합 포장을 출하할 수 있게 되었습니다. 일본의 EPR 제도는 의료용 포장재에도 확대되어 PCR 등급 PP 조달의 촉진요인이 됩니다. 이러한 촉진요인이 더하여 아시아태평양의 개발도상국 및 선진국을 불문하고 의약품 플라스틱 포장 시장을 강화하고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 바이오의약품 및 주사제용 플라스틱 포장재의 수요 증가

- 신흥국의 제네릭 의약품 생산 확대

- 가볍고 잘 깨지지 않는 물류상의 우위성

- 재택 치료 및 전자상거래에서의 단회 투여 단위 도입

- 맞춤형 의료용 온사이트 BFS 및 3D 프린팅 금형

- 항균성 및 스마트 폴리머 대응 포장재

- 억제요인

- 확대하는 플라스틱 폐기물 규제(EU의 SUP, EPR 등)

- 휘발성 폴리머 원료 가격의 변동성

- 바이오 로직 유리에서 COP 바이알로의 정책 전환

- 의약품 등급 재생 수지의 공급 부족

- 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁의 격렬함

- 지정학적 시나리오의 평가

제5장 시장 규모 및 성장 예측

- 원재료별

- 폴리프로필렌(PP)

- 폴리에틸렌테레프탈레이트(PET)

- 고밀도 폴리에틸렌(HDPE)

- 저밀도 폴리에틸렌(LDPE)

- 환상 올레핀계 폴리머 및 코폴리머(COP/COC)

- 바이오 및 재활용 플라스틱

- 제품 유형별

- 병 및 고형 용기

- 바이알 및 앰풀

- 프리필드 주사기 및 카트리지

- 블리스터 포장 및 스트립 포장

- 파우치, 스틱 팩 및 사쉐

- 캡, 뚜껑, 마개

- IV 백 및 연질 백

- 포장 형태별

- 경질

- 연질

- 약제 전달 경로별

- 경구

- 주사제 및 주사용

- 안구 및 비강

- 국소적 및 경피적

- 최종 사용자별

- 제약기업

- 위탁개발생산(CDMO)

- 병원 및 진료소

- 재택 치료 환경

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 중동

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Amcor PLC

- Gerresheimer AG

- AptarGroup Inc.

- West Pharmaceutical Services Inc.

- Klockner Pentaplast Group

- Comar LLC

- O.Berk Company LLC

- Pretium Packaging LLC

- Drug Plastics and Glass Co. Inc.

- Gil-Pack Ltd.

- Alpla Group

- Silgan Holdings Inc.

- Placon Corporation

- Sealed Air Corporation

- Plastipak Holdings

제7장 시장 기회 및 미래 전망

CSM 26.02.04The pharmaceutical plastic packaging market is expected to grow from USD 65.75 billion in 2025 to USD 69.89 billion in 2026 and is forecast to reach USD 94.83 billion by 2031 at 6.29% CAGR over 2026-2031.

Growth rests on the rising share of biologics and injectables, stricter traceability rules, and fast-maturing sustainability mandates that reward recyclable and bio-based polymers. In February 2025 the EU's Packaging and Packaging Waste Regulation (PPWR) entered into force, requiring full recyclability by 2030 and accelerating material substitution programs.North American demand benefits from the Drug Supply Chain Security Act (DSCSA) deadline in November 2025, which pushes smart, serialization-ready formats. Asia-Pacific manufacturers leverage regulatory harmonization and surging generic output, lifting the region's growth prospects. Consolidation among mid-tier converters, exemplified by Amcor's USD 13.5 billion merger with Berry Global, brings scale to tackle PFAS-free formulations and circular-economy investments.

Global Pharmaceutical Plastic Packaging Market Trends and Insights

Growing Demand for Plastic Packs for Biologics and Injectables

Biologics now account for a rising share of new drug approvals, and their sensitivity to alkali leaching, delamination, and breakage positions advanced polymers as preferred primary containers. Cyclic olefin polymer syringes from Gerresheimer combine glass-like transparency with superior break resistance, helping minimize costly biologic losses. The global biopharmaceutical sector is expected to reach USD 856.1 billion by 2030, reinforcing demand for high-integrity parenteral packaging. Validated blow-fill-seal containers show no potency or pH drift for monoclonal antibodies over nine months, broadening polymer uptake in sterile applications. During the pandemic, shortages of glass vials highlighted supply-chain risks, prompting dual-sourcing policies that now favor plastic options with equivalent regulatory acceptance.

Expansion of Generic Drug Production in Emerging Markets

Regulatory reforms in China, notably the Marketing Authorization Holder system, shorten approval cycles and attract contract manufacturing alliances that boost packaging volumes. Beijing's 2025 guidance contains 24 measures to modernize drug oversight by 2027, creating clear targets for compliant packaging lines. India and ASEAN mutual recognition programs further harmonize specifications, letting converters scale a single design across multiple markets. Price-sensitive generics also prioritize cost-efficient plastics that remain robust during long-distance export shipments.

Extended Plastics-Waste Regulation (EU SUP, EPR etc.)

The PPWR obliges all packs sold in the EU to be recyclable by 2030 and introduces EPR fees plus recycled-content thresholds-30% for PET food packs-adding capital and compliance burdens. Healthcare exemptions exist for immediate drug containers, yet brand owners must still fund collection schemes, redesign multilayer laminates, and phase out PFAS in contact materials by 2026. Harmonized symbols due in 2028 compel artwork changes, while the 5% material-reduction target squeezes already lean wall-thickness specs.

Other drivers and restraints analyzed in the detailed report include:

- Lightweight, Shatter-Proof Logistics Advantage

- Home-Health and E-Commerce Unit-Dose Adoption

- Volatile Polymer Feedstock Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polypropylene retained leadership with 30.12% of pharmaceutical plastic packaging market share in 2025 thanks to its sterilization tolerance and regulatory familiarity. Yet bio-based and recycled grades are set to outpace all incumbents at 9.05% CAGR, reshaping the pharmaceutical plastic packaging market through 2031. Avient's Mevopur range delivers up to 120% carbon-footprint reduction while keeping ISO 10993 and USP VI credentials, illustrating how circularity and compliance now co-exist. EU recycled-content quotas and the FDA's looming dye phase-out intensify demand for renewable feedstocks. UPM's wood-based bottle launch underscores commercial feasibility of lignin-rich chemistries.

Second-generation bio-polyolefins and chemically recycled PET now reach pharmaceutical purity, unlocking drop-in substitution without retooling. However, limited pharma-grade recyclate supplies restrain immediate scale, creating price premiums. Resin majors ramp capacity near European and North American hubs to shorten logistics, while Asian players eye export-grade r-resin certification to capture surging orders. The pharmaceutical plastic packaging market therefore balances legacy PP dominance with measured yet accelerating penetration of renewable polymers that align with PPWR and corporate net-zero pledges.

Bottles and solid containers captured 26.05% of the pharmaceutical plastic packaging market in 2025 owing to oral solid dosage prevalence. Yet pre-fillable syringes and cartridges headline the growth story, advancing at 8.29% CAGR as biologics, GLP-1 injectables, and home-administered drugs proliferate. BD's RFID-enabled iDFill syringe merges device and pack, supplying real-time traceability that dovetails with DSCSA needs.

Digital connectivity, higher viscosity tolerances, and on-body injector compatibility move these containers from commodity to high-value engineered systems. Conversely, vials and ampoules remain essential for hospital compounding, though dose-banded biologics see a shift to polymer-based EZ-fill Smart vials from Gerresheimer that streamline fill-finish operations. Stick packs, sachets, and pouches gain foothold in tele-pharmacy mailers where postage and cushioning costs punish rigid lines.

The Pharmaceutical Plastic Packaging Market Report is Segmented by Raw Material (Polypropylene, Polyethylene Terephthalate, and More), Product Type (Bottles and Solid Containers, Vials and Ampoules, and More), Packaging Format (Rigid, Flexible), Route of Drug Delivery (Oral, Parenteral/Injectable, and More), End-User (Pharma Manufacturers, Cdmos, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 36.05% of the pharmaceutical plastic packaging market in 2025, supported by advanced GMP plants, DSCSA serialization deadlines, and reshoring incentives. FDA guidance endorses continuous manufacturing and smart sensors, pushing local converters to embed RFID in pack walls and qualify PFAS-free films.Tariffs on imported resins raise domestic capacity utilization and spur investment in bio-based feedstocks, stabilizing supply chains vulnerable to geopolitical shocks.

Europe combines regulatory stringency with sustainability leadership, forging a robust yet evolving market base. The PPWR enforces recyclability, EPR fees, and PFAS bans, forcing redesigns that stimulate R&D budgets among regional converters. Single-Use Plastics Directive restrictions encourage mono-material blister films, while national eco-modulation schemes reward low-carbon formats. Nordic and DACH states lead pilot take-back schemes for used inhalers and injectors, offering closed-loop polypropylene pathways.

Asia-Pacific delivers the highest 9.76% CAGR for the pharmaceutical plastic packaging market through 2031. China accelerates under its 2025 action plan, aligning packaging quality audits with ICH Q9 while funding green factories. India tightens pharmacopoeial tests and digital traceability, creating opportunities for smart-label suppliers. ASEAN mutual recognition saves months of dossier work, letting exporters ship compliant packs across member borders. Japanese EPR schemes extend to medical packs, catalyzing PCR-grade PP sourcing. Together, these tailwinds strengthen the pharmaceutical plastic packaging market across developing and mature APAC nations.

- Amcor PLC

- Gerresheimer AG

- AptarGroup Inc.

- West Pharmaceutical Services Inc.

- Klockner Pentaplast Group

- Comar LLC

- O.Berk Company LLC

- Pretium Packaging LLC

- Drug Plastics and Glass Co. Inc.

- Gil-Pack Ltd.

- Alpla Group

- Silgan Holdings Inc.

- Placon Corporation

- Sealed Air Corporation

- Plastipak Holdings

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for plastic packs for biologics and injectables

- 4.2.2 Expansion of generic drug production in EMs

- 4.2.3 Lightweight, shatter-proof logistics advantage

- 4.2.4 Home-health and e-commerce unit-dose adoption

- 4.2.5 On-site BFS and 3-D printed molds for personalized meds

- 4.2.6 Antimicrobial / smart-polymer enabled packs

- 4.3 Market Restraints

- 4.3.1 Extended plastics-waste regulation (EU SUP, EPR etc.)

- 4.3.2 Volatile polymer feedstock pricing

- 4.3.3 Biologic-glass policy shift toward COP vials

- 4.3.4 Scarcity of pharma-grade r-resin supply

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Assessment of Geopolitical Scenario

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Raw Material

- 5.1.1 Polypropylene (PP)

- 5.1.2 Polyethylene Terephthalate (PET)

- 5.1.3 High-Density Polyethylene (HDPE)

- 5.1.4 Low-Density Polyethylene (LDPE)

- 5.1.5 Cyclic Olefin Polymer / Copolymer (COP/COC)

- 5.1.6 Bio-based and Recycled Plastics

- 5.2 By Product Type

- 5.2.1 Bottles and Solid Containers

- 5.2.2 Vials and Ampoules

- 5.2.3 Pre-fillable Syringes and Cartridges

- 5.2.4 Blister Packs and Strip Packs

- 5.2.5 Pouches / Stick Packs / Sachets

- 5.2.6 Closures, Caps and Lids

- 5.2.7 IV Bags and Flexible Bags

- 5.3 By Packaging Format

- 5.3.1 Rigid

- 5.3.2 Flexible

- 5.4 By Route of Drug Delivery

- 5.4.1 Oral

- 5.4.2 Parenteral / Injectable

- 5.4.3 Ophthalmic / Nasal

- 5.4.4 Topical / Transdermal

- 5.5 By End-User

- 5.5.1 Pharma Manufacturers

- 5.5.2 Contract Development and Manufacturing Orgs (CDMOs)

- 5.5.3 Hospitals and Clinics

- 5.5.4 Home-care Settings

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 United Arab Emirates

- 5.6.4.1.2 Saudi Arabia

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Nigeria

- 5.6.4.2.3 Egypt

- 5.6.4.2.4 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes global overview, market level overview, core segments, financials as available, strategic info, market rank/share, products and services, recent developments)

- 6.4.1 Amcor PLC

- 6.4.2 Gerresheimer AG

- 6.4.3 AptarGroup Inc.

- 6.4.4 West Pharmaceutical Services Inc.

- 6.4.5 Klockner Pentaplast Group

- 6.4.6 Comar LLC

- 6.4.7 O.Berk Company LLC

- 6.4.8 Pretium Packaging LLC

- 6.4.9 Drug Plastics and Glass Co. Inc.

- 6.4.10 Gil-Pack Ltd.

- 6.4.11 Alpla Group

- 6.4.12 Silgan Holdings Inc.

- 6.4.13 Placon Corporation

- 6.4.14 Sealed Air Corporation

- 6.4.15 Plastipak Holdings

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment