|

시장보고서

상품코드

1892850

자동차 물류 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Logistics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

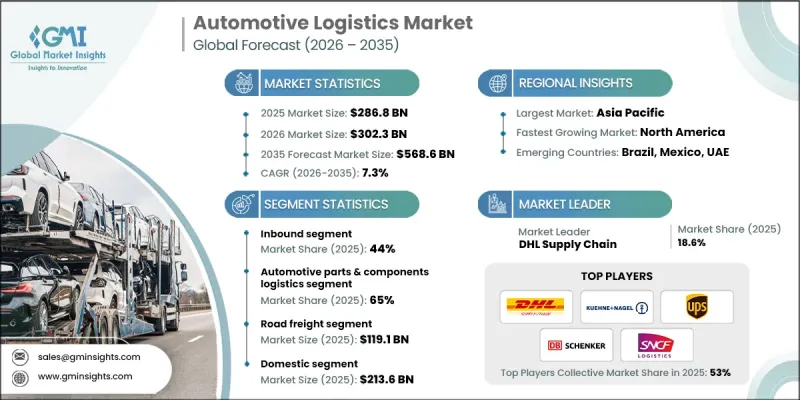

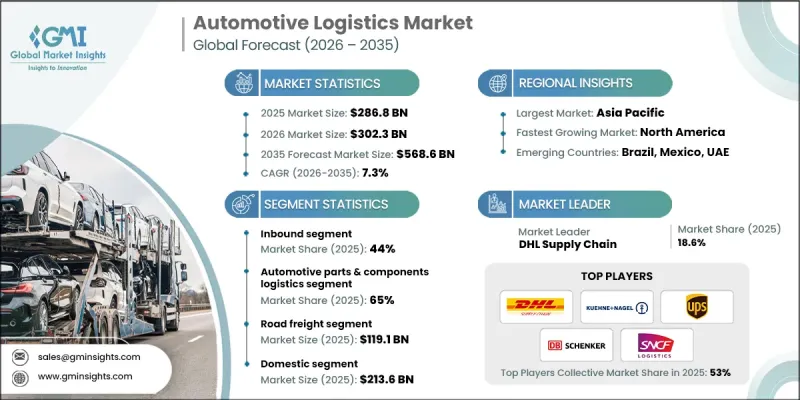

세계의 자동차 물류 시장은 2025년에 2,868억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 7.3%로 성장하여 5,686억 달러에 이를 것으로 예측됩니다.

자동차 산업이 지속적으로 성장함에 따라, 공급망 전체에 걸쳐 차량, 부품 및 구성품을 운송하기 위한 효율적인 물류 솔루션의 필요성이 증가하고 있습니다. 기업들은 운송 경로 최적화, 재고 관리, 실시간 배송 추적이 가능한 소프트웨어의 중요성을 인식하고 있습니다. 많은 자동차 제조업체들은 물류 관리에서 여전히 구식 소프트웨어와 레거시 시스템에 의존하고 있으며, 이는 현대적 솔루션의 통합을 어렵게 만들고 있습니다. 따라서 대규모 데이터 마이그레이션 및 커스터마이징이 필요합니다. 엔드투엔드 공급망의 실시간 가시성 부족, 복잡한 운송 네트워크, 파트너 간 데이터 투명성의 불일치 등은 또 다른 장벽으로 작용하고 있습니다. 이러한 문제를 해결하기 위해 소프트웨어 제공업체들은 AI와 머신러닝을 통합하여 경로 계획 개선, 반복 작업 자동화, 의사결정 강화를 위해 노력하고 있습니다. 예측 분석 및 수요 예측 기능을 통해 기업은 미래 수요를 예측하고, 재고를 최적화하고, 자원을 보다 효율적으로 배분하여 공급망 혼란에 대한 선제적 해결책을 마련할 수 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 시장 규모 | 2,868억 달러 |

| 예측 금액 | 5,686억 달러 |

| CAGR | 7.3% |

인바운드 물류 부문은 2025년 44%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 8%로 성장할 것으로 전망됩니다. 인바운드 물류는 원자재, 부품, 서브 어셈블리를 공급업체에서 OEM 조립 공장으로 효율적으로 운송하는 역할을 담당하며 자동차 물류 시장에서 매우 중요한 위치를 차지하고 있습니다. 고빈도 및 대량 운송 작업은 JIT(Just In Time) 및 JIS(Just In Sequence) 생산을 지원하여 재고 보유 비용을 절감하고 원활한 생산 흐름을 보장합니다. 도로, 철도, 항공, 해상 등 멀티모달 운송의 활용은 인바운드 공급망의 속도, 신뢰성, 비용 효율성을 더욱 향상시킬 수 있습니다.

자동차 부품 및 컴포넌트 물류 부문은 2025년 65%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 7.6%의 성장률을 보일 것으로 전망됩니다. 이 부문이 지배적인 이유는 OEM(자동차 제조업체)과 1, 2차 공급업체 네트워크 간 부품 이동의 복잡성, 양, 빈도에 기인합니다. 이를 통해 부품이 조립 공장, 지역 유통 센터 및 애프터마켓 서비스 네트워크에 안전하고 정시에 비용 효율적으로 배송되어 생산 및 운영이 원활하게 유지될 수 있도록 보장합니다.

중국 자동차 물류 시장은 2025년 432억 달러로 39%의 점유율을 차지할 것으로 예측됩니다. 중국의 우위는 자동차 생산의 급격한 성장, 승용차 및 상용차에 대한 높은 수요, 첨단 물류 기술에 대한 대규모 투자에 의해 촉진되고 있습니다. 이 지역은 발달된 운송 네트워크, 광범위한 창고 및 유통 인프라, 디지털 공급망 솔루션, IoT 기반 추적 시스템, 자동화 자재 운반 시스템의 보급 확대 등의 이점을 가지고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 비용 구조

- 각 단계별 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 가격 동향

- 지역별

- 제품별

- 비용 내역 분석

- 특허 분석

- 지속가능성과 환경 측면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국에 관한 고려사항

- 이용 사례 시나리오

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금조달

제5장 시장 추산 및 예측 : 서비스별, 2022-2035

- 주요 동향

- 인바운드 물류

- 아웃바운드 물류

- 역물류

- 애프터마켓

제6장 시장 추산 및 예측 : 제품별, 2022-2035

- 주요 동향

- 완성차

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 소형차

- 중형

- 대형 차량

- 승용차

- 자동차 부품·컴포넌트

- 차륜 및 타이어

- 전기 및 전자기기

- 보디 및 섀시

- 서스펜션 및 스티어링

- 브레이크 시스템

- 엔진 및 파워트레인

제7장 시장 추산 및 예측 : 운송 수단별, 2022-2035

- 주요 동향

- 도로 화물 운송

- 해상 운송

- 항공 화물

- 철도 화물 운송

제8장 시장 추산 및 예측 : 유통별, 2022-2035

- 주요 동향

- 국내

- 국제

제9장 시장 추산 및 예측 : 지역별, 2022-2035

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 네덜란드

- 스웨덴

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카공화국

- 사우디아라비아

제10장 기업 개요

- Global Player

- C.H. Robinson Worldwide

- CEVA Logistics

- DHL Supply Chain &Global Forwarding

- DSV-Schenker

- Expeditors International of Washington

- GEODIS(SNCF)

- Hellmann Worldwide Logistics

- Kuehne+Nagel International

- Penske Logistics

- XPO Logistics

- Regional Player

- BLG Logistics

- Hyundai Glovis

- Kintetsu World Express

- Mosolf

- Nippon Express

- Schnellecke Logistics

- Toll

- Yusen Logistics

- 신규 기업

- Flexport

- FourKites

- Hodlmayr International

- project44

- Uber Freight

The Global Automotive Logistics Market was valued at USD 286.8 billion in 2025 and is estimated to grow at a CAGR of 7.3% to reach USD 568.6 billion by 2035.

The expanding automotive industry has increased the need for efficient logistics solutions to transport vehicles, parts, and components across the supply chain. Companies are recognizing the importance of software that can optimize transportation routes, manage inventory, and provide real-time shipment tracking. Many automakers still rely on outdated software and legacy systems for logistics management, which makes integration of modern solutions challenging, requiring extensive data migration and customization. Limited real-time visibility into the end-to-end supply chain, complex transportation networks, and varying data transparency among partners pose additional hurdles. To address these challenges, software providers are incorporating AI and machine learning to improve route planning, automate repetitive tasks, and enhance decision-making. Predictive analytics and demand forecasting capabilities allow companies to anticipate future demand, optimize inventory, and allocate resources more efficiently, enabling proactive solutions to supply chain disruptions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $286.8 Billion |

| Forecast Value | $568.6 Billion |

| CAGR | 7.3% |

The inbound logistics segment held a 44% share in 2025 and is projected to grow at a CAGR of 8% between 2026 and 2035. Inbound logistics plays a critical role in the automotive logistics market by efficiently transporting raw materials, components, and subassemblies from suppliers to OEM assembly plants. Its high-frequency, high-volume operations ensure smooth production flows while supporting just-in-time (JIT) and just-in-sequence (JIS) manufacturing, reducing inventory carrying costs. The use of multimodal transportation, including road, rail, air, and sea, further enhances the speed, reliability, and cost-efficiency of inbound supply chains.

The automotive parts and components logistics segment accounted for a 65% share in 2025 and is expected to grow at a CAGR of 7.6% from 2026 to 2035. This segment dominates due to the complexity, volume, and frequency of part movements across OEMs and Tier-1 and Tier-2 supplier networks. It ensures that parts are delivered securely, on time, and cost-effectively to assembly plants, regional distribution centers, and aftermarket service networks, maintaining seamless production and operations.

China Automotive Logistics Market held a 39% share, generating USD 43.2 billion in 2025. China's dominance is driven by rapid growth in vehicle production, strong demand for passenger and commercial vehicles, and large-scale investments in advanced logistics technologies. The region benefits from well-developed transportation networks, extensive warehousing and distribution infrastructure, and rising adoption of digital supply chain solutions, IoT-based tracking, and automated material handling systems.

Key players in the Global Automotive Logistics Market include Bosch Service Solutions GmbH, Basware Oy, Blue Yonder, SAP SE, Kinaxis, Inc., Infor Corporation, Oracle Corporation, Ceres Technology Inc., and Manhattan Associates, Inc. Companies in the Global Automotive Logistics Market are strengthening their position by investing in AI and ML integration to enhance predictive capabilities and operational efficiency. They are prioritizing cloud-based platforms to offer scalable and flexible solutions that meet evolving customer demands. Strategic partnerships with technology providers and industry stakeholders help expand market reach and ensure seamless software integration. Firms are also focusing on continuous R&D to innovate features such as real-time tracking, advanced analytics, and automated workflow management, creating a competitive edge.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service

- 2.2.3 Product

- 2.2.4 Mode of Transportation

- 2.2.5 Distribution

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global vehicle production & aftermarket expansion

- 3.2.1.2 Adoption of digital & intelligent logistics technologies

- 3.2.1.3 Growth of EV manufacturing & battery logistics

- 3.2.1.4 Expansion of globalized supply chains & cross-border trade

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain disruptions & capacity bottlenecks

- 3.2.2.2 High operational costs & complexity of handling EV components

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for sustainable & green logistics

- 3.2.3.2 Rapid growth in aftermarket e-commerce distribution

- 3.2.3.3 Integration of advanced technologies

- 3.2.3.4 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 FMCSA, NHTSA, EPA Emissions Standards

- 3.4.1.2 Transport Canada Safety Regulations

- 3.4.2 Europe

- 3.4.2.1 Germany EU Vehicle Safety Regulations, TUV Certification

- 3.4.2.2 France CNRS Emissions & Safety Standards

- 3.4.2.3 United Kingdom DVSA Vehicle Safety & Compliance

- 3.4.2.4 Italy Ministry of Transport Vehicle Regulations

- 3.4.3 Asia Pacific

- 3.4.3.1 China Ministry of Transport Safety Rules, NEV Policies

- 3.4.3.2 Japan JAMA Vehicle Safety Regulations, Emission Standards

- 3.4.3.3 South Korea MOTIE Safety & Environmental Compliance

- 3.4.3.4 India AIS (Automotive Industry Standards)

- 3.4.4 Latin America

- 3.4.4.1 CONTRAN Vehicle Safety & Emission Rules

- 3.4.4.2 NOM Automotive Safety Standards

- 3.4.5 Middle East and Africa

- 3.4.5.1 Emirates Authority for Standardization & Metrology Vehicle Regulations

- 3.4.5.2 SASO Vehicle Safety & Environmental Standards

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2022 - 2035 ($ Bn, TEU)

- 5.1 Key trends

- 5.2 Inbound Logistics

- 5.3 Outbound

- 5.4 Reverse

- 5.5 Aftermarket

Chapter 6 Market Estimates & Forecast, By Product, 2022 - 2035 ($ Bn, TEU)

- 6.1 Key trends

- 6.2 Finished Vehicle

- 6.2.1 Passenger car

- 6.2.1.1 Hatchback

- 6.2.1.2 Sedan

- 6.2.1.3 SUV

- 6.2.2 Commercial vehicle

- 6.2.2.1 Light duty

- 6.2.2.2 Medium duty

- 6.2.2.3 Heavy duty

- 6.2.1 Passenger car

- 6.3 Automotive Parts & Components

- 6.3.1 Wheels and tires

- 6.3.2 Electrical and electronic

- 6.3.3 Body and chassis

- 6.3.4 Suspension and steering

- 6.3.5 Braking system

- 6.3.6 Engine and powertrain

Chapter 7 Market Estimates & Forecast, By Mode of Transportation, 2022 - 2035 ($ Bn, TEU)

- 7.1 Key trends

- 7.2 Road Freight

- 7.3 Sea Freight

- 7.4 Air Freight

- 7.5 Rail Freight

Chapter 8 Market Estimates & Forecast, By Distribution, 2022 - 2035 ($ Bn, TEU)

- 8.1 Key trends

- 8.2 Domestic

- 8.3 International

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn, TEU)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Belgium

- 9.3.7 Netherlands

- 9.3.8 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 Singapore

- 9.4.6 South Korea

- 9.4.7 Vietnam

- 9.4.8 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Global Player

- 10.1.1 C.H. Robinson Worldwide

- 10.1.2 CEVA Logistics

- 10.1.3 DHL Supply Chain & Global Forwarding

- 10.1.4 DSV-Schenker

- 10.1.5 Expeditors International of Washington

- 10.1.6 GEODIS (SNCF)

- 10.1.7 Hellmann Worldwide Logistics

- 10.1.8 Kuehne+Nagel International

- 10.1.9 Penske Logistics

- 10.1.10 XPO Logistics

- 10.2 Regional Player

- 10.2.1 BLG Logistics

- 10.2.2 Hyundai Glovis

- 10.2.3 Kintetsu World Express

- 10.2.4 Mosolf

- 10.2.5 Nippon Express

- 10.2.6 Schnellecke Logistics

- 10.2.7 Toll

- 10.2.8 Yusen Logistics

- 10.3 Emerging Players

- 10.3.1 Flexport

- 10.3.2 FourKites

- 10.3.3 Hodlmayr International

- 10.3.4 project44

- 10.3.5 Uber Freight