|

시장보고서

상품코드

1740778

태양광 PV 제조 장비 시장 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Solar PV Manufacturing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

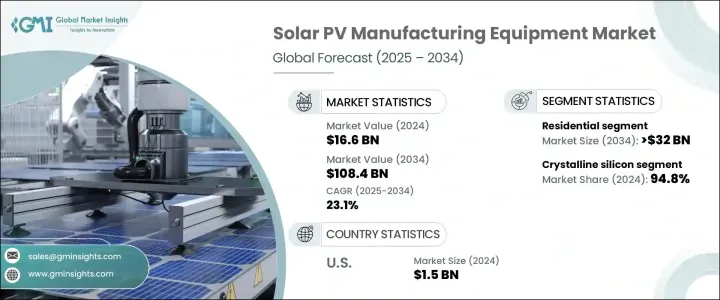

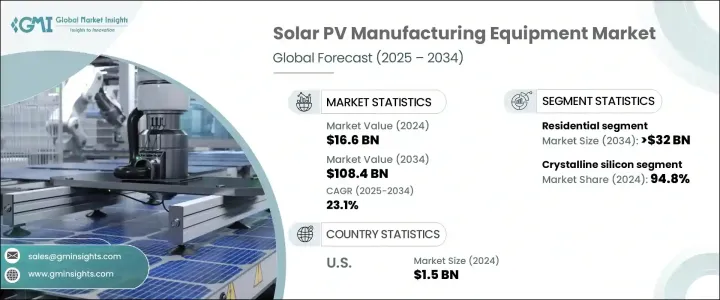

태양광 PV 제조 장비 세계 시장 규모는 2024년에 166억 달러에 달했고, CAGR 23.1%로, 2034년에는 1,084억 달러에 이를 것으로 추정됩니다.

이 시장 확대의 배경에는 에너지 자급에 대한 관심이 높아지고 신뢰성이 높고 탄력있는 태양전지 부품의 국내 생산에 대한 요구가 높아지고 있습니다. 지정학적 불확실성 증가로 인해 각 국은 특히 웨이퍼, 셀, 모듈과 같은 중요한 상류 부품의 제조 운영을 현지화하는 것이 시급해졌습니다.

첨단 셀 기술의 채용이 진행되어 태양광 PV 제조 장비 시장의 정세는 더욱 변화하고 있습니다. 비용 최적화에도 도움이 됩니다. 장비 개발 기업은 자동화, AI 도구 및 머신러닝을 시스템에 통합하는 경향을 강화하고 있으며, 이로 인해 제조 정확성과 확장성이 크게 향상되었습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 166억 달러 |

| 예측 금액 | 1,084억 달러 |

| CAGR | 23.1% |

각 국이 탈탄소화 목표의 달성과 전력소비량 증가에 대한 대처를 강화하는 가운데 태양광발전설비에 대한 수요는 여러 분야에서 증가하고 있습니다. 이러한 이유로 산업 규모의 기계 가공이 그 어느 때보다도 필수적입니다.

무역 정책은 시장 역학을 크게 형성하고 있습니다. 이 전환은 신흥 산업 허브의 개발을 지원하고 전통적인 공급원에 대한 의존도를 줄이는 반면, 단기적인 장비 가격 상승을 유발하고 전환 기간 동안 프로젝트 일정에 영향을 미칠 것으로 예측됩니다.

응용 분야별로 시장은 주거용, 상업용, 유틸리티의 각 부문으로 분류됩니다. 주택 시스템의 스마트 기능과 축전지의 통합과 같은 기술의 진보가 주택용 태양광 발전의 설치를 보다 매력적인 것으로 하고 있습니다.

기술면에서 태양광 PV 제조 장비 시장 세분화는 박막 실리콘과 결정 실리콘으로 구분됩니다. 수수료의 가용성, 지속적인 기술 강화로 인해 다양한 응용 분야에서 단결정 실리콘은 제한된 공간에서 더 큰 출력을 제공할 수 있기 때문에 여전히 선호되는 선택이며 주택 옥상 및 고밀도 상업시설 및 공공시설 모두에 이상적입니다.

지역별로는 북미 시장의 성장이 현저하며 2024년 세계 시장 점유율의 9.6% 이상을 차지하고 있습니다. 지원 정책 조치는 이러한 성장을 촉진하는 데 중요한 역할을 하고 있습니다. 세액 공제나 생산 장려금 등, 국내 생산을 강화하는 것을 목적으로 한 종합적인 법 제도는 자본 코스트를 삭감해, 태양전지 공급 체인 전체에 새로운 투자를 유치하고 있습니다.

세계 공급망의 취약성이 지속적으로 표면화되는 가운데 국내 제조 에코시스템이 우선하여 수직 통합형 사업에 대한 투자가 급증하고 있습니다. 기업이 늘어나고 있으며, 지역 기업과의 전략적 파트너십도 빈번히 이루어지고, 지역의 전문지식에 대한 액세스를 제공하고, 시장에의 신속한 침투를 촉진하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 에코시스템

- 트럼프 정권의 관세 분석

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율

- 전략적 대시보드

- 기업 벤치마킹

- 혁신과 기술의 상황

제5장 시장 규모와 예측 : 제조장치별, 2021-2034년

- 주요 동향

- 실리콘 장치

- 잉곳 장치

- 웨이퍼 장치

- 셀 장치

- 모듈 장치

제6장 시장 규모와 예측 : 기술별, 2021-2034년

- 주요 동향

- 결정 실리콘

- 박막

제7장 시장 규모와 예측 : 용도별, 2021-2034년

- 주요 동향

- 주택

- 상업

- 유틸리티

제8장 시장 규모와 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 남아프리카

- 라틴아메리카

- 브라질

- 아르헨티나

- 칠레

- 멕시코

제9장 기업 프로파일

- Adani Solar

- Emmvee

- First Solar

- Goldi Solar

- Grew Solar

- JA Solar

- LDK Solar

- Premier Energies

- RenewSys

- Servotech Renewable Power System

- Tata Power Solar

- Tongwei Solar

- Trina Solar

- Vikram Solar

- Waaree Energies

The Global Solar PV Manufacturing Equipment Market was valued at USD 16.6 billion in 2024 and is estimated to grow at a CAGR of 23.1% to reach USD 108.4 billion by 2034. This expansion is driven by the increasing focus on energy independence and the growing need for reliable and resilient domestic production of solar components. Rising geopolitical uncertainties have intensified the urgency for countries to localize manufacturing operations, especially for critical upstream components such as wafers, cells, and modules. This shift toward domestic production is enhancing industrial activity and encouraging major investments in solar PV infrastructure and equipment.

Growing adoption of advanced cell technologies is further reshaping the landscape of the solar PV manufacturing equipment market. Manufacturers are heavily investing in state-of-the-art production lines capable of handling innovations in high-efficiency cell types and module designs. These enhancements not only improve energy yields but also help optimize production costs. Equipment developers are increasingly integrating automation, AI tools, and machine learning into their systems, which is significantly improving manufacturing precision and scalability. This trend is lowering entry barriers for new players and providing opportunities for existing companies to expand operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.6 Billion |

| Forecast Value | $108.4 Billion |

| CAGR | 23.1% |

As countries ramp up efforts to meet decarbonization goals and tackle rising electricity consumption, demand for solar equipment is intensifying across multiple sectors. Industrial-scale machinery fabrication is becoming more vital than ever to meet the rising need for solar deployment across residential, commercial, and utility applications. The upstream segment, which includes the production of polysilicon, ingots, wafers, solar cells, and finished modules, continues to experience substantial demand, fueling the expansion of the equipment market.

Trade policies are also shaping the market dynamics significantly. Trade restrictions on foreign solar PV products are prompting global manufacturers to diversify their supply chains and relocate production capacities to alternative manufacturing-friendly regions. While this shift supports the development of emerging industrial hubs and reduces dependency on traditional supply sources, it is expected to cause a short-term increase in equipment prices and affect project timelines during the transition.

By application, the market is categorized into residential, commercial, and utility segments. The residential segment is expected to surpass USD 32 billion by 2034, bolstered by rising energy costs, increased homeowner awareness of sustainability, and favorable regulatory incentives. Technological advancements, such as the integration of smart features and battery storage in home systems, are making residential solar installations more appealing. Consumers are also seeking greater energy autonomy, and their growing interest in backup solutions during grid outages is contributing to the sector's momentum.

In terms of technology, the solar PV manufacturing equipment market is segmented into thin film and crystalline silicon categories. Crystalline silicon technology currently dominates the market with a 94.8% share as of 2024. Its dominance is attributed to its higher energy conversion rates, abundant material availability, and ongoing technological enhancements. Among the various applications, monocrystalline silicon remains the preferred choice due to its ability to deliver greater output in limited space, making it ideal for both residential rooftops and high-density commercial or utility installations.

Regionally, the market is witnessing notable growth in North America, which accounted for over 9.6% of the global market share in 2024-a figure expected to increase by 2034. The United States alone recorded a market value of USD 1 billion in 2022, rising to USD 1.2 billion in 2023 and USD 1.5 billion in 2024. Supportive policy measures are playing a crucial role in driving this growth. Comprehensive legislative packages aimed at bolstering domestic manufacturing, including tax credits and production incentives, are reducing capital costs and attracting new investments across the solar supply chain.

As global supply chain vulnerabilities continue to surface, domestic manufacturing ecosystems are being prioritized, leading to a surge in investment in vertically integrated operations. Companies are increasingly bringing in-house the entire production process-from raw materials to final product assembly-to ensure better control over costs, quality, and lead times. Strategic partnerships with regional firms are also becoming more frequent, providing access to local expertise and facilitating faster market penetration. These collaborations are fostering technology transfer and speeding up the commercialization of next-generation solar technologies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Strategic dashboard

- 4.4 Company benchmarking

- 4.5 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Manufacturing Equipment, 2021 – 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Silicon equipment

- 5.3 Ingots equipment

- 5.4 Wafer equipment

- 5.5 Cells equipment

- 5.6 Module equipment

Chapter 6 Market Size and Forecast, By Technology, 2021 – 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Crystalline silicon

- 6.3 Thin film

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.4 Utility

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

- 8.6.4 Mexico

Chapter 9 Company Profiles

- 9.1 Adani Solar

- 9.2 Emmvee

- 9.3 First Solar

- 9.4 Goldi Solar

- 9.5 Grew Solar

- 9.6 JA Solar

- 9.7 LDK Solar

- 9.8 Premier Energies

- 9.9 RenewSys

- 9.10 Servotech Renewable Power System

- 9.11 Tata Power Solar

- 9.12 Tongwei Solar

- 9.13 Trina Solar

- 9.14 Vikram Solar

- 9.15 Waaree Energies