|

시장보고서

상품코드

1740891

EV 배터리 팩 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)EV Battery Pack Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

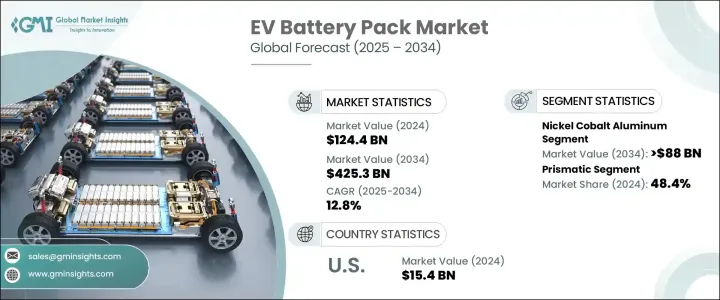

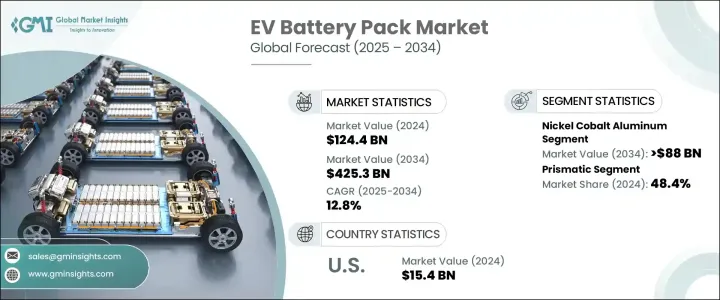

세계의 EV 배터리 팩 시장은 2024년에는 1,244억 달러로 평가되었고 전동 이동성으로의 전환 가속화, 환경 규제 증가, 강력한 정책 지원에 힘입어 CAGR 12.8%를 나타내 2034년에는 4,253억 달러에 이를 것으로 추정됩니다.

각국이 배기가스 규제를 강화하고 지속 가능한 수송을 추진하는 중 고성능 전기자동차 수요가 급증하고 있습니다. EV 보급을 더욱 뒷받침하고 있습니다. 자동차 제조업체는 EV 포트폴리오를 급속히 확대하여 소비자의 기대에 부응하여 효율적이고 신뢰성 있는 배터리 시스템의 필요성이 높아지고 있습니다.

리튬이온, 니켈·코발트·알루미늄(NCA), 솔리드 스테이트 기술 등의 전지 화학의 진보에 의해 에너지 밀도가 향상하고, 충전 시간이 단축되어, 전지 전체의 수명이 연장되고 있습니다. 둘 다 EV의 대량 도입에 자신감을 보이고 역동적이고 경쟁적인 상황이 형성되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 1,244억 달러 |

| 예측 금액 | 4,253억 달러 |

| CAGR | 12.8% |

전동 이동성으로의 전환이 기세를 늘리는 가운데, 자동차 제조업체는 생산 능력을 확대하고, 보다 작고 고효율의 배터리 팩을 통합하기 위해 차량 아키텍처를 재설계하고 있습니다. 자동차 제조업체는 안정적인 공급을 보장하고 화학 및 설계 혁신을 활용하기 위해 배터리 제조업체와 전략적 제휴를 맺고 있습니다.

니켈 코발트 알루미늄(NCA) 배터리 화학은 강력한 견인력이 되고 있으며 EV 배터리 팩 시장은 2034년까지 880억 달러에 달할 것으로 예상되고 있습니다. NCA 배터리는 자동차 제조업체가 효율을 유지하면서 EV 성능을 높이는 데 도움이 됩니다. 급속 충전 능력과 뛰어난 열 안정성으로 인해 증가하는 급속 충전소 네트워크의 지원에 최적이며, 결국 소비자의 항속 거리 불안을 완화하고 EV 보급률 전체를 강화합니다.

프리즘형 전지 셀은 2024년에 48.4%의 압도적인 점유율을 차지했고, 자동차 제조업체에 설계의 유연성을 제공해, 축전 용량을 극대화하면서, 보다 스마트하고 안전한 전지 팩을 만들 수 있습니다. 상처나 팽창에 대한 보호가 강화되어 전지 수명의 연장에 공헌합니다. 대형 EV 제조업체는 안전성과 항속 거리를 우선한 차량 설계의 진화에 따라 급증하는 수요에 대응하기 위해, 각형 셀 제조업체와 장기 공급 계약을 맺거나 합작회사를 설립하기도 합니다.

미국의 EV 배터리 팩 시장은 2024년까지 154억 달러를 기록했고 13.1%의 점유율을 차지했습니다. 뿐만 아니라 국내 생산과 투자를 계속해서 추진하고 있습니다.

세계의 EV 배터리 팩 시장에서 기업이 채용하고 있는 주요 전략으로는 지역 확대, 장기적인 공급 체인 파트너십, 차세대 배터리 기술에 대한 다액의 투자 등이 있습니다. 자동차 제조 업체 및 원료 공급업체와 협력 관계 구축, 중요 광물 확보는 각 브랜드가 전기자동차 세계 수요 급증에 대응하는 탄력적인 생태계를 구축하는 데 도움이 됩니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 에코시스템

- 트럼프 정권의 관세 분석

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 전략적 대시보드

- 혁신 및 지속가능성 전망

제5장 시장 규모와 예측 : 배터리 형태별(2021-2034년)

- 주요 동향

- 원통형

- 파우치

- 프리즘

제6장 시장 규모와 예측 : 배터리 화학별(2021-2034년)

- 주요 동향

- 리튬 인산철 인산염

- 니켈 코발트 알루미늄

- 니켈 망간 코발트

- 산화 리튬 망간 산화물

- 기타

제7장 시장 규모와 예측 : 추진 유형별(2021-2034년)

- 주요 동향

- BEV

- PHEV

제8장 시장 규모와 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 프랑스

- 스페인

- 영국

- 이탈리아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 라틴아메리카

- 브라질

- 아르헨티나

제9장 기업 프로파일

- FRIWO

- LG Energy Solution

- Octillion Power Systems

- Panasonic

- PMBL Limited

- Rivian

- Rapport

- Samsung

- TOSHIBA

- VARTA

The Global EV Battery Pack Market was valued at USD 124.4 billion in 2024 and is estimated to grow at a CAGR of 12.8% to reach USD 425.3 billion by 2034, fueled by the accelerating shift toward electric mobility, rising environmental regulations, and robust policy support. As countries tighten emission norms and push for sustainable transportation, the demand for high-performance electric vehicles is skyrocketing. Government initiatives such as subsidies, tax credits, and incentives for manufacturers and end-users are further propelling EV adoption worldwide. Automakers are rapidly expanding their EV portfolios to meet growing consumer expectations, increasing the need for efficient and reliable battery systems.

Advances in battery chemistries like lithium-ion, nickel cobalt aluminum (NCA), and solid-state technologies are improving energy density, reducing charging times, and extending the overall lifespan of batteries. As energy storage technology evolves, both consumers and automakers are showing greater confidence in mass EV integration, creating a dynamic and competitive market landscape. Increasing investments in battery R&D, establishment of regional gigafactories, and strategic partnerships across the supply chain are laying the foundation for sustained industry growth over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $124.4 Billion |

| Forecast Value | $425.3 Billion |

| CAGR | 12.8% |

As the shift toward electric mobility gains momentum, automakers are scaling up production capabilities and redesigning vehicle architectures to integrate more compact, high-efficiency battery packs. This surge in EV manufacturing is intensifying demand for advanced battery technologies that balance power, longevity, and energy density within a smaller, lighter footprint. Automakers are forming strategic alliances with battery producers to ensure consistent supply and leverage innovations in chemistry and design. Manufacturers are also prioritizing lightweight materials and modular battery systems to enhance overall performance and maximize driving range without compromising safety.

Nickel cobalt aluminum (NCA) battery chemistry continues to gain strong traction, with the EV Backup Market expected to reach USD 88 billion by 2034. Known for high energy density, lightweight properties, and long cycle life, NCA batteries are helping automakers enhance EV performance while maintaining efficiency. Their fast-charging capability and superior thermal stability make them ideal for supporting the growing network of rapid charging stations, ultimately easing range anxiety for consumers and strengthening overall EV adoption rates.

Prismatic battery cells held a commanding 48.4% share in 2024, offering automakers design flexibility to create sleeker, safer battery packs while maximizing storage capacity. The rigid casing of prismatic cells provides enhanced protection against physical damage and swelling, contributing to extended battery life. Leading EV manufacturers are securing long-term supply agreements and forming joint ventures with prismatic cell producers to meet surging demand as vehicle designs evolve to prioritize safety and range.

The U.S. EV Battery Pack Market generated USD 15.4 billion by 2024, claiming a 13.1% share. Federal legislation like the Inflation Reduction Act of 2022, along with growing awareness of clean energy solutions, continues to boost domestic manufacturing and investment. Established automakers expanding their EV portfolios are further fueling the need for advanced, high-efficiency battery systems across the region.

Key strategies adopted by companies in the Global EV Battery Pack Market include regional expansion, long-term supply chain partnerships, and significant investment in next-generation battery technologies. Prioritizing R&D to enhance energy density and safety, building collaborations with automakers and raw material suppliers, and securing critical minerals are helping brands create resilient ecosystems that meet the surging global demand for electric vehicles.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Battery Form, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Cylindrical

- 5.3 Pouch

- 5.4 Prismatic

Chapter 6 Market Size and Forecast, By Battery Chemistry, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Lithium iron phosphate

- 6.3 Nickel cobalt aluminum

- 6.4 Nickel manganese cobalt

- 6.5 Lithium manganese oxide

- 6.6 Others

Chapter 7 Market Size and Forecast, By Propulsion Type, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 BEV

- 7.3 PHEV

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 Spain

- 8.3.4 UK

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 FRIWO

- 9.2 LG Energy Solution

- 9.3 Octillion Power Systems

- 9.4 Panasonic

- 9.5 PMBL Limited

- 9.6 Rivian

- 9.7 Rapport

- 9.8 Samsung

- 9.9 TOSHIBA

- 9.10 VARTA