|

시장보고서

상품코드

1687054

EV 배터리 팩 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)EV Battery Pack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

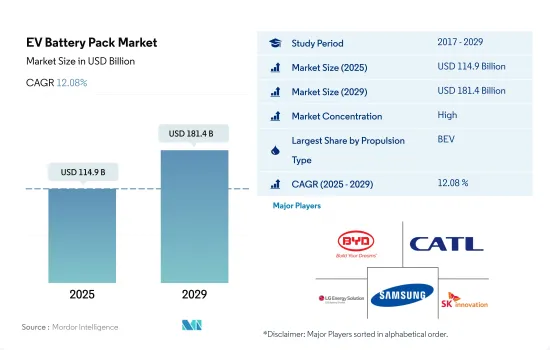

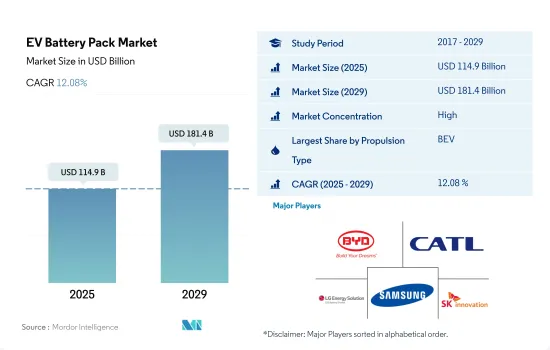

EV 배터리 팩 시장 규모는 2025년에 1,149억 달러로 추정되고, 2029년에는 1,814억 달러에 이를 것으로 예측되며, 예측기간 2025년부터 2029년까지 CAGR 12.08%로 성장할 전망입니다.

중국이 BEV 배터리 수요를 선도, PHEV는 유럽과 북미에서 급증

- 세계 각국의 자동차 전동화는 지난 수년간 크게 성장하여 전기자동차의 주요 부품 중 하나인 배터리 수요에 긍정적인 영향을 미쳤습니다. 전기자동차의 보급은 전기자동차에 대한 인식, EV 보급에 대한 정부의 엄격한 기준, 옛 화석 연료 차량에 대한 EV의 우위, 각국의 제로 방출 계획 등 다양한 요인에 따라 확대되고 있습니다. 그 결과 배터리 산업은 병행하여 성장해 2021년에는 전 세계적으로 2017년 대비 205%의 매출 성장을 보였습니다.

- PHEV 및 BEV 배터리의 주요 수요는 아시아 국가이며, 중국은 전기자동차 산업의 가장 큰 기업 중 하나입니다. BEV 수요는 PHEV에 비해 시장 대부분에서 높고, 예를 들어 90%는 중국이 획득하고 있습니다. 유럽과 북미 등 다양한 지역에서도 BEV 및 PHEV 수요가 크게 늘어나고 있으며, 세계 배터리 수요의 성장에도 기여하고 있습니다. 그 결과 배터리 전기자동차에서 리튬 이온 배터리의 사용은 2022년에는 전 세계적으로 2021년 대비 89% 증가했습니다.

- 신제품 출시는 소비자의 EV에 대한 투자를 유치하고 있습니다. 예를 들어 중국의 자동차 제조업체 BYD는 2022년 11월 인도에서 60.48kWh의 배터리를 탑재해 항속거리 521km의 전기자동차 SUV 'Atto 3'을 출시했습니다. 이 차량은 이미 2,000대 이상의 예약을 획득했으며, 2023년 1월에 납차가 시작되었습니다. 이러한 발매가 고객을 유치하고 있어 예측기간 중 세계 각국에서 PHEV 및 BEV 모델을 탑재한 배터리 수요가 더욱 높아질 것으로 예상됩니다.

EV에 대한 정부의 뒷받침과 배터리 생산 인프라 개발이 세계의 EV 배터리 팩 시장을 견인

- 자동차의 전동화는 최근 몇 년간 여러 나라에서 크게 성장하고 있으며 배터리 산업의 성장에도 영향을 미쳤습니다. 세계 각국 정부에 의한 전기자동차에 대한 엄격한 기준 도입, 기존 연료 자동차에 대한 EV의 다양한 이점, 보조금, 리베이트를 포함한 세제 우대 등 다양한 요인이 EV의 경이적인 성장을 돕고 역사적인 기간에 약 219.05% 증가하여 OEM 및 애프터마켓 공급업체의 배터리 수요에 긍정적인 영향을 주었습니다. EV의 보급률 상승은 과거 기간(2017-2021년)에 배터리 수요를 세계에서 217.99% 증가시켰습니다.

- 전기자동차는 배터리 팩 전체의 판매에 크게 기여하고 있으며, 그 다음 소형 트럭과 버스가 계속됩니다. 중국, 미국, 독일 등 다양한 국가에서 2022년 EV 수요의 성장은 주로 APAC 국가가 견인하여 배터리 수요를 약 86.00% 증가시켰습니다. 그 결과, EV 배터리 팩의 세계 수요는 2022년에 전년 대비 87.78%의 성장을 기록했습니다. 인도와 태국 등 다양한 신흥 시장이 EV 판매 증가를 기록할 것으로 예상되며, 앞으로 배터리 팩 수요를 더욱 밀어올릴 것으로 보입니다.

- 세계 각국의 정부는 배터리 제조업체의 국내 생산 강화를 지원합니다. 2023년 5월 캐나다 정부는 제조세 공제 99억 달러와 국내 전지 제조 공장 건설에 5억 3,200만 달러를 제공할 것이라고 발표했습니다. 이러한 각국의 개발은 예측기간 동안 전 세계적으로 배터리 수요가 높아질 것으로 예상됩니다.

EV 배터리 팩 시장 동향

BYD와 테슬라가 EV 시장을 선도하고 미래를 형성

- 2022년 BYD는 전기차 판매로 시장을 선도해 13.3%의 점유율을 차지했습니다. BYD의 주도적 지위에는 몇 가지 요인이 있습니다. BYD는 전기자동차와 관련 기술의 생산에 중점을 두고 EV 업계에서 일찍부터 유력한 기업로 활약해 왔습니다. BYD는 일찍부터 시장에 진출했기 때문에 확고한 기반을 구축하고 소비자들 사이에서 인정받게 되었습니다. BYD는 또한 적극적으로 세계로 사업을 확장하고, 파트너십을 맺고, 연구개발에 투자하고 있으며, 이들 모두가 주도적 지위에 기여하고 있습니다.

- 테슬라는 전기자동차 기술 혁신의 최전선에 서서 EV 세계 보급에 중요한 역할을 해왔습니다. 테슬라는 2022년 EV 업계에서 12.2% 시장 점유율을 가진 중요한 기업이었습니다. 테슬라의 강력한 브랜드 이미지, 최첨단 기술, 광범위한 슈퍼 충전 네트워크가 성공에 기여합니다.

- EV 시장의 다른 주요 기업 중에서도 큰 시장 점유율을 가진 기업이 있습니다. BMW는 서브 브랜드 'BMW i'에 의한 전동 모빌리티에 대한 헌신과 함께 자동차 업계에서 정평을 확립하고 시장에서의 존재감을 높이고 있습니다. 마찬가지로 2022년에 3.9% 시장 점유율을 차지한 폭스바겐은 폭스바겐 그룹 산하의 전동 모빌리티에 적극적으로 투자하고 있습니다. 이들 기업은 메르세데스 벤츠, 기아차, 현대자동차 등 다른 기업과 함께 기존 브랜드 인지도를 활용하고, 매력적인 전기차 모델을 투입하고, 전기차의 항속거리와 성능을 향상시키는 기술에 투자함으로써 EV 업계를 재식민지화하고 있습니다.

테슬라와 BYD가 2022년 베스트셀러 EV 모델을 독점

- 2022년에 가장 많이 팔린 EV 모델은 두 가지 주요 OEM이 독점했습니다. : 테슬라와 BYD였습니다. 테슬라는 모델 Y와 모델 3의 두 모델로 각각 1위와 3위를 차지하며 시장에서 확고한 지위를 쌓았습니다. 테슬라의 모델 Y는 가장 인기 있는 플러그인 전기자동차로 2022년 세계 판매량은 약 77만 1,300대였습니다. 같은 해 테슬라의 모델 3과 모델 Y의 판매 대수는 120만 대를 돌파했고, 테슬라의 베스트셀러 모델은 전년 대비 36.77% 증가했습니다. 플러그인 전기자동차(PEV)의 베스트셀러 5개 모델 중 2개 모델은 테슬라 브랜드였지만, 배터리 전기자동차 제조업체는 2022년 아시아 브랜드와의 경쟁에 직면했습니다. 중국을 거점으로 하는 BYD는 플러그인 하이브리드 전기자동차 모델의 풍부한 라인업을 무기로 2022년 테슬라를 제치고 PEV의 베스트셀러 브랜드가 되었습니다. 테슬라 모델 Y에 약간의 차이가 계속된 것은 BYD Song Plus(BEV+PHEV)로 판매 대수는 47만 7,090대에 달하여, 2위 자리를 확보했습니다. BYD는 중국 시장에서 확고한 지위를 확립하고 있으며, 신뢰성이 높고 기술적으로 선진적인 전기차를 생산하고 있다는 평판이 Song Plus 모델의 호조로운 판매 실적에 기여한 것으로 보입니다.

- 폴크스바겐 ID.4는 유럽의 PEV(플러그인 전기자동차) 중에서 유일하게 톱 10에 들어가 베스트셀러 EV 모델 중에서 두드러졌습니다. 2022년 판매량은 17만 4,090대로, ID.4는 폭스바겐의 전동 모빌리티에 대한 헌신과 EV 시장에서 존재감의 고조를 실증했습니다.

- 전반적으로 Tesla와 BYD의 이러한 상위 EV 모델과 Wuling Hong Guang MINI EV 및 Volkswagen ID.4와 같은 다른 주목할 만한 경쟁 모델은 전기자동차에 대한 소비자 수요가 증가하고 있음을 보여줍니다.

EV 배터리 팩 산업 개요

EV 배터리 팩 시장은 상당히 통합되어 있으며 상위 5개사에서 125.96%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. BYD Company Ltd., Contemporary Amperex Technology(CATL), LG Energy Solution Ltd., Samsung SDI and SK Innovation(sorted alphabetically).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

- 조사 전제조건 및 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 전기자동차 판매 대수

- OEM별 전기자동차 판매 대수

- 판매 LINE EV 모델

- 선호되는 배터리 케미스트리를 가진 OEM

- 배터리 팩 가격

- 배터리 재료 비용

- 각 배터리 케미스트리 가격표

- 누가 누구에게 공급하는가

- EV 배터리 용량 및 효율

- EV 발매 모델수

- 규제 프레임워크

- 벨기에

- 브라질

- 캐나다

- 중국

- 콜롬비아

- 프랑스

- 독일

- 헝가리

- 인도

- 인도네시아

- 일본

- 멕시코

- 폴란드

- 태국

- 영국

- 미국

- 밸류체인 및 유통채널 분석

제5장 시장 세분화

- 바디 유형별

- 버스

- LCV

- M&HDT

- 승용차

- 추진 유형별

- BEV

- PHEV

- 배터리 케미스트리별

- LFP

- NCA

- NCM

- NMC

- 기타

- 용량별

- 15kWh-40kWh

- 40kWh-80kWh

- 80kWh 이상

- 15kWh 미만

- 배터리 형상별

- 원통형

- 파우치

- 각형

- 방식별

- 레이저

- 와이어

- 컴포넌트별

- 애노드

- 음극

- 전해액

- 세퍼레이터

- 재료 유형별

- 코발트

- 리튬

- 망간

- 천연 흑연

- 니켈

- 기타 재료

- 지역별

- 아시아태평양

- 국가별

- 중국

- 인도

- 일본

- 한국

- 태국

- 기타 아시아태평양

- 유럽

- 국가별

- 프랑스

- 독일

- 헝가리

- 이탈리아

- 폴란드

- 스웨덴

- 영국

- 기타 유럽

- 중동 및 아프리카

- 북미

- 국가별

- 캐나다

- 미국

- 남미

- 아시아태평양

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- BYD Company Ltd.

- China Aviation Battery Co. Ltd.(CALB)

- Contemporary Amperex Technology Co. Ltd.(CATL)

- ENVISION AESC UK Ltd.

- EVE Energy Co. Ltd.

- Farasis Energy(Ganzhou) Co. Ltd.

- Guoxuan High-tech Co. Ltd.

- LG Energy Solution Ltd.

- Panasonic Holdings Corporation

- Primearth EV Energy Co. Ltd.

- Samsung SDI Co. Ltd.

- SK Innovation Co. Ltd.

- SVOLT Energy Technology Co. Ltd.(SVOLT)

- TOSHIBA Corp.

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The EV Battery Pack Market size is estimated at 114.9 billion USD in 2025, and is expected to reach 181.4 billion USD by 2029, growing at a CAGR of 12.08% during the forecast period (2025-2029).

China leads battery demand for BEVs, PHEVs surge in Europe and North America

- The electrification of vehicles in various countries globally has grown significantly over the past few years, making a positive impact on the demand for batteries as it is one of the major components of electric vehicles. The adoption of electric vehicles is growing due to various factors, including awareness of electric vehicles, strict norms from the government for EV adoption, advantages of EVs over the old fossil fuel vehicles, and zero-emission programs in various countries. As a result, the battery industry has grown parallelly and witnessed sales growth of 205% in 2021 over 2017 globally.

- The major demand for batteries for PHEVs and BEVs is from Asian countries, with China as one of the biggest players in the electric automotive industry. The demand for BEVs is higher compared to the PHEVs in the majority of the market; for instance, 90% is acquired by China. Various regions, such as Europe and North America, are also witnessing a significant growth in the demand for BEV and PHEV, which has also contributed to the growth of the demand for batteries across the globe. As a result, the use of lithium-ion batteries in battery electric vehicles grew by 89% in 2022 over 2021 globally.

- Launching of new products is attracting consumers to invest in EVs. For instance, in November 2022, the Chinese automaker BYD launched its electric SUV Atto 3 in India, which is equipped with a 60.48 kWh battery and offers a range of 521 km. The car has already got more than 2,000 bookings, and deliveries started in January 2023. Such launches are attracting customers, which is further expected to raise the demand for batteries with PHEV and BEV models during the forecast period in various countries globally.

Governmental push for EVs and development in battery production infrastructure are driving the global EV battery pack market

- The electrification of vehicles has been growing significantly across various countries over the past few years and also impacting the growth of the battery industry. Various factors, such as the introduction of stringent norms by governments worldwide for electric vehicles, the various advantages of EVs over conventional fuel vehicles, subsidies, and tax benefits, including rebates, aided the tremendous growth of EVs by around 219.05% in the historical period, thus, positively impacting the battery demand from OEMs and aftermarket suppliers. The rise in EV adoption rates increased the battery demand by 217.99% in the historical period (2017-2021) worldwide.

- Electric cars are among the major contributors to the overall battery pack sales, followed by light trucks and buses. Growth in the demand for EVs in 2022 in various countries such as China, the United States, and Germany increased the demand for batteries by around 86.00% in 2022, majorly driven by APAC countries. As a result, global demand for EV battery packs witnessed a growth of 87.78% in 2022 over the previous year. Various emerging markets, such as India and Thailand, are expected to register increased sales of EVs, which would further boost their demand for battery packs in the future.

- The governments of various countries worldwide are supporting battery manufacturers in enhancing their production of batteries domestically. In May 2023, the Government of Canada announced that it would provide USD 9.90 billion in manufacturing tax credits and USD 532 million to construct a battery manufacturing plant in the country. Such developments in various countries are expected to enhance the demand for batteries during the forecast period globally.

EV Battery Pack Market Trends

BYD AND TESLA ARE LEADING THE CHARGE IN THE EV MARKET AND SHAPING THE FUTURE

- In 2022, BYD was the market leader in electric vehicle sales and held a share of 13.3%. BYD's leading position can be attributed to several factors. It has been an early and prominent player in the EV industry, with a strong focus on producing electric vehicles and related technologies. The company's early entry into the market allowed it to establish a solid foundation and gain recognition among consumers. BYD has also been actively expanding its operations globally, forging partnerships, and investing in research and development, all of which contribute to its leading position.

- Tesla has been at the forefront of electric vehicle innovation and has played a crucial role in popularizing EVs worldwide. Tesla was a significant player in the EV industry in 2022, with a market share of 12.2%. Tesla's strong brand image, cutting-edge technology, and extensive Supercharger network have contributed to its success.

- Among the other players in the EV market, there are several notable companies that hold significant market shares. BMW's established reputation in the automotive industry, coupled with its commitment to electric mobility through its "BMW i" sub-brand, has contributed to its market presence. Similarly, Volkswagen, which held a market share of 3.9% in 2022, has been actively investing in electric mobility under its "Volkswagen Group" umbrella. These companies, along with others like Mercedes-Benz, Kia, and Hyundai, are recolonizing the EV industry by leveraging their existing brand recognition, introducing compelling electric vehicle models, and investing in technology to enhance the range and performance of their electric offerings.

TESLA AND BYD DOMINATED THE BEST-SELLING EV MODELS OF 2022

- The best-selling EV models in 2022 were dominated by two key OEMs: Tesla and BYD. Tesla held a strong market position with two of its models, the Model Y and Model 3, capturing the first and third spots, respectively. The Tesla Model Y was the most popular plug-in electric vehicle, with global unit sales of roughly 771,300 in 2022. That year, deliveries of Tesla's Model 3 and Model Y surpassed 1.2 million, a Y-o-Y increase of 36.77% for Tesla's best-selling models. While two of the five best-selling plug-in electric vehicle (PEV) models were Tesla-branded, the battery electric vehicle manufacturer faced competition from Asian brands in 2022. China-based BYD overtook Tesla as the best-selling PEV brand in 2022, relying on a large offering of plug-in hybrid electric models. Following closely behind the Tesla Model Y, the BYD Song Plus (BEV + PHEV) secured the second spot, with sales reaching 477,090 units. BYD's established presence in the Chinese market, along with its reputation for producing reliable and technologically advanced electric vehicles, likely contributed to the strong sales performance of the Song Plus models.

- The Volkswagen ID.4 stood out among the best-selling EV models as the only European PEV (Plug-in Electric Vehicle) in the top ten. With a sales volume of 174,090 units in 2022, the ID.4 demonstrated Volkswagen's commitment to electric mobility and its growing presence in the EV market.

- Overall, these top-performing EV models from Tesla and BYD, along with other notable contenders like the Wuling Hong Guang MINI EV and Volkswagen ID.4, demonstrate the increasing consumer demand for electric vehicles.

EV Battery Pack Industry Overview

The EV Battery Pack Market is fairly consolidated, with the top five companies occupying 125.96%. The major players in this market are BYD Company Ltd., Contemporary Amperex Technology Co. Ltd. (CATL), LG Energy Solution Ltd., Samsung SDI Co. Ltd. and SK Innovation Co. Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Electric Vehicle Sales

- 4.2 Electric Vehicle Sales By OEMs

- 4.3 Best-selling EV Models

- 4.4 OEMs With Preferable Battery Chemistry

- 4.5 Battery Pack Price

- 4.6 Battery Material Cost

- 4.7 Price Chart Of Different Battery Chemistry

- 4.8 Who Supply Whom

- 4.9 EV Battery Capacity And Efficiency

- 4.10 Number Of EV Models Launched

- 4.11 Regulatory Framework

- 4.11.1 Belgium

- 4.11.2 Brazil

- 4.11.3 Canada

- 4.11.4 China

- 4.11.5 Colombia

- 4.11.6 France

- 4.11.7 Germany

- 4.11.8 Hungary

- 4.11.9 India

- 4.11.10 Indonesia

- 4.11.11 Japan

- 4.11.12 Mexico

- 4.11.13 Poland

- 4.11.14 Thailand

- 4.11.15 UK

- 4.11.16 US

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Body Type

- 5.1.1 Bus

- 5.1.2 LCV

- 5.1.3 M&HDT

- 5.1.4 Passenger Car

- 5.2 Propulsion Type

- 5.2.1 BEV

- 5.2.2 PHEV

- 5.3 Battery Chemistry

- 5.3.1 LFP

- 5.3.2 NCA

- 5.3.3 NCM

- 5.3.4 NMC

- 5.3.5 Others

- 5.4 Capacity

- 5.4.1 15 kWh to 40 kWh

- 5.4.2 40 kWh to 80 kWh

- 5.4.3 Above 80 kWh

- 5.4.4 Less than 15 kWh

- 5.5 Battery Form

- 5.5.1 Cylindrical

- 5.5.2 Pouch

- 5.5.3 Prismatic

- 5.6 Method

- 5.6.1 Laser

- 5.6.2 Wire

- 5.7 Component

- 5.7.1 Anode

- 5.7.2 Cathode

- 5.7.3 Electrolyte

- 5.7.4 Separator

- 5.8 Material Type

- 5.8.1 Cobalt

- 5.8.2 Lithium

- 5.8.3 Manganese

- 5.8.4 Natural Graphite

- 5.8.5 Nickel

- 5.8.6 Other Materials

- 5.9 Region

- 5.9.1 Asia-Pacific

- 5.9.1.1 By Country

- 5.9.1.1.1 China

- 5.9.1.1.2 India

- 5.9.1.1.3 Japan

- 5.9.1.1.4 South Korea

- 5.9.1.1.5 Thailand

- 5.9.1.1.6 Rest-of-Asia-Pacific

- 5.9.2 Europe

- 5.9.2.1 By Country

- 5.9.2.1.1 France

- 5.9.2.1.2 Germany

- 5.9.2.1.3 Hungary

- 5.9.2.1.4 Italy

- 5.9.2.1.5 Poland

- 5.9.2.1.6 Sweden

- 5.9.2.1.7 UK

- 5.9.2.1.8 Rest-of-Europe

- 5.9.3 Middle East & Africa

- 5.9.4 North America

- 5.9.4.1 By Country

- 5.9.4.1.1 Canada

- 5.9.4.1.2 US

- 5.9.5 South America

- 5.9.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 BYD Company Ltd.

- 6.4.2 China Aviation Battery Co. Ltd. (CALB)

- 6.4.3 Contemporary Amperex Technology Co. Ltd. (CATL)

- 6.4.4 ENVISION AESC UK Ltd.

- 6.4.5 EVE Energy Co. Ltd.

- 6.4.6 Farasis Energy (Ganzhou) Co. Ltd.

- 6.4.7 Guoxuan High-tech Co. Ltd.

- 6.4.8 LG Energy Solution Ltd.

- 6.4.9 Panasonic Holdings Corporation

- 6.4.10 Primearth EV Energy Co. Ltd.

- 6.4.11 Samsung SDI Co. Ltd.

- 6.4.12 SK Innovation Co. Ltd.

- 6.4.13 SVOLT Energy Technology Co. Ltd. (SVOLT)

- 6.4.14 TOSHIBA Corp.

7 KEY STRATEGIC QUESTIONS FOR EV BATTERY PACK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms