|

시장보고서

상품코드

1740892

누수 감지 시스템 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Water Leak Detector Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

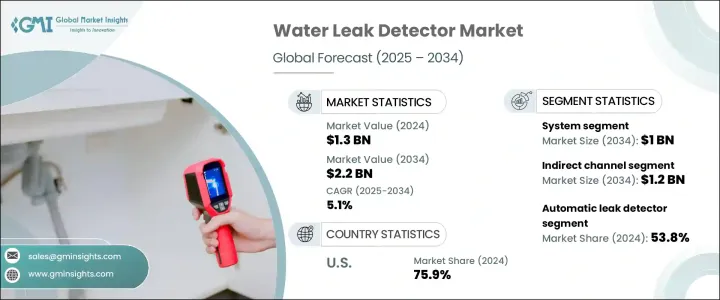

세계의 누수 감지 시스템 시장은 2024년에 13억 달러로 평가되었으며 CAGR 5.1%를 나타내 2034년에는 22억 달러에 이를 것으로 추정됩니다.

누수 감지 기술은 누수를 조기에 발견하고 적시에 수리를 가능하게 함으로써 물 손실을 최소화하는데 점점 더 중요한 역할을 하고 있습니다. 이와 같은 진보로 절수전략의 효율이 대폭 향상되고 있습니다.

이 문제의 가장 큰 요인 중 하나는 주택, 상업, 산업용 물 인프라에서의 시스템 누수이며, 매년 많은 양의 물 손실로 이어지고 있습니다. 회복이 불가능해지기 전에 시스템의 모니터링, 제어, 수리를 용이하게 함으로써 물관리에 적극적인 접근을 제공합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 13억 달러 |

| 예측 금액 | 22억 달러 |

| CAGR | 5.1% |

제공 제품의 관점에서 시장은 솔루션과 시스템으로 분류됩니다. 시스템 부문은 2024년에 5억 달러의 매출을 올려 지배적인 세력으로 부상했고 2034년에는 10억 달러에 이를 전망입니다. 이러한 시스템은 특히 서비스 지향 모델과 비교하여 설치 및 유지 보수가 쉽고 전반적으로 사용자 친화적인 운영이 가능하기 때문에 지원을 수집합니다. 또한 실시간 인사이트를 제공하는 스마트하고 연결된 기술에 대한 지원도 높아지고 있습니다. 더 많은 소비자가 지능형 시스템을 선택하게 되어 IoT 기반 누수 감지 시스템가 표준화되고 있습니다. 이 제품은 적시 경고 및 자동 응답을 제공하여 사용자가 물 손실과 관련 비용을 최소화하는 데 도움이 됩니다. 합리적인 가격, 향상된 정확성 및 연결성의 향상된 조합으로 인해 주도적 지위가 확고해졌습니다. 소비자는 이러한 시스템이 제공하는 편의성, 사용자 정의 및 최신 기능을 높이 평가합니다.

유통면에서는 간접 루트가 2024년의 매출 점유율 55.4%로 시장을 리드했고, 2034년에는 12억 달러에 이를 것으로 예상되고 있습니다. 누수 감지 제품을 배관이나 급수 시스템 서비스 등의 부가 서비스와 조합하여 그 매력을 높이고 판매를 촉진합니다.

유형별로 누수 감지 시스템는 고정식과 휴대용으로 구분됩니다. 단기간의 사용, 임대 물건, 상설 시스템의 설치가 현실적이지 않은 장소 등에 최적입니다. 대부분은 현재, 라이브 모니터링이나 모바일 경고등의 스마트 기능을 탑재하고 있습니다. 한편, 고정식 감지 시스템는 지속적인 감시가 불가결한 대규모 상업 및 산업 환경에서 보다 일반적으로 도입되고 있습니다.

북미에서는 미국이 2024년 지역별 시장에서 75.9%의 압도적인 점유율을 차지했습니다. 또한 파이프라인의 노후화 등의 인프라 과제도 수요를 뒷받침하고 있습니다.

업계의 대기업은 강력한 브랜드 존재, 최첨단 기술, 광범위한 유통망을 활용하여 합계로 시장의 30-35%의 점유율을 차지하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 파괴적 혁신

- 향후 전망

- 제조업체

- 유통업체

- 트럼프 정권의 관세 분석

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 영향을 받는 주요 기업

- 전략적 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 영향요인

- 성장 촉진요인

- 물 부족에 대한 우려 증가

- 수자원 보전에의 의식의 고조

- 상업 및 산업에서의 채용

- 업계의 잠재적 위험 및 과제

- 높은 초기 투자액

- 신흥 국가에서의 도입은 한정적

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 누수 감지 시스템 시장 추계·예측 : 제공별(2021-2034년)

- 주요 동향

- 솔루션

- 시스템

제6장 누수 감지 시스템 시장 추계·예측 : 유형별(2021-2034년)

- 주요 동향

- 고정식 누설 검출기

- 휴대용 누설 검출기

제7장 누수 감지 시스템 시장 추계·예측 : 기술별(2021-2034년)

- 주요 동향

- 기존

- 스마트

제8장 누수 감지 시스템 시장 추계·예측 : 제품별(2021-2034년)

- 주요 동향

- 수동적 누출

- 능동적 누출

제9장 누수 감지 시스템 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 주택용

- 상업용

- 산업용

제10장 누수 감지 시스템 시장 추계·예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접

- 간접

제11장 누수 감지 시스템 시장 추계·예측 :지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제12장 기업 프로파일

- Amprobe

- Bosch Security Systems

- Emerson Electric

- FIBAR Group

- Grove Leak Detection

- Honeywell International

- Johnson Controls

- Krohne Group

- Leak Detection Systems

- PSI Software AG

- RLE Technologies

- Siemens

- Tait Communication

- Water Hero

- Wagner Meters

The Global Water Leak Detector Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 2.2 billion by 2034. Leak detection technologies play an increasingly vital role in minimizing water loss by identifying leaks early and enabling timely repairs. These systems use advanced tools, including sensor-based solutions, sound detection, and connected devices, to pinpoint hidden or minor leaks that would otherwise go unnoticed. Such advancements are significantly improving the efficiency of water conservation strategies. Water scarcity continues to worsen due to growing urban populations, rapid industrialization, and the impacts of climate change. As a result, addressing water wastage has become a global concern.

One of the most significant contributors to this issue is system leakage in residential, commercial, and industrial water infrastructure, which leads to massive water loss each year. With increasing awareness and urgency around water preservation, the adoption of leak detection technology is gaining momentum across sectors. These solutions offer a proactive approach to water management by making it easier to monitor, control, and repair systems before the damage becomes costly or irreversible. Rising demand for sustainable resource use, tighter regulations, and government initiatives aimed at upgrading aging water systems are further fueling market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 5.1% |

In terms of offerings, the market is categorized into solutions and systems. The systems segment emerged as the dominant force in 2024, generating USD 500 million in revenue and is on track to reach USD 1 billion by 2034. These systems have gained favor due to their ease of installation, maintenance, and overall user-friendly operation, especially compared to service-oriented models. There's also growing traction for smart and connected technologies that offer real-time insights. As more consumers opt for intelligent systems, IoT-based leak detectors are becoming standard. These products provide timely alerts and automatic responses, helping users minimize water loss and associated costs. The combination of affordability, improved precision, and enhanced connectivity has solidified their leading position. The trend toward do-it-yourself installations among homeowners is further accelerating product adoption, with consumers valuing the convenience, customization, and modern features these systems provide.

Distribution-wise, the indirect channel led the market in 2024 with a 55.4% revenue share and is expected to hit USD 1.2 billion by 2034. The indirect route, which includes distributors, resellers, and retailers, has become the go-to strategy for manufacturers looking to expand reach and tap into remote customer bases. These intermediaries often pair leak detection products with additional offerings like plumbing or water system services, enhancing their appeal and driving sales. The availability of products in physical stores and online platforms, as well as faster fulfillment through local inventory hubs, makes this channel highly efficient and accessible for end users.

By type, water leak detectors are segmented into fixed and portable units. In 2024, automatic detectors dominated with a market share of approximately 53.8%. Portable devices are especially favored for their flexibility, cost-effectiveness, and ease of deployment. They are an ideal fit for short-term uses, rented properties, or locations where installing a permanent system is not practical. The rise in smart home adoption and DIY home improvement trends has led to greater interest in portable options, many of which now include smart features like live monitoring and mobile alerts. On the other hand, fixed detectors are more commonly deployed in large-scale commercial or industrial environments where continuous surveillance is essential. However, their higher costs and installation complexities limit their use in smaller or residential setups, which is why portable variants are seeing faster growth in overall market penetration.

In North America, the United States held the lion's share of the regional market in 2024, accounting for 75.9%. This dominance is forecast to continue, supported by a CAGR of 4.9% through 2034. The country's focus on water conservation, regulatory support, and the adoption of high-tech solutions is creating strong momentum in the market. Infrastructure challenges such as aging pipelines are also driving demand, as a significant volume of water is lost daily due to undetected leaks. The widespread adoption of smart sensors and connected devices is enabling more accurate detection and faster response times, making these tools essential for residential, municipal, and commercial water management systems.

Leading players in the industry collectively hold a 30-35% share of the market, leveraging their strong brand presence, cutting-edge technology, and expansive distribution networks. These companies continue to drive growth through innovation and strategic partnerships while aligning with global sustainability goals and addressing the rising demand for water-efficient technologies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump Administration Tariffs Analysis

- 3.2.1 Impact on Trade

- 3.2.1.1 Trade Volume Disruptions

- 3.2.1.2 Retaliatory Measures

- 3.2.2 Impact on the Industry

- 3.2.2.1 Supply-Side Impact (Raw Materials)

- 3.2.2.2 Price Volatility in Key Materials

- 3.2.2.3 Supply Chain Restructuring

- 3.2.2.4 Production Cost Implications

- 3.2.2.5 Demand-Side Impact (Selling Price)

- 3.2.2.6 Price Transmission to End Markets

- 3.2.2.7 Market Share Dynamics

- 3.2.2.8 Consumer Response Patterns

- 3.2.3 Key Companies Impacted

- 3.2.4 Strategic Industry Responses

- 3.2.4.1 Supply Chain Reconfiguration

- 3.2.4.2 Pricing and Product Strategies

- 3.2.4.3 Policy Engagement

- 3.2.5 Outlook and Future Considerations

- 3.2.1 Impact on Trade

- 3.3 Impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Growing concerns about water scarcity

- 3.3.1.2 Rising Awareness of Water Conservation

- 3.3.1.3 Commercial and Industrial Adoption

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 High Initial Investment

- 3.3.2.2 Limited Adoption in Developing Countries

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Water Leak Detector Market Estimates & Forecast, By Offering, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Solution

- 5.3 System

Chapter 6 Water Leak Detector Market Estimates & Forecast, By Type, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Fixed leak detector

- 6.3 Portable leak detector

Chapter 7 Water Leak Detector Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Conventional

- 7.3 Smart

Chapter 8 Water Leak Detector Market Estimates & Forecast, By Product, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Passive leak

- 8.3 Active leak

Chapter 9 Water Leak Detector Market Estimates & Forecast, By Application 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.4 Industrial

Chapter 10 Water Leak Detector Market Estimates & Forecast, By Distribution Channel 2021-2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Water Leak Detector Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 United States

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 United kingdom

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 Middle East & Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 United Arab Emirates

Chapter 12 Company Profiles

- 12.1 Amprobe

- 12.2 Bosch Security Systems

- 12.3 Emerson Electric

- 12.4 FIBAR Group

- 12.5 Grove Leak Detection

- 12.6 Honeywell International

- 12.7 Johnson Controls

- 12.8 Krohne Group

- 12.9 Leak Detection Systems

- 12.10 PSI Software AG

- 12.11 RLE Technologies

- 12.12 Siemens

- 12.13 Tait Communication

- 12.14 Water Hero

- 12.15 Wagner Meters