|

시장보고서

상품코드

1750587

백업 왕복 발전 엔진 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Backup Reciprocating Power Generating Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

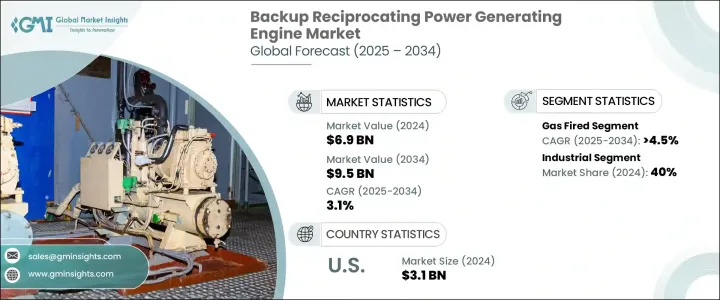

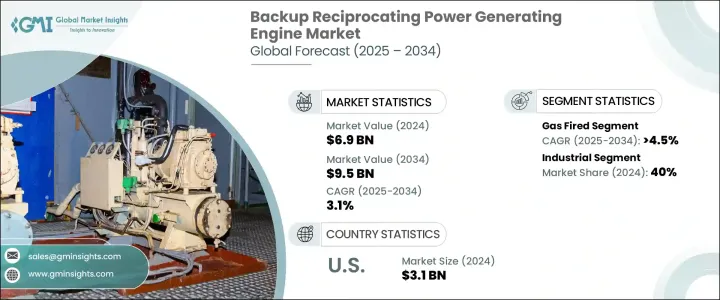

세계의 백업 왕복 발전 엔진 시장은 2024년에는 69억 달러로 평가되었고, 신뢰성 있는 백업 전원 시스템 수요에 견인되어, 2034년에는 95억 달러에 이를 것으로 추정되며, CAGR 3.1%로 성장할 전망입니다.

분산형 에너지 생산으로의 전환, 특히 원격 지역에서의 전환은 시장을 더욱 확대시키고 있습니다. 이러한 엔진은 전기 공급 중단이 자주 발생하는 지역, 특히 고립되거나 취약한 지역에서 안정적인 전력 공급을 보장하는 데 필수적입니다. 비상 전력 공급 외에도, 백업 회전식 엔진은 전력 신뢰성이 중요한 산업에서 운영 연속성을 유지하는 데 점점 더 중요해지고 있습니다.

개발도상국의 전기 공급 변동성 증가와 재난 취약 지역에서의 에너지 수요 증가는 백업 전력 시스템 채택을 촉진할 것으로 예상됩니다. 또한 IoT(사물인터넷)를 탑재한 엔진의 통합은 시스템 지능을 향상시키고 예측 유지보수를 가능하게 하여 핵심 및 원격 응용 프로그램의 성능을 개선하고 있습니다. 엄격한 배출 규제로 인해 산업 부문에서 대기 전력 수요가 증가하고 있는 점도 시장 확대에 기여하고 있습니다. 수입 부품에 대한 관세 등 규제 환경의 변화는 국제 무역에 영향을 미치고 백업 발전 엔진의 생산 비용을 증가시킬 수 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 69억 달러 |

| 예측 금액 | 95억 달러 |

| CAGR | 3.1% |

가스 연소식 백업 피스톤식 발전 엔진 시장은 엄격한 환경 규제와 천연 가스의 접근성 향상으로 인해 2034년까지 4.5%의 견고한 연평균 성장률(CAGR)로 성장할 것으로 예상됩니다. 이는 전통적인 발전 방법에 비해 탄소 배출량을 줄이면서 신뢰할 수 있는 전력 공급을 유지하려는 산업계의 수요를 충족시키기 때문입니다. 이 엔진은 전통적인 화석 연료 발전 엔진보다 높은 효율성과 낮은 배출량을 갖추고 있어, 탄소 배출량을 줄이면서 안정적인 전력 공급을 유지하려는 산업계에서 선호되는 선택지로 부상하고 있습니다.

또한, 복합 열전력(CHP) 시스템은 2034년까지 4.5%의 CAGR로 눈에 띄는 성장을 기록할 것으로 예상됩니다. 에너지 효율적인 솔루션에 대한 수요가 증가하고 기업들이 연료 소비와 운영 비용을 절감하기 위해 노력하고 있는 것이 이러한 추세의 주요 요인입니다. CHP 시스템은 전기를 생산하는 동시에 폐열을 회수하여 난방에 사용할 수 있는 능력으로 특히 높은 평가를 받고 있으며, 이를 통해 에너지 효율을 개선하고 전체 운영 비용을 절감할 수 있습니다.

미국의 백업 왕복 발전 엔진 시장은 신뢰할 수 있는 전기에 대한 수요가 증가함에 따라 2024년에 31억 달러로 평가되었습니다. 이 급증은 국가의 노후화된 전력망 인프라 현대화와 정전 시 지속적인 전력 공급을 위한 백업 시스템의 필요성에 주로 기인합니다. 또한 다양한 산업 분야에서 에너지 효율적인 기술의 채택이 증가하고 상업 및 산업 활동이 확대됨에 따라 시장 성장이 더욱 가속화될 것으로 예상됩니다.

세계의 백업 왕복 발전 엔진 시장의 주요 기업들은 제품 혁신과 시장 확장을 통해 경쟁력을 강화하기 위해 노력하고 있습니다. 롤스로이스(Rolls-Royce), MAN 에너지 솔루션(MAN Energy Solutions), 워츠일라(Wartsila) 등 기업들은 엔진 성능과 연료 효율성을 개선하기 위해 연구 개발에 투자하고 있습니다. 전략적 파트너십과 인수합병을 통해 신규 지역 시장 진출과 제품 포트폴리오 강화에도 힘쓰고 있습니다. 또한 기업들은 엄격한 배출 기준을 충족하는 엔진을 개발해 지속 가능성을 강조하고 있습니다. 이러한 전략은 다양한 산업 분야에서 신뢰성 있고 환경 친화적인 전력 솔루션에 대한 수요 증가를 충족시키기 위해 채택되고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 트럼프 정권의 관세 분석

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원자재)

- 주요 원자재의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원자재)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 전략적 전망

- 혁신과 지속가능성의 정세

제5장 시장 규모와 예측 : 연료 유형별(2021-2034년)

- 주요 동향

- 가스 화력

- 디젤 연료

- 이중 연료

- 기타

제6장 시장 규모와 예측 : 정격 출력별(2021-2034년)

- 주요 동향

- 0.5-1MW

- 1-2MW 이상

- 2-3.5MW 이상

- 3.5-5MW 이상

- 5-7.5MW 이상

- 7.5MW 이상

제7장 시장 규모와 예측 : 용도별(2021-2034년)

- 주요 동향

- 산업

- CHP

- 에너지 및 유틸리티

- 매립지와 바이오가스

- 기타

제8장 시장 규모와 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 프랑스

- 독일

- 러시아

- 이탈리아

- 스페인

- 네덜란드

- 덴마크

- 노르웨이

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 태국

- 싱가포르

- 인도네시아

- 말레이시아

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 카타르

- 오만

- 쿠웨이트

- 이란

- 이집트

- 튀르키예

- 요르단

- 남아프리카

- 라틴아메리카

- 브라질

- 아르헨티나

- 칠레

- 페루

제9장 기업 프로파일

- AB Volvo Penta

- Atlas Copco

- Caterpillar

- Clarke Energy

- GE Vernova

- HIMOINSA

- Kirloskar

- MAN Energy Solutions

- Mitsubishi Heavy Industries

- Motorenfabrik Hatz

- Rehlko

- Rolls-Royce

- Scania

- Wartsila

- Yamaha Motor

- Yuchai International

The Global Backup Reciprocating Power Generating Engine Market was valued at USD 6.9 billion in 2024 and is estimated to grow at a CAGR of 3.1% to reach USD 9.5 billion by 2034, driven by the demand for reliable backup power systems. The shift toward decentralized energy generation, particularly in remote areas, is further expanding the market. These engines are vital for ensuring a consistent power supply in areas prone to electrical disruptions, especially in isolated or vulnerable locations. In addition to providing emergency power, backup reciprocating engines are becoming increasingly important for maintaining operational continuity in industries where power reliability is critical.

The growing volatility of electricity supply in developing economies and the increasing need for energy in disaster-prone regions are expected to fuel the adoption of backup power systems. Furthermore, the integration of Internet of Things (IoT)-enabled engines is enhancing system intelligence and facilitating predictive maintenance, thus improving the performance of critical and remote applications. Stricter emission regulations and the rising demand for standby power in industrial sectors also contribute to market expansion. The evolving regulatory landscape, including tariffs on imported parts, may impact international trade and increase production costs for backup power-generating engines.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.9 Billion |

| Forecast Value | $9.5 Billion |

| CAGR | 3.1% |

The gas-fired backup reciprocating power generating engine market is projected to grow at a robust CAGR of 4.5% through 2034, driven by stricter environmental regulations and the increasing affordability of natural gas, making it a viable and sustainable alternative to traditional power generation methods. These engines offer a compelling advantage due to their higher efficiency and lower emissions compared to conventional fossil-fuel-powered generators, making them a preferred choice for industries looking to reduce their carbon footprint while maintaining a reliable power supply.

In addition to this, Combined Heat and Power (CHP) systems are expected to see notable growth, with an anticipated CAGR of 4.5% through 2034. The rising demand for energy-efficient solutions and the push for businesses to lower their fuel consumption and operating costs are key factors contributing to this trend. CHP systems are particularly valued for their ability to simultaneously generate electricity and capture waste heat for use in heating, thereby improving energy efficiency and reducing overall operational costs.

United States Backup Reciprocating Power Generating Engine Market was valued at USD 3.1 billion in 2024, reflecting the increasing demand for dependable electricity. This surge is largely attributed to the modernization of the nation's aging grid infrastructure and the need for backup systems to ensure continuous power during outages. Additionally, the growing adoption of energy-efficient technologies across various sectors, coupled with the expansion of commercial and industrial activities, is expected to drive further growth in the market.

Key players in the Global Backup Reciprocating Power Generating Engine Market are focusing on product innovation and market expansion to strengthen their positions. Companies like Rolls-Royce, MAN Energy Solutions, and Wartsila are increasingly investing in research and development to improve engine performance and fuel efficiency. Strategic partnerships and acquisitions are also being utilized to enter new regional markets and enhance product offerings. Additionally, firms are focusing on sustainability by developing engines that comply with stringent emission standards. These strategies are being adopted to meet the growing demand for reliable, environmentally friendly power solutions across various industries.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Fuel Type, 2021 - 2034 (USD Million, MW & Units)

- 5.1 Key trends

- 5.2 Gas-fired

- 5.3 Diesel-fired

- 5.4 Dual fuel

- 5.5 Others

Chapter 6 Market Size and Forecast, By Rated Power, 2021 - 2034 (USD Million, MW & Units)

- 6.1 Key trends

- 6.2 0.5 MW - 1 MW

- 6.3 > 1 MW - 2 MW

- 6.4 > 2 MW - 3.5 MW

- 6.5 > 3.5 MW - 5 MW

- 6.6 > 5 MW - 7.5 MW

- 6.7 > 7.5 MW

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Million, MW & Units)

- 7.1 Key trends

- 7.2 Industrial

- 7.3 CHP

- 7.4 Energy & utility

- 7.5 Landfill & biogas

- 7.6 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million, MW & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Russia

- 8.3.5 Italy

- 8.3.6 Spain

- 8.3.7 Netherlands

- 8.3.8 Denmark

- 8.3.9 Norway

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Thailand

- 8.4.7 Singapore

- 8.4.8 Indonesia

- 8.4.9 Malaysia

- 8.5 Middle East & Africa

- 8.5.1 UAE

- 8.5.2 Saudi Arabia

- 8.5.3 Qatar

- 8.5.4 Oman

- 8.5.5 Kuwait

- 8.5.6 Iran

- 8.5.7 Egypt

- 8.5.8 Turkey

- 8.5.9 Jordan

- 8.5.10 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

- 8.6.4 Peru

Chapter 9 Company Profiles

- 9.1 AB Volvo Penta

- 9.2 Atlas Copco

- 9.3 Caterpillar

- 9.4 Clarke Energy

- 9.5 GE Vernova

- 9.6 HIMOINSA

- 9.7 Kirloskar

- 9.8 MAN Energy Solutions

- 9.9 Mitsubishi Heavy Industries

- 9.10 Motorenfabrik Hatz

- 9.11 Rehlko

- 9.12 Rolls-Royce

- 9.13 Scania

- 9.14 Wartsilä

- 9.15 Yamaha Motor

- 9.16 Yuchai International