|

시장보고서

상품코드

1687308

디젤 엔진 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Diesel Power Engine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

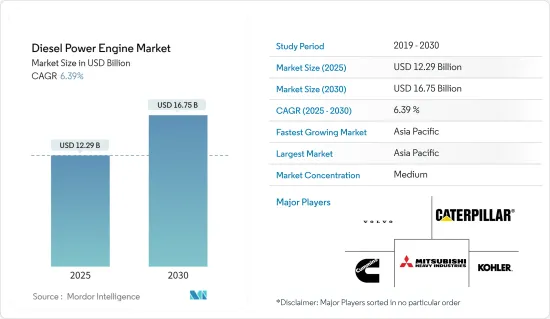

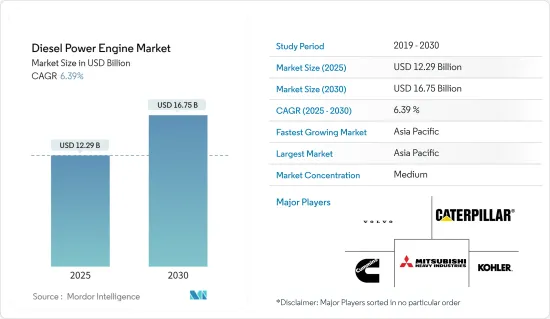

디젤 엔진 시장 규모는 2025년에 122억 9,000만 달러, 2030년에는 167억 5,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2025-2030년)의 CAGR은 6.39%를 나타낼 전망입니다.

주요 하이라이트

- 중기적으로는 산업 부문 수요 증가와 정전 증가 등의 요인이 디젤 발전기 수요를 증가시켜 디젤 엔진 시장을 견인하고 있습니다.

- 한편, 천연가스가 풍부하고 환경친화적이기 때문에 다양한 최종사용자 산업에서 디젤 엔진의 대체로 천연 가스엔진으로의 이행이 진행되고 있으며, 예측기간 중에는 디젤 엔진 시장의 성장을 억제할 것으로 예상됩니다.

- 그럼에도 불구하고 하이브리드 파워 디젤 발전기의 인기가 높아지고 있기 때문에 디젤 엔진 시장의 기업에게는 향후 몇 년동안 엄청난 기회를 가져올 것입니다.

- 아시아태평양은 가장 크고 가장 급성장하는 시장이 될 것으로 예상되며, 대부분 수요는 인도와 중국과 같은 국가에서 발생할 것입니다.

디젤 엔진 시장 동향

시장을 독점하는 산업용 부문

- 디젤 발전은 산업 부문에 가장 적합한 대기 전원입니다. 일반적으로 산업 부문은 사업 운영을 위해 많은 전력을 소비합니다. 디젤 엔진은 신뢰성이 높고 전력 공급의 질을 높입니다.

- 전력 수요는 세계에서 증가하고 있습니다. 급속한 산업 확대와 상업 인프라 개발로 디젤 엔진의 사용이 증가하고 있습니다. 디젤 엔진에서 발전하는 전력에 크게 의존하는 중요한 산업은 건설 부문, 제조업, 의료, 석유 및 가스, 통신, 데이터센터 등입니다.

- 디젤 발전기에는 전류를 모니터링하는 고급 기술이 탑재되어 있으며, 전력에 왜곡이나 장애가 발생하면 자동으로 시동하고, 전력이 회복되면 스위치 오프 모드로 돌아갑니다.

- 디젤 엔진은 휘발율이 낮기 때문에 광업 분야에서 최적의 선택입니다. 특히 광업 분야에서는 중공업에 완벽한 전원 공급과 백업이 필요합니다. 따라서 광업은 내구성이 뛰어난 디젤 엔진에 의존합니다. 헬스케어 분야에서는 산소흡입기, 주입펌프, 심전도장치, 제세동기 등의 정밀기기를 환자의 치료에 사용하고 있습니다. 중단을 피하기 위해 고품질의 전력 공급이 필요합니다. 디젤 엔진은 병원에 가장 신뢰할 수 있는 백업 전원이며, 중단 없는 전력을 공급할 수 있습니다.

- 건설 분야에서는 정전으로 인해 프로젝트가 정체되는 경우가 많았습니다. 정전이 계속되면 프로젝트 수행이 지연되고 경제적 손실로 이어집니다. 건설 현장의 안전과 전력 공급을 향상시키기 위해 디젤 엔진이 필요합니다.

- 제조업의 정전은 소량 생산으로 이어져 저수준의 제품을 제공하게 됩니다. 제조 부문에서 정전이 발생하면 일반적으로 모든 공정에 영향을 미칩니다. 따라서 생산 부서는 이러한 장애를 피하기 위해 최적의 전원으로 작동하는 디젤 엔진에 의존합니다.

- 또한 철강산업에서는 전력 수요와 전력정지시 백업 전원으로 디젤파워 엔진을 사용하고 있습니다. 세계철강협회에 따르면 2022년 12월 현재 조강 생산량에서는 중국이 세계 선두로 전년대비 10% 감소한 7,790만 톤을 생산했습니다. 인도, 일본, 미국, 러시아는 크게 뒤쳐지고 있습니다.

- 따라서 위의 요인들로부터 예측 기간 동안 디젤 엔진 시장은 산업 부문이 지배할 것으로 예상됩니다.

아시아태평양이 시장을 독점

- 평균 에너지 소비율과 GDP 성장률이 크게 증가함에 따라 아시아태평양의 인프라 개척과 전력 수요 증가가 디젤 엔진 시장을 촉진할 것으로 예상됩니다.

- 중국은 인프라 프로젝트 증가, 전력 수급 격차 확대, 전국 제조 시설 확대, 상업 사무실 증가로 아시아태평양 디젤 발전기 시장을 선도하고 있습니다.

- 세계 최대급의 중국 건설 업계는 지난 수십년 동안 현저한 성장을 이루었습니다. 중국의 급속한 산업화는 주택, 상업 및 인프라 건설을 포함한 건설 활동의 급증으로 이어졌습니다. 새로운 프로젝트가 추진됨에 따라 중국 경제는 COVID-19 팬데믹의 영향으로부터 회복하기 시작했습니다.

- 2023년 4월 중국 정부는 지역 경제가 팬데믹으로부터 회복할 수 있도록 지원하기 위해 대규모 건설 및 인프라 프로젝트에 대한 지출을 전년 대비 1조 8,000억 달러 증가할 것이라고 발표했습니다. 건설 활동을 확대하려면 디젤 엔진이 장착된 기계가 필요하며, 이는 시장 성장을 가속할 것으로 예상됩니다.

- 인도 정부는 개방적인 FDI 기준, 스마트 시티 미션, 인프라 부문에 대한 많은 예산 배분 등 중점적인 정책을 통해 인프라와 건설 서비스 개발에 주력하고 있습니다. 2023년 1월, 정부 및 건설 산업 개발 평의회(CIDC)는 국내에 21개의 그린필드 공항 개발을 승인했습니다. 건설 부문이 성장함에 따라 백업용 디젤 발전기가 필요하고 시장 개척의 길이 열립니다.

- 스마트시티 미션하에 2022년 11월 현재 PMAY-U 미션 하에서 1,200만호 이상의 주택이 허가되어 그 중 640만호 이상이 완성되었습니다. 나머지는 다양한 건설 단계에 있습니다. 2024년 현재 AMRUT 2.0 미션 아래, 수역 회춘, 상수도, 하수도, 공원 및 녹지 개발 등 8억 5,512만 달러 상당의 1,174건의 프로젝트가 진행 중입니다. 인도의 많은 주택에는 정전 시 전기를 공급하기 위한 디젤 발전기(DG)가 설치되어 있습니다. 따라서 예측 기간 동안 디젤 엔진 수요가 증가할 것으로 예상됩니다.

- 또한, 급성장하는 제조업에 의한 에너지 수요 증가는 아시아태평양의 발전기 사업에 큰 추진력을 줄 것으로 예상됩니다. 그 결과 예측 기간 동안 아시아태평양은 세계 디젤 엔진 시장에서 가장 빠른 성장을 이룰 것으로 예상됩니다.

디젤 엔진 산업 개요

디젤 엔진 시장은 반 세분화되어 있습니다. 이 시장의 주요 기업(순부동)에는 Caterpillar Inc., Cummins Inc., Kohler Co., Volvo AB, Mitsubishi Heavy Industries, Inc. 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 및 지원

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

- 소개

- 2029년까지 시장 규모와 수요 예측

- 최근 동향과 개발

- 정부의 규제와 정책

- 시장 역학

- 성장 촉진요인

- 산업 부문에서의 수요 증가

- 정전 증가로 인한 디젤 발전기 수요 증가

- 억제요인

- 보다 깨끗한 에너지 자원으로의 변화 증가

- 성장 촉진요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 세분화

- 최종 사용자별

- 산업

- 상업

- 주택

- 용도별

- 대기

- 프라임

- 피크 컷

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 영국

- 프랑스

- 독일

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- ASEAN 국가

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 나이지리아

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- Caterpillar Inc.

- Cummins Inc.

- Kohler Co

- Volvo AB

- Mitsubishi Heavy Industries Ltd

- Wartsila Oyj Abp

- Hyundai Heavy Industries Co.Ltd

- Man SE

- Rolls-Royce Holding PLC

- YANMAR HOLDINGS Co.Ltd

- Market Ranking/Share(%) Analysis

제7장 시장 기회와 앞으로의 동향

- 하이브리드식 디젤 발전기의 인기가 높아져

The Diesel Power Engine Market size is estimated at USD 12.29 billion in 2025, and is expected to reach USD 16.75 billion by 2030, at a CAGR of 6.39% during the forecast period (2025-2030).

Key Highlights

- Over the medium period, factors such as the increasing demand from the industrial sector and rising power outages have increased the demand for diesel generators, thereby driving the diesel power engine market.

- On the other hand, the abundance of natural gas, coupled with its environmental soundness, has led to an increasing shift toward natural gas engines as an alternative to diesel engines in various end-user industries and is expected to restrain the growth of the diesel engine market during the forecast period.

- Nevertheless, the increasing popularity of hybrid power diesel generators presents immense opportunities for the diesel power engine market players in the coming years.

- Asia-Pacific is expected to be the largest and fastest-growing market, with the majority of the demand coming from countries like India and China.

Diesel Power Engine Market Trends

The Industrial Segment to Dominate the Market

- * Diesel power generation is the most appropriate standby source for the industrial sector. Generally, the industrial sector consumes more power for its business operations. A diesel power engine offers better reliability and enhances the quality of the power supply.

- * The demand for electricity is growing worldwide. Rapid industrial expansions and commercial infrastructure development are increasing the utilization of diesel power engines. Significant industries that rely heavily on the power generated from diesel engines are the construction sector, manufacturing, health care, oil and gas, telecommunication and data centers, etc.

- Diesel generators are equipped with advanced technologies for monitoring electric current, which help automatically start when there are power distortions and failures and revert to switch-off mode when the power comes back.

- The diesel engine's low volatility rate makes it the finest option in mining fields. Especially in mining fields, heavy-duty activities need a perfect power source and backup. Hence, mining industries rely on diesel-powered engines for better durability. The healthcare segment uses sensitive equipment such as oxygen ventilators, infusion pumps, ECG machines, and defibrillators to treat patients. There is a need for a quality power supply to avoid interruptions. Diesel power engines are hospitals' most reliable backup power sources for uninterrupted power.

- In the construction sector, projects often stall due to power failures. Constant power interruptions result in delayed project execution, which leads to financial loss. There is a need for a diesel power engine to ensure safety and better power supply on construction sites.

- Disruptions of power in the manufacturing industry lead to low-volume production and result in the offering of low-standard products. When a blackout occurs in manufacturing divisions, it generally affects all the processes. Hence, the production units rely on the diesel power engine to avoid such failures, which acts as the best power source.

- The iron and steel industry also uses diesel power engines as backup power in case of power requirements or power shutdown. According to the World Steel Association, as of December 2022, China was the world leader in crude steel production, with 77.9 million metric tonnes produced, a 10% decrease from the previous year. India, Japan, the United States, and Russia trailed far behind.

- Therefore, based on the abovementioned factors, the industrial segment is expected to dominate the diesel power engine market during the forecast period.

Asia-Pacific to Dominate the Market

- The increasing infrastructural developments and electricity demand in Asia-Pacific, with the huge increase in average energy consumption rate and GDP growth rate, are expected to promulgate the diesel power engine market.

- China is the leading diesel generator market in Asia-Pacific owing to increasing infrastructure projects, widening power demand-supply gap, expanding manufacturing facilities across the nation, and rising commercial office spaces.

- The construction industry in China, one of the largest in the world, has experienced significant growth over the last few decades. Rapid industrialization in China has led to a surge in construction activities, including residential, commercial, and infrastructure construction. The Chinese economy is beginning to recover from the effects of the COVID-19 pandemic as new projects are pushed forward.

- In April 2023, the Chinese government announced that it was set to increase its spending on large construction and infrastructure projects by USD 1.8 trillion Y-o-Y to help regional economies recover from the pandemic. The growing construction activities require machinery fitted with diesel engines; this is expected to promote the growth of the market.

- The Indian government has been focusing on developing infrastructure and construction services through focused policies such as open FDI norms, smart city missions, and large budget allocation to the infrastructure sector. In January 2023, the government and the Construction Industry Development Council (CIDC) approved the development of 21 greenfield airports in the country. The growth in the construction sector will, in turn, need diesel generators to power backup, which will create avenues for the development of the market.

- Under the Smart City Mission, as of November 2022, more than 12.0 million houses were sanctioned under the PMAY-U Mission, out of which more than 6.4 million were completed. The rest are in various stages of construction/grounding. As of 2024, 1174 projects worth USD 855.12 million of Water Body Rejuvenation, Water Supply, Sewage & Sewage Management, and Parks & Green Space Development are ongoing under the AMRUT 2.0 mission. Many of the residential societies in India are equipped with diesel generator (DG) sets to supply electricity during power outages. Thus, such commitments are expected to increase the demand for diesel engines during the forecast period.

- Moreover, the growing energy demands of the burgeoning manufacturing industry are expected to provide a huge impetus to the generator business in Asia-Pacific. As a result, Asia-Pacific is expected to witness the fastest growth in the global diesel power engine market during the forecast period.

Diesel Power Engine Industry Overview

The diesel power engine market is semi fragmented. Some of the key players in this market (in no particular order) include Caterpillar Inc., Cummins Inc., Kohler Co., Volvo AB, and Mitsubishi Heavy Industries Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand From Industrial Sector

- 4.5.1.2 Rising Power Outages To Increase The Demand For Diesel Generators

- 4.5.2 Restraints

- 4.5.2.1 Increasing Shift Toward Cleaner Energy Resources

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By End User

- 5.1.1 Industrial

- 5.1.2 Commercial

- 5.1.3 Residential

- 5.2 By Application

- 5.2.1 Standby

- 5.2.2 Prime

- 5.2.3 Peak Shaving

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Spain

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 ASEAN Countries

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Nigeria

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Caterpillar Inc.

- 6.3.2 Cummins Inc.

- 6.3.3 Kohler Co

- 6.3.4 Volvo AB

- 6.3.5 Mitsubishi Heavy Industries Ltd

- 6.3.6 Wartsila Oyj Abp

- 6.3.7 Hyundai Heavy Industries Co. Ltd

- 6.3.8 Man SE

- 6.3.9 Rolls-Royce Holding PLC

- 6.3.10 YANMAR HOLDINGS Co. Ltd

- 6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Popularity Of Hybrid Power Diesel Generators