|

시장보고서

상품코드

1766197

자동차용 레이더 온칩 기술 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Automotive Radar-on-Chip Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

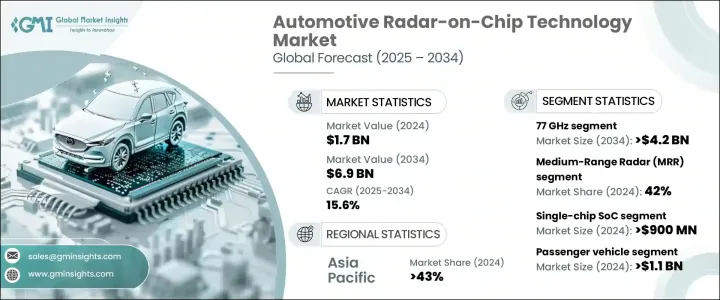

세계의 자동차용 레이더 온칩 기술 시장 규모는 2024년 17억 달러에 달했고, CAGR 15.6%로 성장해 2034년까지 69억 달러에 달할 것으로 예측되고 있습니다.

상대방 상표 제품 제조업체(OEM)가 레벨 2에서 레벨 4 자율성으로의 진화를 추진하고 있는 가운데, 고도로 확장 가능한 지각 시스템에 대한 수요는 증가의 길을 따라가고 있습니다. 레이더 온 칩 기술은 안테나, 송수신기 및 신호 처리 컴포넌트를 단일 칩에 통합하여 기존 레이더 모듈에 비해 전체 시스템 비용을 크게 줄이고 크기를 최소화하고 복잡성을 단순화합니다. 이 통합은 공간과 전력 절약이 중요한 전기자동차와 소형 차량에 특히 유용합니다. 차량 운행 회사와 자동차 산업이 자율 주행 기능의 추진을 강화하는 동안 레이더 센서의 중요성은 차량 부문 전체에서 높아지고 RoC는 전략적 우선 순위로 승격하고 있습니다.

마이크로웨이브 밀리미터파(mmWave) CMOS 및 RF-CMOS 기술의 발전으로 레이더 온칩 시스템의 개발이 가속화되고 있습니다. 이러한 개선으로 76-81GHz 주파수 대역에서 작동하는 모든 레이더 구성 요소를 단일 다이에 통합할 수 있어 크기, 전력 소비 및 비용을 절감할 수 있습니다. RoC 칩의 높은 수율로 경제적인 대량 생산은 자동차 제조에서의 채택을 더욱 향상시킵니다. 또한 최신 RoC 칩에는 인체 지능(AI)과 물체 감지 및 분류를 강화하기 위한 머신 비전 프로세서가 내장되어 있어 적응성을 높이고 제품 수명을 연장하는 소프트웨어 정의로 업데이트 가능한 레이더 시스템을 구현할 수 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 17억 달러 |

| 예측 금액 | 69억 달러 |

| CAGR | 15.6% |

싱글칩 시스템 온칩(SoC) 솔루션이 시장을 선도해 2024년에는 9억 달러를 생산했으며, 이러한 싱글칩 SoC는 RF 트랜시버와 신호 처리 등의 레이더 기능과 로직 회로를 1칩에 통합하여 전력 효율 향상, 제조 비용 절감, 차량 통합의 간소화를 실현합니다. 디지털화에 중점을 둔 이 컴팩트한 설계는 점점 더 중요해지고 있습니다. 맞춤형 ADAS(첨단 운전 지원 시스템)의 고급 컴퓨팅 요구와 중복성을 위해 멀티칩 모듈이 여전히 선호되고 있습니다.

승용차 부문은 2024년 11억 달러로 시장을 독점했습니다. 레이더 온 칩 솔루션은 첨단 안전 기능과 중급 안전 기능의 균형을 비용 효율적으로 실현하는 것으로, 특히 위험 경감이 중요한 세단 및 엔트리 레벨 해치백 차량용입니다.

아시아태평양의 자동차용 레이더 온 칩 기술 시장은 2024년에 43%의 점유율을 획득했습니다. 자율주행이 추진되고 있기 때문에 전기자동차나 인텔리전트차에의 레이더 채용이 가속하고 있습니다. 그리고 전력 소비 감소, 멀티 칩 시스템을 단일 칩 솔루션에 통합하는 데 중점을 둡니다.

자동차용 레이더 온칩 기술 세계 시장의 주요 기업으로는 Valeo, Texas Instruments, Robert Bosch, Infineon Technologies, Continental, Denso Corporation, NXP Semiconductors, ZF Friedrichshafen, Arbe Robotics 등이 있습니다. 시장에서의 존재감을 높이기 위해, 자동차용 레이더 온칩 분야의 각사는 보다 소형의 폼 팩터 내에서의 집적도, 전력 효율, 연산 능력의 강화에 중점을 둔 연구 개발을 우선하고 있습니다. 자동차 OEM 및 기술 기업과의 협업은 진화하는 자율 주행 요구 사항에 맞는 솔루션을 제공합니다. AI 지원 레이더 시스템과 소프트웨어 업데이트 가능한 플랫폼에 대한 전략적 투자는 제품의 적응성과 수명을 향상시킵니다. 칩 수율을 높이고 비용을 절감하기 위한 제조 능력을 확대하는 것은 세계적인 자동차 표준을 준수하는 것처럼 계속 초점을 맞추었습니다. 또한 각사는 파트너십과 합작투자를 활용하여 기술 혁신을 가속화하고 생산 규모를 확대하는 한편 현지 생산 및 판매 네트워크를 통해 신흥 시장을 목표로 하고 있습니다.

목차

제1장 조사 방법

- 시장의 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 지역

- 국가

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 안전규제와 NCAP의 의무

- ADAS와 자율주행 수요 증가

- AI와 센서 퓨전의 통합

- 정부 자금에 의한 모빌리티 프로그램

- 업계의 잠재적 위험 및 과제

- 복잡한 교정과 검증

- 높은 연구개발비와 칩 개발비

- 시장 기회

- 레벨 3 이상의 자율성 채용

- 신흥 시장 진출

- 4D 이미징을 갖춘 차세대 레이더

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 코스트 내역 분석

- 특허 분석

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 삭감 전략

- 생산에 있어서의 에너지 효율

- 친환경적인 노력

- 탄소발자국의 고려

- 소비자 행동 분석

- OEM과 애프터마켓의 취향

- 코스트 퍼포먼스의 결정 요인

- 애프터마켓의 동향 분석

- 레이더 시스템의 유지 보수 및 보증

- 칩 교환 사이클

- Tier 1 모델과 OEM 모델의 비용과 장점

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병인수

- 파트너십 및 협업

- 신제품 발매

- 확장계획과 자금조달

제5장 시장 추계 및 예측 : 주파수 대역별, 2021-2034년

- 주요 동향

- 24GHz

- 77GHz

- 79GHz

제6장 시장 추계 및 예측 : 범위별, 2021-2034년

- 주요 동향

- 단거리 레이더(SRR)

- 중거리 레이더(MRR)

- 장거리 레이더(LRR)

제7장 시장 추계 및 예측 : 기술별, 2021-2034년

- 주요 동향

- 싱글 칩 SoC

- 멀티칩 모듈

- 통합 레이더 어레이

제8장 시장 추계 및 예측 : 차량별, 2021-2034년

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 경형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제9장 시장 추계 및 예측 : 판매 채널별, 2021-2034년

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추계 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 어댑티브 크루즈 컨트롤(ACC)

- 사각지대 감지(BSD)

- 전방 충돌 경보(FCW)

- 자동 긴급 브레이크(AEB)

- 고급 주차 지원

- 자율주행차용 코너 레이더

- 기타

제11장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제12장 기업 프로파일

- Analog Devices

- Aptiv

- Arbe Robotics

- Artsys360

- Autoliv

- Calterah Semiconductor Technology

- Continental

- Delphi Technologies

- Denso

- HELLA GmbH

- Infineon Technologies

- NXP Semiconductors

- Renesas Electronics

- Robert Bosch

- Steradian Semiconductors

- Texas Instruments

- Uhnder

- Valeo

- Veoneer

- ZF Friedrichshafen

The Global Automotive Radar-on-Chip Technology Market was valued at USD 1.7 billion in 2024 and is estimated to grow at a CAGR of 15.6% to reach USD 6.9 billion by 2034. As original equipment manufacturers (OEMs) push advancements from Level 2+ to Level 4 autonomy, the demand for sophisticated and scalable perception systems continues to rise. Radar-on-chip technology integrates antennas, transceivers, and signal processing components onto a single chip, significantly lowering overall system costs, minimizing size, and simplifying complexity compared to traditional radar modules. This integration is particularly beneficial for electric and compact vehicles, where saving space and power is critical. With fleet operators and the automotive industry ramping up their push for autonomous driving capabilities, radar sensors' importance grows across vehicle segments, elevating RoC to a strategic priority.

Advancements in microwave millimeter-wave (mmWave) CMOS and RF-CMOS technologies have accelerated the development of radar-on-chip systems. These improvements allow all radar components operating in the 76 to 81 GHz frequency range to be integrated into a single die, reducing size, power consumption, and costs. Economical mass production of RoC chips with high yields further supports adoption in automotive manufacturing. Moreover, modern RoC chips incorporate artificial intelligence (AI) and machine vision processors for enhanced object detection and classification, resulting in software-defined, updatable radar systems that improve adaptability and extend product life.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 Billion |

| Forecast Value | $6.9 Billion |

| CAGR | 15.6% |

Single-chip system-on-chip (SoC) solutions led the market, generating USD 900 million in 2024. These single-chip SoCs combine radar functions-including RF transceivers and signal processing-with logic circuitry on one chip, enhancing power efficiency, reducing manufacturing costs, and simplifying vehicle integration. This compact design becomes increasingly important as OEMs focus on fleet electrification and digitalization. For advanced computing needs or redundancy in customized advanced driver-assistance systems (ADAS), multi-chip modules remain preferred. Meanwhile, integrated radar arrays are gaining traction in high-definition radar applications.

The passenger vehicle segment dominated the market with USD 1.1 billion in 2024. SUVs are the fastest-growing subcategory within passenger vehicles, driven by consumer preference for larger models that incorporate ADAS features. Radar-on-chip solutions balance advanced and mid-level safety functionalities cost-effectively, especially for sedans and entry-level hatchbacks where risk mitigation is critical.

Asia Pacific Automotive Radar-on-Chip Technology Market captured a 43% share in 2024. Growth here is fueled by strong vehicle production, increasing penetration of ADAS, and robust government initiatives. High manufacturing volumes give regional OEMs advantages in adopting cost-efficient radar technologies. The push toward Level 3+ autonomous driving in countries like China has accelerated radar adoption in electric and intelligent vehicles. National programs support domestic radar-on-chip development through partnerships among industry leaders and tech firms. Japan and South Korea focus on reducing chip size and power consumption, and integrating multi-chip systems into single-chip solutions. Emerging urban air mobility radar SoCs and multi-modal ADAS sensors are being developed and integrated by regional automotive manufacturers.

Key players in the Global Automotive Radar-on-Chip Technology Market include Valeo, Texas Instruments, Robert Bosch, Infineon Technologies, Continental, Denso Corporation, NXP Semiconductors, ZF Friedrichshafen, and Arbe Robotics. To reinforce their market presence, companies in the automotive radar-on-chip space are prioritizing research and development focused on enhancing integration, power efficiency, and computational capabilities within smaller form factors. Collaboration with automotive OEMs and technology firms enables tailored solutions for evolving autonomous driving requirements. Strategic investments in AI-enabled radar systems and software-updatable platforms boost product adaptability and lifespan. Expanding manufacturing capabilities to improve chip yields and reduce costs remains a focus, as does compliance with global automotive standards. Firms are also leveraging partnerships and joint ventures to accelerate innovation and scale production while targeting emerging markets through localized production and distribution networks.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Region

- 1.3.2 Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Frequency band

- 2.2.3 Range

- 2.2.4 Technology

- 2.2.5 Vehicle

- 2.2.6 Sales Channel

- 2.2.7 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Safety regulations and NCAP mandates

- 3.2.1.2 Rising ADAS and autonomous demand

- 3.2.1.3 Integration with AI and sensor fusion

- 3.2.1.4 Government-funded mobility programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex calibration and validation

- 3.2.2.2 High R&D and chip development costs

- 3.2.3 Market opportunities

- 3.2.3.1 Level 3+autonomy adoption

- 3.2.3.2 Emerging markets penetration

- 3.2.3.3 Next-gen radar with 4D imaging

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Consumer behavior analysis

- 3.11.1 OEM vs aftermarket preferences

- 3.11.2 Cost–performance decision factors

- 3.12 Analysis of aftermarket trends

- 3.12.1 Radar system maintenance & warranties

- 3.12.2 Chip replacement cycles

- 3.12.3 Cost vs benefit for Tier 1 vs OEM models

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Frequency Band, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 24 GHz

- 5.3 77 GHz

- 5.4 79 GHz

Chapter 6 Market Estimates & Forecast, By Range, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Short-Range Radar (SRR)

- 6.3 Medium-Range Radar (MRR)

- 6.4 Long-Range Radar (LRR)

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Single-chip SoC

- 7.3 Multi-chip module

- 7.4 Integrated radar arrays

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Passenger vehicle

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUV

- 8.3 Commercial vehicle

- 8.3.1 Light Commercial Vehicle (LCV)

- 8.3.2 Medium Commercial Vehicle (MCV)

- 8.3.3 Heavy Commercial Vehicles (HCV)

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 Adaptive Cruise Control (ACC)

- 10.3 Blind Spot Detection (BSD)

- 10.4 Forward Collision Warning (FCW)

- 10.5 Automatic Emergency Braking (AEB)

- 10.6 Advanced parking assist

- 10.7 Corner radar for autonomous vehicles

- 10.8 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Analog Devices

- 12.2 Aptiv

- 12.3 Arbe Robotics

- 12.4 Artsys360

- 12.5 Autoliv

- 12.6 Calterah Semiconductor Technology

- 12.7 Continental

- 12.8 Delphi Technologies

- 12.9 Denso

- 12.10 HELLA GmbH

- 12.11 Infineon Technologies

- 12.12 NXP Semiconductors

- 12.13 Renesas Electronics

- 12.14 Robert Bosch

- 12.15 Steradian Semiconductors

- 12.16 Texas Instruments

- 12.17 Uhnder

- 12.18 Valeo

- 12.19 Veoneer

- 12.20 ZF Friedrichshafen